AAPL - Unity Software: Apple's Approval Boosts Growth Tailwind (Rating Upgrade)

2023-06-21 10:00:00 ET

Summary

- U has recently rallied by +37.29% after AAPL announced its partnership with the software company for the spatial computing headset, Vision Pro.

- The partnership may trigger a long-term tailwind in adoption, with AR/VR headsets potentially reaching widespread use in various industries.

- We may see U onboard more developers from H2'23, with AAPL about to offer the Vision Pro developer kit while hosting developer labs in six major cities from July onwards.

- The stock remains a Buy here for so long that the portfolio is sized appropriately given the immense rally thus far.

The Unity Investment Thesis Looks Highly Promising, Thanks To Apple's Vision Pro

We previously covered Unity Software Inc. (U) in September 2022, discussing its previous ironSource acquisition. We were of the opinion that the deal might aid the former's monetization strategy in the Metaverse and advertising market.

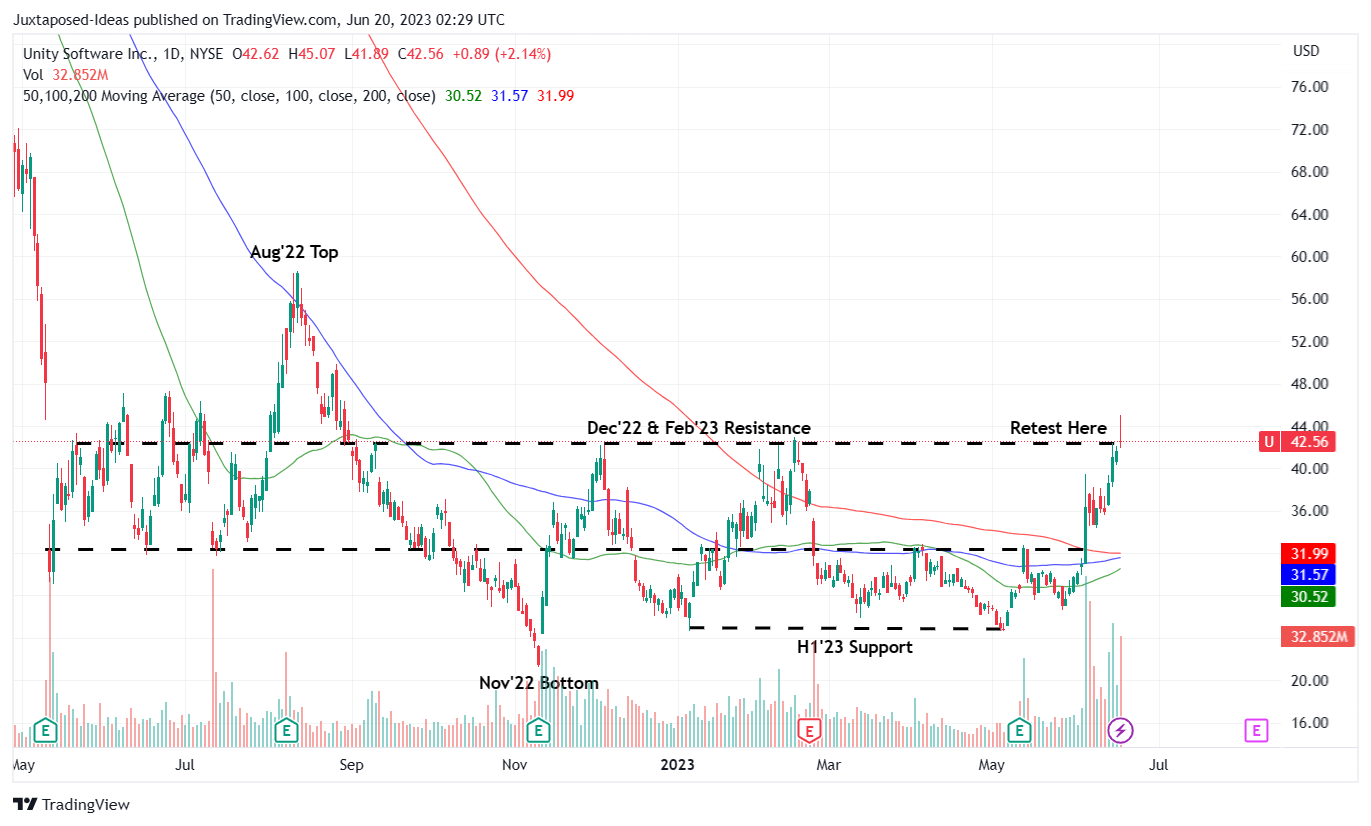

U 1Y Stock Price

{kind=link}

However, due to its cash burn and share dilution, we also iterated a lower entry point for an improved margin of safety. True enough, U had breached its previous support levels of mid $30s since then, cratering at the $20s by November 2022, thanks to the peak recessionary fears.

Then again, it is also evident that the stock has recently rallied by +37.29% after Apple's ( AAPL ) presentation of Vision Pro on June 05, 2023. The Cupertino giant has elected to use the software company's gaming and developer platform for the spatial computing headset, naturally triggering renewed enthusiasm surrounding its offerings.

It was a similar cadence to one we witnessed back in October 2021, when Meta ( META ) introduced its Metaverse ambitions. While that story is still developing, with the advertising company reporting -$4B of operating losses in the Reality Labs segment by FQ1'23, it appears that the AR/VR future is becoming a reality after all.

We believe U has much to gain through the integration with the iOS platform, since it has generally been well-loved by developers, with 1.76M of available apps. The platform also commanded 67% of the global app consumer spending in 2022, generating an annualized app and game revenues of $90.8B by Q1'23 (+3.6% QoQ/ +4.1% YoY). This is on top of the App Store facilitating $1.1T in billings and sales last year.

With AAPL only commanding 21.5% of the smartphone market share, it appears that its users are generally high spenders, generating massive revenues for both the smartphone maker and developers alike. This is why the partnership between AAPL and U may trigger a massive tailwind in the latter's platform adoption and top/ bottom lines moving forward.

We believe the AR/VR headsets also have the opportunity to reach a similar widespread use case as that of the next generation computing platform, (think Tom Cruise in Minority Report or Tony Stark in Iron Man). This may be a similar trend to that of smartphones in 2023, 16 years after Steve Jobs' introduction of the first generation iPhone.

With developers likely to build 3D apps for professional, retail, commercial, educational, research and development, and many other end markets, we believe U's prospects remain very promising for the next decade, especially aided by AAPL's stamp of approval and "massive $800B AI opportunity."

Now, how will this impact U's top and bottom lines moving forward?

For now, the software company does neither a royalty pricing strategy nor a revenue share model, but opts for an annual subscription model (per developer seat) under Create Solutions . This is on top of its consulting/ training/ custom development with revenue recognized after services are rendered, and the cloud hosting arrangement with revenue based on fixed or consumption-based fees.

Under this plan, we may see U onboard more developers from henceforth, with AAPL about to offer a Vision Pro developer kit , while hosting developer labs in six major cities (Cupertino, London, Munich, Shanghai, Singapore, and Tokyo) from July 2023 onwards.

As a result, we may see a notable contribution in the software company's top and bottom lines from H2'23 onwards, way ahead of the Vision Pro launch in 2024. Given AAPL's obvious partnership with Disney ( DIS ), the possibility of developers using the headset to develop 3D games, virtual theme parks, and movies is not out of the picture as well.

This cadence may naturally increase U's market share in the AR/VR segment, while similarly boosting its app and ecosystem offerings as more developers onboard its platform and publishers partner with its in-house R&D team for customized products.

Investors must also not forget the software company's advertising services, under Grow Solutions, which has been further strengthened by the previous ironSource acquisition.

In FQ1'23, U reported an annualized Create revenue of $749M (+13.8% YoY) and Grow revenue of $1.25B (+101.1% YoY), while guiding FY2023 total revenues of $2.14B (+53.9% YoY) and adj EBITDA of $275M (+638.1% YoY) at the midpoint.

Now, we belatedly realize that much of the optimistic numbers are attributed to Vision Pro, a partnership previously not disclosed in its previous earnings call on May 10, 2023, with the software company likely sworn to secrecy prior to the launch.

So, Is U Stock A Buy , Sell, or Hold?

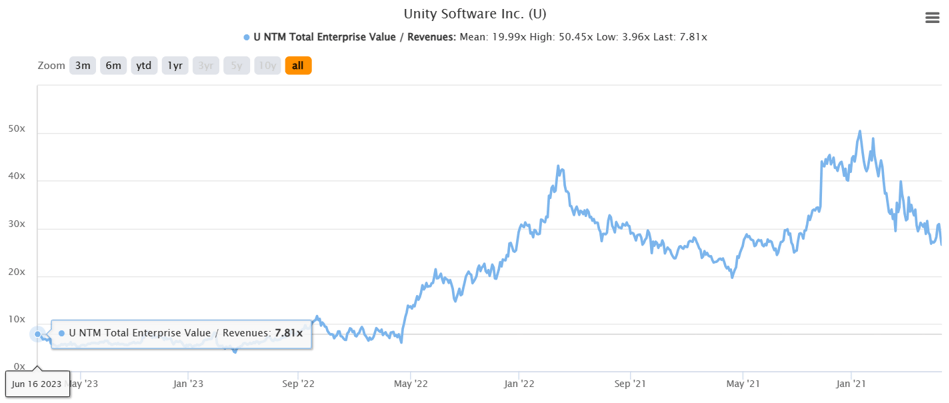

U 3Y EV/Revenue

{kind=link}

Thanks to AAPL, U's valuation has also risen to NTM EV/ Revenues of 7.81x at the time of writing, against the pre-Vision-Pro-launch levels of 5.20x and its 1Y low of 3.96x in November 2022.

We are also seeing a similar cadence in its stock prices, already retesting its December 2022 and February 2023 resistance levels of low $40s at the time of writing. While there may be volatility from its elevated short interest of 8.74%, we suppose the tailwind remains more than decent, due to AAPL's push into the AR/VR market by 2024.

While it remains to be seen if the Cupertino giant may exclusively work with U, or diversify with other developer platforms, the market analysts have already revised the latter's top-line expansion to an impressive CAGR of +29.5% through FY2025, nearing its hyper pandemic levels of +36.9%.

In addition, the software company is expected to achieve positive EBITDA, FCF, and adj EPS by FY2023, suggesting that the optimism embedded in its valuations and stock prices may be warranted after all.

Naturally, given the massive rally thus far, it remains to be seen if U may break through the current resistance levels and, if it does, whether the optimism may hold through the uncertain macroeconomic outlook through 2023. Therefore, while we are rating U as a Buy here, investors must also size their portfolio accordingly.

Otherwise, bottom-fishing investors may consider observing for a little longer and adding after a moderate retracement for improved upside potential. However, one may also miss the departing train, with the AR/VR game still in its infancy and the stock market on the verge of a bull run.

For further details see:

Unity Software: Apple's Approval Boosts Growth Tailwind (Rating Upgrade)