UNP - Union Pacific: Is Now The Time To Buy This Awesome Dividend Stock?

2024-01-02 08:00:00 ET

Summary

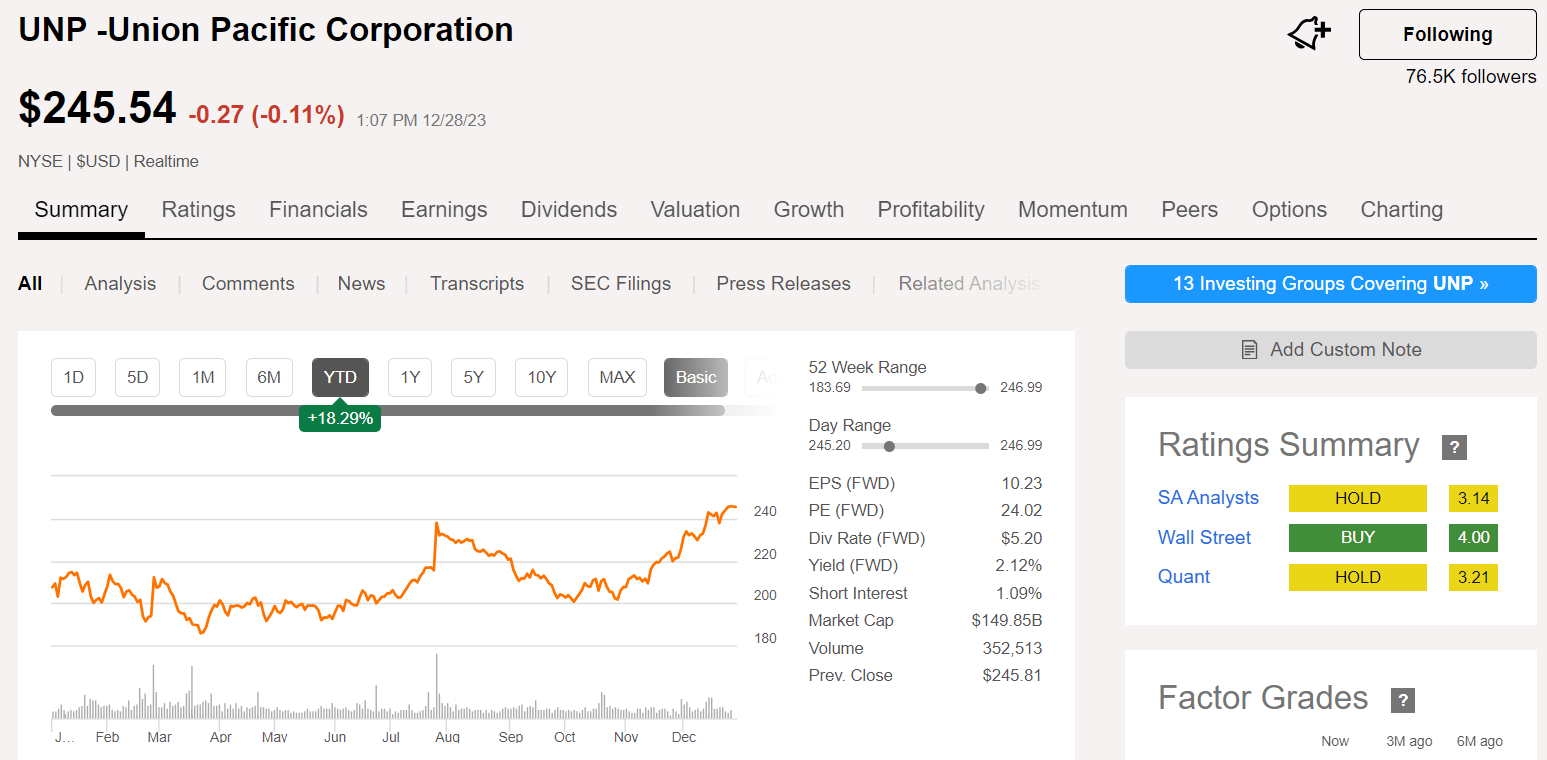

- Alongside the rally in the broader market, shares of Union Pacific have climbed 18% higher in 2023.

- The railroad operator's third quarter results were mixed.

- Union Pacific possesses an A- credit rating from S&P on a stable outlook.

- Shares of the stock appear to be trading at an 8% premium to fair value.

- Union Pacific's total returns could be almost nonexistent through 2025 from the current valuation.

As of Dec. 28, the S&P 500 ( SP500 ) has rallied 25% so far in 2023. With just one trading day left this year, it's fair to say that the index has had quite the bounce-back year from the 19% decline in 2022.

Although I recently noted that a near super-majority of these total returns was driven by the Magnificent 7, there were still plenty of strong performers in 2023.

{kind=link}

Chief among them was the railroad operator, Union Pacific (UNP), which is up 18% year to date. Moderating inflation and a resilient economy have swung overall market sentiment from pessimism to optimism over the last 12 months.

This raises the question that I posed in the headline of this article: Is Union Pacific still a buy after this recent rally? I will initiate coverage by digging into the company's fundamentals and valuation to get an answer to this question.

{kind=link}

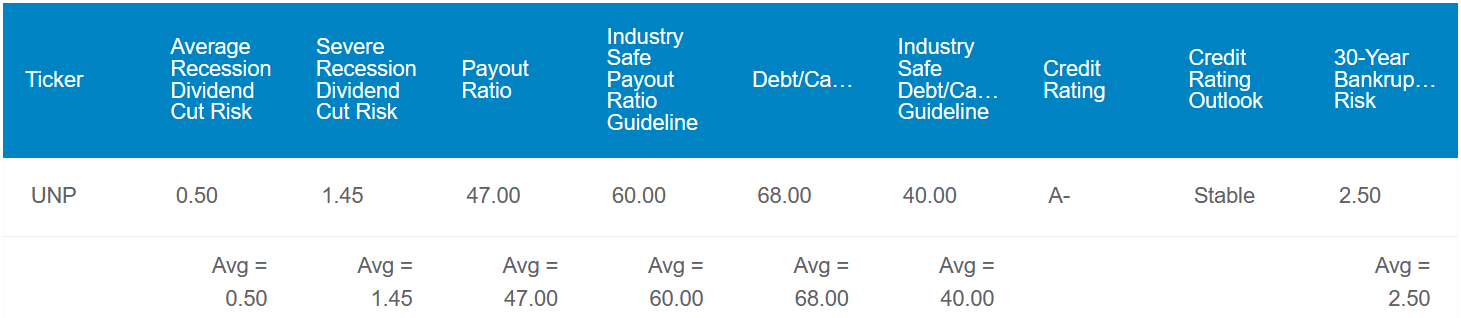

Union Pacific's 2.1% dividend yield is higher than the 1.5% yield of the S&P 500 index. The company also doesn't just offer a greater starting yield relative to the market: Union Pacific's 47% EPS payout ratio is well below the 60% EPS payout ratio that rating agencies view as sustainable for the railroad industry.

The company's 68% debt-to-capital ratio is moderately elevated vs. the 40% debt-to-capital ratio that rating agencies like to see. However, Union Pacific's wide moat and low payout ratio compensate for this fact. Not to mention that, as I'll discuss in the fundamentals section, the company's interest coverage ratio is also fine.

Thus, Union Pacific's debt is rated A- by S&P on a stable outlook. That implies that the risk of the railroad operator going to zero through 2053 is just 2.5%.

This explains why we peg the risk of a dividend cut in the next average recession at just 0.5%. If the next recession were to be severe, this probability would still only be 1.45%.

{kind=link}

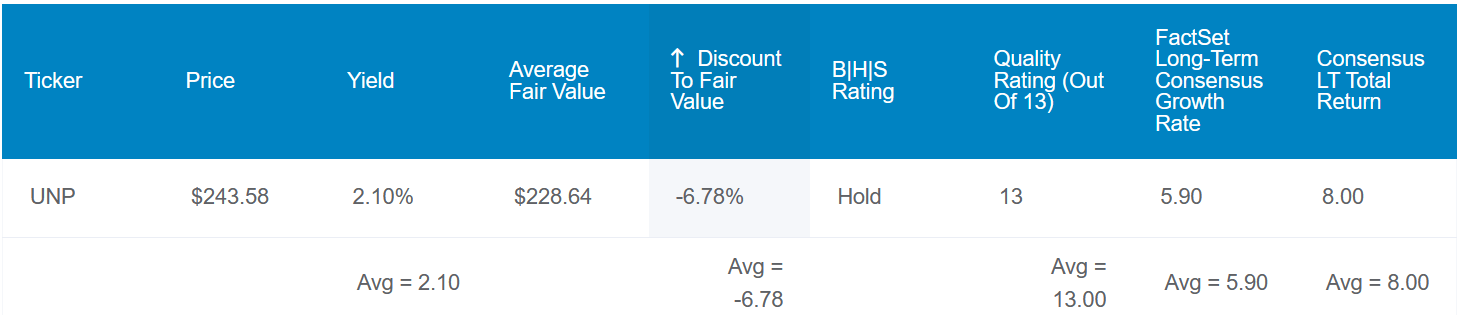

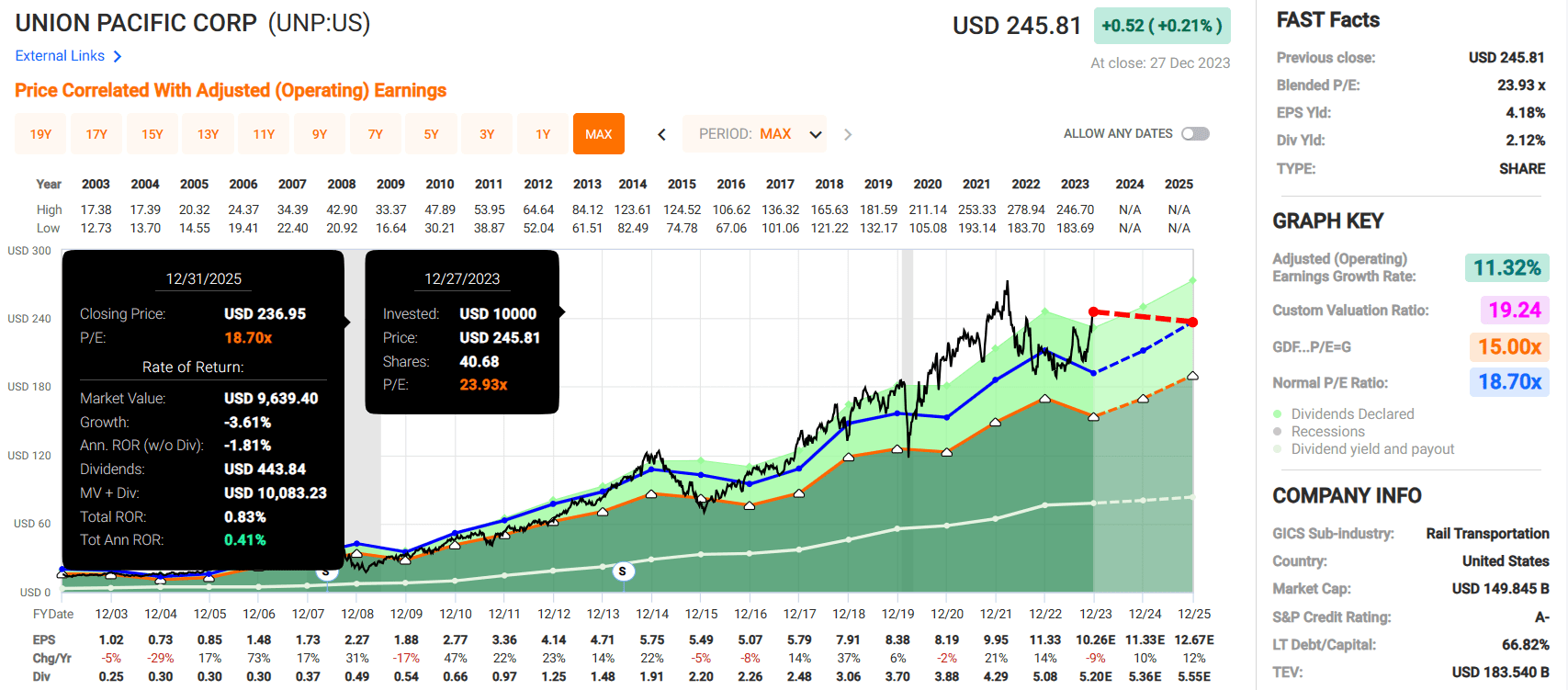

Union Pacific is a fundamentally sound business. However, the recent rally looks to have overextended shares. Our historical valuation metrics such as P/E ratio and dividend yield illustrate Union Pacific to be worth $229 a share. Relative to the current $246 share price, this suggests the stock is priced 8% above fair value.

If Union Pacific were to revert to fair value and match growth expectations, here are the total returns that it could produce for the coming 10 years:

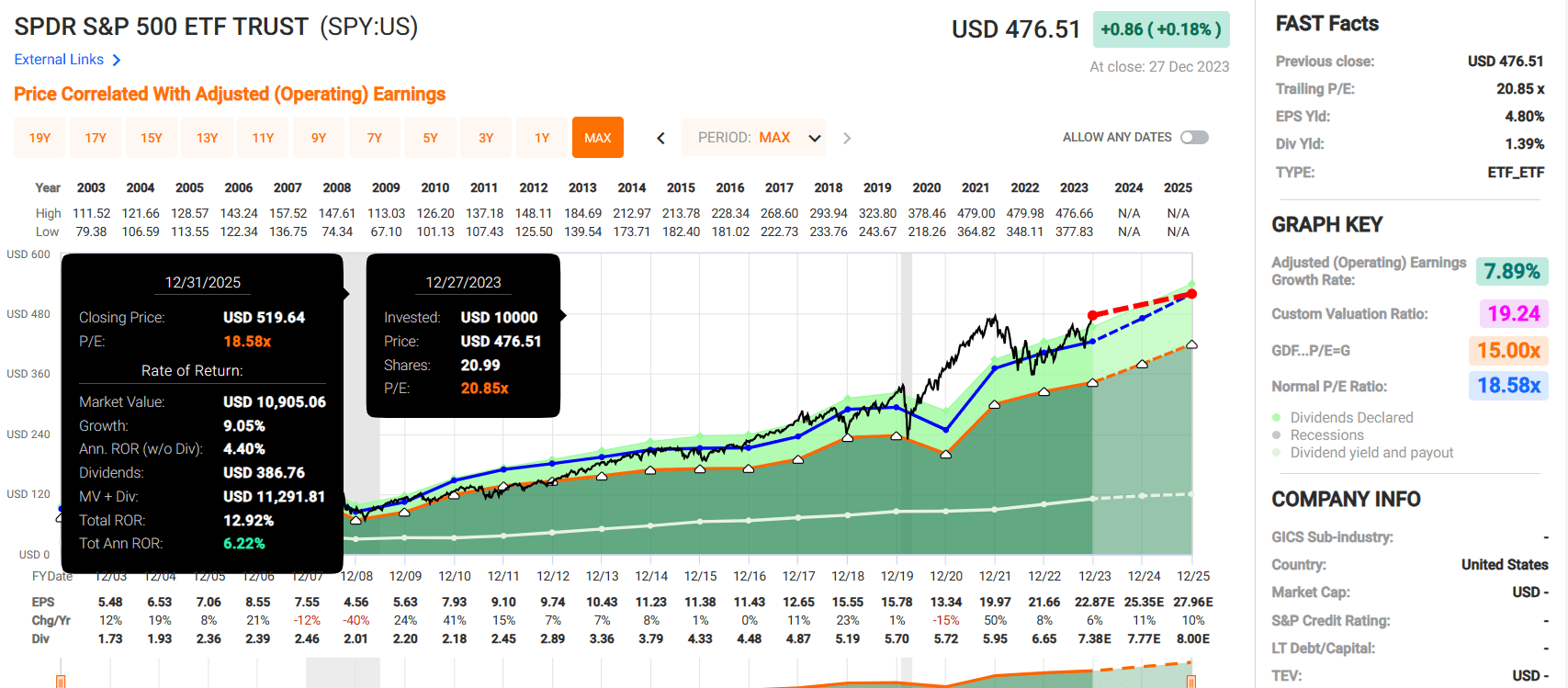

- 2.1% yield + 5.9% FactSet Research annual growth consensus - 0.7% annual valuation multiple contraction = 7.3% annual total return potential or a 102% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

Third Quarter Results Were Okay Given The Operating Environment

{kind=link}

Railroads play an important role in the U.S. economy. As I noted last month when covering the eastern U.S. railroad operator Norfolk Southern ( NSC ), railroads transport almost 30% of the freight in this country.

As the economy grows throughout a full economic cycle, so too should consumption. This should lead to more demand for freight to be transported by railroad operators. That's why I believe that best-in-class railroad companies can grow their revenue and earnings over time.

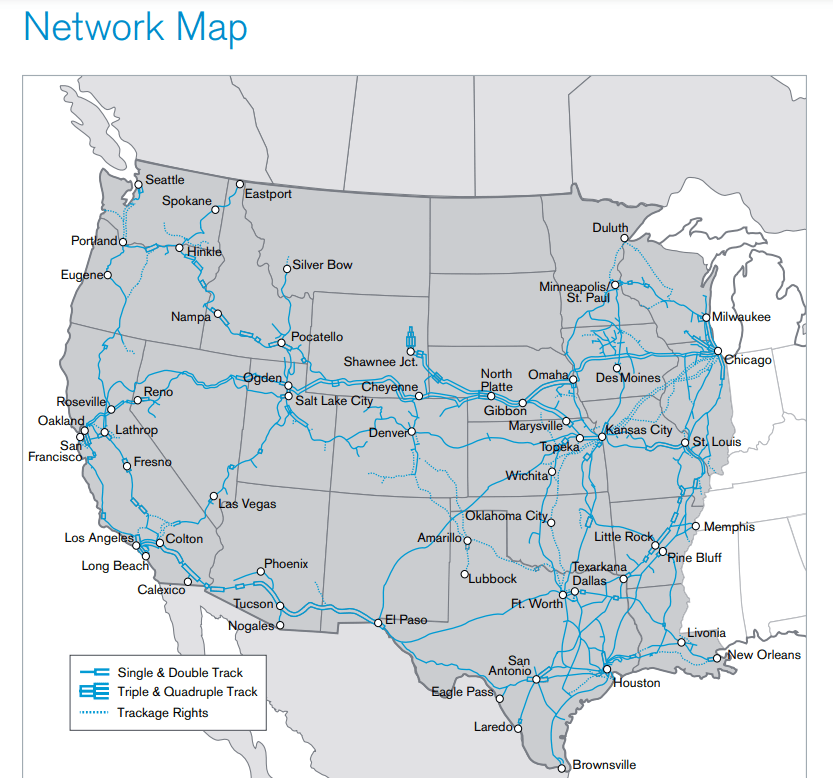

Covering 23 states in the western two-thirds of the U.S., Union Pacific is a leading railroad operator. As of the end of 2022, the company operated more than 56,000 freight cars and 7,000-plus locomotives on more than 32,000 miles of route track.

{kind=link}

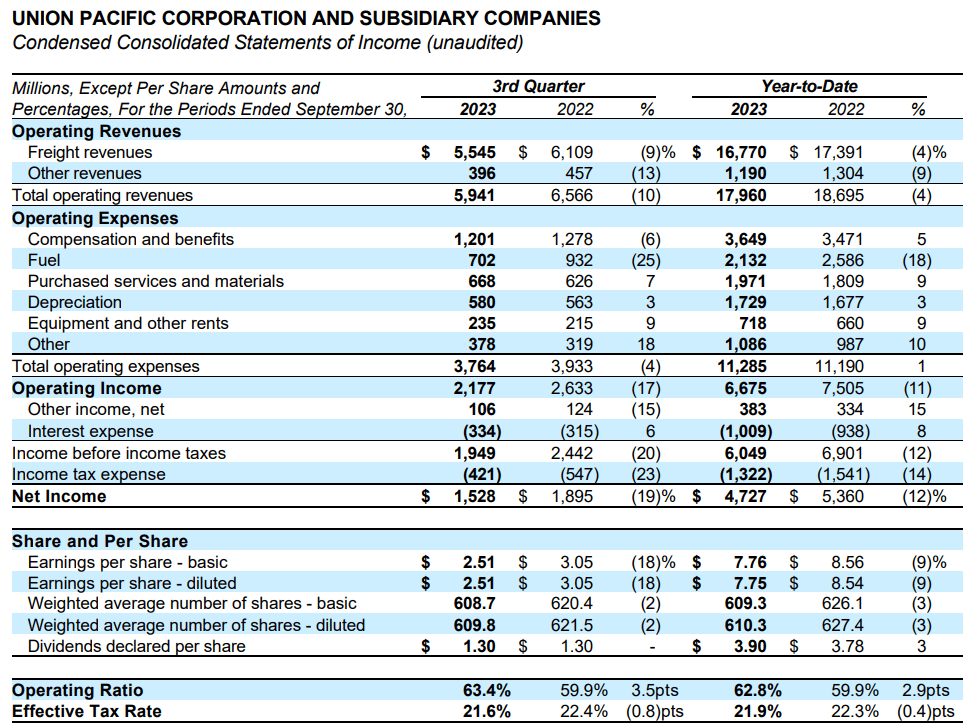

Union Pacific's operating revenue fell by 9.5% year-over-year to $5.9 billion during the third quarter ended Sept. 30. For context, this missed the analyst mark by $40 million .

This would seem to be disappointing on its face. However, railroad operators are economically cyclical. This reality was merely reflected in Union Pacific's operating results for the third quarter.

Two factors were behind the company's less-than-ideal operating results in the third quarter. First, a year-over-year decline in fuel prices negatively impacted total fuel surcharge revenue during the quarter. By how much? According to CFO Jennifer Hamann's opening remarks in the Q3 2023 earnings call , fuel surcharge revenue of $637 million represented a drop of $515 million over the year-ago period.

Second, the company's transported volumes decreased by 3% year-over-year for the third quarter. Per the EVP of Marketing and Sales Kenny Rocker, these lower volumes were the result of lower grain exports. That stemmed from a tight supply. Less coal volume due to more competitive natural gas prices played a part as well. Finally, lower lumber demand was another contributing factor to these lower volumes.

Union Pacific's diluted EPS dipped by 17.7% over the year-ago period to $2.51 in the third quarter, though this did top the analyst consensus by $0.04. Aside from a lower operating revenue base, higher fuel prices during the quarter and a lag in surcharge revenue were to blame for falling profits. These factors led Union Pacific's operating ratio (operating expenses divided by operating revenue) to rise by 350 basis points to 63.4% for the quarter.

The good news is that analysts expect fuel surcharges and volumes to turn the corner beginning next year. According to estimates from FAST Graphs, Union Pacific's diluted EPS will grow by 10% in 2024 to recover to the 2022 level of $11.33 (e.g., its previous peak). From there, diluted EPS is expected to move 12% higher to $12.67 in 2025.

Turning to its financial solvency, Union Pacific remains healthy. The company's interest coverage ratio through the first nine months of 2023 clocked in at 7. Given that this year is expected to be an earnings trough for Union Pacific, that's not a bad interest coverage ratio.

Dividend Growth Should Be Decent Moving Forward

Union Pacific's dividend hasn't grown in 2023. Yet, the company has been such an amazing dividend grower that its quarterly dividend per share has surged higher by 62.5% since 2018 to the current rate of $1.30 .

Through the first nine months of 2023, Union Pacific has posted $3.4 billion in free cash flow. Against the $2.4 billion in dividends paid over that time, this works out to a 70% free cash flow payout ratio (page 6 of 40 of Union Pacific's 10-Q filing ).

As operating cash flow recovers, free cash flow generation should be stronger in the years to come. That should be enough to make high- single-digit annual dividend growth possible for the foreseeable future.

Risks To Consider

Union Pacific's overall fundamentals are enough to earn it our 13/13 ultra SWAN rating. Even with that being the case, the company still has risks.

As I alluded to earlier, Union Pacific's economically cyclical nature may be disqualifying to some investors. That's because economic downturns tend to weigh on the company's results every few years, which can result in earnings volatility from year to year.

Another risk to the company is that like Norfolk Southern, it transports hazardous materials. If railcars carrying dangerous chemicals were to derail, this could cost Union Pacific billions of dollars and harm its reputation as well.

Additionally, U.S. Class I railroads are heavily unionized. That opens Union Pacific up to the risks of strikes and disruptions to workflow. This could weigh on the company's financial results.

Summary: Waiting For A Better Entry Point Before I Add

{kind=link}

{kind=link}

Union Pacific is an attractive business, but like ownership in any company, it must be purchased at the right price. Shares are trading at a blended P/E ratio of 23.9, which is moderately above the historical norm of 18.7 per FAST Graphs. If the company matches the current growth consensus and the valuation dwindles to its normal P/E ratio, cumulative total returns through 2025 could be just 1%. That's far less than the 13% cumulative total returns that the SPDR S&P 500 ETF Trust ( SPY ) is expected to generate during that time. This is why until shares of Union Pacific grow more valuable and/or fall to around $220 a share, I will initiate coverage with a hold rating.

For further details see:

Union Pacific: Is Now The Time To Buy This Awesome Dividend Stock?