UNFI - United Natural Foods: Some Hope Remaining

2023-09-07 04:56:59 ET

Summary

- United Natural Foods has seen a decline in stock price due to the underperformance of targeted synergies after the SuperValu acquisition, as well as a declining EBIT margin.

- The company still holds a very large debt balance after the acquisition, raising risk levels for investors.

- Despite these challenges, there is potential for improvement through cost savings and potential synergies, making the stock worth watching.

United Natural Foods ( UNFI ) distributes food products to businesses with a focus on natural and organic products. The company's financials have largely been altered by the acquisition of SuperValu in 2018, and as the targeted synergies haven't been met, the stock has seen a large decline in price. Although the company has a significant debt balance and a worsening margin, I have remaining hope for the company with a hold rating.

The Company

United Natural Foods distributes mostly organic and natural grocery items in the United States and Canada - altogether, the company's customers have more than 43,000 locations, according to the company's website. The company provides items from over ten thousand suppliers, including brands such as alter eco, Crofter's, and Nature's Path:

{kind=link}

The company's stock has seen a wide decline in price in the past ten years, as financials haven't performed up to investors' expectations:

{kind=link}

Financials - A Mess After the SuperValu Acquisition

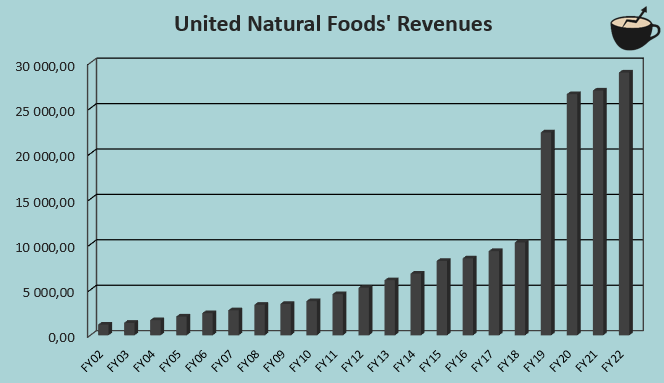

United Natural Foods' revenues have grown quite well in the company's long-term history - prior to the company's acquisition of U.S. food wholesaler SuperValu in FY19, the company achieved a compounded annual growth of 14.5%:

{kind=link}

The acquisition seems to have made the distributor's revenue growth more stagnant - in FY21 and FY22 the company's growth rates were 1.5% and 7.3% respectively , with the middle point of the current guidance representing a growth of 4.7% in FY23, significantly below the growth levels prior to the acquisition.

As the SuperValu acquisition was made, United Natural Foods communicated that the two companies would achieve great synergies through an integration of the separate companies' offerings:

UNFI's and SuperValu's Cross-Selling (SuperValu Acquisition Presentation)

{kind=link}

More than just cross-selling, synergies were told to happen through an improved supply chain, the consolidation of certain infrastructure, and further efficiencies in SG&A as well as an expanded gross margin with improved logistics; I believe that some of these synergies have not happened at the scale that investors would have hoped. For example, the company's gross margin has slightly fallen from FY19's level of 14.4% to the current trailing figure of 14.0% instead of the communicated expansion.

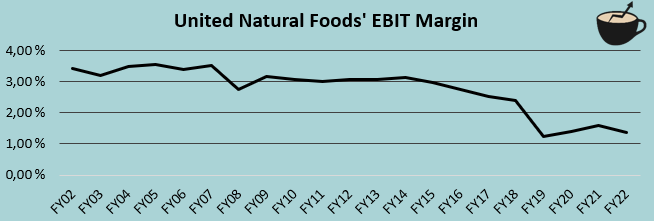

Despite the company's very low historical margins, United Natural Foods' EBIT margin has continued to fall further even years after the acquisition:

{kind=link}

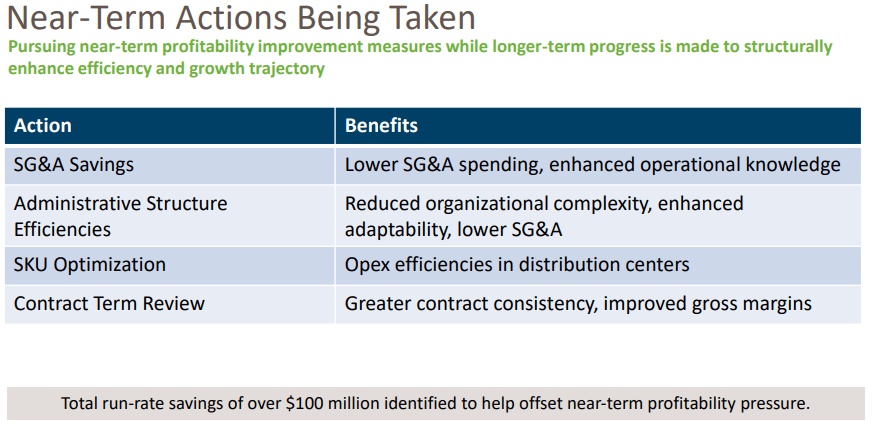

With an adjusted EBITDA guidance around 23% below the previous year, the dropping operating margin doesn't seem to have found a stable level. In the company's Q3/FY23 earnings presentation, though, the company does communicate that it is taking actions to combat the low operating margin:

{kind=link}

The communicated savings of $100 million would improve the company's bottom line significantly - In the last twelve months, United Natural Foods' net income has been $131 million.

The SuperValu acquisition also worsened United Natural Foods' balance sheet, as the company drew a very large amount of long-term debt related to the acquisition worth around $2.9 billion - the company's long-term debt grew from $321 million in FY18 to $2984 million in FY19. The company has been able to pay off the debt partly, as currently, the long-term debt amount stands at $2032 million, of which $10 million is in the current portion. The debt is somewhat manageable but does eat up almost half of United Natural Foods' operating income.

I do still think that the synergies from the acquisition could have potential. Although the acquisition was made multiple years ago, the pandemic could have slowed down progress in integrating the companies. Also, although the financial performance hasn't been up to expectations, the stock price has already seen a large decrease and seems to be pricing in a lower earnings level as discussed in the next chapter.

Valuation

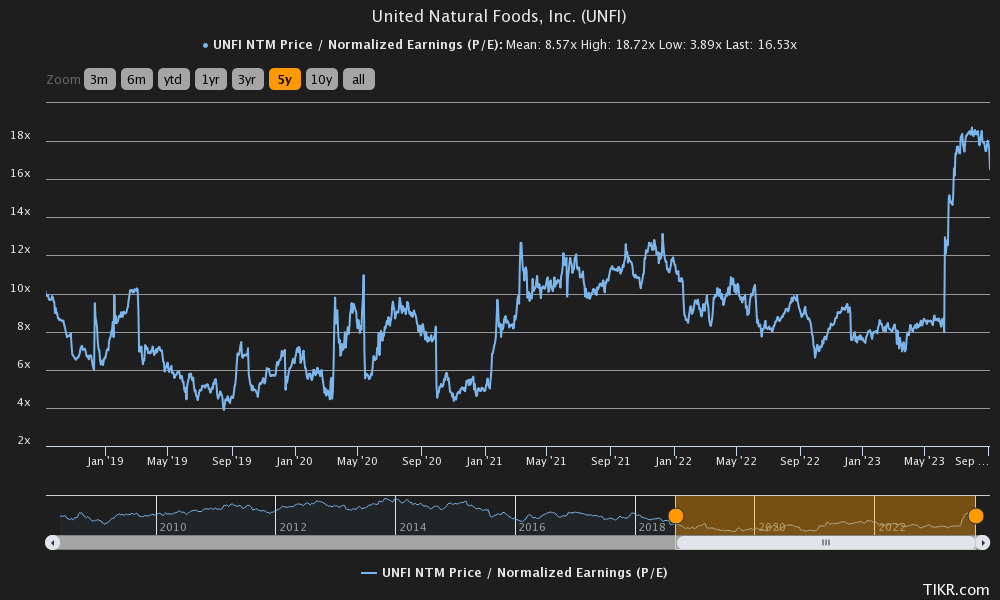

The stock's forward price-to-earnings ratio has varied very significantly in the past five years from a low of 3.89 to a high of 18.72. The current figure of 16.53 is on the higher side, as the ratio has jumped from forward earnings estimate cuts after Q3:

{kind=link}

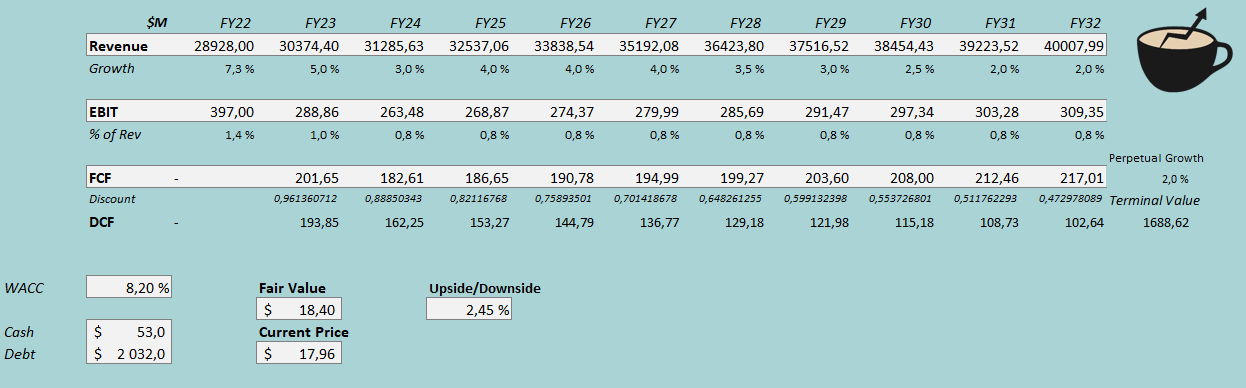

To get a grasp of an estimated fair level for the stock, I constructed a discounted cash flow model. In the model, I estimate United Natural Foods to hit its current fiscal year revenue guidance. Going forward, I estimate a growth of 3% to 4% for six years, after which the growth slows into a perpetual growth of 2% - the estimate doesn't reach the company's historical figures, but does match with growth that has been achieved after the SuperValu acquisition.

For the margin, I expect the company to have an EBIT margin of 1.0% in FY23, below FY22's margin of 1.4%. The company seems to still be struggling with margin control, and I don't see sufficient evidence for a turnaround to estimate such as occurring in the DCF model - after FY23, I estimate the margin to find a stable level at 0.8%.

The company's cash flows are usually quite stable, and the company converts its earnings into cash flow moderately well. The mentioned assumptions and a cost of capital of 8.20% craft the following DCF scenario with an estimated fair value of $18.40, around 2% above the current price:

{kind=link}

The used weighted average cost of capital of 8.20% is shaped through a capital asset pricing model:

CAPM (Author's Calculation)

In Q3 of FY23, the company had $36 million in interest expenses - when compared to the company's long-term debt amount, the company's interest rate is approximately 7.09%. With a currently very high level of debt that should take a long period to pay off, I estimate a high long-term debt-to-equity ratio of 45% for the company.

On the cost of equity side, I use the United States' 10-year bond yield of 4.30% as the risk-free rate. For the equity risk premium, I use Professor Aswath Damodaran's latest estimate for the United States. TIKR estimates United Natural Foods' beta to be 0.99 , which I use in the model. Finally, I add a small liquidity premium of 0.4% into the cost of equity, crafting a cost of equity of 10.55% and a WACC of 8.20%.

Takeaway

Although the investment case for United Natural Foods is unclear as financials have performed quite worryingly after the acquisition of SuperValu, I believe the stock is at least worthy of having on a watchlist - the poor financials seem priced in, and with further cost savings and some unlikely synergies could create significant upside. For the time being, I have a hold rating.

For further details see:

United Natural Foods: Some Hope Remaining