UAL - United Airlines: A Buy On Market Overreaction?

2023-10-24 09:26:46 ET

Summary

- United Airlines Q3 earnings beat estimates with total revenues of $14.48 billion.

- The company added capacity to increase revenues, but unit revenues and yields are weakening.

- Q4 guidance shows further softening in unit revenues and eroding margins due to high fuel prices and labor costs.

In a previous report , I provided a preview of the Q3 earnings for United Airlines (UAL). With the results in, I will be discussing the results in detail as well as the forward guidance and whether this warrants any adjustment to my buy rating.

{kind=link}

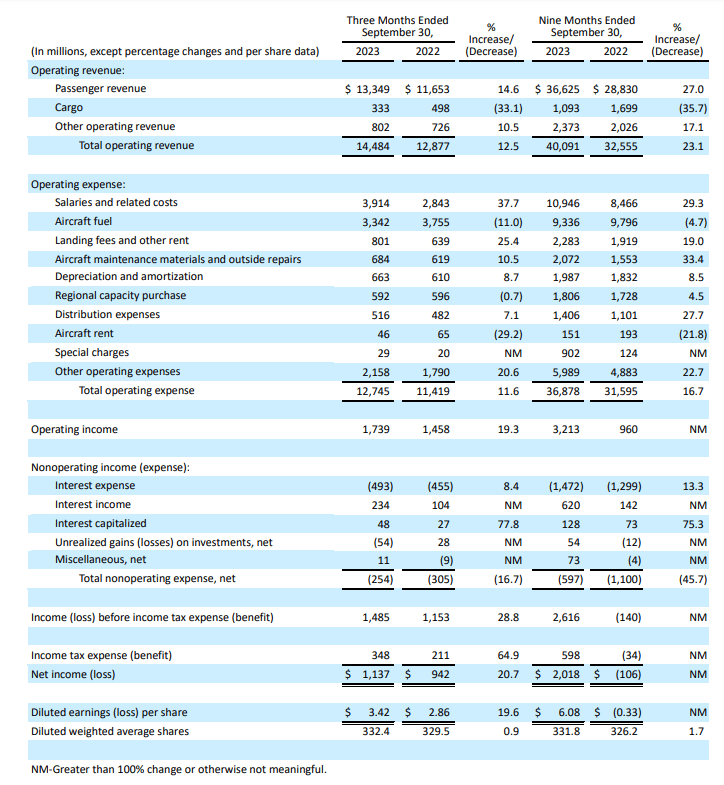

Total revenues of $14.48 billion beat estimates by almost $75 million. Cargo revenues were down by a third reflecting rate normalization as more and more belly freight capacity is coming back online. Passenger revenues increased 14.6% while total expenses increased 11.6% resulting in operating income to increase 19.3% and realize a margin of 12% compared to 11.3% in the same quarter last year. The costs included a 37.7% increase in salaries and related costs as well as an 11% decrease in fuel costs. While results beat on top and bottom line, the post-earnings pressure on United Airlines and its peers is caused by the fact that the company is now facing a combination of high labor costs and high oil prices while that was not the case in Q3 and it feeds the thought that margins will be eroded.

Furthermore, we also have to consider what capacity United Airlines had to put in to increase its results, and what we see is that the company added 15.7% in capacity to realize a 14.6% increase in revenues pointing at a weakening in revenue per available seat mile and yields to be flat. So, the name of the game more than ever is to manage yields amidst falling unit revenues.

On unit cost level, all-in unit costs declined 3.6% driven by lower fuel costs and unit costs excluding fuel increased 2.6%. So, we are seeing that the capacity added is actually barely enough to offset the higher cost profile and with pressure to manage yields and therefore capacity, the airline essentially has one way less to control costs.

Situation In Israel Affects Q4 2023 Guidance For United Airlines

{kind=link}

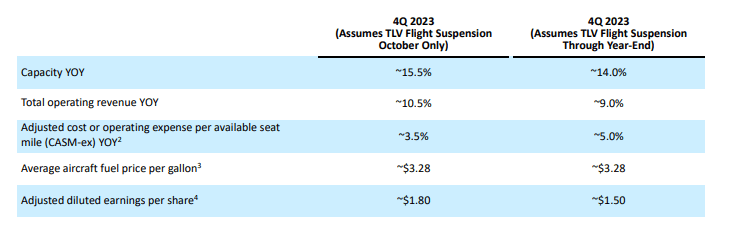

For the fourth quarter, United Airlines has provided two guidance basis figures. One assumes that flights to Tel Aviv will be suspended until the end of October and the other assumes flight suspension through the end of the year which I would think is quite plausible. Capacity is expected to be up 14 to 15.5 percent depending on the scenario, while revenues are expected to be up 9 to 10.5 percent pointing at further softening in unit revenues while CASM-ex has been guided to be up 3.5 to 5 percent and adjusted earnings of $1.50 to $1.80 pointing at net margins of 3.5 to 4.2 percent compared to 7.85 percent in Q3 2023 and 6.8% in Q4 2022. So, we are seeing how elevated fuel prices and higher labor costs are expected to erode margins with or without the operations in Tel Aviv. The company is adding flight capacity to Athens, but that is not providing a full offset to lower capacity to and from Tel Aviv.

Is United Airlines Stock Still A Buy?

For the 2023-2025 timeframe, EBITDA estimates have come down by 4% in total while the company is now expected to generate $1.2 billion less in free cash flow over that same time period. I have entered the balance sheet data and forward projections into the evoX Financial Analytics model. While United Airlines will be facing a tough time ahead with uncertainty regarding the Tel Aviv operations and fuel prices, the current projections do not give any reason to alter my rating as the stock price has come down 40% in recent months while EBITDA estimates only came down 4%. So, I am maintaining my buy rating. The price target, however, has come down.

Nevertheless, there is potential to double as the current EV/EBITDA of 5.4x falls short of the company median of 8.55x or the targeted 8.5x for the industry. Forward projections of earnings would put the EV/EBITDA on 4.2x. Combined, 14% of the upside is driven by earnings expansion and 86% would be driven by expansion of the EV/EBITDA to more appropriate levels.

Conclusion: Potential To Double For United Airlines Stock

The results that United Airlines posted beat expectations, but the focus has already shifted towards future quarters and concerns about the current cost structure including high labor costs as well as high oil prices. This has led to a sell-off in the stock, even though United's balance sheet and the forward projections do indicate the higher implied share prices, and perhaps too much risk is now pulled into the share prices.

For further details see:

United Airlines: A Buy On Market Overreaction?