FVRR - Upwork: The Future Of (Up)Work Looks Bright

2023-07-13 12:44:22 ET

Summary

- Upwork Inc. is a leading digital freelance marketplace that has seen significant growth in the gig economy and online talent market.

- Upwork monetizes both ends of its marketplace successfully, generating revenue from both freelancers and clients.

- The company has successfully grown revenue consistently YoY, driven by strong active client, GSV per active client, and take rate growth.

- Despite competition and risks, Upwork's growth, market-leading position, and ability to monetize suggest a potential for long-term equity value.

- I view the current valuation as undervalued, with a weighted average price target that implies a 15% premium to today’s price.

Thesis

Upwork Inc. (UPWK) is an attractive digital freelance marketplace business that has experienced secular growth in the fast-growing freelancing space. The global freelance, or "gig economy", industry represents a $3.8 billion industry according to LinkedIn in 2020, and is expected to grow to $12 billion by 2028.

UPWK operates the largest online global marketplace as measured by gross services volume ((GSV)). The company serves 2 million projects, 375,000 freelancers, and 475,000 clients in over 180 countries globally. The company has two main business segments: Marketplace, which is divided into Marketplace (84% of LTM total revenue) and Enterprise (8%) offerings, and Managed Services (8%).

The company operates in a highly competitive, low-barrier to entry market that has one major public company competitor, Fiverr International Ltd. (FVRR), and others including Toptal, 99designs, and Hubstaff. Despite the competitive nature of the industry, I believe that UPWK has entrenched itself as the leader in the space, with LTM revenue of $638M, which is 88% more than that of FVRR with $339M in LTM revenue, and faster LTM GSV, active client, and GSV per active client growth rates as well.

My weighted average NTM price target for the stock is ~$12.5, implying a 21% premium to the current share price with weighted average upside of 15% at the time this analysis was written. My analysis will cover the various levers for growth, including Talent and Client monetization success, take rate expansion, active client growth, GSV expansion, and growth in ancillary business lines.

Monetization of Both Talent and Client

UPWK is one of the only online freelancing platforms in the market to monetize both ends of the marketplace: Talent (the freelancers) and Clients (those that hire the freelancers). UPWK's largest competitor, FVRR, fails to do this as successfully as UPWK has been able to. FVRR generates substantially all of its revenues through transaction fees . When an order is placed, the client pays FVRR the price of the job plus a 5% service fee, with a minimum service fee of $2.

UPWK, on the other hand, generates revenue from both Talent and Clients. Revenue comes in the form of a percentage fee from billings to Clients (10% on all jobs), Client marketplace fees ($4.95 contract initiation fee and 3-5% payment processing fee), Talent subscription fees for Freelancer Plus ($14.99 per month), Talent purchases of Connects ($0.15 to $0.30 per Connect), and other services including foreign currency exchange fees and payroll services.

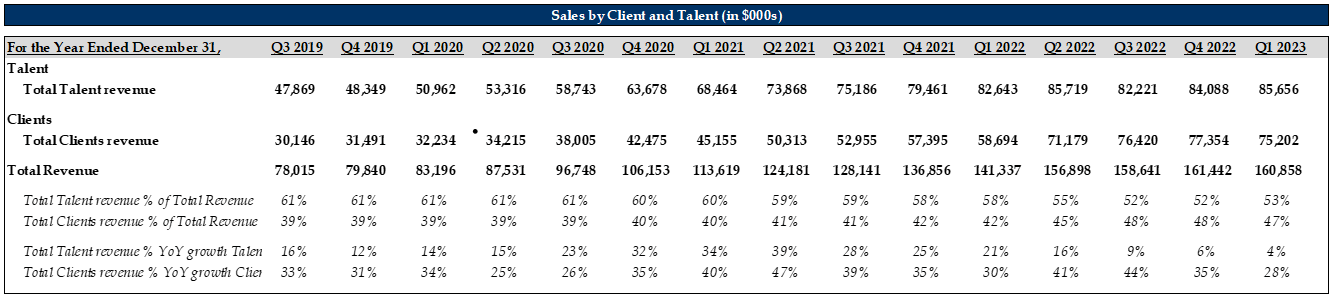

In the chart below, I put together an analysis of UPWK's revenue by Talent and Clients quarterly since 3Q2019. The analysis highlights several notable data points: first, that Talent revenue as a percentage of total has declined from 61% to 53%. Second, that Client revenue is reaching near-parity (50/50) with Talent revenue in terms of dollar volume. And third, and perhaps most notably, that Client revenue has grown consistently at 30%+ over the last 15 quarters while Talent revenue has slowed to 4% growth in the latest quarter, 1Q2023.

{kind=link}

My takeaways from this highlights the importance of monetizing both side of the marketplace and how successfully UPWK has done so over the last 4 years. Additionally, the rapid growth in Client revenue signals to me where the company is headed in terms of strategy - an area that FVRR hasn't yet forayed much in yet as FVRR has solely been focused on charging only the Clients to date.

These various monetization strategies are more similar to what other public companies with similar marketplace models, such as eBay , have done with moderate success. Later in my analysis I will explain in greater detail how UPWK has been able to successfully expand their take rate while charting a path for further growth in take rates alone.

Take Rate Expansion

In Mach of 2023, UPWK announced a new fee structure across the entire platform. The new fee structure moved all Talent to a 10% fee rate while retiring the sliding scale fee structure (20% fee for contracts up to $500, 10% for over $500, and 5% for over $10,000). In addition, UPWK instituted a $4.95 initiation Client contract initiation fee as a one-time fee. What did these changes do, and how did this impact the business financially?

I will analyze the ripple effects further below, but will explain at a high-level first: the company, in my opinion, can now earn a higher take rate percentage for smaller jobs via charging the $4.95 flat fee while also capturing an additional 5% take rate (going from 5% to 10%) for large jobs ($10,000 and up). The results of these changes were announced to take place beginning May 3, 2023, so the financial impact to the company's topline should be reflected in later quarters and will likely, in my opinion, contribute meaningful long-term growth.

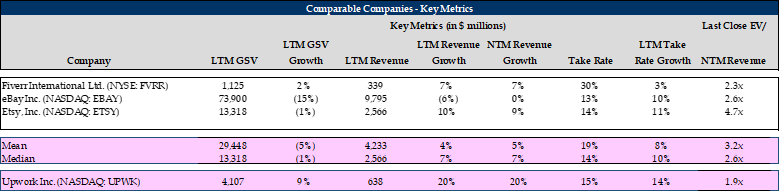

The analysis I put together below showcases various metrics for UPWK against some marketplace comps. I used FVRR as the closest peer, and then used eBay and Etsy as other competitors who operate similar marketplace models with buyers, sellers, GSV, and take rates. While both eBay and Etsy are much larger in terms of size and different in terms of what they sell, the take rates I think are most notable. In the analysis, you can see that UPWK has a higher take rate of 15% than both eBay and Etsy, who have 13% and 14%, respectively. Additionally, UPWK has the highest LTM take rate growth of 14% of the comp set, and as previously mentioned, I believe that the take rate should continue to push higher in subsequent quarters with the new fee structure UPWK put in place.

{kind=link}

It should be worth mentioning that FVRR has a take rate of 30% because the majority of the jobs completed on their platform are small jobs with small dollar values. FVRRs pricing model of a flat fee and percent of GSV helps the company garner a much higher take rate than UPWK, which competes primarily in the medium- to large-size job space. I see UPWK's recent fee structure changes as a maneuver meant to compete squarely head to head with FVRR while also boosting take rates in the long run.

Lastly, I should mention that UPWK leads the comps in the set in terms of LTM GSV growth of 9%, LTM revenue growth of 20%, and take rate growth of 14%. In my opinion, UPWKs growth and position as leader in the online freelance marketplace should continue to push take rate, and therefore marketplace revenue, further closer to that of FVRR's of 30%.

Active Client and GSV Per Active Client Growth

I previously mentioned that Client revenue at UPWK is growing faster than that of Talent revenue. However, I also see further upside in Client growth, on a pure user basis over time. In the analysis below, I took a look at active clients, which are Clients who have spent on the platform at least once in the last 12 months, and saw a trend in active client compounded annual growth rate [CAGR] of 10% and GSV per active client of 11% over the last two years.

{kind=link}

Moreover, I then compared the active client base to that of FVRR's. The chart below shows that UPWK's client base is just 19% of FVRR's (827,000 versus 4,263,000), illuminating an opportunity for UPWK to gain significant traction with over 4 million users. I also see upside in GSV per active user for UPWK, which currently obtains $4,967 of GSV per active user, compared to FVRR's $262. This difference of $4,705 per user is stark, and in my opinion, represents an opportunity for UPWK to scale meaningfully over time as users continue to spend more on the platform. Said differently, in my view, if UPWK can attract Clients to the platform, they have a high degree of success of growing existing clients while also increasing their Client's share of wallet.

{kind=link}

GSV Expansion

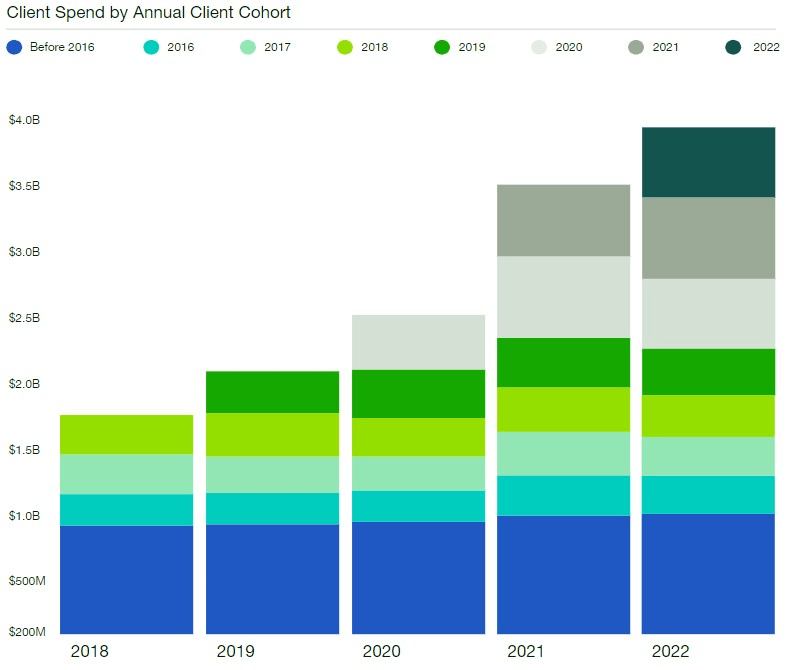

UPWK has exhibited a keen ability to not only attract Clients to their platform, but to keep the Clients coming back for more, and with bigger check sizes. In the latest public filing, UPWK shared the below cohort analysis Enterprise growth, cohort analysis. In it, I saw that the company has been able to retain client spend over years with historical cohorts continuing to spend meaningfully year over year.

{kind=link}

The customer stickiness of the platform is evident to me in their cohort analysis, and the growth in GSV per Active Client in my prior analysis provides further confirmation of that. I see future upside in UPWK's ability to grow GSV per Active User over time, and will highlight this in my valuation.

Enterprise and Managed Services Expansion

Launched in 2018 , the Enterprise business has grown and scaled to represent 8% of Marketplace sales and 7% of sales in about 5 years. Enterprise is designed primarily for larger clients with at least 250 employees which provides access to additional product features, premium access to top talent, and other benefits. The success of Enterprise, along with UPWK's industry-leading GSV per active client, in my view cements UPWK's position as a juggernaut in medium- to large-scale projects.

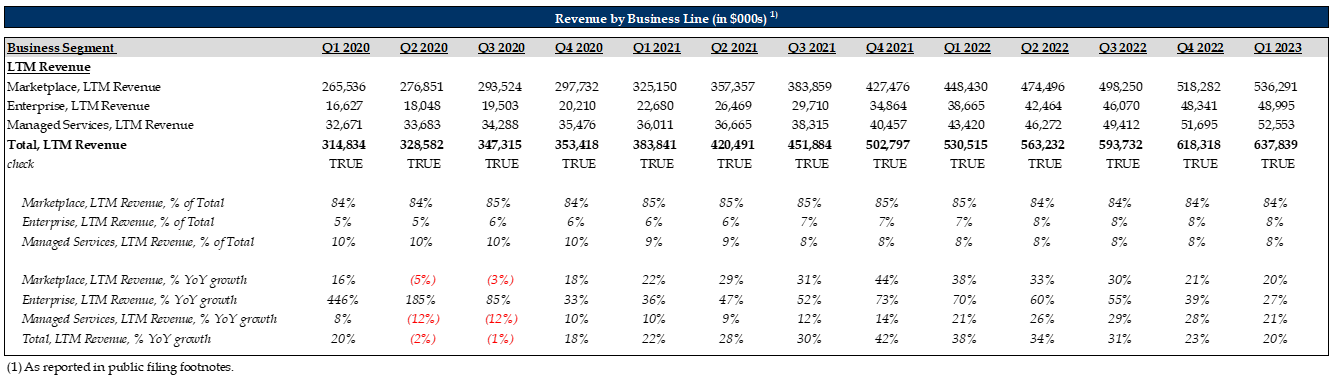

In the analysis I put together below, I examined the revenue breakdown of UPWK by business line. The analysis showed me that Enterprise and Managed Services have grown to and have stabilized at approximately 8% of revenue each on an LTM basis, signaling that these business lines are scaling nicely. Both of these business lines are growth at 21%+ quarter over quarter, more than that of the Marketplace business line, which indicates that these business lines will continue to be a meaningful contributor to topline.

{kind=link}

In my opinion, the Enterprise and Managed Services business lines also have more customer stickiness than the Marketplace line. This is because both business lines are centered around B2B sales, with UPWK acting as the outsourced HR function. I see future, large project, sticky upside in the form of recurring jobs with businesses through the Enterprise and Manages Services units.

Valuation

I view the current valuation of the stock as undervalued today. I believe there is a lot to like in the short- and medium-term with UPWK's platform. Namely, the recent and projected growth on both sides of the marketplace, Client and Talent, coupled with the growth in medium- to large-sized projects in the Enterprise and Managed Services businesses, should continue to contribute to meaningful growth over the next 12 to 24 months.

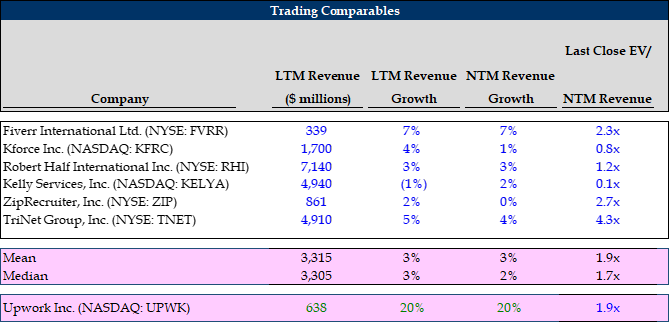

Below is a peer comparison table of UPWK. I chose various companies that specialize in human capital management, temporary labor placement, and recruiting firms. I compared UPWK's LTM revenue, LTM revenue growth, NTM revenue growth and EV/NTM revenue to the comps set and found that UPWK is well ahead of competitors on LTM and NTM revenue growth, which I modeled at 20% for both, versus the peer average and median of 3% and 2%, respectively.

The upside in UPWK is made more clear to me when I compared UPWK's EV/NTM revenue of 1.9x to FVRR's, the closest competitor, of 2.3x. I see significantly more upside in UPWK, and its currently EV/NTM revenue multiple lagging that of FVRR and in line with the comp set gives me conviction in my belief that UPWK is undervalued. I chose EV/NTM revenue because the company and some of its competitors are not yet profitable or have high fluctuations in EBITDA, eliminating and distorting valuation methods including EV/EBITDA.

{kind=link}

I see 15% upside from today's share price, factoring in highly conservative downside, base, and upside scenarios. I see the company's efforts in monetization paying off over the next twelve to twenty-four months, as the changes to the fee structure, growth in the Enterprise and Managed Services Client base, and investments in the AI Services hub begin to show stock price accretion over time.

Author's representation

The proprietary weighted average price model I built is based on Active Client, GSV per Active Client, Take Rate, and Enterprise & Managed Services growth models as previously described. Additionally, and perhaps more importantly, I used the average EV/NTM revenue multiple in the base case and adjusted in both the upside and downside scenarios to reflect modest fluctuations in multiples. At a blended rate, the upside relative to current valuation is worth considering.

Risks

The online freelancing marketplace is inherently a highly competitive, low barrier to entry industry with many competitors. As such, there are several risks I see that could switch my position from long to hold or short.

First, I view a slowdown in general macro environment as a catalyst that may lead to both Client and Talent declines. However, this risk is partly mitigated by my hypothesis that during financially difficult times, cash strapped businesses will seek low-cost, temporary labor which could prove to increase activity on Upwork's platform.

Second, I view the recent changes in fee structures that UPWK implemented this year, along with the various fees and sources of revenue that I outlined above, may hurt loyal and new Client and Talent pools. The fees on both sides of the marketplace can add up in a highly competitive industry where other online marketplaces, such as FVRR, may be a better alternative to UPWK. These other marketplaces represent a risk to UPWK since they do not charge as much, if at all, on one or both sides of the marketplace like Upwork currently does. The fees ultimately may alienate customers.

Third, the use of artificial intelligence as a free tool for businesses and individuals to leverage can hurt UPWK's growth potential. Many freelancing jobs on the platform are for small, menial tasks that artificial intelligence may be able to take on, reducing future revenue to UPWK that the company previously would have had if AI did not exist. I view this risk as partly mitigated by the fact that the bulk of UPWK's jobs are for middle- and large-scale projects which require more than AI. This risk, in my opinion, hurts the value proposition of FVRR and other small-scale freelancer platforms.

Last, the general competitiveness from other freelance and temporary worker platforms are a threat to UPWK's business proposition. This is a low barrier to entry business with nothing that is seemingly proprietary by way of. However, the platform has entrenched itself as a market leader and one that engages in what I believe appears to be a Duopoly between UPWK and FVRR.

Conclusion

UPWK has invested significantly over the last several years in testing new features, rolling out Beta services, and iterating on various monetization strategies. Despite the fact that company's stock performance has shrunk from a high of $59 per share nearly a year and a half ago and the business has, in my opinion, grossly overspent in SG&A, I see room the potential for future growth as being real.

UPWK has been able to show many signs of early success on monetizing both sides of its rapidly growing two-sided marketplace, and the true test of its investments remains to be seen as the economy braces itself for a potential market decline. All told, there is a lot to like about UPWK's story and organic growth in a highly competitive industry. I see a path for UPWK to generate long-term shareholder value if the company can protect, invest in, and monetize its loyal Talent base with an evolving Client base that includes everyone from individuals, startups, and large Fortune 500 companies looking for talent.

For further details see:

Upwork: The Future Of (Up)Work Looks Bright