WFC - United Security Bancshares Undervalued As Higher Profitability Goes Unnoticed

Summary

- UBFO trades at a discounted valuation of 6.4x 2023 P/E and 1.2x P/TBV.

- The discount is unwarranted, given UBFO generates industry-leading ROE, 19.8% ROTE and 1.64% ROA.

- That industry-leading profitability is driven by UBFO's low cost deposit franchise with 22 bps cost of deposits vs industry ~100 bps.

- The CEO and founder is a top shareholder and continues to buy shares.

- I estimate fair value is $12/share and investors are paid a 5.7% dividend while waiting for the market to re-rate UBFO.

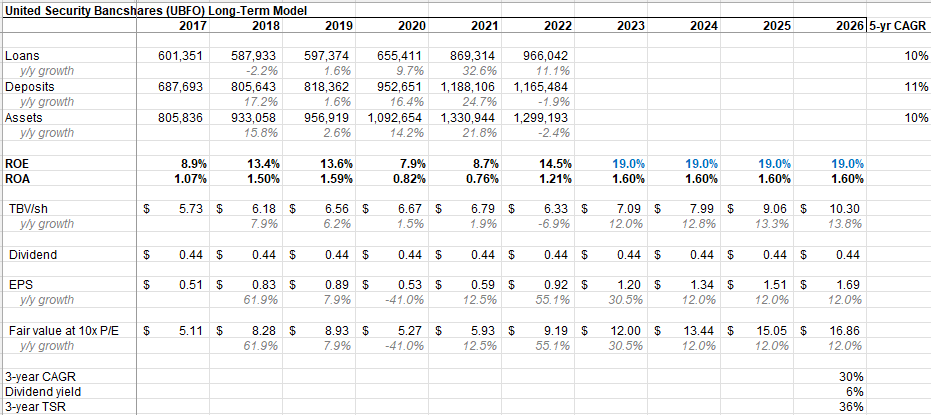

United Security Bancshares ( UBFO ) is a Fresno, California-based bank with $1.3bn assets. The company has a $130m market cap and trades $0.2m of volume per day on the Nasdaq. The stock is undervalued because the market has not yet noticed the bank’s improved earnings, ROE, and ROA, which have significantly increased due to higher interest rates. In 4Q22, the bank reported $0.31 EPS, up 55% y/y, and a 19.8% ROTE and 1.64% ROA. These profitability metrics are a significant improvement from 2017-2021 when the bank averaged 10.5% ROE and 1.15% ROA, which were average profitability metrics for the banking industry over that period. Generally a ~20% ROE bank is considered best-in-class profitability and warrants a 2.0x P/TBV multiple. Because the bank does not have and sell side coverage, investors have not yet noticed UBFO’s significantly improved profitability. I believe the bank will earn $1.20 EPS in 2023 and is worth $12/share today, up from $7.66. Further, with a ~20% ROE, the bank may be able to pay out a 5.7% dividend yield while also growing EPS 12-14% over the next 3 years. The initial undervaluation, combined with strong go-forward profitability, due to the improved interest rate environment, creates a compelling opportunity in UBFO stock.

The CEO founded the bank and is the second largest shareholder (and largest individual shareholder). He knows the bank better than anyone and has been buying in the open market as recently as Feb 16 th , 2023 at $7.84/share.

UBFO has a strong deposit franchise, which did not make much of a difference from 2008-2021 because interest rates were near zero and everyone had near-zero cost of deposits. With interest rates in a new regime (my guess is fed funds will be between 3% and 6% for the next decade), UBFO’s deposit franchise has significantly increased in value and is under-appreciated. UBFO paid just 22 bps on its deposits in 4Q22 (flat from 22 bps in 3Q22) vs the banking industry average deposit cost ~100 bps, up ~35 bps q/q vs 3Q22. UBFO’s non-interest bearing deposits are 40% of the deposit base vs industry average 30%. Non-bearing deposits are generally the stickiest and most valuable part of the deposit franchise. This is driven in part by Fresno being an unusually strong deposit market – with only ~3 community banks, significant farming operations that are long cash and do not change banks often – creating no incentive to aggressively compete for deposits. Closest competitor CVCY has $2.1bn deposits and just $1.25bn of loans (60% loan-to-deposit vs industry ~80%), meaning that they do not need to pay up to defend their deposits.

The closest regional competitor is CVCY, which trades at 9.7x 2023 P/E and 2.5x P/TBV. At these multiples, UBFO would trade at $1.20 2023 EPS x 9.7x = $11.64/share and $6.33 TBV/share x 2.5x = $15.82/share.

Valuation

I estimate that UBFO is worth $12 today, based on 10x P/E on $1.20 2023 EPS. And is worth $16.86/share in 2026, based on 10x P/E. While we wait for the market to realized UBFO’s earnings power, we are paid 5.7% dividend yield.

Looking out to 2026, I estimate that UBFO may deliver a 30% per year appreciation plus 5.7% dividend for a ~36% CAGR over the next 3 years. This is driven from a combination of initial undervaluation, then continued ~20% ROE causing intrinsic value to rise by a similar amount per year over that horizon.

Company filings and my estimates

{kind=link}

Risks

- Interest rates decline, pressuring net interest margins and profitability

- Loan losses increase from a recession

- The bank is not able to retain key employees

For further details see:

United Security Bancshares Undervalued As Higher Profitability Goes Unnoticed