UNP - Union Pacific Q3 Earnings: Investors Take A Note UNP Stock Is A Buy

2023-10-19 16:01:26 ET

Summary

- Union Pacific remains a significant investment in my dividend growth portfolio, and despite recent economic challenges, I maintain my bullish outlook on the company.

- UNP's recent Q3 earnings call revealed resilience in the face of economic headwinds, with a focus on improving operational efficiency and protecting its balance sheet while maintaining shareholder distributions.

- Union Pacific stock's attractive valuation, earnings recovery potential, and long-term growth prospects lead me to rate UNP as a Buy.

Introduction

The Union Pacific Corporation (UNP) is my third-largest investment and one of the first five stocks that I bought for my dividend growth portfolio.

As most readers know, I've been bullish on the company's future for a very long time. I have also aggressively bought this stock on dips, making it one of my top holdings.

On July 26, I wrote an article titled Union Pacific Stock Goes Boom, Is It A Buy Now?

In that article, I discussed the company's second-quarter earnings, the new CEO, Jim Vena, its ability to distribute cash to shareholders, and its valuation.

Back then, the stock surged more than 10% after earnings, which was caused by the news that Mr Vena would take over from Lance Fritz.

It's also caused me to remain cautious about UNP as I believed that economic weakness would offset the short-term euphoria caused by the new CEO.

Since then, UNP shares have erased the entire post-earnings rally.

FINVIZ

Having said that, UNP just reported its third-quarter earnings.

As expected, revenue was under tremendous pressure from weakening economic growth. Pricing also suffered as lower energy prices caused fuel surcharges to drop.

Due to these risks, the company massively reduced buybacks to protect its balance sheet.

However, the company is upbeat about its future. It maintained its full-year guidance and continues to see market opportunities.

While the economy is not out of the woods yet, I'm an aggressive buyer of UNP shares on any major weakness. It's not only a major holding of my portfolio but also of almost every portfolio that I advise.

This earnings call confirmed my bullishness.

So, let's dive into the details!

Withstanding Cyclical Weakness

One of the most important things to keep in mind before investing in railroads is how cyclical they are. While all North American Class I railroads are well-managed corporations (some more than others), none of them can escape cyclical downtrends.

Union Pacific, for example, has a duopoly in the West with Berkshire-owned BNSF. It connects major economic hubs, ports, sellers to buyers in every supply chain imaginable, and goods transportation from the East to the West and the other way around.

Association of American Railroads

Having said that, the economy isn't in a great place. Economic growth is weakening, inflation is sticky, and rates are elevated and not expected to come down meaningfully anytime soon.

The ISM Manufacturing Index, for example, has been in a downtrend since early 2020 and in contraction territory since the second half of 2020.

Bloomberg

This is the biggest reason why investors haven't been keen to invest in the company behind the UNP ticker.

In these situations, I don't expect Union Pacific to grow its business. That's impossible, anyway.

What I care about is operating efficiency, which could pave the way for outperforming gains the moment it benefits from rising demand again.

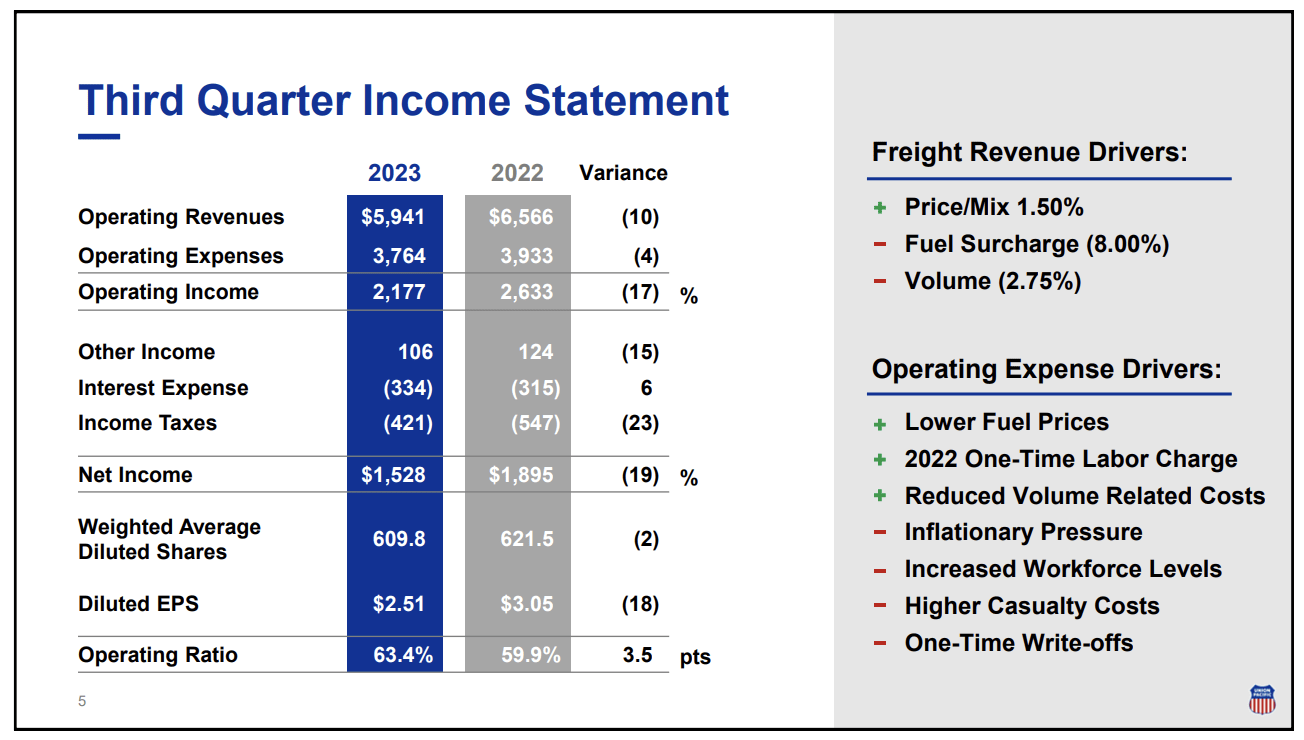

In Jim Vena's first earnings call as CEO of UNP, the company reported net income of $1.5 billion, or $2.51 per share, compared to $1.9 billion, or $3.05 per share, in the same period of the previous year.

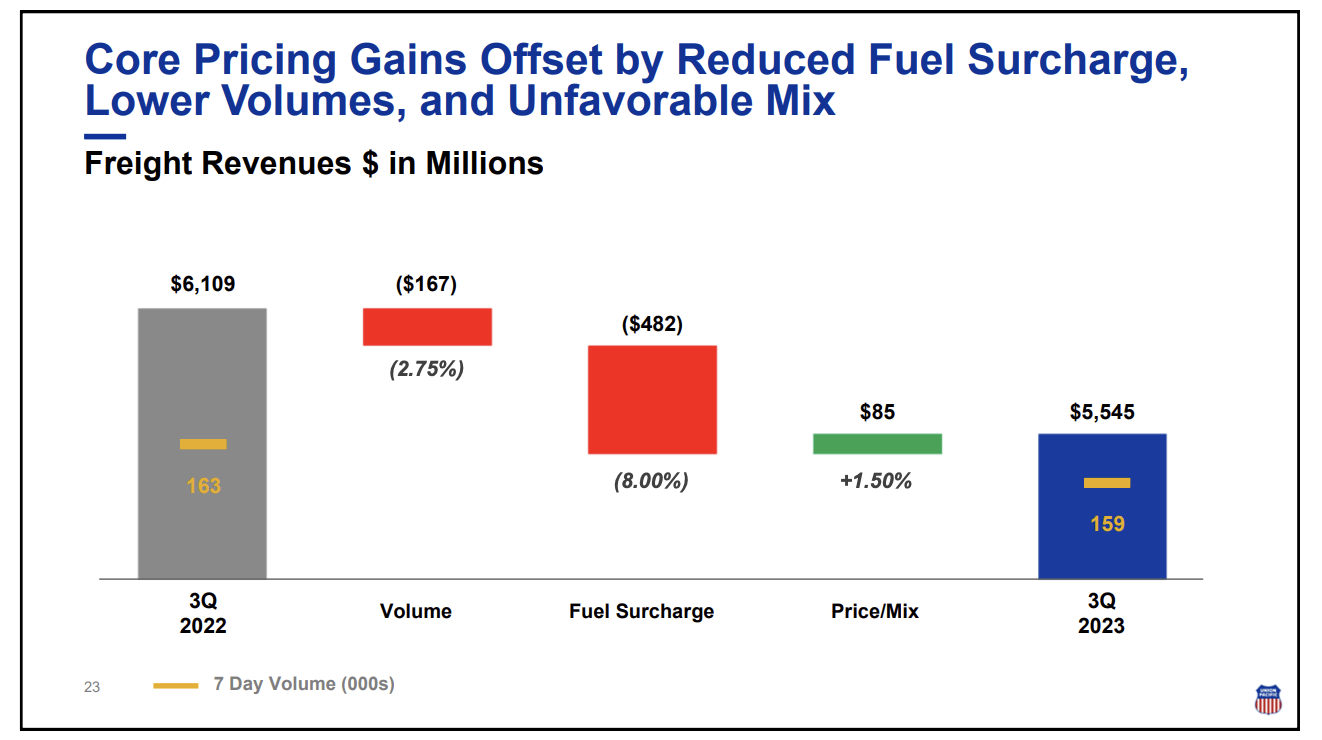

Operating revenue decreased by 10%, mainly due to lower fuel surcharge revenue, reduced volumes, and a decrease in other revenue.

{kind=link}

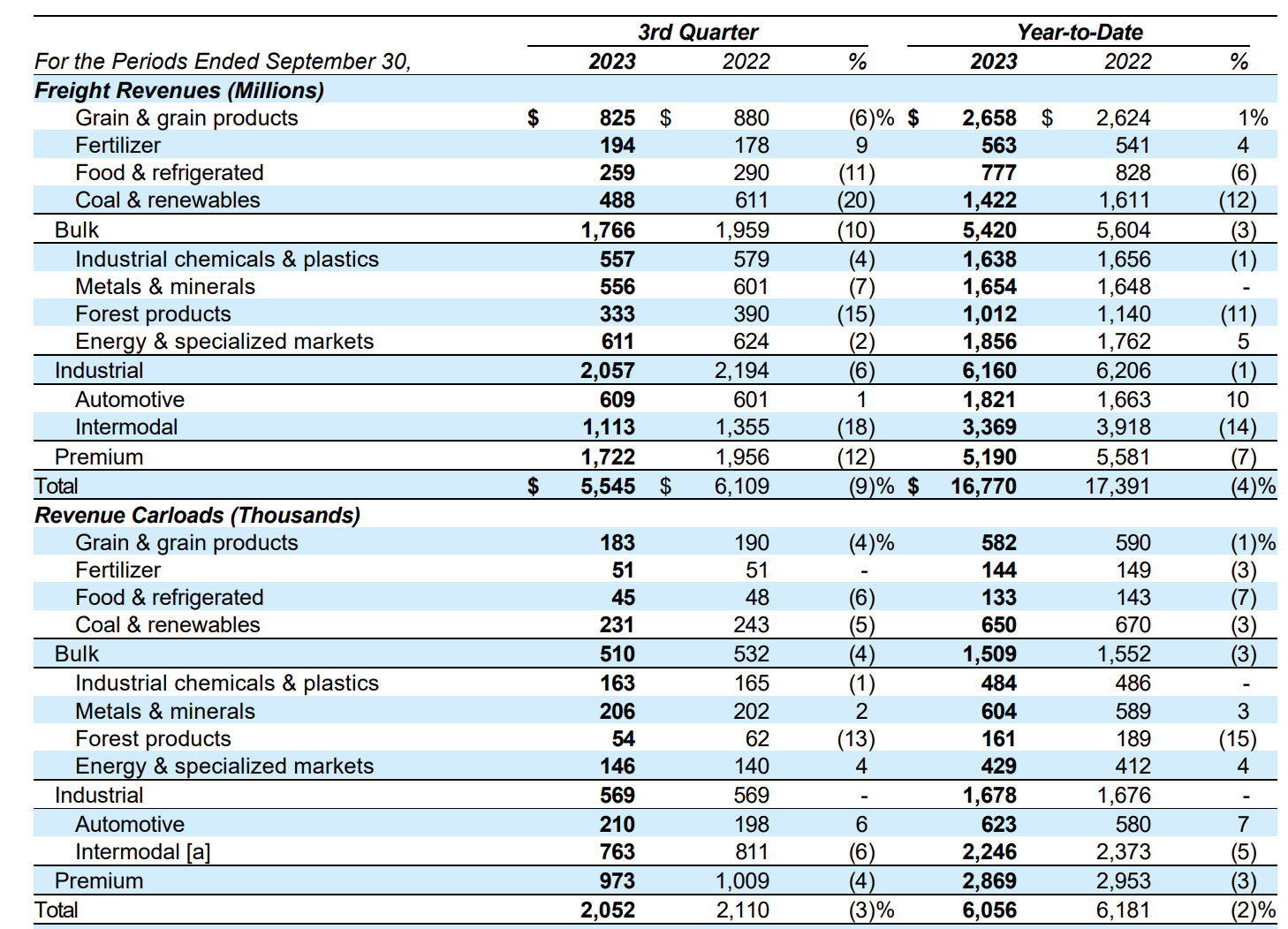

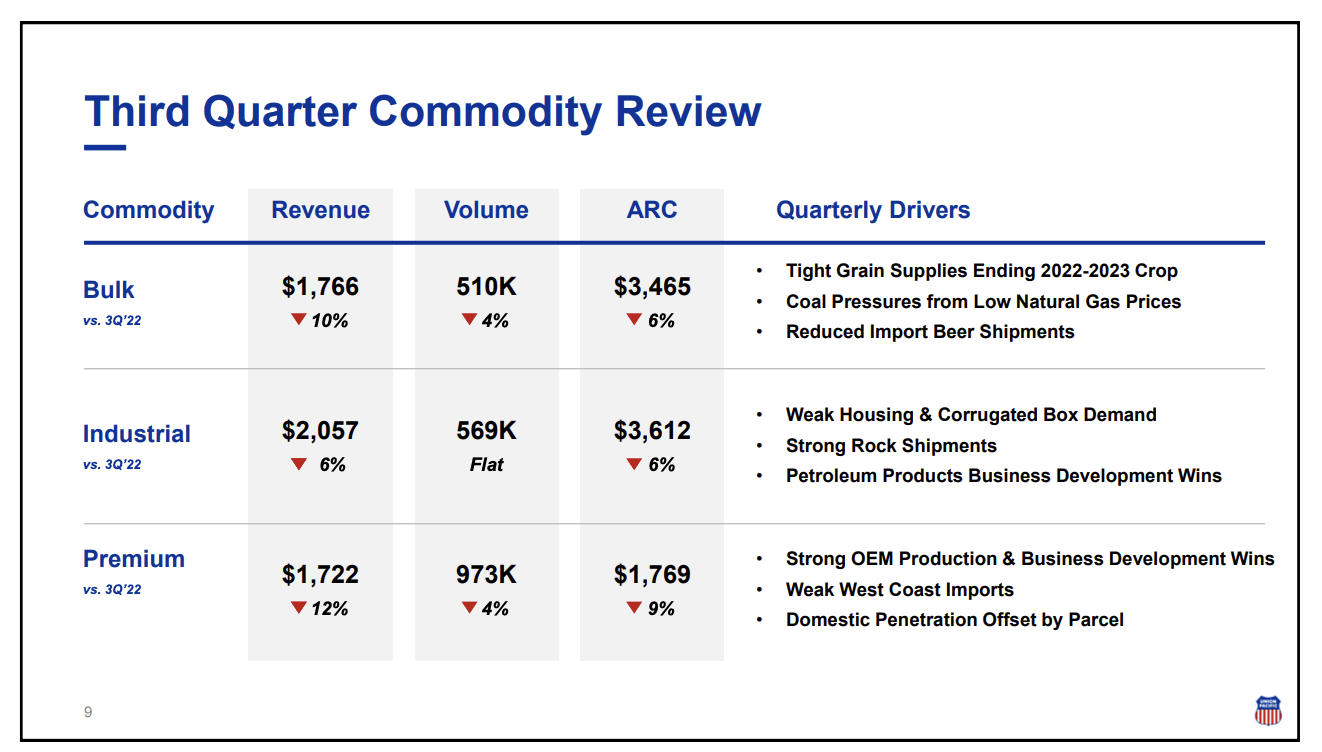

Total freight revenue saw a 9% decline, driven by a 3% decrease in volume.

- Bulk revenue was down by 10%, mainly due to a 6% decrease in average revenue per car, influenced by lower fuel surcharges and a 4% decline in volume. This decline was attributed to weaker grain exports, reduced coal volume due to shifts in electricity generation, and a drop in imported beer carloads.

{kind=link}

- The industrial revenue also declined, primarily due to a 6% decrease in average revenue per car. Core pricing gains were offset by both lower fuel surcharges and a negative mix in volumes.

- The premium revenue witnessed a 12% decline, with a 4% decrease in volume and a 9% decrease in average revenue per car, largely due to fuel surcharges and challenges in the trucking market. Positive aspects included automotive volumes, which showed strength in OEM production and dealer inventory replenishment.

However, intermodal volumes were down, driven by softness in the parcel segment and weak imports on the West Coast. Despite these challenges, Union Pacific's focus on business development yielded opportunities, such as winning wagon shipments from the Texas Gulf, which is an important tailwind in an otherwise expected intermodal demand downtrend.

{kind=link}

With that in mind, the other important financial number we need to discuss is expenses. After all, expenses are a major driver of operating income.

As the overview below shows, expenses declined by 4%, causing operating income to fall by 17% (revenue dropped more than expenses, having a negative impact on margins). The operating ratio rose by 3.5 points to 63.4%.

{kind=link}

Compensation and benefits expenses decreased by $77 million, though it included a one-time labor charge from the previous year.

Workforce levels increased by 3%, and active train crew personnel were up by 2%. Fuel expenses dropped by 25% due to lower fuel prices, and fuel consumption remained steady.

Speaking of workforce levels, the company's operations improved, although it faced weather challenges but managed to restore operations efficiently.

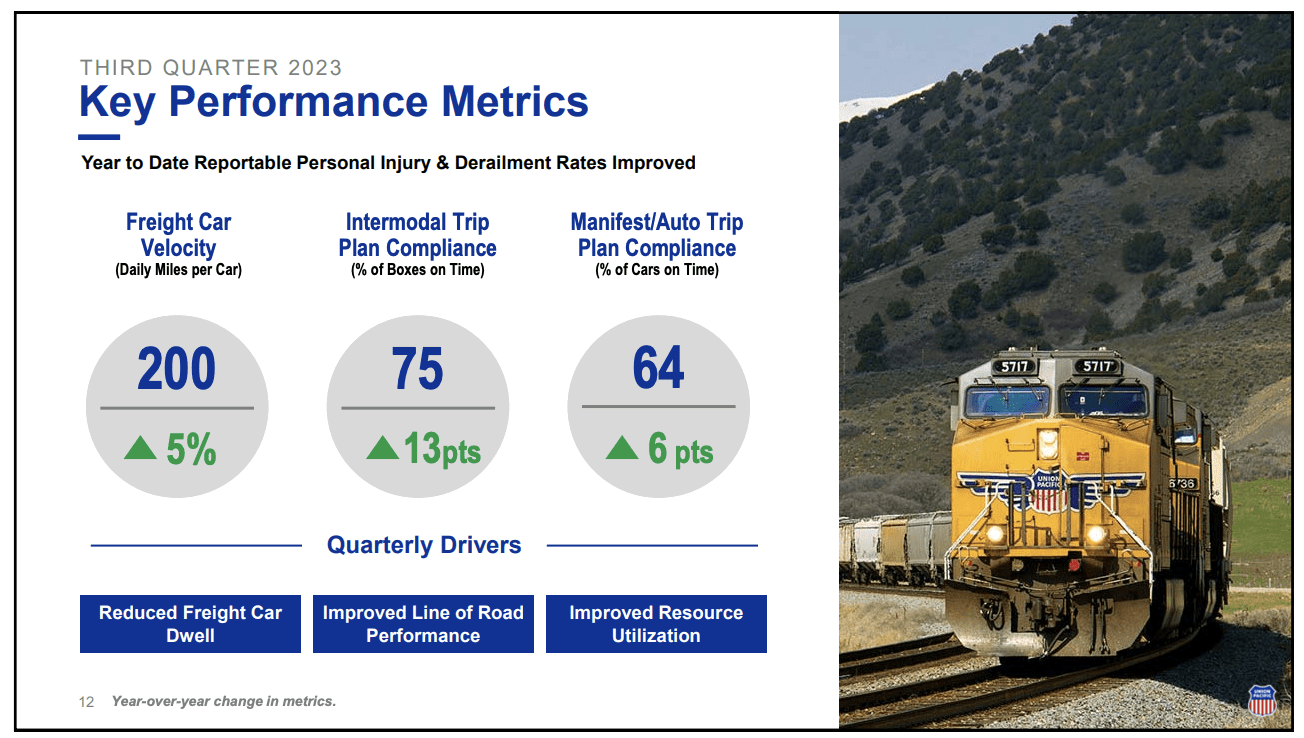

Key operational metrics improved year-over-year, including a 5% increase in freight car velocity, a 13-point improvement in intermodal trip plan compliance, and a 6-point improvement in auto TPC.

{kind=link}

These improvements are important, as services (in the entire industry) got so bad after the pandemic that it was even considered to let competing railroads use each other's rails.

During the earnings call, efficiency metrics were also highlighted, with a 4% improvement in locomotive productivity and a 6% decrease in workforce productivity, reflecting volume declines and increased workforce levels.

Right now, that's the price the company needs to pay in order to become more reliable.

Having said that, the company's focus on train length paid dividends, with a 1% improvement in train length despite lower volumes in the intermodal business.

Shareholder Distributions

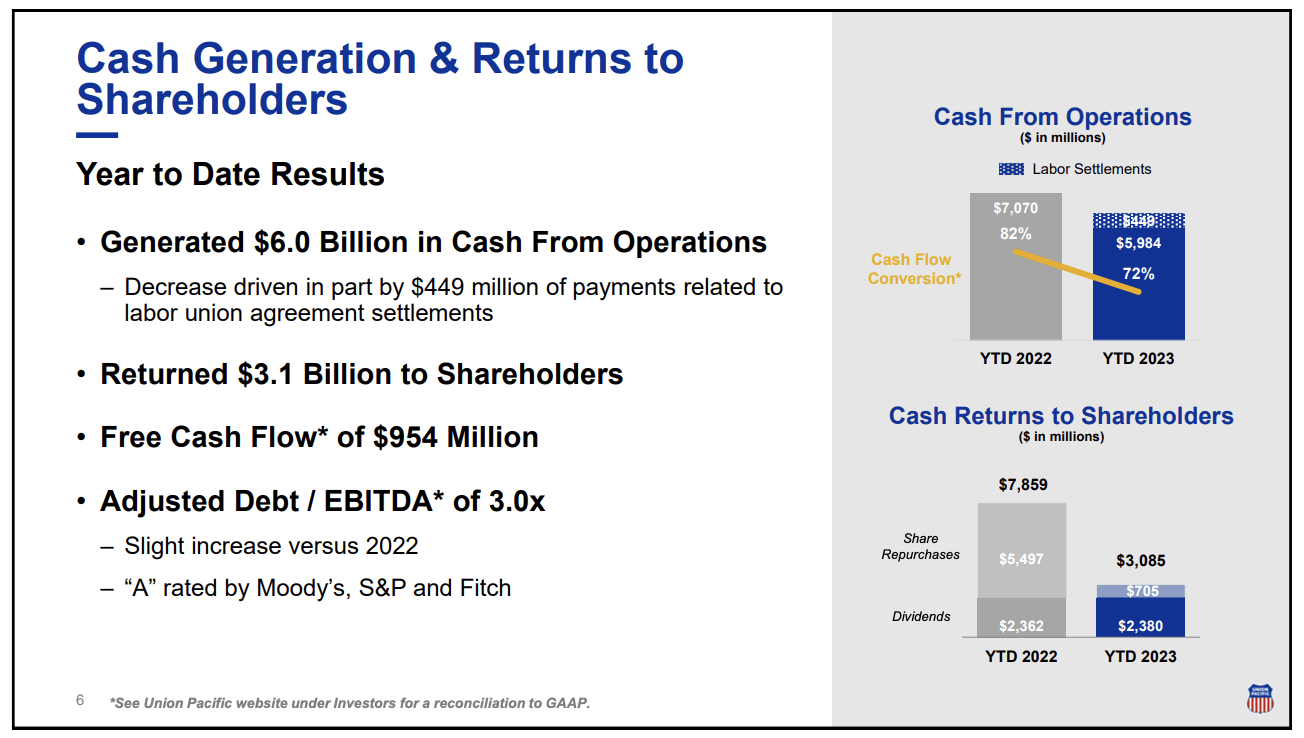

Union Pacific's cash from operations for the year-to-date was $6 billion, a decrease of approximately $1 billion compared to the previous year, primarily driven by lower net income and labor payments.

The cash flow conversion rate dropped to 72%.

{kind=link}

The company returned $3.1 billion to shareholders through dividends and share repurchases during the year. The adjusted debt-to-EBITDA ratio increased slightly from 2022 levels to 3x.

Last year, the company returned close to $8 billion to shareholders.

I'm actually glad the buybacks are down, as this allows the company to protect its A-rated balance sheet.

This also shows that the company is protective of its balance sheets. Over the past few years, UNP has used some debt to buy back stock. This caused a lot of readers to drop the stock because of fears that this isn't sustainable.

However, in the past, UNP used its extremely healthy balance sheet to buy back stock. Its debt was so low that it could afford to buy back stock using debt. Now, the company has become careful.

Nonetheless, its 2.5% dividend yield is well protected. The payout ratio is 48%. The five-year CAGR is 12.2%. The most recent hike was on May 12, 2022, when the company hiked by 10.2%.

Furthermore, over the past 10 years, the company has bought back a third of its shares, making it one of the most aggressive railroads with regard to indirect shareholder distributions.

This also is one of the reasons why UNP has been a great source of wealth for countless shareholders. Despite regular corrections due to cyclical weakness, the company has outperformed the S&P 500 by roughly 40 points over the past 10 years.

Going forward, the company is focused on maximizing growth opportunities, improving service, and generating productivity to achieve financial improvement, which is somewhat obvious.

Union Pacific Outlook

During its earnings call, the company also gave us a fourth-quarter outlook.

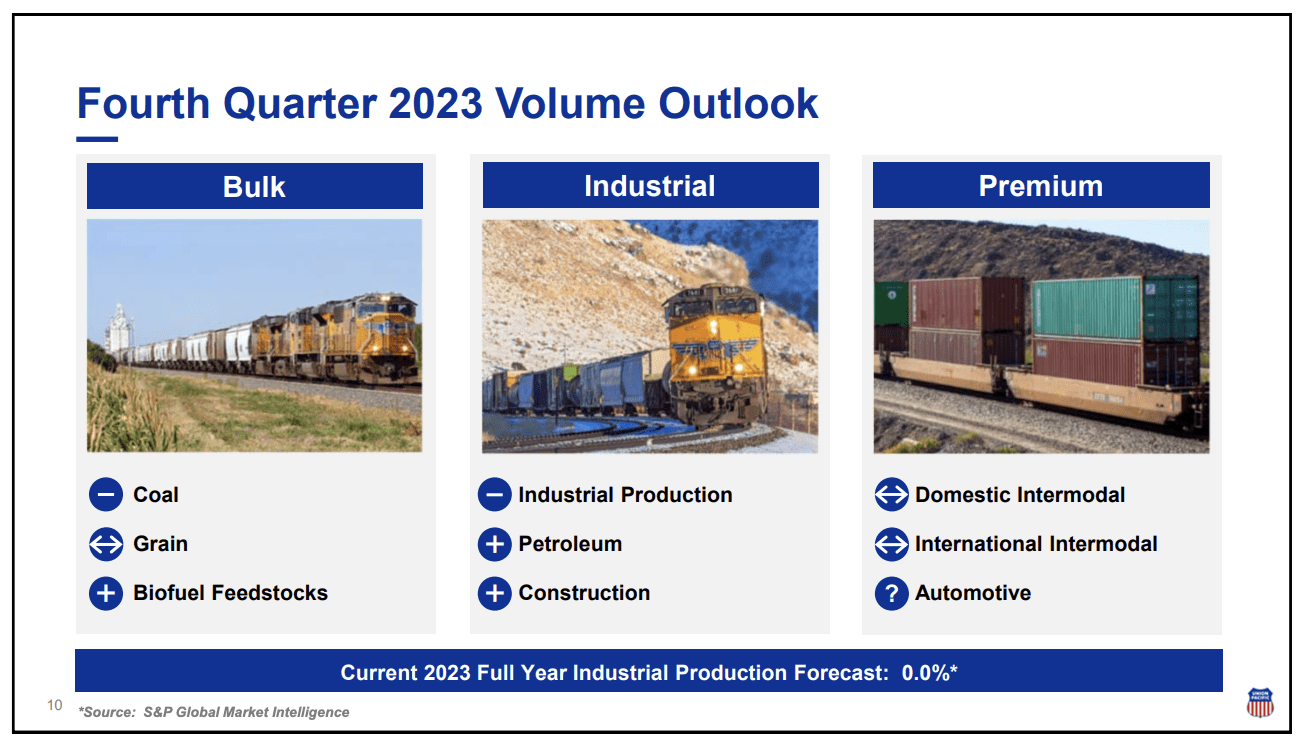

In the bulk sector, challenges in the coal market persisted due to volatile natural gas futures. The company closely monitors grain exports, which are expected to increase with an improved service product capturing more available demand.

Renewable biofuel feedstock demand remains strong, with new opportunities in Iowa, Louisiana, and Nevada.

Union Pacific expects favorable conditions in the petroleum and construction markets, driven by business development efforts.

Meanwhile, the premium sector faces challenges in the intermodal segment, while automotive growth is expected to continue, supported by strong OEM production.

However, ongoing UAW negotiations and strikes could impact fourth-quarter volumes.

{kind=link}

Thanks to positive developments, the company was able to stick to its full-year outlook - despite poor economic developments.

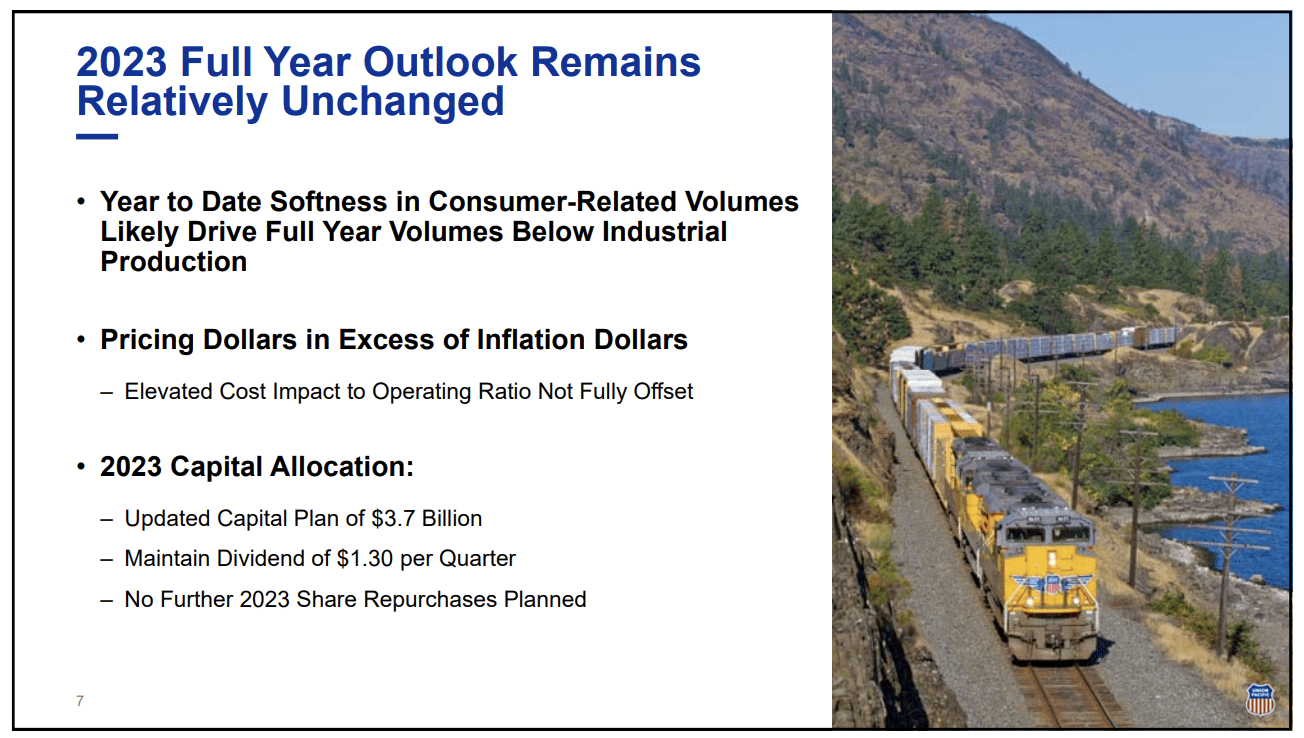

- As expected going into the third quarter, the company is facing a demand environment where full-year volumes are not expected to exceed industrial production.

- Pricing dollars are expected to exceed inflation dollars, but the impact of elevated costs on the operating ratio will persist.

- Fuel remains an earnings headwind, albeit moderating, and significant inflation headwinds continue, primarily from new labor agreements.

- The capital plan for the year is expected to be $3.7 billion.

{kind=link}

I believe that sticking to its guidance is the main reason why the stock is doing well after earnings. I would not have been surprised if the company had cut its guidance.

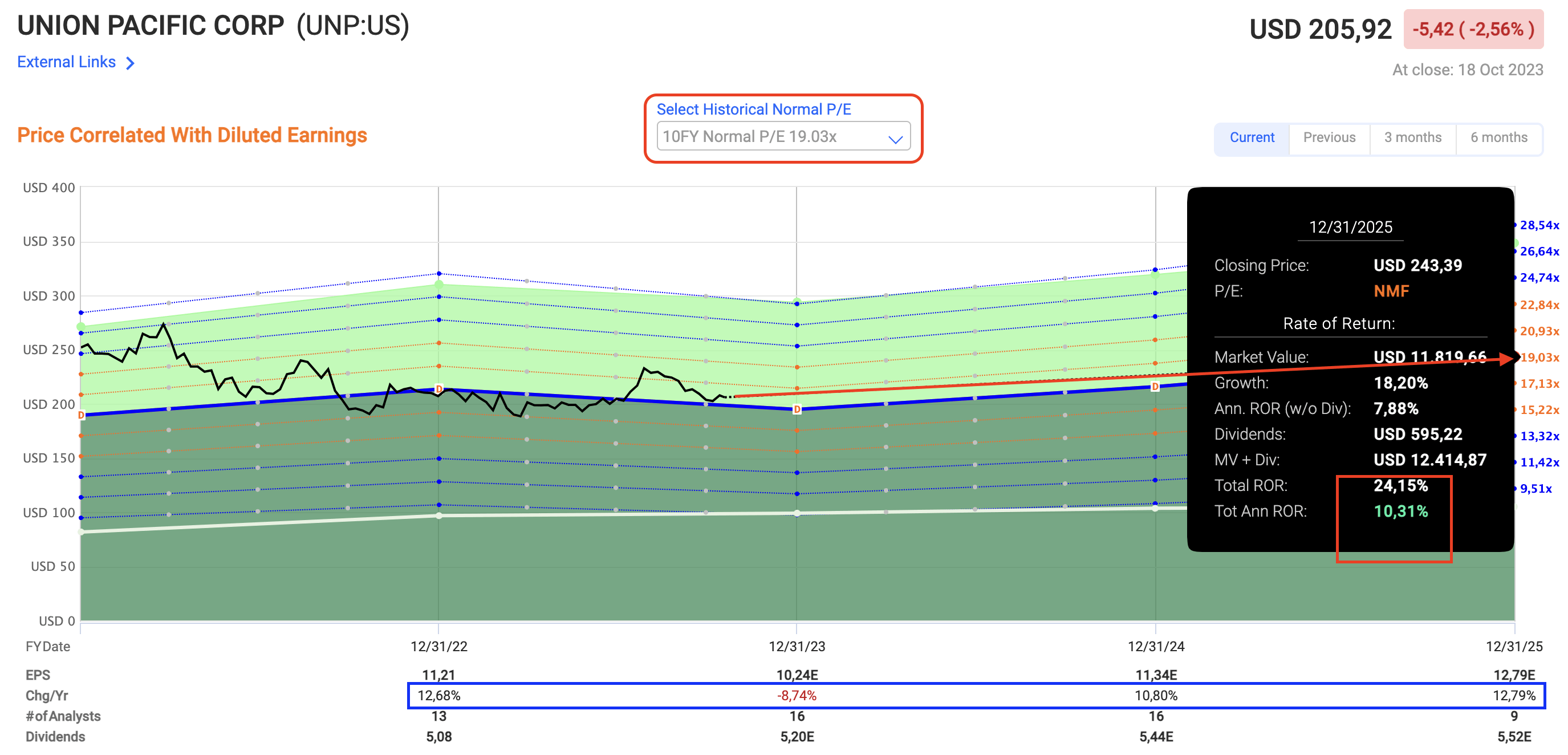

UNP Stock Valuation

UNP is trading at 19.7x earnings. Its 10-year normalized multiple is 19.0x. Despite this slight valuation premium, the company is, technically speaking, able to return more than 10% per year through 2025.

This is based on an expected earnings recovery starting next year. Analysts expect the company to grow earnings by 11% in 2024, followed by an improvement of 13% in 2025.

All of these numbers can be seen in the chart below.

FAST Graphs (Leo Nelissen annotations)

{kind=link}

I believe these numbers could be much higher if the ISM Manufacturing Index improves.

However, it also could mean that the stock price remains subdued if the economy remains weak. Inflation is sticky, the Fed is unlikely to cut rates soon, and pressure on consumers and businesses is building.

While I do not expect a full-blown Great Financial Crisis-like recession, I'm still holding more cash than I usually do to capitalize on buying opportunities.

So far, I mainly accumulated shares below $200. My plan is to keep doing this, although the odds of this happening are getting slimmer, thanks to UNP's strong performance.

Investors who want to refrain from timing the market might be better off buying gradually. That way, if the stock falls, they can average down. If the stock takes off, they have a foot in the door.

This is how I currently deal with every investment.

The bottom line is that I will give UNP a Buy rating. The company is attractively valued and in a great spot to generate long-term outperforming returns.

I expect that it will get help from cyclical demand growth in 2024 and beyond, further fueled by economic re-shoring tailwinds, truck-to-rail conversion benefits, and secular growth in commodities and export opportunities.

It's truly one of my favorite dividend growth stocks.

Takeaway

My outlook on Union Pacific remains as bullish as ever. Despite facing challenges like weakening economic growth and rising costs, the company's commitment to efficiency, shareholder distributions, and maintaining its full-year guidance during uncertain times reflects its strength and resilience.

UNP's long-term performance has consistently outperformed the S&P 500, making it a valuable asset in my dividend growth portfolio.

While the road ahead may have its share of bumps, the company's favorable valuation, growth prospects, and potential for outperforming returns keep me optimistic.

As we look forward, the key drivers to watch are the ISM Manufacturing Index and the broader economic landscape. I continue to accumulate UNP shares on dips, believing in its potential to benefit from cyclical demand growth and other favorable industry trends.

For further details see:

Union Pacific Q3 Earnings: Investors Take A Note, UNP Stock Is A Buy