UAL - United Airlines Is The Industry's Most Vulnerable Player (Rating Downgrade)

2023-09-27 15:10:19 ET

Summary

- United Airlines Holdings, Inc. has been one of the strongest U.S. airlines during the pandemic recovery, but there are signs of trouble looming.

- The airline faces increasing fuel and labor costs, which could impact its profits.

- United also faces challenges in the changing revenue environment, particularly in the international market, where it has been strong.

As the summer 2023 travel season winds down and a growing number of investors ask if the rapid recovery of the airline industry post covid has slowed, there is ample reason to look at each of the players in the industry - especially those that have performed particularly well during the recovery as well as those that are weaker on the edges. United Airlines Holdings, Inc. ( UAL ) has been one of the strongest U.S. airlines during the pandemic recovery period. It intentionally chose not to retire older aircraft during the pandemic so that it would be ready to capture demand when it returned.

Although all U.S. airlines compete in the domestic and most in the near-international market to Latin America and the Caribbean, the long-haul international market is carried by just four U.S. airlines which all compete with foreign carriers. United has long been the largest U.S. airline by revenue in international markets, followed by American ( AAL ) and Delta ( DAL ) which historically have been similarly sized in the international marketplace and Hawaiian ( HA ), which operates entirely from its home base in the Island Paradise to countries throughout Asia and the South Pacific.

Conversely, of the big four U.S. carriers, which includes Southwest ( LUV ) but not Hawaiian, United is the smallest in the domestic marketplace. Thus, United always provides an interesting study in airline strategy and market dynamics, and that is true as summer storms give way to a chill in the air in many parts of North America. Several key changes indicates that trouble could be looming that could threaten United's strong position since COVID recovery began.

United stock has been one of the strongest airline stocks driven by its ability to capture revenue, especially in the long-haul international market. Low fuel prices have been a boon to airline recovery while the international marketplace has consolidated heavily in favor of incumbent/legacy airlines and away from the burgeoning low-cost carrier segment, especially across the Atlantic. United, along with multiple other U.S. airlines, offered investor updates over the last month and all of them included higher costs and/or weaker revenue. United's update follows along with as a discussion of other issues that the industry is facing, whether United cited them or not, as well as an examination of United's strategies and how they might be impacted.

{kind=link}

{kind=link}

Increasing fuel and labor costs

Increased crude oil prices are a threat to many components of Western economies, and transportation companies are particularly at the pointed end of the spear. Airline stocks usually move inversely to crude oil prices. Crude oil prices are flirting with their one-year highs in the low $90s after hovering in the low $70s for the early part of the summer.

Crude oil prices are not a direct correlation to the jet fuel cost for airlines which must incorporate the cost to refine crude oil into jet fuel. Jet fuel competes in the refining process with, or is similar to, diesel and home heating oil and, for many refiners, jet fuel is not the primary product of the refining process. Historically, the jet fuel crack spread, the additional price that refiners essentially charge to convert crude oil into jet fuel, has been in the low teens of dollars per barrel.

During the pandemic, especially as total refinery volumes declined, jet fuel crack spreads vacillated wildly even as demand for diesel fuel remained strong. As the U.S. and Western Europe adapt to more efficient transportation sources including electric vehicles, demand for gasoline has weakened, but fuel for heavy transportation such as diesel and jet fuel have remained strong since there are limited alternatives for those fuels - with the exception of relatively small amounts of sustainable aviation fuels -SAF. In addition, autumn often coincides with refinery maintenance. This fall, several large refineries will be offline for scheduled overhauls including Delta's Trainer refinery which is tuned to maximize jet fuel output, most of which is destined for the airline's operations in the Northeast U.S. although some distillates are sold on the spot market; Trainer expects to be able to provide contracted jet fuel volumes during the shutdown but will not be able to supply the spot market.

Delta and United are the largest commercial users of jet fuel in the Northeast U.S., both of which have large hubs in the New York City area, while United also has a hub at Washington Dulles airport and Delta has a hub at Boston. Jet fuel prices in the Northeast are typically at a premium to the U.S. due to the relatively few number of refineries that remain in the region.

{kind=link}

Currently, jet fuel crack spreads are near $40/bbl and could move higher. Even when crude oil touched its one-year highs in March 2023, jet fuel crack spreads were around $30/bbl, indicating that there is the possibility that jet fuel prices could move even higher than they did during the pandemic recovery. In the third quarter of 2022, United paid $3.81/gal for jet fuel. United has long paid the most per gallon of the big four U.S. airlines, a reflection of the size of its operations in the Northeast U.S. and its lack of fuel hedging or cost reduction efforts such as Delta's refinery. By the fourth quarter of 2022, UAL's fuel price had eased to $3.54/gallon. If fuel prices increase even as demand decreases, UAL's profits could tumble.

In addition to higher fuel costs on the horizon, United also faces higher labor costs. United pilots are currently deciding whether to accept the contract proposal endorsed by their union leadership that would increase pay and benefits by $10 billion over the four year contract including retroactive pay that covers the pandemic period. UAL has taken the appropriate accounting adjustments for its increased pilot expenses but pilot wages will be much higher now than when fuel spiked last summer. In addition, United has not reached an agreement with its flight attendants on a new post-pandemic contract. Delta is the only one of the big 4 airlines that has hiked the pay of its flight attendants including adding pay during the boarding process for the first time; most U.S. airlines have not paid cockpit or cabin crew members during boarding or flight preparation but rather only when the aircraft door was closed.

Delta changed the paradigm, which will particularly benefit junior flight attendants who often work shorter flights and spend more of their workday on the ground rather than in the air. American has made an offer to its flight attendant union that essentially matches Delta's pay rates and major proposals including boarding pay and Delta's higher profit-sharing formulae but the AAL flight attendants have not adopted the company proposal. Each of AAL, DAL and UAL employ more than 20,000 flight attendants which could add another billion dollars per year to each of the big 4's labor costs. Southwest has not lifted the pay of either its pilots or flight attendants.

A Changing Revenue Environment

While cost increases are troublesome, the potential for a weakening revenue environment creates concern for some airline investors. United has both reasons for optimism but also concern.

Like American and Delta, United caters to premium passengers that pay for a higher caliber of service than the low cost carriers provide. UAL's revenue guidance reflected much less concern about a weaker revenue environment than low cost carriers including LUV expect for the third quarter. Nonetheless, inflation, rising interest rates, the restarting of student loan payments, and greater labor unrest outside of the industry including the UAW strike which have ripple effects throughout the U.S. economy are bound to impact the big 3 global carriers; while they cater to passengers that pay more, those airlines fill many seats with leisure passengers that could potentially have much less to spend, including leisure travel by their business customers. Domestically, the big 3 are less vulnerable to a degradation of the fare environment than low cost carriers.

However, United does have a high degree of vulnerability to a decrease in the international revenue environment. United's post-pandemic strength came from the international marketplace where it was first able to capture postponed transatlantic trips amid a reduced presence of transatlantic low fare carriers. European demand this past summer has been described by many carriers as particularly strong with reports of high costs in Europe despite the relatively strong U.S. dollar which will mute demand from Europe to the U.S. during the winter. While several carriers including United report that the normal summer travel period is stretching later into the fall and beginning earlier in the spring, there is a growing expectation that travel demand will return to normal levels. The need to increase international air fares in the off-peak periods could lead to reduced levels of surplus demand outside of the traditional peak periods.

United faces several competitive and regional challenges across its international network. United has been the largest carrier across the Pacific, regardless of nationality, for a number of years. The Asian market was much slower to reopen than Europe and many major markets such as Japan only began to see the normalization of demand levels this past summer. The Japanese Yen is considerably weaker now than it was pre-covid, limiting the ability of Japanese tourists to travel to the U.S.; there is more transpacific capacity between Japan and the U.S. than for any other country, partly the result of Tokyo's historic role as a major connecting hub for the region. United says Japanese demand is returning but they are funneling large amounts of connecting traffic over All Nippon Airways, their Japanese joint venture partner.

United was the largest carrier between the U.S. and China pre-COVID, but draconian limits on the number of flights imposed by the Chinese government has reduced each of the big 3 U.S. carriers to just 4 flights/week between the U.S. and China. China is allowing a further expansion this fall and all 3 carriers are eyeing significant expansions, petitioning the U.S. DOT for the more than double the number of flights they operate. United is focusing its efforts on gaining the right to reinstate San Francisco service on a daily basis to both Beijing and Shanghai. Since the pandemic started, U.S. airlines have used their limited number of flights just to serve Shanghai. Fares between the U.S. and China are at historically high levels so the Chinese government loosening will help ease fares but only about the Chinese are only allowing a return of about 25% of pre-pandemic capacity so fares will remain much higher than they were pre-pandemic. Because of the strict Chinese capacity controls, significant amounts of traffic has connected over other gateways including Japan and so the slow addition of capacity to Japan will partially weaken the revenue environment in other markets; United serves a number of other markets and has announced expansion of transpacific services this winter, opposite of when northern hemisphere flights are usually started.

Latin America traffic neither fell during the pandemic as far as to Europe or Asia and promises to not rebound as strongly; many Latin American economies, especially in Central America and the Caribbean, remained open during the pandemic and benefitted from increased tourist traffic as other parts of the world remained open. Competitively, United faces a more challenging environment as Aeromexico and Latam, both Delta joint venture partners, rebuild following their restructurings under U.S. bankruptcy laws.

United has traditionally been the second-largest U.S. airline to Latin America, but Delta is likely to displace United as the two Latin carriers cooperate more closely with Delta and expand post-pandemic and post-restructuring. In addition, Mexico just regained its high level status for aviation safety which limited airlines from that country to expand in the U.S. for the past several years. There has been rapid growth by Mexican low cost carriers and United's position could be weakened by its weaker position in the region as a whole and by weaker partners.

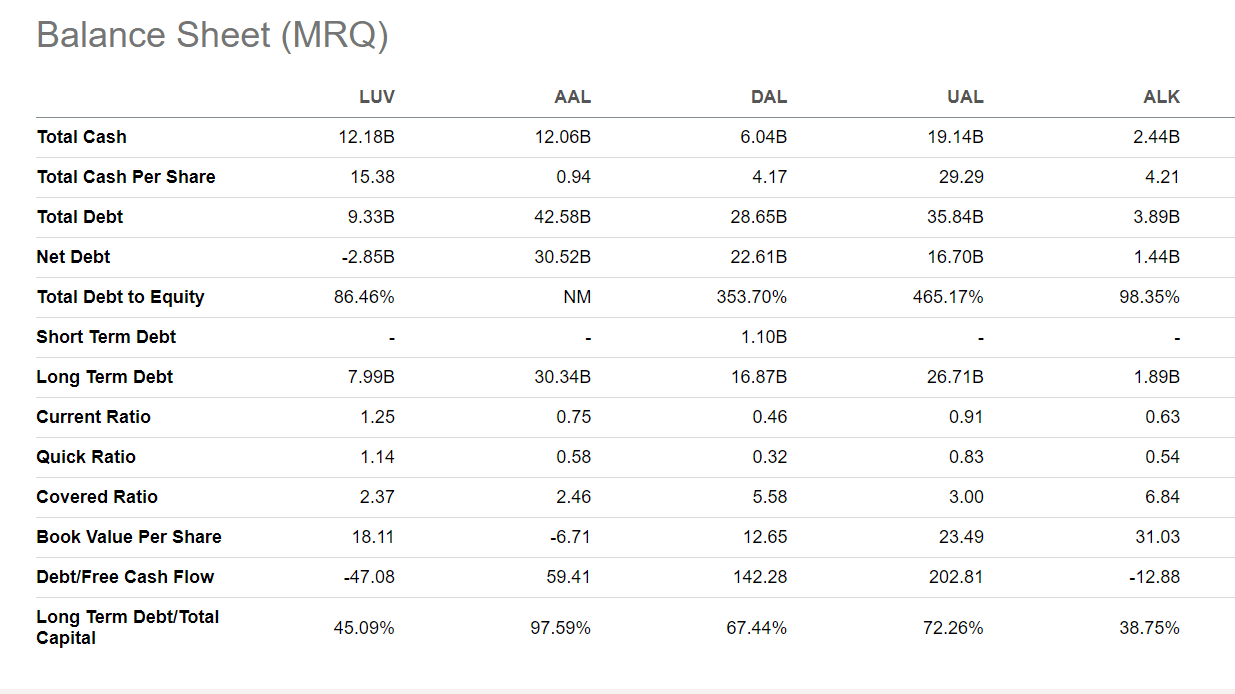

The DOT has released profitability data by global region through the second quarter of 2023 for the four U.S. airlines that operate long haul international flights and United's international strategies have not been near as successful as Delta's in terms of profit generation. While many people argue that airlines can report costs and revenues differently, there is much more uniformity than some might expect and, more importantly, the total for each region has to sum up to the total for the company on a global basis. UAL for years has been willing to settle for lower profits in exchange for larger size.

AAL - Latin America $336 million profit, Atlantic $52 million profit, Pacific $52 million loss; DAL - Latin America $124M profit, Atlantic - $530M profit, Pacific - $104M profit HA - Pacific - $5.5 million loss; UAL - Latin - $74M profit, Atlantic - $305M profit, Pacific, $116M profit.

Delta was more profitable than United flying both to Latin America and across the Atlantic. United's profit on the Pacific was just 10% larger than Delta even though United's Pacific revenue was almost exactly twice as much as Delta.

{kind=link}

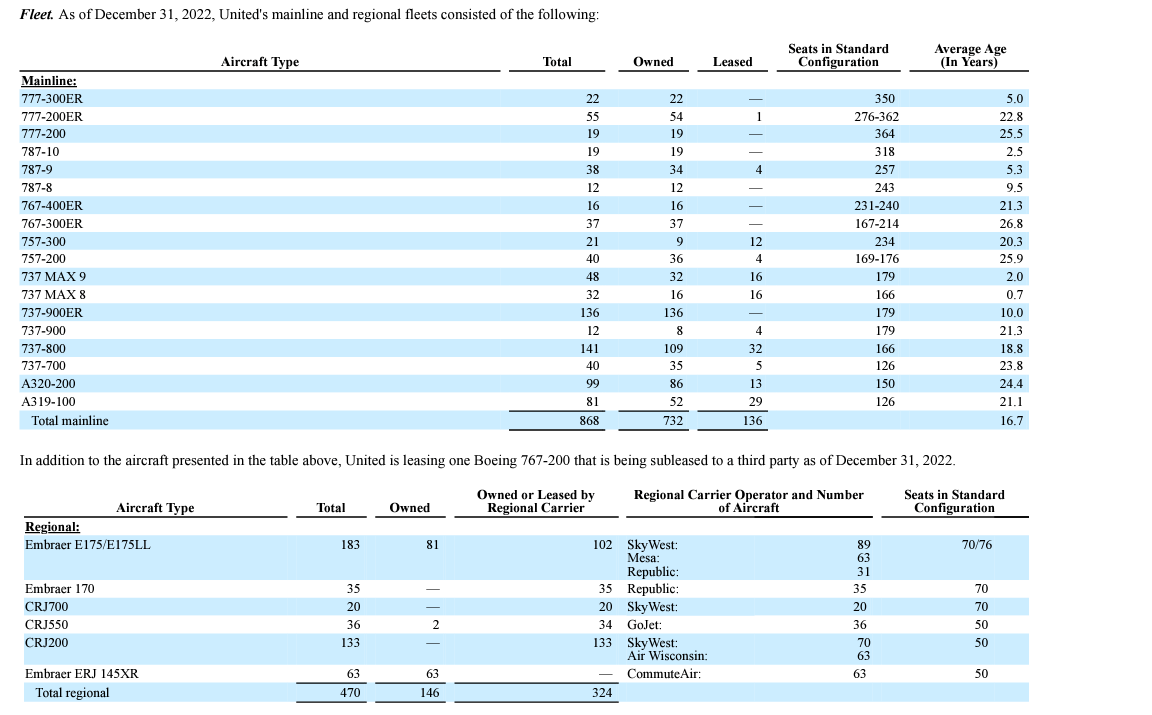

Risky fleet strategies

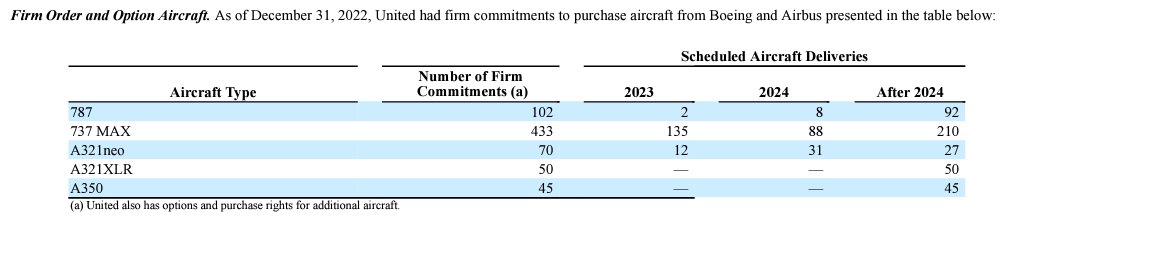

United's biggest risk relative to its competitors is its high capex, driven by its intention to grow its network. More than three times larger than its nearest competitor's order book, UAL plans to spend a whopping $50 billion on new aircraft over the next 7-10 years, far more than any other U.S. airline has ever spent. Both in terms of sheer numbers of aircraft and in the complexity of its plans, UAL's fleet spending is unprecedented.

{kind=link}

{kind=link}

Internationally, UAL committed to an order for 100 Boeing ( BA ) 787s, the first of which are just now arriving. UAL is one of a handful of airlines that operate all 3 variants of the 787 from the initial 787-8 which seats 240-250 passengers depending on configuration to the -9, the longest range model with approximately 265 seats, and the 787-10, the largest model at ~315 seats; -10 has less range than the - 9 but outstanding economics with enough range to comfortably fly 12-hour flights. UAL operates one of the longest current -10 flights from Chicago to Tokyo at more than 12 hours at certain times of the year.

Domestically, UAL is the smallest of the big 4 in terms of passengers carried and smaller than AAL and DAL in domestic revenue, a result of predecessor airline Continental's heavy use of regional jets and small market shares outside of its hubs. UAL is determined to correct its domestic weakness and is committed to using large portions of its order book for growth, adding hundreds of aircraft to its fleet.

While some of those new domestic aircraft will be for growth, many will be replacements of regional jets, including 50 seat regional jets; United contracts for the largest number of 50 seat regional jets in the world. The economics of small regional jets, including UAL's CRJ550s which are 70 passenger aircraft which have been retrofitted to 50 seats including first and extra space economy classes, have deteriorated dramatically as pilot and fuel costs have increased. While UAL has now outlined firm plans to retire large portions its regional jet fleet, many of those aircraft are reaching the end of their life. Because of U.S. airline scope requirements, new generation regional jets cannot be used as contracted aircraft for U.S. airlines so the fuel economy of regional jet will continue to deteriorate relative to narrowbody mainline aircraft. In addition, mainline aircraft are more efficient from a labor standpoint as 2 pilots are required for all commercial aircraft; even at higher rates for mainline aircraft, there is much greater labor efficiency in the cockpit as well as for ground staff working an aircraft that can hold 140-200 passengers than 50-70 passengers.

Part of UAL's fleet challenge is that it operates large numbers of older aircraft. United currently operates the oldest fleet among large jet U.S. carriers. While aircraft can be maintained to remain in service for years, economics favor newer aircraft as maintenance costs increase with age and as fuel prices favor the use of newer technology aircraft. International aircraft have larger fuel efficiency gains going from one generation to the next and also benefit more from new airframe technology such as carbon fiber reinforced polymer -CFRP- construction which the A350 and B787 have.

Even with its massive fleet replacement and growth plans, UAL will still large portions of its fleet that will not be as efficient as competitors. UAL, like AAL, ordered Boeing 777-300ER aircraft near the end of the production line, which Boeing intended at the time to bridge the gap to the B777X, which will be the largest twinjet ever and will have a CFRP wing but a traditional metal fuselage. UAL has not ordered the B777X and so will have 777s well into the 2030s as competitors replace their 777 fleets with newer and more fuel-efficient aircraft.

The greatest risk for UAL's fleet plan is that interest rates are increasing and the Fed indicates they may remain so for much longer than expected. UAL has used portions of the cash it accumulated during the pandemic to help supplement its cash flow but it will soon reach a point where its levels of fleet spending - more than $8 billion/year - will far outstrip its cash generation, requiring the addition of debt. In addition, UAL has committed to a number of airport terminal upgrades which will also be costly; many of its airport terminals as configured cannot accommodate the number of flights or the number of mainline aircraft that UAL anticipates so UAL will be increasing its debt if it finances its own terminals or increasing its airport rental costs much more than competitors if airports build facilities, which is the norm in the U.S. airline industry.

The bottom line is that UAL might not grow its fleet near as much as it says it will but its fleet spending will remain very high for years, debt will increase, heightened by terminal projects, and UAL will still not gain fuel efficiency levels as great as many of its competitors unless it begins to retire many of its less fuel efficient fleets, something it says it will not do for years.

One final source of fleet-related vulnerability for UAL is its dependence on the Boeing 737 MAX 10 in its fleet expansion and replacement plan. The MAX 10 is the largest of the Boeing 737 MAX family and is intended to compete with the Airbus A321NEO, which has taken the lion's share of orders for large, new generation aircraft. United was very slow to order the A321NEO, but will be receiving its first copies in the next few months. Still, UAL has committed to the MAX 10 and will use it on domestic routes with some of the aircraft configured with lie flat seating which is competitively necessary in long haul domestic routes, including from the Northeast to the west coast.

Certification of the MAX 7, the smallest model of the family, and the MAX 10 have been delayed due to concerns from the FAA about the MAX family as a result of the two fatal foreign carrier crashes that resulted in the grounding of the global MAX fleet but also of the entire certification process, in which Boeing has been allowed to self-certify many processes over which the FAA wants greater control.

United has been converting some of its MAX 10 orders to the smaller MAX 8 and MAX 9 models in a process similar to what Southwest is doing for the MAX 7 which is delayed even longer than the MAX 10. However, there is a lead time for airlines to switch models in the family and UAL and LUV along with Boeing continue to base their plans on BA's best estimates of when they complete the certification process. The MAX 7 will be the first of the two models to be certified and certification could come later his year with deliveries to Southwest in the first half of 2024 and entry into service shortly thereafter. While getting the MAX 7 certified should help clear the roadblocks to MAX 10 certification, the MAX 10 will not likely enter service in 2024 or at least not until late in the year. As with the MAX 7, there are MAX 10s that are already built, so Boeing will begin to delivering some of those aircraft fairly quickly, but there will still be a lag until Boeing can right size the MAX family order book for United.

{kind=link}

{kind=link}

Conclusion

United financially benefitted relative to its competitors in 2022 because of its decision to not retire aircraft during the pandemic. It was able to quickly respond to a massive return of demand both in the domestic and later the international markets. However, as oil prices once again surge, very likely headed for over $100/bbl, and as demand weakens, both because of higher interest rates worldwide and because of growing fears of recession, and as UAL's massive fleet spending plan takes larger and larger portions of its earnings to service debt, UAL could quickly move from being one of the airline industry's darlings from a stock performance standpoint to one of its weakest players.

For further details see:

United Airlines Is The Industry's Most Vulnerable Player (Rating Downgrade)