UNP - Union Pacific Is One Of My Favorite Plays Going Into 2024

2023-11-25 02:49:00 ET

Summary

- Union Pacific is a high-conviction investment, accounting for 6.1% of my portfolio.

- Despite challenges, Union Pacific has shown strength and resilience, reflected in its stock performance.

- The involvement of Soroban Capital Partners and new CEO Jim Vena could potentially lead to value creation and improved metrics for Union Pacific.

Introduction

It's time to talk about the Union Pacific Corporation (UNP) , the economy, trends going into 2024, and my investment strategy.

As most of my readers know, Union Pacific is one of my high-conviction investments, as it accounts for 6.1% of my current portfolio value. This makes it the fourth-largest holding behind three defense companies.

My most recent article on Union Pacific was written on October 19, when I used the title Union Pacific Q3 Earnings: Investors Take A Note, UNP Stock Is A Buy .

As the title suggests, that article was an earnings review. Below is a part of my takeaway:

My outlook on Union Pacific remains as bullish as ever. Despite facing challenges like weakening economic growth and rising costs, the company's commitment to efficiency, shareholder distributions, and maintaining its full-year guidance during uncertain times reflects its strength and resilience.

Interestingly enough, UNP shares are up 5.2% since then. In fact, all but one of my bullish calls this year are in positive territory despite a steady downtrend in economic growth expectations.

That's why I'm writing this article, as we have a lot to discuss.

In this particular article, I will detail the reasons why I am optimistic about Union Pacific's prospects for 2024.

This includes discussing recent advancements made in business operations, the company's competitive advantages, potential (unexpected) economic developments that could benefit the company, and an analysis of the company's risk/reward ratio.

In other words, there are a lot of new developments we need to talk about.

So, let's get right to it!

Union Pacific's Struggles

One of my favorite articles I've written this year (regardless of the ticker) is my Union Pacific article from March 3 titled Why Union Pacific Could Potentially Double By 2025 .

In that article, I focused on the involvement of Soroban Capital Partners, a top-10 investor in Union Pacific.

As some may recall, the fund pushed hard to get former CEO Lance Fritz replaced by Jim Vena. The fund used UNP's poor performance compared to its peers as a reason for a change of course at the railroad's leadership top.

Reasons include UNP's underperformance in safety, volume growth, revenue growth, cost management, and shareholder returns. In other words, all the things that matter.

Soroban Capital Partners

Back then, it also used the comparison to the Canadian railroads, which are known for operating excellence, as a reason to highlight potential value creation in case Union Pacific wins back investors' trust by improving key metrics.

Soroban Capital Partners

Fast forward to mid-October, Union Pacific reported its third-quarter earnings, which was the first earnings call that Jim Vena attended as the company's CEO.

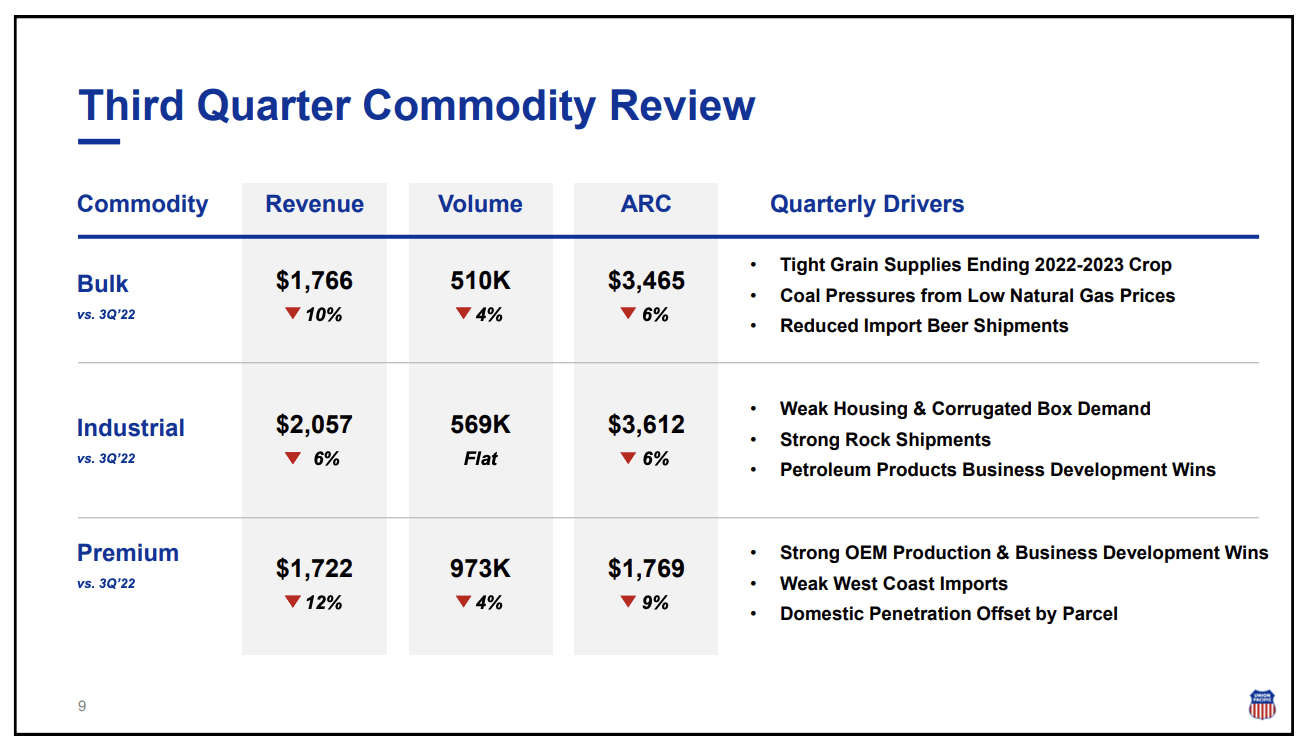

The third quarter was tough, as bulk revenue was down 10%, driven by lower fuel surcharges and a decline in volume, particularly in grain exports and coal.

Industrial revenue decreased due to lower fuel surcharges and a negative mix in volumes.

Premium revenue was down 12%, with a decrease in volume and average revenue per car.

{kind=link}

Although the company largely kept the full-year outlook unchanged, it noted that the demand environment would not exceed industrial production, while elevated costs would negatively impact the operating ratio.

The operating ratio has been an issue since America's railroads faced higher inflation, pressure to hire more employees to deal with post-pandemic demand, and the demand weakness that followed.

3Q23 saw an operating ratio of 63.4%, which is up 350 basis points compared to the prior year quarter.

The operating ratio measures the percentage of revenue that is spent on operations. The lower, the better.

Earlier this year (in my Soroban Capital article), I showed the chart below. In 2004, the operating ratio was 87%. That number rapidly declined to 56% in 2020. Although 2020 had the tailwind of mass layoffs, a big chunk of efficiency gains came from technology adoption, precision railroading, railroad consolidations, and similar efforts.

Soroban Capital Partners

Getting the OR down to the mid-50% range is tough, especially because it needs to be done with care. After all, safety measures and customer satisfaction cannot suffer in the company's ever-ongoing quest for efficiency gains.

On top of that, the railroad is dealing with demand weakness.

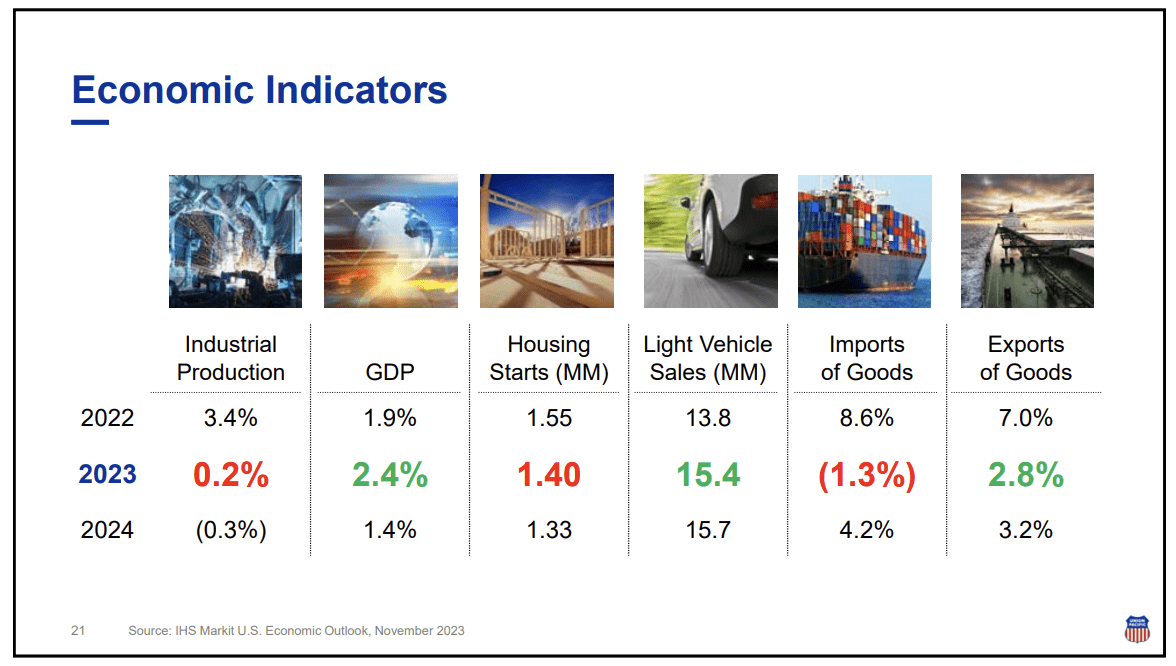

In October, the leading ISM Manufacturing Index took another hit, indicating that manufacturing demand is expected to worsen at a faster pace than in September. Even worse, manufacturing sentiment has been in a steady downtrend since early 2021! It has been in contraction since late-2022.

Bloomberg

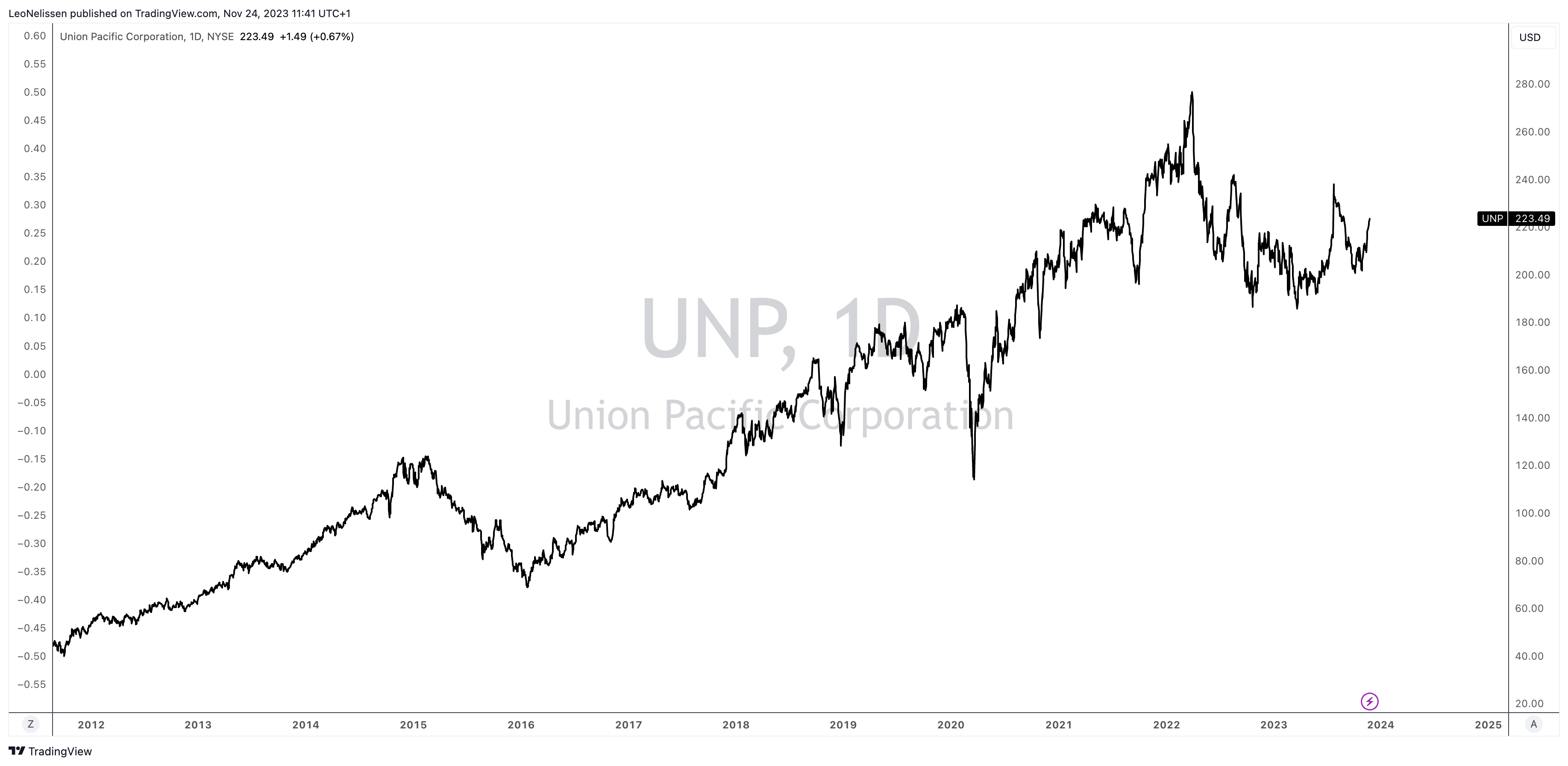

With that in mind, note that Union Pacific's stock price hasn't gone anywhere since early 2021. That's the power of leading indicators!

- Since 2Q21, UNP has returned 0%.

- Between 1Q16 and 2Q21, UNP has returned 25.8% per year!

TradingView (UNP)

{kind=link}

This brings me to the next part of this article.

Reasons To Be Upbeat About UNP

Earlier this month, the company presented at the Stephens 2023 Annual Investment Conference, where it discussed its outlook and efforts to improve its business.

The company discussed key aspects that are expected to bring UNP back to the top.

Measure one is safety .

With a focus on becoming the safest railroad in North America, Union Pacific aims to set a high standard in the industry. This commitment aligns with the broader industry trend towards enhanced safety measures.

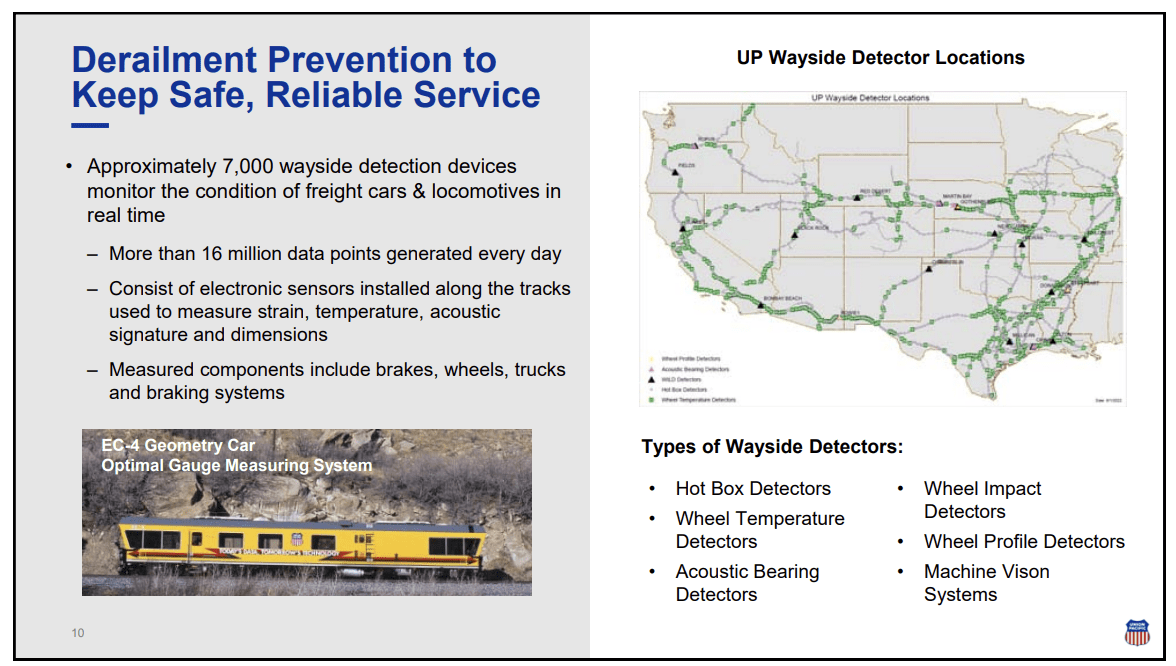

The company highlighted that railroad transportation is the safest transportation method. For example, more than 99.9% of hazmat shipments arrive safely. Now, UNP is boosting investments in technology to detect risks earlier. This prevents derailments and enhances employee safety.

{kind=link}

Measure two is service excellence .

Union Pacific distinguishes itself by tailoring services to meet diverse customer needs. The company acknowledges the varied expectations of different customers and commits to delivering on the promises made to them. This is a response to poor service levels after the pandemic, which raised a lot of eyebrows in the industry.

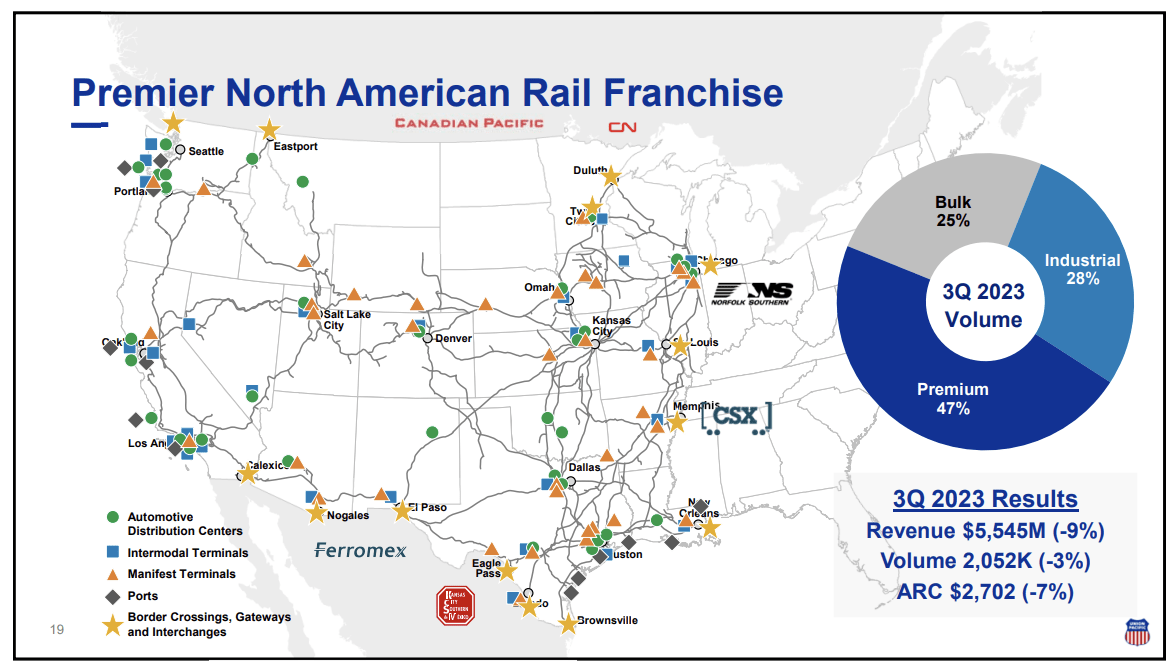

It also needs to be said that Union Pacific runs the most diversified railroad business in North America, with major exposure in bulk, industrial, and premium categories.

Its network combines all major markets in the Western two-thirds of the United States, including ports, metro areas, and every supply chain imaginable.

Moreover, it has the advantage of a 70-mile-per-hour train speed, which railroads in the East cannot compete with due to geographical reasons.

{kind=link}

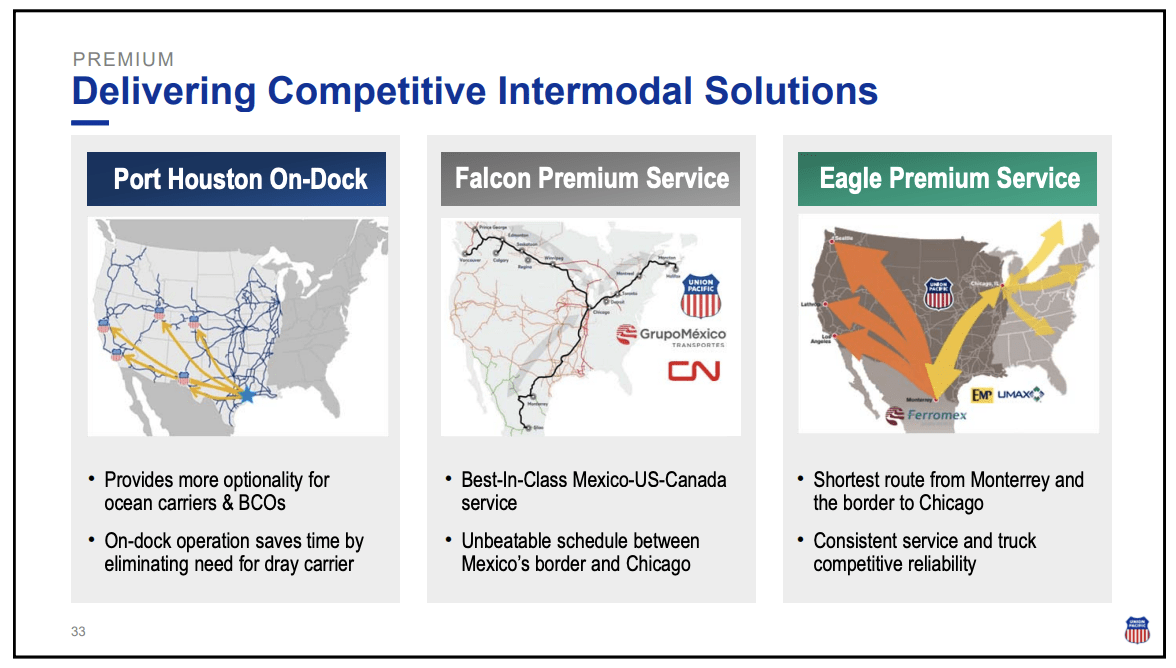

It is also expanding its services. For example, it has an Eagle Premium Service with the Mexican Ferromex railroad to connect U.S. markets to Mexico. Also note that UNP owns slightly more than a quarter of Ferromex, which positions UNP to benefit from growth in Mexico and economic re-shoring.

Furthermore, UNP has a deal with Grupo Mexico and Canadian National (CNI), which resulted in the Falcon Premium Service. This service aims to compete with Canadian Pacific Kansas City (CP), the first North American railroad to connect all North American nations through a single railroad.

{kind=link}

Measure three is operational efficiency .

Operational excellence forms the third pillar of UP's strategy. This involves ensuring the most efficient and streamlined operations, aiming for the best margin and operating ratio in North America.

Union Pacific emphasizes its focus on fundamentals, such as efficient yard operations, reduced dwell times, and optimized train velocity. The focus on efficiency is seen as a key driver for achieving financial goals.

{kind=link}

Furthermore, when it comes to inflationary pressures, the company has confidence in overcoming these challenges through a combination of revenue growth, cost reduction, and strategic leveraging of the company's unique strengths.

The bottom line is that UNP is done playing around.

According to Mr. Vena, the vision is clear: Union Pacific aims not only to compete but to be the best-margin railroad in North America.

Time will tell how successful they will be, but they certainly have the tools to get it done.

2024 Uncertainties & Shareholder Distributions

As good as all of this sounds, the mid-term will see some challenges. During the same conference, Mr. Vena acknowledged the challenges faced by the railroad business, including inflation and labor shortages.

The strategy to address these challenges involves a dual approach:

- Focusing on price adjustments to recover from inflation and

- Enhancing operational efficiency.

Furthermore, the company pointed out specific headwinds expected to continue into 2024, including challenges with coal contracts indexed to natural gas and potential pressures on the intermodal side.

{kind=link}

Despite these challenges, the company's approach is strategic and forward-looking.

Union Pacific will provide a new long-term outlook in the second half of 2024.

While that may take a while, I understand the decision, as I also wouldn't want to give a long-term outlook in this environment. There's just too much room for error, and it doesn't add a lot of value, as most investors are aware of long-term guidance risk in this environment.

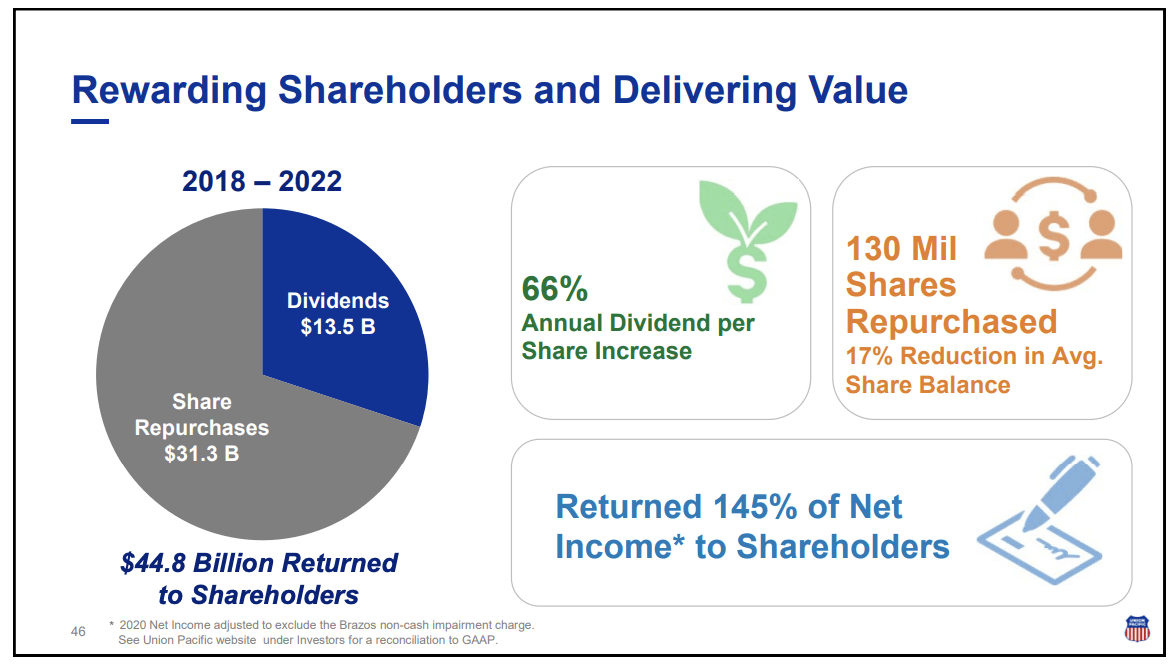

Now, onto the good news. UNP is one of the most shareholder-friendly companies on the market.

Between 2018 and 2022, it has distributed $44.8 billion to shareholders - most of it through buybacks. This translates to 145% of net income, as UNP used its balance sheet to buy back stock. The only reason why it did that was its very low leverage ratio.

{kind=link}

Over the past ten years, UNP has bought back a third of its shares. Its dividend has risen by roughly 230%.

Furthermore:

- UNP currently yields 2.3%.

- This dividend is protected by a 51% payout ratio.

- The five-year dividend CAGR is 12.2%.

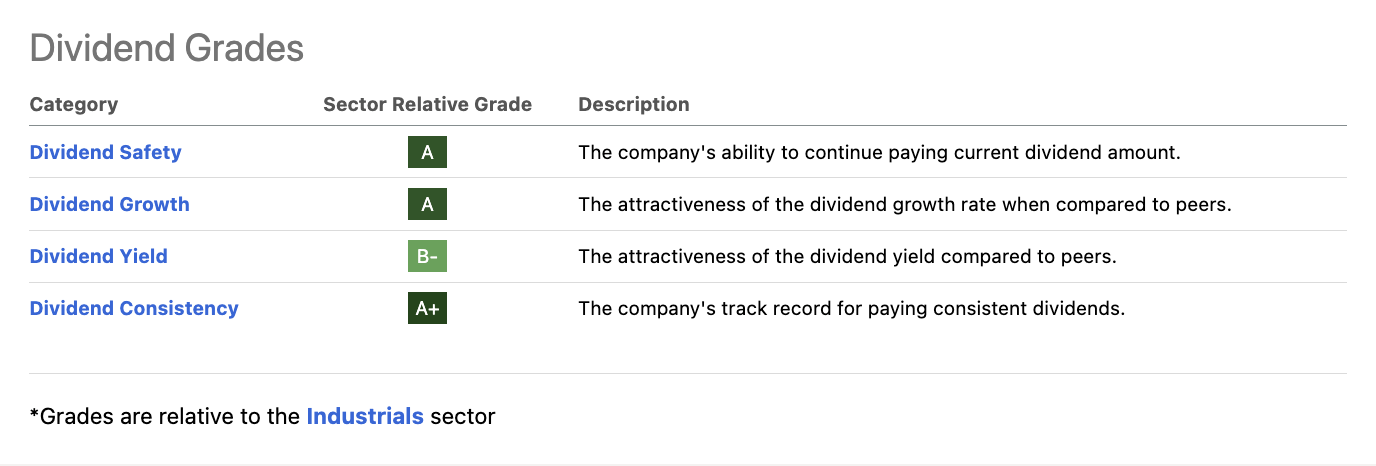

As a result, it has one of the best-looking dividend scorecards in its sector.

{kind=link}

With that in mind, due to economic challenges, UNP has reduced buybacks. In the first three quarters of this year, it bought back stock worth $705 million. That's down from $5.5 billion in the prior-year quarter.

As I said in the past, UNP used its balance sheet to buy back stock. Now, it is reducing buybacks to protect its balance sheet. It is not risking its business to make its per-share performance look good.

As of 3Q23, it has an adjusted leverage ratio of 3.0x EBITDA, which is healthy. It has an A-rated balance sheet.

Valuation

Earlier in this article, I discussed the longer-term decline in the ISM Manufacturing Index and the impact this has on the UNP stock price.

The good news is that we could be looking at a potential bottom.

For example, regional manufacturing surveys (albeit very volatile) have started to start a bottoming process this year. Both the Empire State and Philadelphia manufacturing indexes are indicating a potential ISM bottom in 1H24.

Wells Fargo

We're seeing similar developments in other nations.

For example, Europe's industrial heart, Germany, is seeing a bottoming process in its leading Ifo Business Climate index.

Ifo Institute

Nonetheless, please be aware of elevated economic risks.

- The Fed is still fighting sticky inflation.

- We're seeing a wave of maturing debt in the next two years, which will likely have to be refinanced at elevated rates. This could do serious damage to economic stability.

Bloomberg, Game of Trades

Unemployment is starting to increase, which could hurt consumer spending and housing demand more than markets may anticipate.

The good news is that UNP hasn't gone anywhere since 2021. It is also still trading roughly 19% below its all-time high despite rising 22% from its 52-week lows.

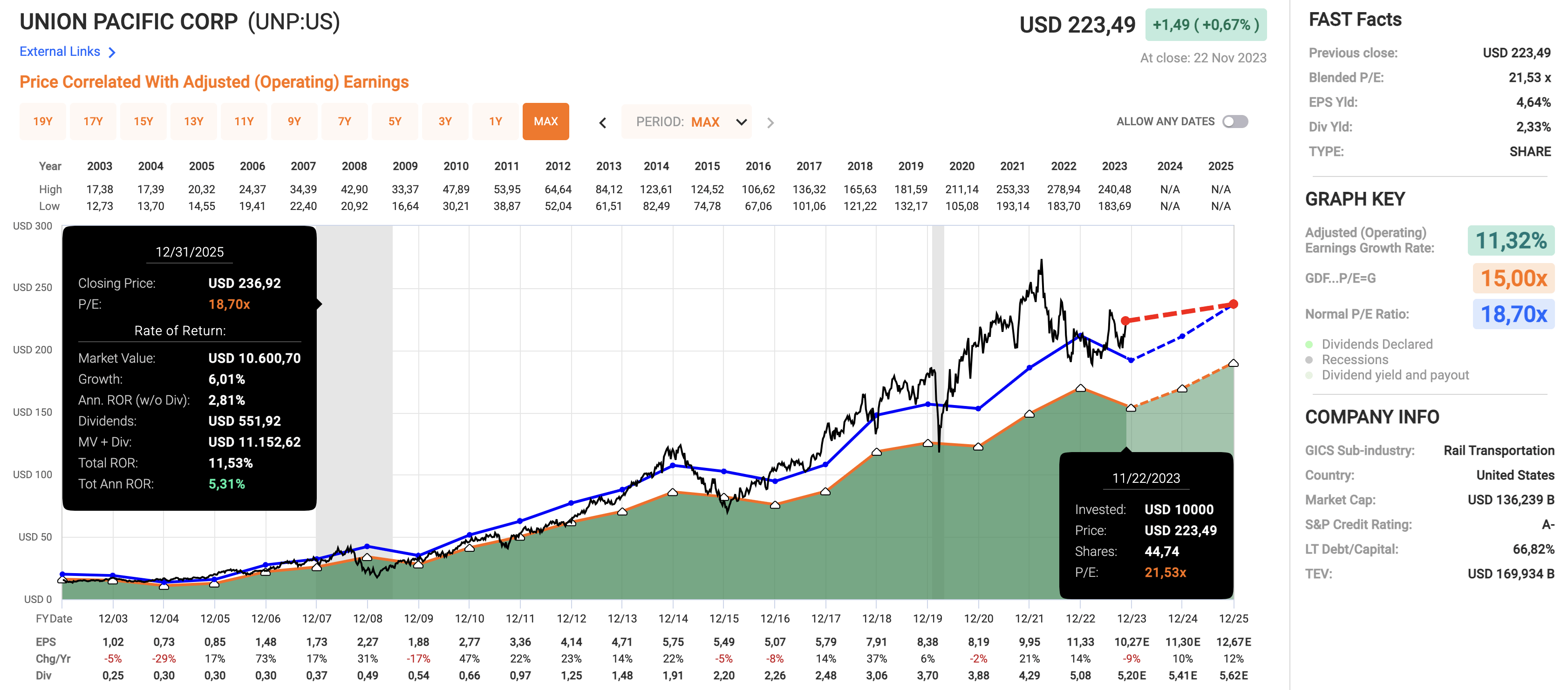

Using the data in the chart below:

- UNP is currently trading at a blended P/E ratio of 21.5x.

- Its 20-year normalized P/E ratio is 18.7x. In other words, UNP trades at a premium despite its poor performance.

- This year, EPS is expected to decline by 9%, followed by 10% and 12% growth in 2024 and 2025, respectively.

- When combining a return to its normalized valuation (a lower valuation) and expected EPS growth, the company has a fair stock price value of $237. That's 6% above the current price. It would imply an annual return of 5.3% through 2025 by incorporation of its dividend.

{kind=link}

This is not a very juicy return outlook.

However, we need to look further.

- EPS estimates are very volatile.

- Six months ago, analysts expected UNP to generate $12.31 in 2024 EPS. Now, that number is $11.30.

- The same goes for 2025 expectations, which have come down from $13.79 to $12.70.

Based on expectations from six months ago and a 22.1x multiple, the company has a fair price target of $300. This would imply an annual return of 18%!

Obviously, all of these numbers are theoretical. However, it shows if I'm right and we get an ISM bottom, we will likely see meaningful EPS revisions, leading to higher gains.

That said, I believe that UNP has a fair stock price of $300 to $320. I expect to see this target in the second half of 2025 or early 2026, depending on the timing of a potential economic bottom.

My strategy remains unchanged. I'm adding during stock price corrections. If UNP moves to the $200 to $210 area again, I'll add to my position.

Needless to say, in the short term, we could see headwinds. If you believe that UNP is right for you, gradual buying is the way to go.

If the stock dips, investors can average down. If it takes off, investors have a foot in the door.

I currently apply this to all of my investments and believe that UNP will continue to be one of my best long-term investments.

For further details see:

Union Pacific Is One Of My Favorite Plays Going Into 2024