UAL - United Airlines Q3 Earnings Preview: I See Huge Gains Ahead

2023-10-12 17:30:37 ET

Summary

- Airlines are facing pressure due to concerns about pricing strength, higher oil prices, and increased labor costs.

- United Airlines Holdings, Inc. will report Q3 earnings post-market on October 17th, with analysts expecting revenue growth of nearly 12% and earnings per share of $3.41.

- United Airlines updated its Q3 guidance in September, expecting higher fuel costs.

In April, I marked shares of United Airlines Holdings, Inc. ( UAL ) a buy. Initially, that buy was playing out the way I expected, with the stock appreciating more than 30% and filling around 60% of the upside I saw. However, since then, UAL share prices have sunk due to a combination of concerns on pricing strength and airline cost structures as oil prices headed higher, coupled with higher labor costs. In this report, I will be looking at the updated UAL guidance, offer a preview for Q3, and re-assess my rating on the stock.

Airlines Are Facing Pressure

For airlines, the current environment is a tough one to operate despite demand for air travel remaining high. Generally, we see that on the domestic market, the recovery is complete, which begs the question of how much room there is to extract value from the domestic operations. International operations still have a lot of growth ahead, but we have also seen that oil prices (CL1:COM) have been lifted off their $66 per barrel lows of June to as high as $94 by the end of September, with a current barrel price of $84. So, there is significant fuel price volatility. What also hurts airlines is that labor costs have increased as new labor agreements were announced. Bringing labor, oil prices, and demand together, the big question has become whether a weaker or normalized demand environment can carry the costs of higher oil prices and labor. I would be inclined to say that that is not the case.

Airline crews have rightfully demanded higher pay amidst inflation with sky-high demand strengthening their position at the negotiating table, but those are multi-year agreements based on the strong business environment envisioned in the last years, and one can wonder how prudent those labor agreements will be going forward on a softer demand cycle.

When Will United Airlines Report Q3 Financial Results?

United Airlines will report Q3 earnings on the 17th of October after the closing bell. Since United Airlines did update its Q3 guidance in September to reflect climbing oil prices, the major surprise element seems to be taken out of the equation already.

What Are Analysts Expecting From UAL's Q3 2023 Earnings Report?

{kind=link}

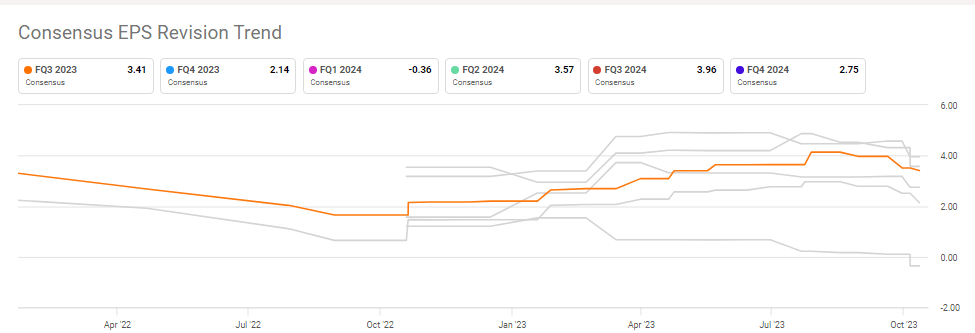

Analysts are expecting revenues of $14.41 billion, indicating nearly 12% growth in revenues year-over-year while earnings per share are expected to be $3.41. Looking at the Q3 2023 EPS estimate development, we see that it has been trending down from roughly $4.14. What we also see in the earnings estimate is that it is down to the range where it was around May-June, which shows that much of the positive view for Q3 has evaporated. The revenue estimates have actually moved very little, indicating that demand is still expected to be robust for United Airlines. For what it is worth it, United Airlines beat analyst expectations 6 out of the 8 previous quarters and missed only two out of 8 quarters, which from previous quarters would indicate there is a high chance United Airlines will beat Q3 estimates. Delta ( DAL ), which kicked off airline earnings season on the 12th of September, also beat estimates raising expectations, and United could do the same.

United Airlines Sees Higher Costs In Q3

United Airlines updated its Q3 guidance in September on the back of rising fuel prices. The company now expects fuel price per gallon to be in the range of $2.95 to $3.05 compared to gallon prices of $2.50 to $2.80. Signs of continued strength are that the revenues are still expected to be up 10 to 13 percent year-over-year, with the note that revenue growth is expected to fall behind capacity growth of 16%. CASM-ex is expected to be up 2 to 3 percent. Previously, United Airlines had guided for earnings per share of $3.85 to $4.35, but the company did not provide any updated guidance to incorporate the higher fuel prices, and these numbers are unlikely to still be valid in the elevated fuel price environment.

While the guidance is generally perceived as negative, we see the strong demand expectations reflected offset by higher fuel. That is really all there is to it. It is not a major change in booking trends that we saw other airlines reporting . United likely is less susceptible to this change in trends on domestic operations because it can lean on growth in the international and long-haul markets and is not solely dependent on the trends in the domestic markets.

What Is United Airlines Stock Worth?

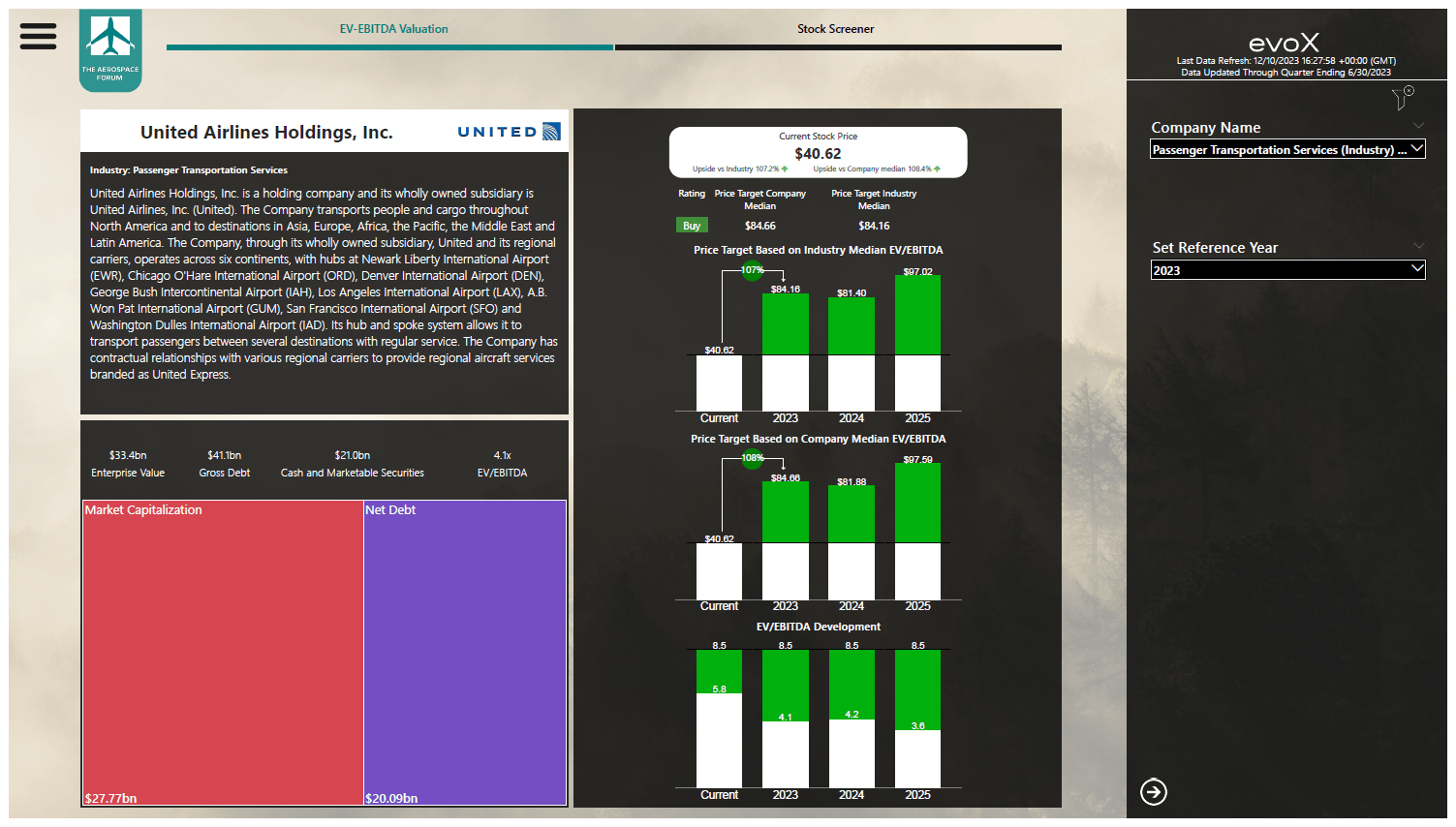

I previously saw around 60% upside, indicative of a $74 price target for United Airlines stock, and it is useful to assess whether that still is the case. The previous estimate was based on a simplified model, so any new upside or absence thereof is not solely driven by a revised estimate on earnings, but also incorporates a more capable estimation tool (available to subscribers) which includes stock price targets and ratings for over 60 (and counting) companies in the airline and aerospace industry as well as closely related companies.

Stock price valuation United Airlines (The Aerospace Forum)

{kind=link}

Interestingly, the renewed model and assumptions show an even higher price target and upside of more than 100%, but this is largely driven by significant multiple expansions towards the company median, which closely coincides with the industry median. Even if we were to fix the company median at the current EV/EBITDA, we would still see 43% upside with a $57 price target. Wall Street analysts have a $63.39 median price target for United Airlines, so I feel more than comfortable with a buy rating on the stock.

What Are The Risks For United Airlines?

The obvious risks for United Airlines and many other airlines are that unit revenues weaken while the companies are facing elevated labor costs and fuel costs. For United Airlines, the additional risk is the company has been ordering hundreds of jets, including a recent order for more than 100 jets.

Conclusion: The Buy Thesis For United Airlines Remains Intact

While there are significant risks to the business, many of which are industry risks, United Airlines still provides significant upside, and that is even when we factor in the higher oil price expectations. So, there is upside to United Airlines, but chances are significant the upside does not materialize due to market fears.

For further details see:

United Airlines Q3 Earnings Preview: I See Huge Gains Ahead