UAL - United Airlines Looks Undervalued Given Improving Fundamentals

2023-11-24 02:33:44 ET

Summary

- Fears of airlines over-earning, flight attendant and pilot wage increases, business travel not returning, and United’s “United Next” plan have depressed the value of United’s stock.

- The oil market is in backwardation, meaning oil is expected to be cheaper in the future. Jet fuel prices should decrease as a result.

- The jet fuel crack spread is expected to narrow, reducing fuel prices.

- UAL’s intrinsic value is higher than $40/share, so there is asymmetric risk/reward to the upside.

- Applying UAL’s 2019 EV/EBITDAR ratio to expected EBITDAR yields a share price of ~$60/share.

United Airlines Holdings (UAL) has a terrible reputation within the airline industry - think United breaks guitars or the 2017 passenger removal . However, a bad business can be an excellent investment when bought at the right price. I believe that United is undervalued because conservative assumptions yield an intrinsic value close to where United is currently trading. I think the market is mispricing United because of fears over pilot wage increases, fears over business travel not returning, and fears over United's " United Next " plan. While pilot wage increases are concerning, they should be offset by lower jet fuel prices in the future. Also, business travel seems to have returned, and United's commitment to monitoring ROIC should ensure that United Next doesn't destroy value.

Industry

Deregulation

The airline industry is notorious for generating negative alpha. Troubles for major airline carriers began in 1978 when the Airline Deregulation Act was passed. This law prohibited states from regulating the prices and routes of airlines . Soon after this law was passed, low-cost and ultra-low-cost carriers flooded the market, putting significant downward pressure on airfares. Seat capacity increased rapidly in the 80s and 90s because barriers to entry were low.

More than 100 US airlines have gone bankrupt since the industry was deregulated because of little to no capacity discipline. Airlines would increase capacity when demand increased but could not adjust capacity when demand decreased (can't get rid of airplanes overnight).

Airlines Today

Bankruptcies and airline consolidation in the 2000s have made major airlines investable again. The four largest air carriers in the US now control 80% of the market , and people now talk about ROIC and capacity discipline. Charlie Munger also recognized the shift in the airline business during a 2017 meeting :

You know we said, "Railroads are no damn good, you know. Too many of them. Truck competition." And we were right. It was a terrible business for about 80 years. But finally, they got down to four big railroads, and it was a better business. And something similar is happening in the airline business.

Airline fundamentals are also stronger because load factors have increased from ~70% in the 1990s to ~80% in the 2010s. Additionally, the major airlines are now "too big to fail," so a government backstop exists during crises. For example, the CARES Act of 2020 granted airlines $50 billion in grants and loans, and airlines received a $15 billion bailout following 9/11.

Business models in the airline industry have also shifted over time. Airlines now make significant revenue from frequent flier programs and credit card companies (some argue frequent flier programs are worth more than airlines themselves). Credit card companies buy airline points/miles and award them to customers.

Airline demand is also expected to be healthy over the next decade. The IATA expects demand for air travel to double by 2040 (origin-passengers are expected to increase from ~4 million to ~8 million), resulting in a 3.4% CAGR. If inflation reverts to 2%, the airline industry will grow 5.4% annually over the next two decades. United's management seemed to agree with this number in UAL's latest conference call , given the following comment from CEO Scott Kirby:

I'll continue closely tracking the airline industry revenue to GDP relationship. I've talked about this in the past. That ratio declined by approximately 35% in the past few decades. I don't think we'll make all that up, but almost everything we do make up goes straight to the bottom line.

Management seems to be expecting profitable "catch-up growth," which the market currently doesn't seem to be pricing in (current EV/EBITDAR is 4.26 vs. 5.66 in 2019).

Other factors also make major airlines investable:

- Airport slots are difficult to get

- There's a 20% price premium in airports where a legacy carrier dominates the majority of traffic

- Only two new airlines have launched in the past 15 years

- There is no close substitute for the service (air travel is much quicker than other transportation)

UAL Overview

Recent History

United Airlines filed for Chapter 11 bankruptcy in 2002, canceled their common stock, and didn't exit bankruptcy until 2006. The bankruptcy was a result of several factors:

- United aggressively increased capacity during the dot com boom, resulting in higher fixed costs

- 9/11, which drastically reduced business travel. United laid off nearly 20,000 workers following 9/11

- Rising fuel costs

United then merged with Continental in 2012 to create one of the largest airlines in the United States. At the time, both airlines reported losses because of the GFC. Additionally, analysts projected the deal to create more than $1.2 billion in value .

Business Model

United Airlines has a hub-and-spoke model where all flights fly into a "hub" (Example: Chicago O'Hare airport) and out of the hub. This model allows United to offer more frequent flights to more locations versus a point-to-point model adopted by low-cost and ultra-low-cost airlines (which may service routes a few times a week). United's most noteworthy hubs are Newark Liberty International Airport, Chicago-O'Hare International Airport, Denver International Airport, and San Francisco International Airport.

The hub-and-spoke model appeals to business travelers because business travelers must travel on short notice. Additionally, business travelers often want to return within a few hours of completing a business meeting.

Business Travel

Many analysts have predicted that business travel will be 15-20% lower post-COVID because of virtual meetings. For example, Morgan Stanley expects 18% of corporate travel to be replaced by virtual meetings. A decline of this size would be catastrophic for airlines because business class seats can be 5x as profitable as economy seats. However, business travel seems to have rebounded, given some of the comments made during UAL's Q1 and Q2 conference call:

Q1: "So, in Q4, the revenue recovery rate was between 70% and 85% for these three categories. In Q1, the revenue recovery rate for these three measurements ranges from 85% to 97%. And for the first two weeks of April, the recovery ranged from 95% to 101%. I think this data in the last two weeks of April was a surprise to us as we have seen more conservative measurements start to approach 100%. The fact that large corporations are getting close to 100% is a nice tailwind to United."

Q2: "On a ticketed basis, business travel revenue continues to trend roughly flat to 2019."

Deloitte also aligns with the business travel recovery narrative. Deloitte expects business travel to revert to pre-pandemic levels by 2024 or early 2025.

Business travel fully recovering makes sense because client acquisition and connecting with others at conferences is less effective when done virtually. People also used to think that telecommunications would destroy business travel, but this never happened.

United Next

United has 700 firm orders for new narrow and widebody aircrafts, expected to be delivered between now and 2033. As part of the United Next plan, United is increasing average seats per departure by >40%. Given the current pilot shortage, increasing plane capacity is a sensible way to grow. United has also cited limitations on airport gates and shortages of air traffic controllers as reasons to increase seat capacity rather than add new flights.

However, United has received pushback for its plan. Ordering new planes is expensive and will require United to spend more on flight training. However, better fuel efficiency should offset increased CapEx and expenses (newer aircraft are more fuel efficient). Also, in the latest earnings call , management claimed they're monitoring their operating margins and ROIC. United Next should generate shareholder value if the corporate finance department is somewhat competent.

Premium Shift

Management noted that first-class seats are expected to increase from 9 per departure in 2019 to 16 in 2027. Additionally, management has emphasized the success of United's premium plus segmentation because the premium plus cabin is the most profitable.

Competitiveness with Low-Cost Carriers

Andrew Nocella argued that UAL is more competitive with low-cost carriers in UAL's latest conference call for the following reasons:

- The cost gap between low-cost carriers and United is shrinking

- Saturation of low-cost carriers in certain regions, creating low marginal RASMs for competitors

- United's focus on domestic gauge (number of seats) should mean that United will "no longer spill as much revenue to others…"

Low-cost carriers are also weaker , relative to United, for other reasons. For example, operating expenses as a percentage of revenue have declined (vs. 2019) for major airlines but have risen for ULCCs (partly because major airlines are shifting toward premium cabins - something that low-cost carriers are missing). Higher oil prices and the recent pilot shortage should also hit low-cost carriers harder.

Pilot Shortage

The airline industry is experiencing a pilot shortage, which may worsen, given that 50% of commercial airline pilots will be forced to retire over the next 15 years. Pilot salaries have sharply increased across the industry - in particular, United pilots recently got a 40% pay increase.

Jet Fuel

Oil Price

Using the Brent curve from TradingView , oil is expected to decline from ~$80/barrel to ~$67/barrel in 2030. However, the 30-year inflation-adjusted oil price is ~$74/barrel (~$92/barrel in 2033 adjusting for expected inflation ).

Crack Spread

The jet fuel crack spread is currently ~$33 , but the 30-year inflation-adjusted crack spread is ~$15/barrel (~$19/barrel in 2033, adjusting for expected inflation ). The crack spread is unusually wide because abnormal circumstances pushed the crack spread up. Net global refining capacity declined in 2021 for the first time in 30 years, while air travel rebounded. Lower supply and increased jet fuel demand pushed the price to elevated levels.

Given that net global refining capacity is supposed to grow in 2023, and airline travel demand is expected to stabilize, I expect the crack spread to narrow to ~$15/barrel (~$19 inflation-adjusted). The IATA expects the crack spread to narrow to 23% ($17.02/barrel with $74 oil).

However, the crack spread has widened since that forecast because of a lack of infrastructure investment and demand for other middle distillate fuels. Using the futures curve from TradingView , the crack spread is expected to narrow to ~$25 by late 2025.

In my valuation, I assume that oil and the jet fuel crack spread both mean revert. Using the futures curve for the crack spread and oil should produce a similar result because oil is expected to be lower than its 30-year average, but the crack spread is expected to be higher than its 30-year average.

Valuation

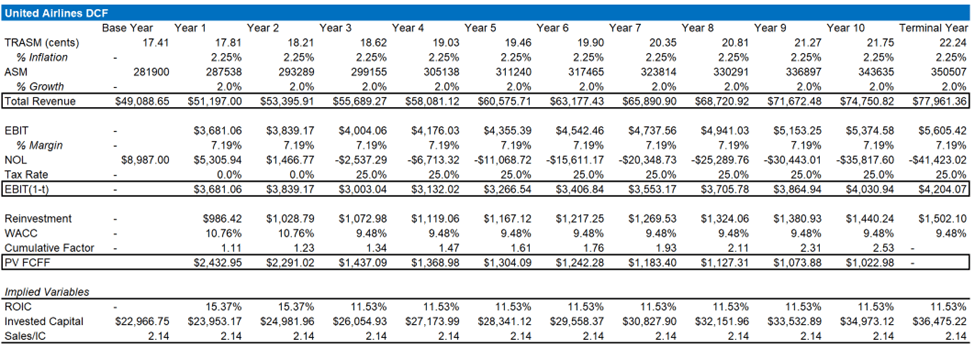

DCF #1: Historical Case

Author's Calculations Author's Calculations S&P Capital IQ

{kind=link}

{kind=link}

{kind=link}

The purpose of this valuation is to provide a lower bound on UAL's intrinsic value. Also, this valuation attempts to value UAL across the business cycle by including the GFC. I use UAL's average EBIT margin from 2006-2025E (7.19%), excluding 2020, because the industry was far more competitive before 2006, and 2020 was a once-in-a-lifetime shock. Using 7.19% should be too conservative because the industry was less consolidated and less focused on ROIC during the earlier part of the chosen period. Additionally, United incurred merger-related costs when the company merged with Continental.

TRASM (base year): 2019 + ~15% inflation (I used 2019 as my starting point because UAL is currently over-earning). Using this methodology, my base year TRASM is similar to UAL's current TRASM (17.41 cents projected vs. LTM TRASM of 17.96 cents), so United is moderately over-earning .

ASM Growth: 2012-2019 Average (~2%)

EBIT Margins: Cumulative 2006-2025E EBIT margin (sum of operating income divided by sum of revenue), Ex. 2020

Tax Rate: Worldwide average tax rate

Reinvestment: Historical average (Sales/(Invested Capital) ratio) - I assume that United generates $2.14 for every dollar invested in the business, so United must invest ~47 cents for every dollar in revenue growth.

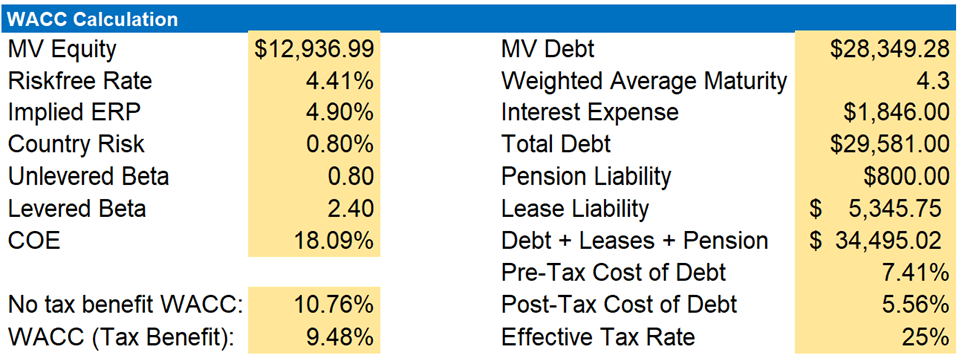

WACC: 7.41% pre-tax cost of debt (Yield to maturity on 2029 bonds). WACC is initially higher because there's no tax benefit due to NOLs

UAL Investor Relations S&P Capital IQ

{kind=link}

{kind=link}

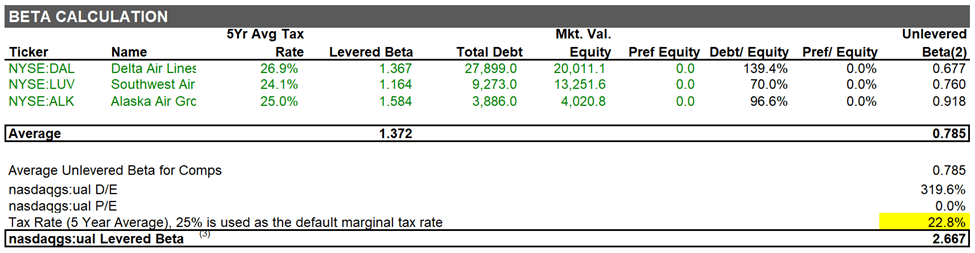

Note: Aswath Damodaran estimates that airlines have unlevered betas of 0.7. I include a scenario analysis later in this write-up.

Debt: I estimate the market value of debt here . I include pension liability in debt.

Terminal ROIC: I assume 1% excess returns because of industry consolidation

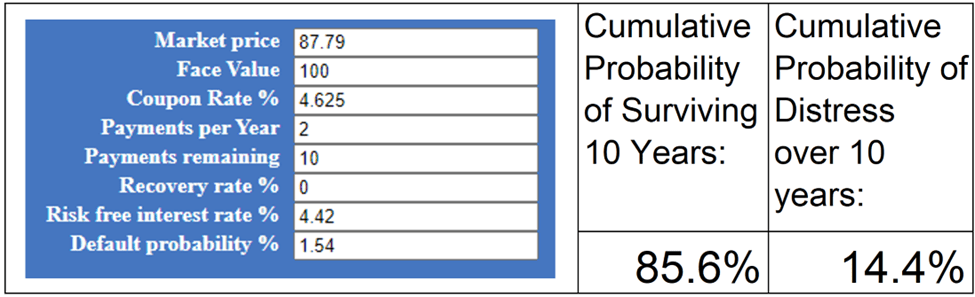

Failure Risk: I calculated the 10-year cumulative probability of default ( Aswath Damodaran's method ). Probability of surviving ten years: (1-(default probability))^10.

{kind=link}

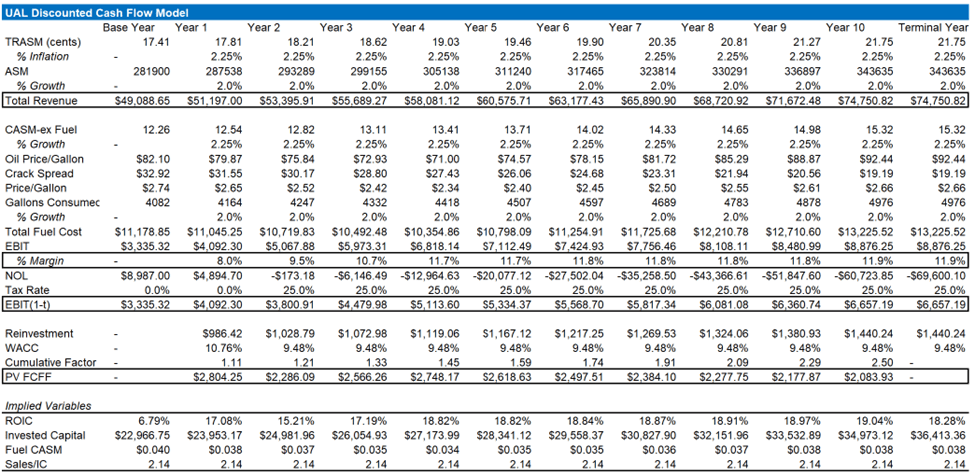

DCF #2: No Recession Scenario

Author's Calculations Author's Calculations

{kind=link}

{kind=link}

$106.12/share is unrealistic because it assumes 2019 conditions in perpetuity. In reality, the economy will slow down during certain periods, so United's margins across the business cycle should be lower than 12%.

TRASM, ASM, WACC, Reinvestment, Failure Risk, and Tax Rate are the same as in the historical case.

Fuel: Using the Brent curve, oil will decrease to ~$70/barrel over the next five years. However, this is below the long-term inflation-adjusted price of Brent, so I model Brent returning to its inflation-adjusted price during years 5-10.

Crack Spread: The jet fuel crack spread sits at ~$30/barrel (30-year inflation-adjusted crack spread is ~$15/barrel). I expect this to narrow as conditions normalize (the crack spread is wide because jet fuel demand suddenly decreased in 2020 and then suddenly increased in 2022). I model the crack spread returning to ~$19/barrel over the next ten years.

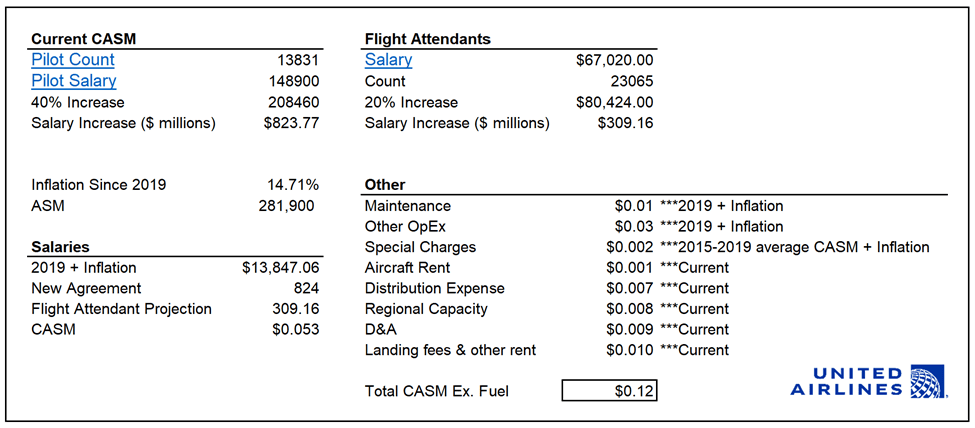

Salaries: UAL pilots recently got a 40% pay raise due to a pilot shortage. I estimate this will cost United ~ $800 million. The flight attendant union also demands a pay raise, so I expect a 20% pay raise (in line with the recent JetBlue pay increase), costing ~$300 million.

Maintenance: Maintenance is inflated because of unusual circumstances, so I base maintenance per available seat mile ((ASM)) off 2019 numbers. The following quote from an FT article describes the current situation well:

"Michaels said three factors were driving the higher spend: airlines investing in discretionary maintenance that had been deferred during the Covid-19 pandemic; older aircraft due for retirement having to fly longer than expected given issues with new generations of engines, as well as supply chain constraints; and inflation as the cost of labor and parts had risen.

Other OpEx: I base this number off 2015-2019 Other OpEx because the current Other OpEx is inflated due to a one-time expense associated with the recent pilot compensation agreement.

CASM-ex Fuel Growth: 2.25% (10-year breakeven inflation rate)

Terminal ROIC: Excess returns of 2.5% assume moderate competitive advantages and excess returns from consolidation

{kind=link}

The graphic above can be found in the OpEx tab of my Excel spreadsheet.

Scenario Analysis

{kind=link}

Some readers may feel uncomfortable with the assumption that United will grow at the 10-year rate (a proxy for the economy's growth rate) in perpetuity. Aswath Damodaran argues that the economy must grow at the 10-year rate . Still, I include a scenario with 0% excess returns because the terminal growth rate doesn't affect intrinsic value when excess returns are 0%. I also included a 5% excess return scenario if readers think United has substantial competitive advantages.

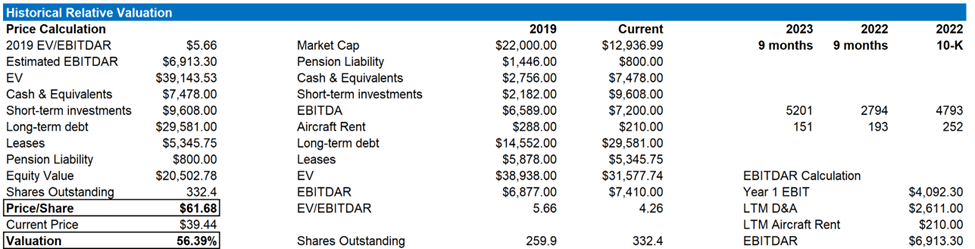

Relative Valuation

{kind=link}

Applying UAL's 2019 EV/EBITDAR ratio to my estimate of EBITDAR (see DCF above for EBIT calculation) yields an expected value of ~$60/share. My view is that UAL deserves a 2019 multiple because most of the market's concerns have been alleviated:

- Cheaper jet fuel prices should offset pilot wage increases

- UAL is only moderately over-earning given that LTM TRASM is 17.96 cents, but I estimate normalized TRASM to be 17.41 cents

- Business travel has already returned

Should a higher discount rate and risk from UAL's United Next plan lead to a $20/share discount (shares are currently $40 vs. my estimate of $60)? I believe the risk/reward associated with United Next makes sense because United has been earning well above its cost of capital. However, it's hard to assess the impact of a higher discount rate when using relative valuation metrics, which is why I made a DCF. Airline discount rates have historically been in the 8-9% range (current is 9.48%), so my view is that the increase in WACC shouldn't lead to a $20/share price discrepancy.

Risks

Macro

United Airlines is a high-beta business (I estimate UAL's levered beta to be 2.66). A recession will significantly reduce United Airlines' intrinsic value, but the market doesn't seem to be pricing in a recession currently. Analysts still estimate earnings for the S&P to grow double digits next year (data retrieved from CapIQ).

United Next Execution

United will have to train pilots and staff on newly ordered planes. In addition, purchasing hundreds of new aircraft should increase CapEx. It's hard to say if increased CapEx and costs will be adequately offset by additional seat revenue and lower fuel costs (what will the ROIC from this project be?).

Conclusion

Given the shift in airline industry fundamentals, buying and holding major airlines like United makes sense. While United looks attractive at current levels, I do not expect the market to revalue United at >$60/share in the short-medium term. However, there seems to be a clear path to $50-$60/share as conditions normalize and investors reassess UAL's risk.

For further details see:

United Airlines Looks Undervalued Given Improving Fundamentals