CA - Ur-Energy: Cashed-Up Production-Ready And Recession Resilient

2023-04-28 10:51:57 ET

Summary

- Uranium is one of the few commodities with very inelastic demand, regardless of the economic cycle.

- At the same time, the uranium market is projected to maintain supply shortfall for years to come, supporting high pricing.

- Ur-Energy is one of the few production-ready companies and is well-positioned to benefit from potential uranium rally.

- I estimate that the current share price offers about 40% upside.

With recession fears growing and the FED warning about possible economic downturn later this year, investors may want to reassess their portfolios. Naturally, in the potential event of a recession, especially one following rapid raising of interest rates, it's logical to assume that many sectors will suffer from demand destruction. In turn, many companies' revenues will likely plummet, eventually resulting in negative returns for investors. However, uranium should be an exception as demand from nuclear utilities is not sensitive to the economic cycle. The market for U 3 O 8 is currently in a shortfall, projected to persist for years to come. This should benefit miners, who have ability to quickly bring production to the table. With the majority of uranium companies still in exploration/development stage, which comes with permitting risk and access to capital challenges the choice is rather limited. I believe Ur-Energy ( URG ) is one of the few miners in an excellent spot to benefit as the company is fully-funded and production-ready. When it comes to valuation, I estimate the shares of URG to offer about 40% upside.

The uranium opportunity

Following the Fukushima accident in Japan, uranium has been out of favor. However, during the past few years, especially in light of the 2021-2 energy crisis common sense is starting to return. While Germany, with radical greens in the front seat in the current government, closed down its last three remaining reactors in 2023, the majority of countries are warming up towards the opportunity that nuclear energy presents in the energy transition process. For example, public opinion in Japan has radically shifted and now majority of citizens support nuclear energy. The two largest countries in the world in terms of population - India and China are rapidly building giant fleets of nuclear power plants in order to satisfy the growing energy needs of their economies in a low-carbon way.

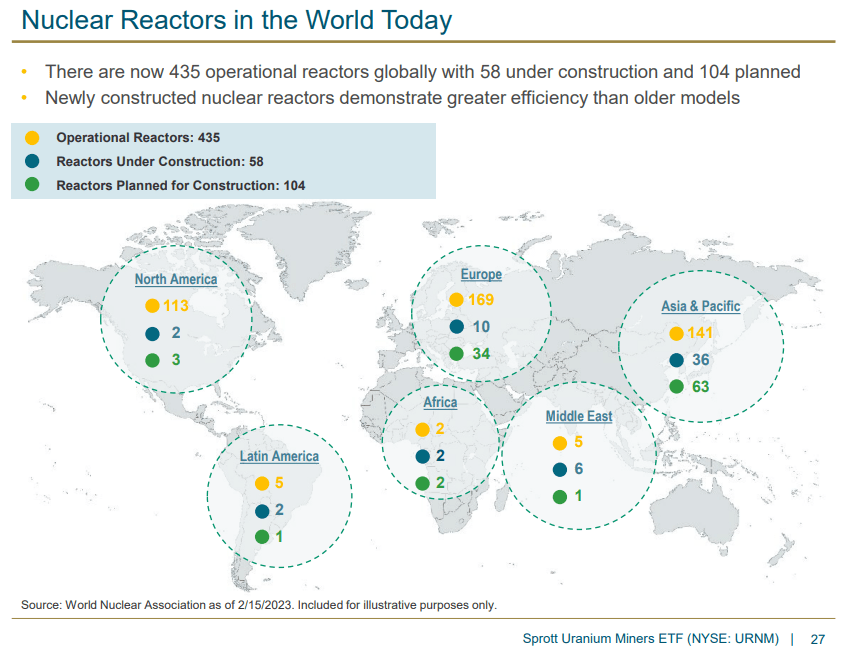

Global nuclear reactor fleet (World Nuclear Association)

{kind=link}

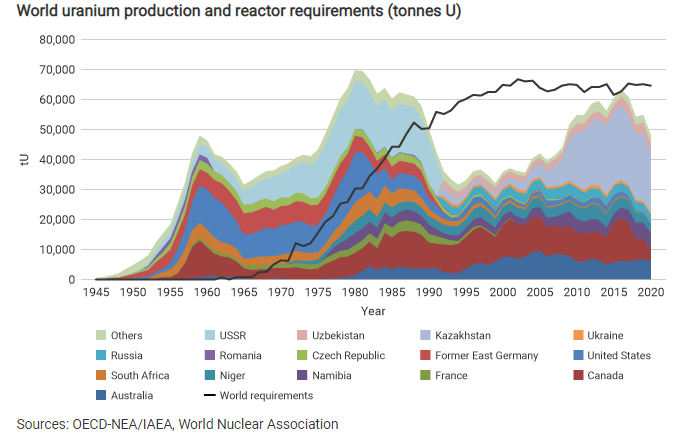

On the supply side, production has been declining since 2016 as a result in weaker uranium prices and accounts for only 77% of reactor requirements in 2021. Miners are faced with raising OPEX as a result of inflation and even the uranium kingpin - Kazatomprom (KAP:LSE) is guiding for lower production in 2023. With demand expected to pick-up, much needed supply has to be brought to market. The most promising area, where it could come from is Canada's prolific Athabasca basin, where dozens of exploration/development projects are located. The problem is that permitting is slow and some of these projects require uranium prices in the US$ 60-70/lbs range in order to be economic. The current market environment with raising interest rates and higher cost of capital is making things even worse, as those explorers/developers have harder time financing their activities. For these reasons, the supply/demand shortfall on the uranium market is expected to persist for years to come.

Historical uranium supply and reactor requirements (OECD-NEA/IAEA, World Nuclear Association)

{kind=link}

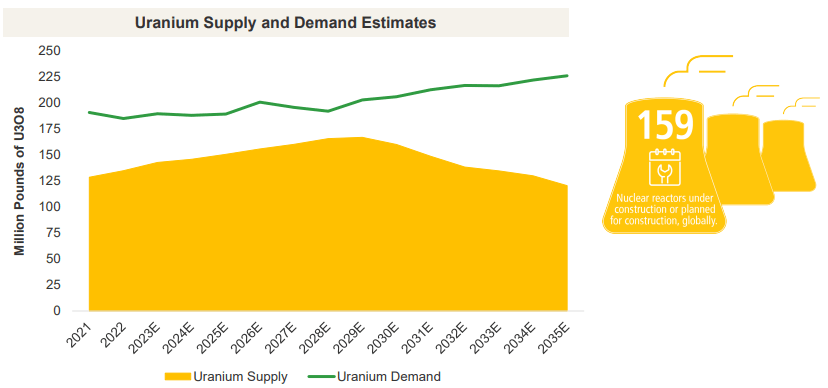

It has to be noted, that the uranium demand is very inelastic to price changes - the U 3 O 8 component in the cost of electricity produced by a nuclear power plant is very low, so even if uranium prices double, the impact on costs will be minimal. Also, nuclear power plants are usually owned and backed by a government, so funding risk is quite low. In that regard, even in the case of a recession, I expect the uranium market to be largely unaffected.

Uranium market projections (UxC LLC)

{kind=link}

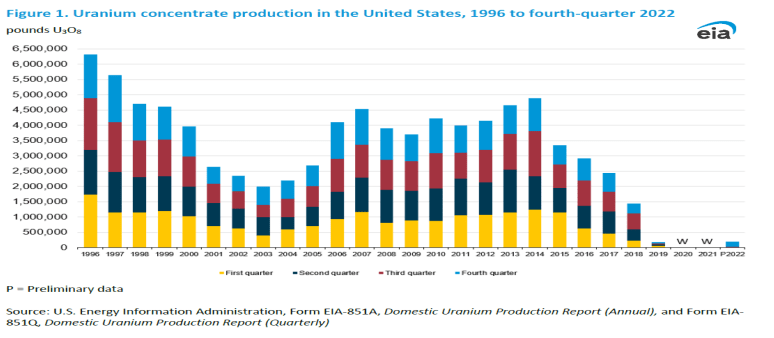

Looking at the uranium market from geopolitical standpoint, the important role of Russia and the former Soviet republic - Kazakhstan in the supply chain has to be considered. In light of the Russian invasion in Ukraine, the west is trying to reduce its dependence on Russia on the nuclear power supply chain. In the case of US, the country is a big consumer of uranium, yet very little is produced domestically. For that reason, the Department of Energy decided to create a strategic uranium reserve and tendered first pounds at about 30% premium to market prices. This highlights the opportunity for a US based producers to capitalize and Ur-Energy looks greatly positioned to do so.

US uranium production/consumption (EIA)

{kind=link}

The case for Ur-Energy

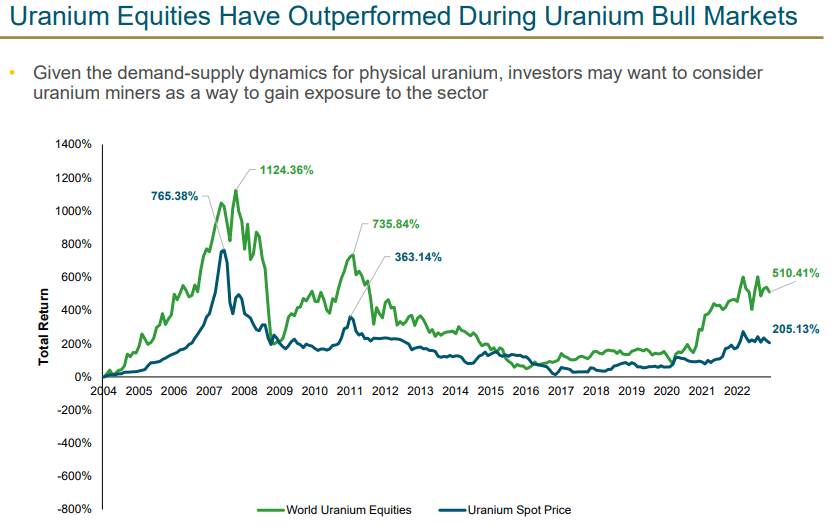

When it comes to commodities, producers often offer leverage to the case of the commodity itself. So in a bull market, those willing to accept higher risk could end up with higher returns. Uranium is not an exception, as equities have considerably outperformed the metal itself in bull markets, as evident from the historical record. Of course, the opposite is also true - in a bear market, the commodity outperforms equities, but as I'm bullish on uranium it makes sense to look into equities for higher returns.

Uranium equities vs uranium (URNM)

{kind=link}

However, not all equities are the same. Most uranium companies are in exploration/development stage, while the biggest producers, with the exception of Kazatomprom and Cameco (CCJ), are not publicly listed. On the other hand, Cameco is diversifying away from being a pure-play miner as evident from the Westinghouse acquisition. So the choice for pure-play producers is rather limited. One of the very few that should be producing pounds this year is Ur-Energy.

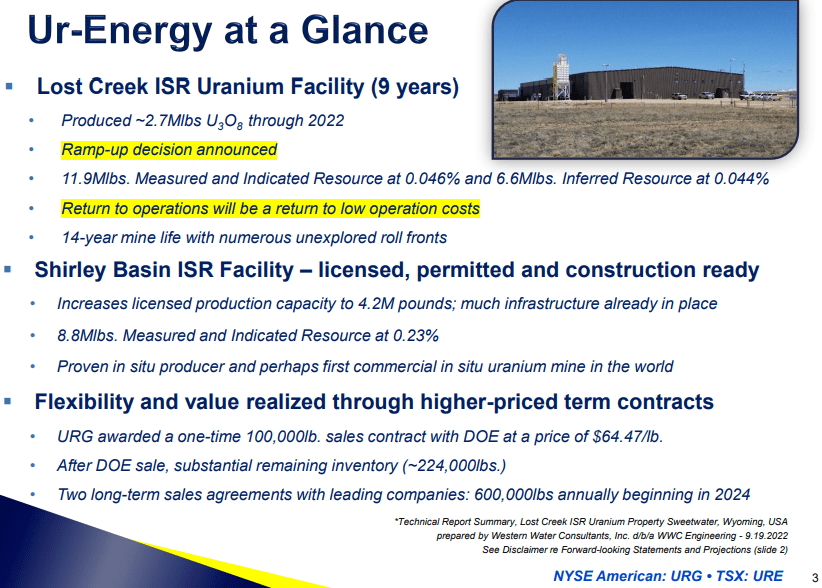

URG's projects

The flagship project of URG is the Lost Creek project in the mining-friendly state of Wyoming. It has been producing in the past and has all the necessary infrastructure already in place. Now that uranium prices have gone up, URG is restarting and gradually ramping-up production up to 1.2Mlbs. Out of those, roughly 50% are already contracted beginning in 2024. According to its Technical report , OPEX is expected to be US$16.34/lbs, while total cost to reach US$33.61/lbs, making the project cash-flow positive in the current environment. The reserve pool of Lost Creek includes 11.9Mlbs of Measured and Indicated as well as 6.6Mlbs of Inferred resources.

Ur-Energy highlights (Ur-Energy)

{kind=link}

The other main project of URG - Shirley Basin has been in operation in the 20th century, using a conventional mining technique. Now URG plans to implement the ISR mining method, which should allow for the project to be economically viable even in the current uranium price environment. The project has estimated OPEX of US$15.95/lbs and total cost of US$33.23/lbs on a reserve pool of 8.8Mlbs of Measured and Indicated resources and projected annual production of 1Mlbs.

Strong liquidity position

Looking at URG's 2022 annual report , the company has US$33M of cash on its balance sheet as well as 325klbs of uranium in inventory. The company anticipated to sell approximately 280klbs of those in 2023 for an average price of US$61.89/lbs and total proceeds of US$17.3M in 2023. At the same time, IB debt on the balance sheet was only US$11.1M.

In 2023, URG announced a public offering, as part of a shelf prospectus from 2021, and subsequently issued 39.1M new shares at US$1.18/share and 19.55M warrants with an exercise price of US$1.50 each for total gross proceeds of US$46.1M. The offering did spook the markets, as shares have dropped significantly since the offering. But looking at it from another perspective, the current price of US$0.88/share offers more than 25% discount to what some large players were willing and did pay a less than two months ago.

With the newly raised capital, I estimate that URG has a net cash position of about US$85M, when accounting for the uranium in inventory and some capital raise-related expenses. This should be more than sufficient to meet the initial capital needs of Lost Creek and Shirley Basin. As infrastructure and production facilities are already built at Lost Creek, URG plans to spent only US$3.2M on one more disposal well, while initial CAPEX at Shirley Basin is projected at US$33.1M.

Valuation

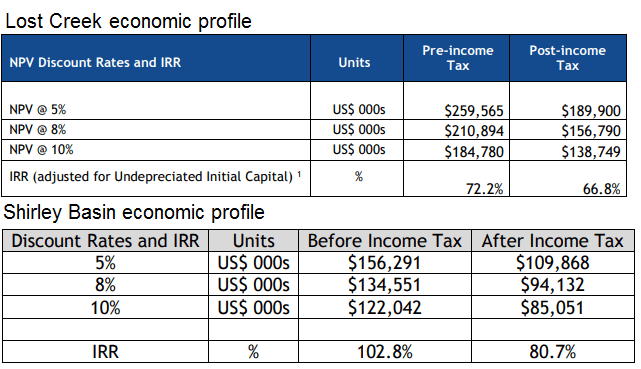

For valuation purposes, I'll use the estimated economics from the technical reports of Lost Creek and Shirley Basin as a starting point. It has to be noted that both reports used uranium price assumption in the low-mid US$60/lbs, which is higher than current market prices, but in line with the price at which URG sold 100klbs to the DoE - US$64.47/lbs.

Lost Creek and Shirley Basin economic profiles (Ur-Energy)

{kind=link}

Looking at the two projects' economic, their combined estimated after-tax NPV, using a 8% discount rate, is about US$251M. Considering the my net cash estimates of US$85M and around 264.7M shares outstanding, the calculations indicate fair value of US$1.27/share or approximately 44.4% upside potential. The fact that the recent offering at US$1.18/share fully subscribed only strengthens my conviction, as large players have found value and upside potential in the company at considerably higher than current prices.

| Unit |

| Projects estimated NPV |

| US |

| 251 |

| Net debt |

| US |

| 85 |

| Implied equity value |

| US |

| 336 |

| Shares outstanding |

| M |

| 265 |

| Fair value |

| US$/share |

| 1.27 |

| Implied upside |

| % |

| 44.4% |

* Author's estimates

Risks

As Ur-Energy has been past producing at Lost Creek and has the infrastructure already built, while Shirley Basin is fully permitted, the risk profile of the company is much better than the median uranium company. Still, some risk have to be considered.

Dilution risk

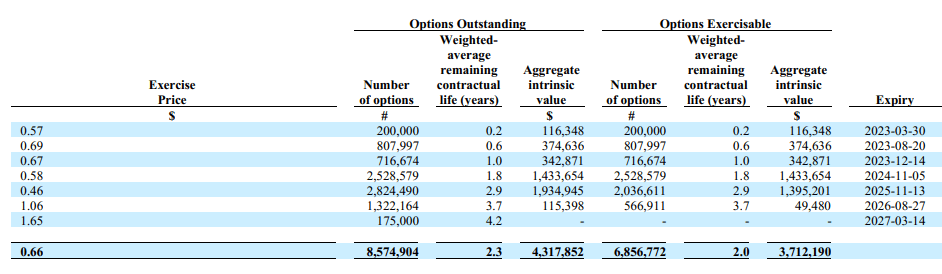

While I find additional equity raises very unlikely, the warrants outstanding could be a source of dilution. As of 2022 year-end the company had 16.7M warrants outstanding with an exercise price of US$1.35 each, which is above my target price. In addition to that the 19.55M warrants from the 2023 offering have to be considered. They have exercise price of US$1.50, which is even higher.

Options outstanding (URG's 10-K)

{kind=link}

However, the company has options outstanding with about 7M of them being in the money and quite likely source of dilution. Still, on a shares outstanding number of 264.7M, the effect will me quite low.

Cost inflation risk

This risk is relevant for all uranium companies. URG is still at better position than most, as initial capex at Lost Creek has been spent long ago, while the ISR mining method is superior to conventional mining in terms of OPEX and should be less affected by cost inflation. Even if Shirley Basin's CAPEX goes up, the liquidity position of URG appears more than adequate to meet it.

Uranium price risk

Obviously, uranium price is very relevant for URG as for any producer. As outlined in the first section of the article, I believe that the supply/demand balance on the uranium market should be supportive of higher prices and adverse price effects are not very likely.

Conclusion

The uranium market is one of the few sectors, which I believe will be largely unaffected by a potential recession. The supply/demand dynamics on the market should support higher prices of the commodity to the benefit of uranium equities. Ur-Energy looks greatly positioned to take advantage with its flagship project already built and with production history. The company is well capitalized and should meet its initial capital needs at Shirley Basin with ease. At the same time, I estimate the fair value of the company at US$1.27/share, implying more than 40% upside.

Editor's Note: This article was submitted as part of Seeking Alpha's Best Investment Idea For A Potential Recession competition, which runs through April 28. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Ur-Energy: Cashed-Up, Production-Ready And Recession Resilient