ET - Uniti: 14% Yielding Debt A Far Better Option Than The Equity

Summary

- Uniti continues to disappoint investors, and returns have been extremely poor since the spin-off.

- The underlying value of assets is likely the only thing holding this up even at these levels.

- Equity offers a poor risk-reward setup compared to the bonds.

When we last covered Uniti Group Inc. ( UNIT ) and that was a long time ago, we suggested investors hit the bid and move on. Failing that, perhaps another security was a far better choice than UNIT if investors wanted cheap and discounted plays.

Energy Transfer ( ET ) for example trades at about 3X what it calls "distributable cash flow". Something that is about as useful as AFFO today. ET's debt to EBITDA based on 2021 numbers likely will be at about three turns lower than Uniti's. The median ET customer looks as distressed as Windstream. ET spends a large amount of cash on "growth capex" and this is not going to produce any growth. Overall, ET looks far stronger of the two. So does ET deserve to trade at $15 or does Uniti deserve to trade at $3?

Source: A Look At 2021 Numbers

That article was just prior to the vaccine announcement and as everyone knows, the stock markets had a fantastic 2021. UNIT felt the impact as well. But as the wise man said, "In the short run, the market is a voting machine but in the long run, it is a weighing machine." That weighing part is well underway as can be seen below, and this one is ready for another look.

Windstream Drama 2.0

The idea that landlords hold all the cards in a tenant-landlord relationship is questionable at best. We have seen this play out in many tenants in different industries. CorEnergy ( CORR ) basically sold its asset for about the unpaid rent owed , after repeatedly emphasizing how important the asset was to the tenant. Medical Properties Trust, Inc. ( MPW ) has moved in 2022 more or less in line with credit-related news about its largest tenant, Steward. UNIT bulls had long insisted on "mission-critical nature" if we are getting that phrase correct, of the fiber network for Windstream. Windstream still forced a negotiation for the exact reason we had long argued, no other tenant wants that loss-making asset. That knocked at least $15 off the fair value of UNIT equity.

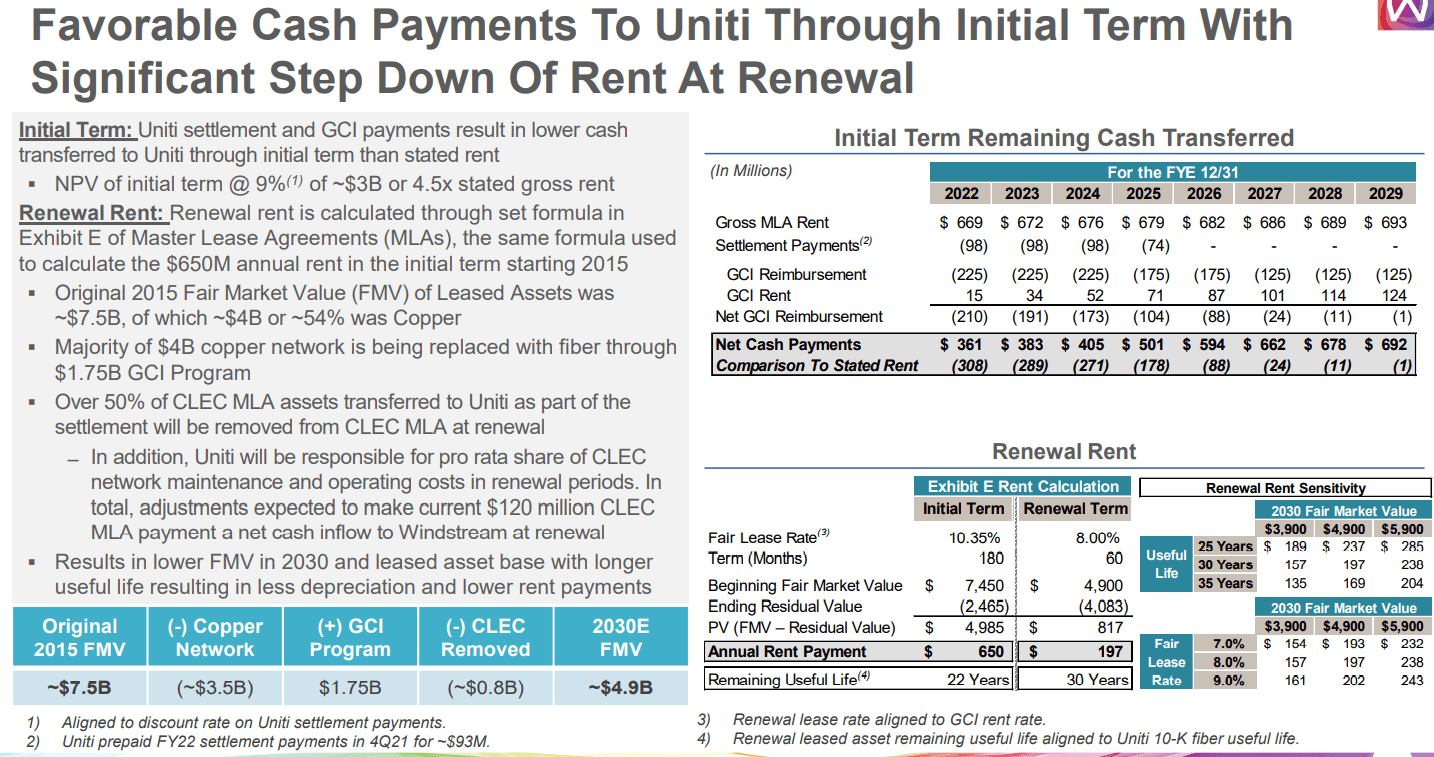

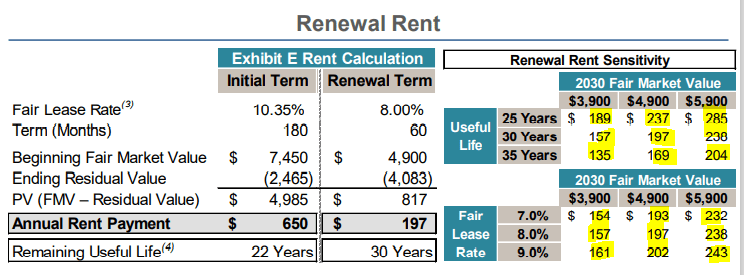

Stunningly enough, that was not the end of it. UNIT got into a second dispute with Windstream on the rent payments post-2030. The whole logic of that dispute is beyond the scope of this article, although there are others who have written exclusively about it. The crux of the issue is that according to Windstream, rents will be based on fair market value of those assets and hence rents will be cut a lot, post-2030.

{kind=link}

What is a lot? In case you could not find it in the slide above, here is the zoomed version.

{kind=link}

So nine different amounts are mentioned, which at the low and the high end would result in UNIT filing bankruptcy. Of course, there is a lot of wood to chop between 2022 and 2030. UNIT in the meantime has whipped out the same playbook as the first time around. The rent will not be renegotiated, and we don't have to worry about it until 2028 (possible arbitration timeline).

Q3-2022

UNIT's results for Q3-2022 were about in line with adjusted funds from operations (AFFO) coming in at 43 cents a share. For the full year, AFFO should come in at $1.69, which certainly makes it mouth-watering if you examine just the AFFO multiple. There are three problems with getting attached to that. The first is of course the artist known as Windstream, which still makes up 80% of their adjusted EBITDA.

Uniti Presentation Q3-2022

The second is that the AFFO is not free cash flow, not even close. Capex was close to $293 million for the first nine months of the year, and that capex is not deducted in calculating AFFO. Sure, there is the usual response of the split between maintenance and growth capex. To that is the usual rebuttal that the bulk of that growth capex is spent on Windstream and that tenant of course is not exactly setting up to grow its payments.

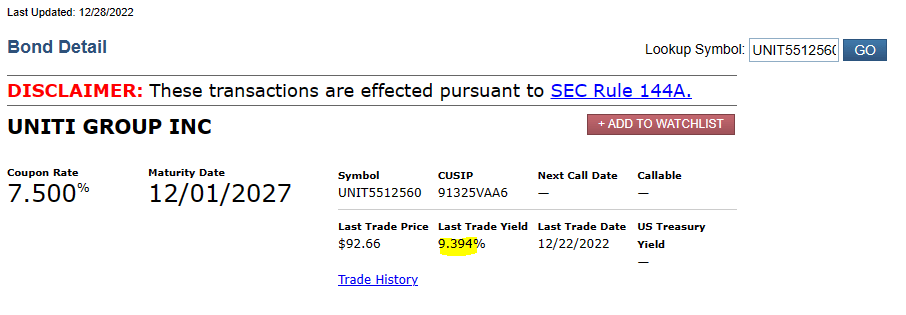

The final problem is that UNIT's bonds look about as distressed as they can get. The yields to maturity are at double digits and the recent convertible offering is also yielding almost 9.4%.

{kind=link}

This is despite a solid price to convert into common.

The Convertible Notes will bear interest at a fixed rate of 7.50% per year, payable semiannually in arrears on June 1 and December 1 of each year, beginning on June 1, 2023. The Convertible Notes will mature on December 1, 2027, unless earlier repurchased, redeemed or converted.

Prior to September 1, 2027, the Convertible Notes will be convertible only upon satisfaction of certain conditions and during certain periods, and thereafter, the Convertible Notes will be convertible at any time until the close of business on the second scheduled trading day immediately preceding the maturity date. The Convertible Notes will be convertible on the terms set forth in the indenture into cash, shares of common stock of the Company (the "Common Stock"), or a combination thereof, at the Company's election. The conversion rate will initially be 137.1742 shares of Common Stock per $1,000 principal amount of Convertible Notes (equivalent to an initial conversion price of approximately $7.29 per share of Common Stock). The initial conversion price of the Convertible Notes represents a premium of approximately 20% to the $6.075 closing price of the Common Stock on the Nasdaq Global Select Market on December 7, 2022

Source: Seeking Alpha

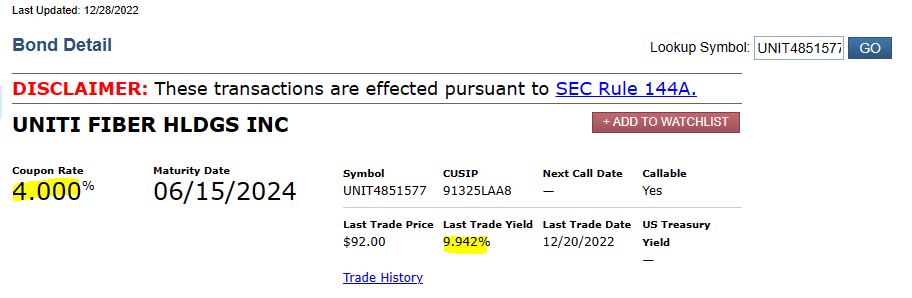

Refinancing the entire debt stack at anywhere close to market rates will reduce AFFO substantially. For example, a 4% move in interest rates would cut AFFO by half. That 4% move is hardly a far-fetched idea. The 2024's are trading 6% wide of their coupon.

{kind=link}

Verdict

We can all pretend we can see out in full high definition clarity to 2030, but that is far from the truth. What we do know here is that after a long history of trying to diversify, UNIT still gets the bulk of its EBITDA from one client. What we do know is that UNIT has not created any value for its shareholders in its entire history. The underperformance versus Vanguard Real Estate ETF ( VNQ ) speaks volumes. The underperformance versus American Tower Corp. ( AMT ) and Crown Castle Inc. ( CCI ) is embarrassing.

What UNIT has going for it is the debt to EBITDA of close to 6.0X. While that is hardly a low number, we can argue that the assets are at least worth that. This fits in line with what Fitch sees as well:

The recovery analysis assumes that Uniti would be considered a going concern in a bankruptcy and that the company would be reorganized rather than liquidated. Fitch has assumed a 10% administrative claim. The revolver is assumed to be fully drawn. The going-concern EBITDA estimate reflects Fitch's view of a sustainable, post-reorganization EBITDA level, upon which Fitch bases the valuation of the company. This leads to a post-reorganization EBITDA estimate of $750 million. The reduced EBITDA could come about by a rent reset at Windstream (and there are no immediate EBITDA generating benefits received by Uniti in return for the reduction) and/or weakness in other lines of business as fiber contracts are renewed at lower levels.

Post-reorganization valuation uses a 6.0x enterprise value multiple. The 6.0x multiple reflects the high margin, large contractual backlog of revenues, and high asset value of the fiber networks. Fitch uses this multiple for fiber-based infrastructure companies, for which there have been historical transaction multiples in the high single digit range. The multiple is in line with the range for telecom companies published in Fitch's Telecom, Media and Technology Bankruptcy Enterprise Values and Creditor Recoveries report. The most recent report indicates a median of 5.4x.

The recovery analysis produces a Recovery Rating of 'RR1' for the secured debt, reflecting strong recovery prospects (100%); the 'RR5' for the senior unsecured debt reflects the lower recovery prospects of the unsecured debt, given its position in the capital structure.

Source: Fitch

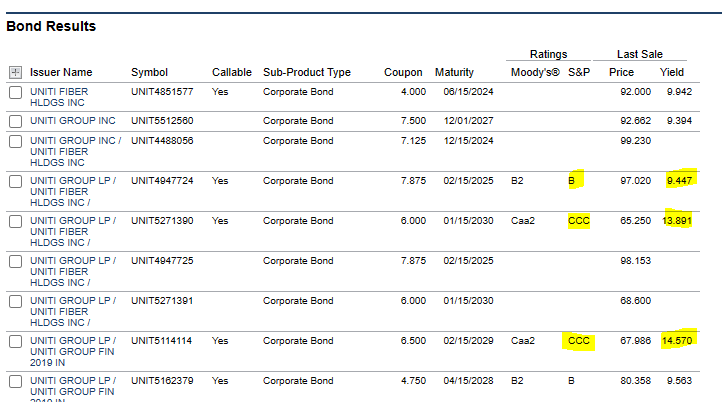

So if you really had the itch to play it, the bonds would be the way to go. Here you would be confronted with the secured and the unsecured debt and there is a huge difference in yields and ratings.

{kind=link}

Nonetheless, both are interesting options for a longer-term play on the company, relative to the common equity. We rate the common equity at "hold", which is a big upgrade from the Strong Sell ratings the last time around.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Uniti: 14% Yielding Debt A Far Better Option Than The Equity