UAL - United Airlines: Lack Of Faith

2023-12-01 11:08:10 ET

Summary

- United Airlines Holdings, Inc. has maintained strong profit forecasts despite market skepticism.

- The airline reported a strong Q3 profit and is expected to earn nearly $10 per share in 2023.

- The market undervalues the stock, trading at just 11x the Q3 EPS alone and nearly 3x 2023 EPS targets.

The airlines have a solid history of reporting strong profits now, but the market is still acting like 2020 is more the norm. United Airlines Holdings, Inc. ( UAL ) has maintained strong profit forecasts due to a focus on International travel, yet the market doesn't care. My investment thesis remains ultra Bullish on the airline stock not being given credit for massive ongoing profits.

Source: Finviz

Profit Machine

While some airlines have struggled due to issues with domestic capacity and higher fuel costs, United Airlines has maintained rather robust EPS forecasts. Our investment case for a double made when the stock traded above $50 isn't altered by the current turbulence in the sector, yet the stock is far lower now.

United Airlines just reported a quarter where the airline reported a $3.65 EPS for just Q3 alone. The stock currently trades at just 11x the one quarterly EPS alone.

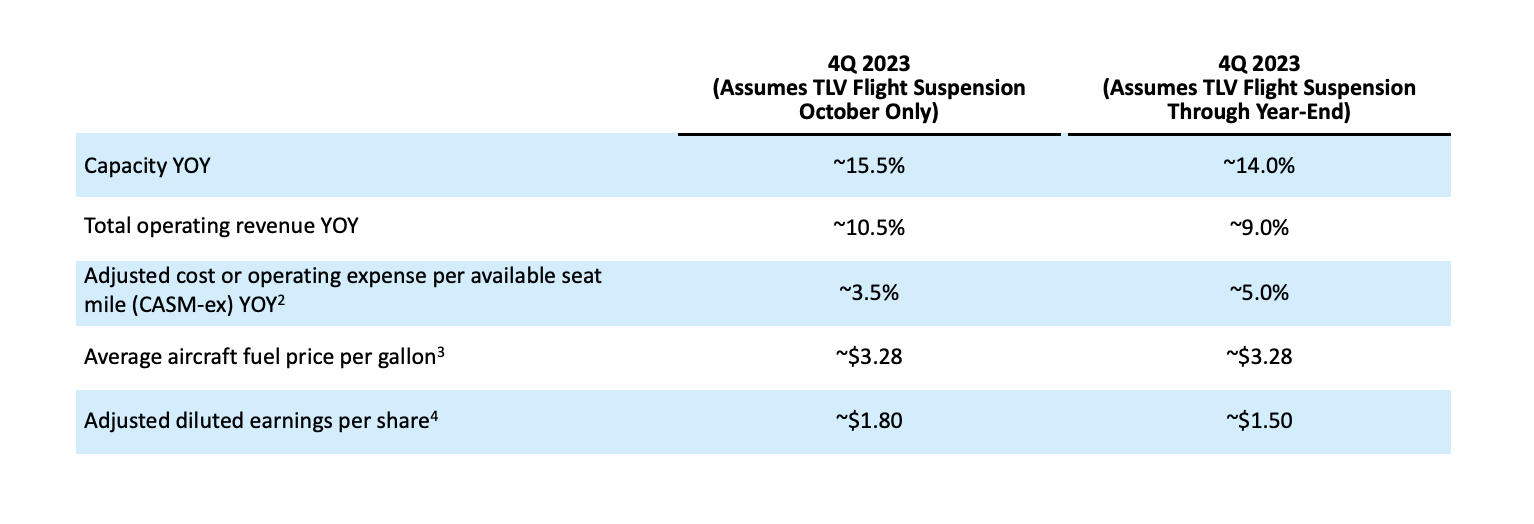

Remember, Q3 wasn't even the best quarter with United Airlines earning $5.03 per share in Q2'23. The airline even forecast a Q4 EPS of $1.50, with a shutdown of travel to Tel Aviv in Israel for the whole quarter, which appears the case now.

{kind=link}

United Airlines is on a path to earning nearly $10 per share in 2023 with similar expectations for 2024. The airline would have to see far worse operating results to warrant the current price, considering the benefit from repaying debt and lowering interest expenses from over $3 billion in annual profits.

The stock trades at hardy 3x EPS targets due to investors not trusting the ability of an airline to consistently generate profits. The reason the legacy airlines were buying large amounts of stock prior to Covid was this disconnect with the reality of financial discipline in the sector.

Economist Clifford Winston summed up the current market view of airlines with this statement back in January:

The airline industry has periods of fat profits, but those profits are notoriously fickle. And if they’re expected to stay in business in down times, airlines can’t be expected to sacrifice revenue generated when demand is high without trying to make it up elsewhere.

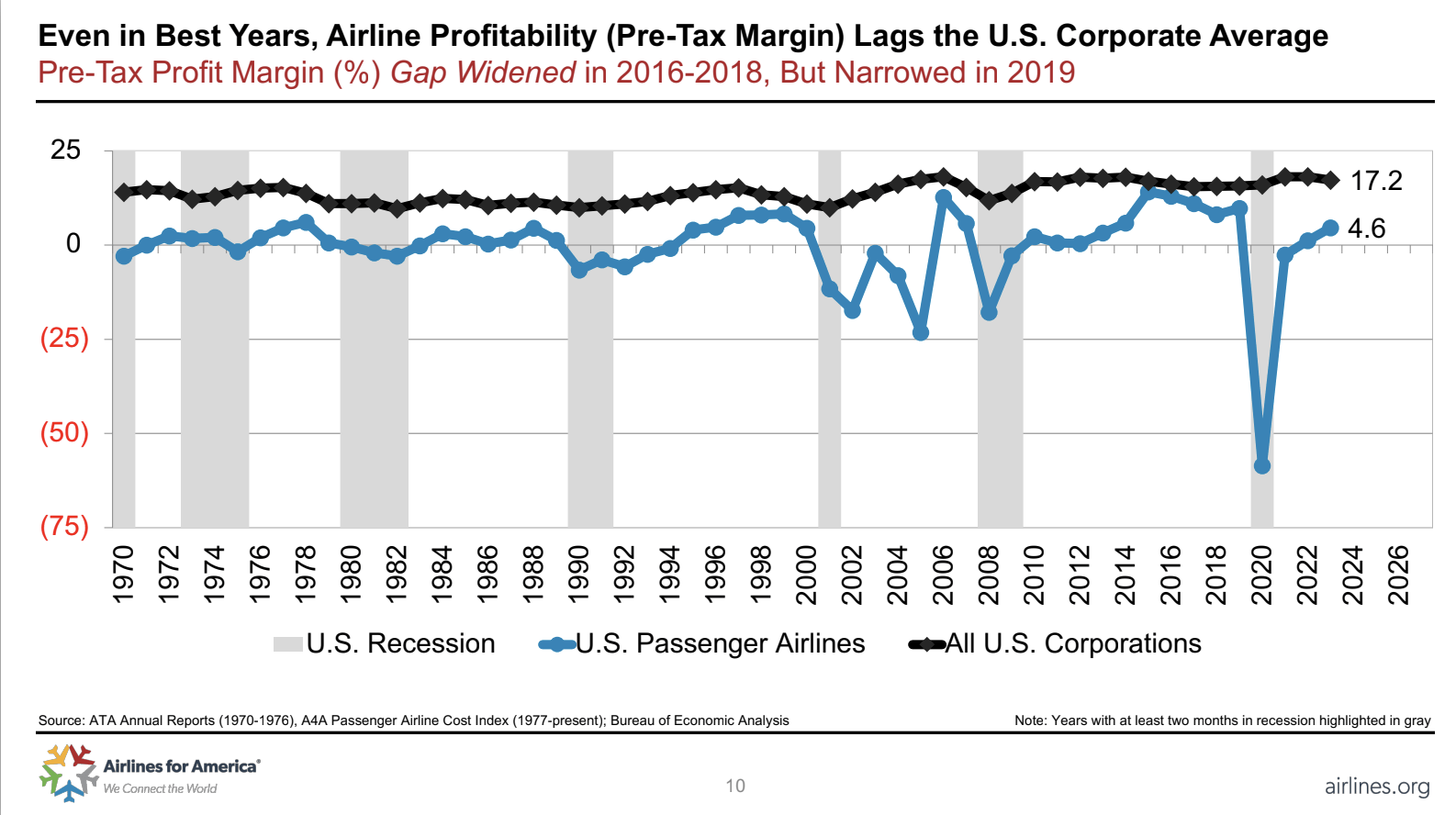

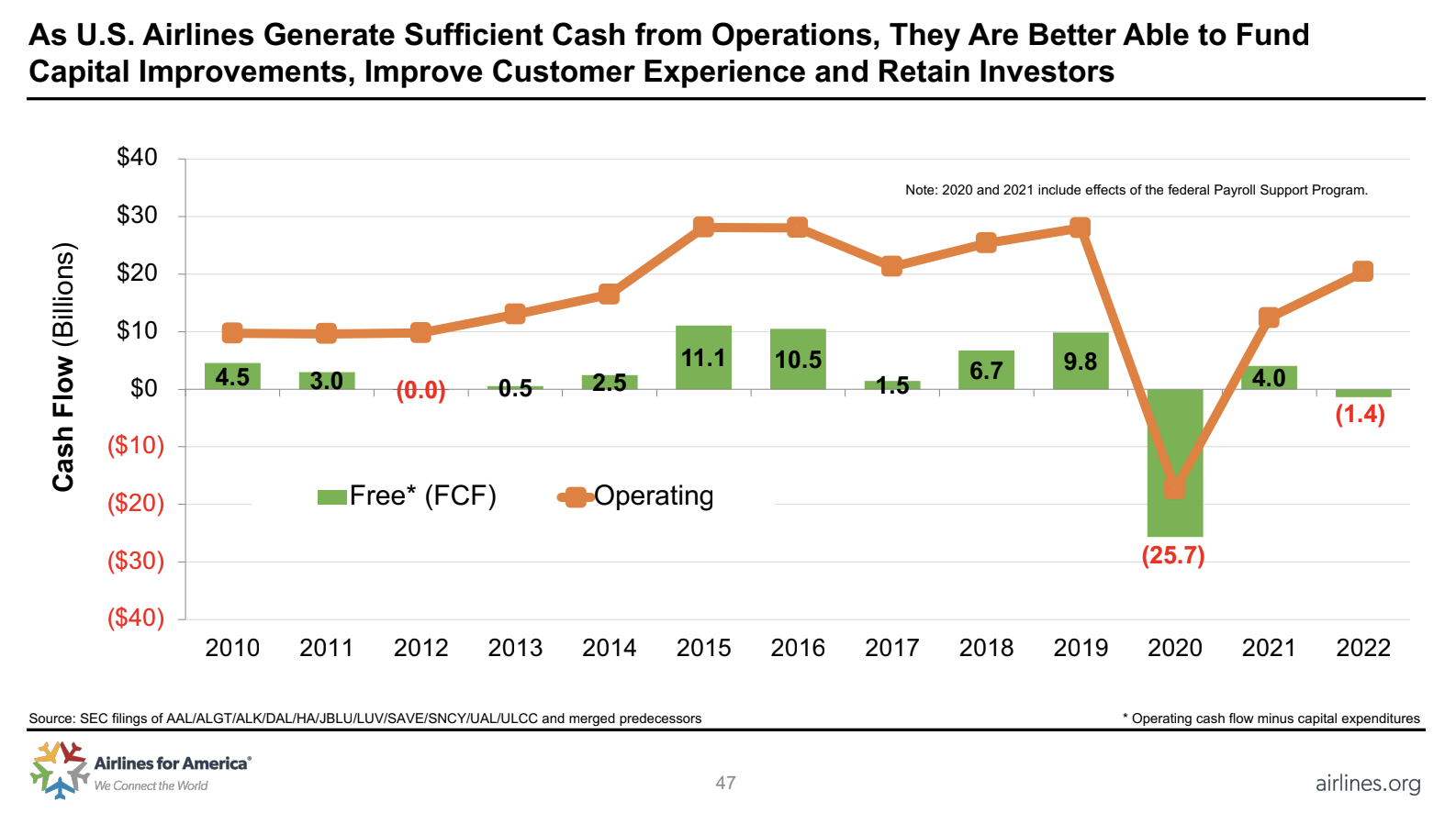

Going back to 2010, the market data just doesn't agree with this view. Outside of the Covid period where the governments around the world shut down the world, airlines have been extremely profitable, especially starting around 2014.

{kind=link}

The consolidation of legacy airlines and better discipline in the sector has made the airlines far more profitable now. Even at higher fuel prices, the sector was very profitable due to adjusting fares to match higher costs.

From 2015 to 2019, the U.S. airline sector created nearly $40 billion in total free cash flow. The sector generated $30 billion in operating cash flows in 2019 alone before Covid hit travel demand.

{kind=link}

An investor has to ask whether the view of Clifford Winston, a senior fellow at the Brookings Institute, is still accurate in light of over a decade of counter information, or if the airlines are really headed right into another cycle of self inflicted wounds. The industry is far different now with Raymond James predicting airlines adjust capacity in 2024 to meet demand.

At least the fuel costs aren't the issue forecast back in October. United predicted a fuel cost per gallon of $3.28 and prices have collapsed from these near record levels to only $2.62 per gallon with WTI down to mid-$70s/bbl.

Debit Issue Quickly Resolved

The only way United Airlines is currently correctly valued is a scenario where profits plunge and the airline is hardly profitable in the future. The airline now generates the type of profits to where debt will be repaid and the end result will be returning cash flows to shareholders under a scenario where the airline has access to capital on any shutdown of the industry again.

Under Airlines has already cut net debt levels to only $12.5 billion. The amount is only slightly above the pre-Covid levels, especially for an airline with annual operating cash flows in the $9 billion range now.

The market constantly forgets that United Airlines has $38.4 billion in PP&E. Whether or not the airline has free cash flow in the next few years is irrelevant because any cash flow will go towards buying new aircraft. The difference between PP&E and net debt will only widen as the company generates massive profits and cash flows and reinvests a lot into new aircraft.

Takeaway

The key takeaway is that the market clearly lacks faith in airlines generating consistent profits, though no signs exist the industry has strayed from the 2010 path of financial discipline. Investors should continue using weakness to load up on United Airlines.

For further details see:

United Airlines: Lack Of Faith