UNP - Union Pacific Is Facing Temporary Headwinds

2023-11-21 14:10:51 ET

Summary

- Union Pacific is one of the largest rail transportation companies in the US, with a diversified product mix that helps mitigate risks.

- Concerns about the push towards sustainable energy may pose challenges for Union Pacific in the long term.

- The company has a high debt burden and has been overly enthusiastic about its share buyback program, which may not be sustainable in the long term.

Introduction

Union Pacific ( UNP ) has a rich history, dating back to the 19th century as part of the Pacific Railroad Act signed by President Abraham Lincoln. At that time, the company played a crucial role in the construction of the first transcontinental railroad. And now, Union Pacific has grown to one of the largest rail transportation companies in the United States.

Union Pacific's railways are utilized for transporting various goods, including bulk commodities (grain, coal, and biofuels), industrial goods (industrial products, forest products, petroleum, and metals), as well as premium goods (automotive, domestic intermodal, and international intermodal). Their diversified product mix helps mitigate risks by covering both discretionary and non-discretionary products. Revenue streams from stable commodities like grain, biofuels, forest products, and metals are consistent due to their constant demand. However, revenue from products like automotive tends to be more volatile.

One area of concern is the transportation of fossil fuels. Revenue from coal and renewables is significant ($231 million in 3Q23). In the long term, I anticipate challenges in this sector due to the push towards sustainable energy.

Union Pacific is not unfamiliar to me, as I wrote an article in February of this year expressing my positive sentiments about their shareholder return policy. At that time, I gave a buy rating, partly due to the appealing stock valuation. However, I am now more cautious with my buy rating due to concerns about the balance sheet.

Balancing Efficiency, Sustainability, and the Preservation of History

In my view, railroads are essential for efficiently transporting goods. While comparisons are often drawn between railroads and trucks, I don't foresee a complete overlap. Transportation via railroads is faster and generally more efficient due to the higher volume per transport. However, I do have reservations about using fossil fuels to power locomotives. In the long run, I foresee the energy transition offering a more sustainable alternative. This means Union Pacific will have to make investments to meet this evolving requirement. On the flip side, it would be a pity to retire the current locomotives, which are a beautiful part of American history, in favor of an electric or sustainable alternative. I expect the market for railroad transport to persist, and the shift to sustainable means of transportation will likely take place in the mid to long term. This implies that Union Pacific will need to upgrade its fleet, impacting profits. Fortunately, we are still far from that scenario.

Economic Challenges and Outlook

In earlier years, it was quite common for railroad companies to go bankrupt due to high debts and increased interest rates. Over 37 railroad companies filed for bankruptcy in history; a substantial number. Things have changed now as several smaller railroad companies have joined forces to be financially stronger.

Railroad companies are capital-intensive businesses, and profits depend on various factors such as fuel costs, fleet and track maintenance, and depreciation. These three factors are variable and sometimes challenging to estimate. Their investment decision is based on whether a new (fuel-efficient) locomotive is financially more advantageous than a current one that is less fuel-efficient and requires maintenance. Union Pacific has good control over costs, evident from the high profit margins; the operating margin was over 40% in 2022.

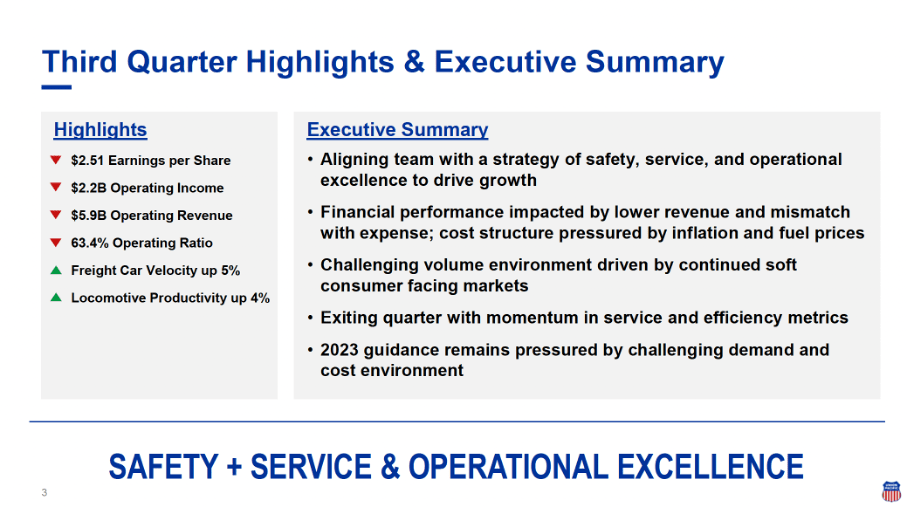

UNP's third quarter highlights and executive summary (3Q23 Investor Presentation)

{kind=link}

Results for the third quarter of 2023 showed a decline in both revenue and earnings. In the same quarter in 2022, earnings per share were $3.05 (down 17%) and revenue was $6.6 billion (down 11%). The revenue decline was due to several weak markets. Bulk segment revenues fell 10% year over year due to reduced coal demand as a result of lower natural gas prices. I find this worrying because, in the long term, the world's coal consumption will decline as several developing economies encourage the use of alternative energy sources. Currently, coal consumption in Asia is still growing, but in the US, coal demand fell by 24% in the first half of the year. Union Pacific's revenues from coal and renewables remain a large portion compared to total revenues (about 4%).

Other business segments showed similar results. In the Premium segment, revenue declined about 12%. This segment consists of automobile transportation. The automotive segment is weak because interest rates have increased significantly this year. Since interest rates are expected to fall only by the end of 2024, I expect the market to be under pressure in the coming year. And I expect a more positive outlook at the beginning of 2025 once interest rates have fallen. For now, I don't see many growth catalysts ahead for Union Pacific. And that's why I'm taking a conservative approach. Let's take a look at its balance sheet.

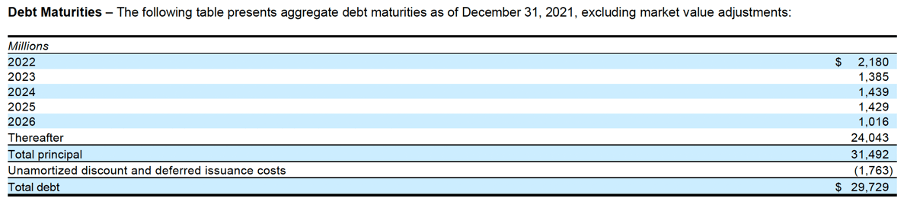

Debt Maturities

The modest outlook for the coming year is a minor setback, but the high profit margins provide ample cushion to absorb setbacks.

What does raise concern for me is the high debt burden. Total debt has increased to $32.8 billion currently, compared to only $22.4 billion in 2018. This poses a problem because the profit has not significantly increased (net income in 2022 = $7 billion, and net income in 2018 = $6 billion). What we do observe is that Union Pacific has engaged in substantial share repurchases. This is beneficial as it is a tax-efficient way to return cash to shareholders. Additionally, a share buyback contributes to an increase in the dividend per share.

However, Union Pacific seems to have been overly enthusiastic about its share buyback program. Dividends + share repurchases consistently exceed both net income and free cash flow. This is not sustainable in the long term. The cash reserve is not growing; in fact, the balance sheet reveals that it has remained approximately the same, but the debts have significantly increased. Hence, it is plausible to assume that the share buybacks and dividends have been partially funded by taking on debts. Now, the debt burden and interest expenses have escalated, which is problematic.

Union Pacific's shareholder return policy (Financial Highlights) (Analyst's Research)

{kind=link}

The debt maturities are primarily in the distant future. In the short term, approximately within the next 5 years, there are no significant repayments scheduled. Our assessment is that Union Pacific will not encounter difficulties in repaying the debts.

Union Pacific's Debt Maturities (2022 Annual Report)

{kind=link}

However, with an interest coverage of only 6.5x, I anticipate a swift halt to the share buybacks. The increased interest rates make financing expensive, and the economic outlook is less optimistic than before. Additionally, other railroad companies are more attractively valued in the market. Currently, I don't see any catalysts that would propel the stock price upward.

Forward P/E Ratio of Railroad Companies (Analyst's Table, Data from Seeking Alpha)

Conclusion

Railroad transportation will be needed for years to efficiently transport goods. Over the years, various small companies have gone bankrupt due to high debts and rising interest rates. The landscape looks much more favorable now as many railroad companies have merged. The third-quarter results were not well-received due to a decline in revenue and volumes across all segments. Because of the high profit margins, I don't see imminent problems. However, I anticipate stagnation in coal transportation in the coming years due to the energy transition. Although the profit margin is substantial, the debt is also significant. Over the past years, we observe that Union Pacific has distributed a significant portion to shareholders, even more than it generated in profit. In the long term, this is not sustainable. With an interest coverage of only 6.5x, I see the end approaching for share buybacks. The stagnant economy, high debt burden, potential reduction in share buybacks, and a relatively rich stock valuation lead me to put this stock on hold. I don't see strong growth catalysts in the short or long term (yet).

For further details see:

Union Pacific Is Facing Temporary Headwinds