CCJ - Uranium Energy Corp.: The Good And The Bad

2023-11-21 12:41:20 ET

Summary

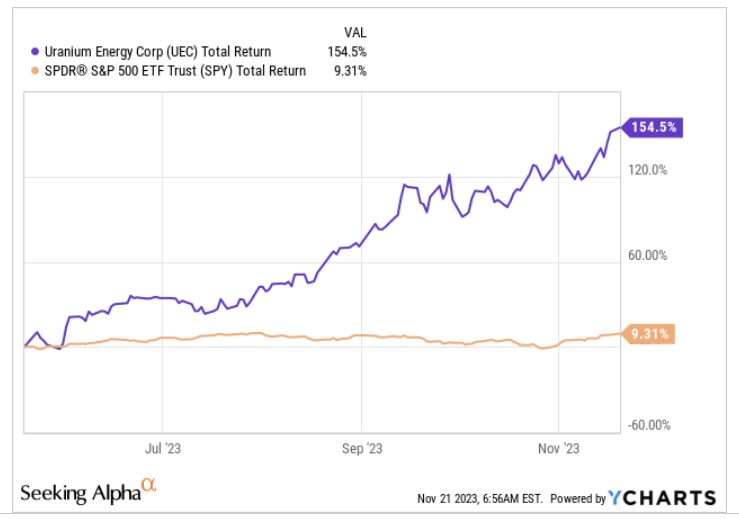

- Uranium Energy Corporation has experienced a 155% increase in stock returns over the past 6 months, outperforming the broader market.

- The growing interest in nuclear energy and the potential for a uranium supply deficit create a favorable landscape for UEC, particularly given its reliance on the spot market.

- UEC has low-cost inventory on its balance sheet, it carries no debt, and its cash is at record highs.

- UEC is a volatile play, and the overreliance on the spot market could put it in a vulnerable position when the market turns.

- Valuations look pricey and the stock looks overbought in the short-term.

Introduction

Over the last six months, the stock of uranium mining firm- Uranium Energy Corporation (UEC) has been on an astounding run, delivering returns of 155%, and thus also trouncing the quantum of returns seen in the broader markets.

{kind=link}

UEC has the wind in its sails and with good reason. However, one may also ponder if UEC would make a great investment at these levels. We have a mixed perspective on UEC and this article will cover some of the major drivers that influence our neutral stance on UEC. We'll first start with the positives before concluding with the less appealing bits of UEC.

The Good

Nuclear energy is on the rise once again, and this bodes well for uranium demand. Increased interest from financial buyers and the growing emergence of small modular reactors of sub 300MW (e) threaten to tilt the demand-supply imbalance in a big way. For much of the last few years, there's been a healthy source of secondary uranium supplies from military stockpiles and the like, but this is finite, and will soon run out. Given the growing risk of geopolitical tensions, the threat of supply disruptions is always looming in the air; this only pressurizes utilities to lock in supplies by attempting to sign more long-term agreements . Meanwhile, uranium producers are still pondering the merits of fresh mining investment as market prices are still not conducive enough to facilitate that (prices would probably need to hit $85-$95 levels), and even if that happens over time, it's not as though fresh inventories are going to come into the system in the blink of an eye. All this suggests that utilities could be staring at a uranium deficit gap of 44m pounds a year, on average, over the next decade (source: UxC). With a lingering market imbalance of this sort, you can imagine how these pressures filter into the spot market. Uranium spot prices are now at 15-year highs with sellers increasing their offer prices every week.

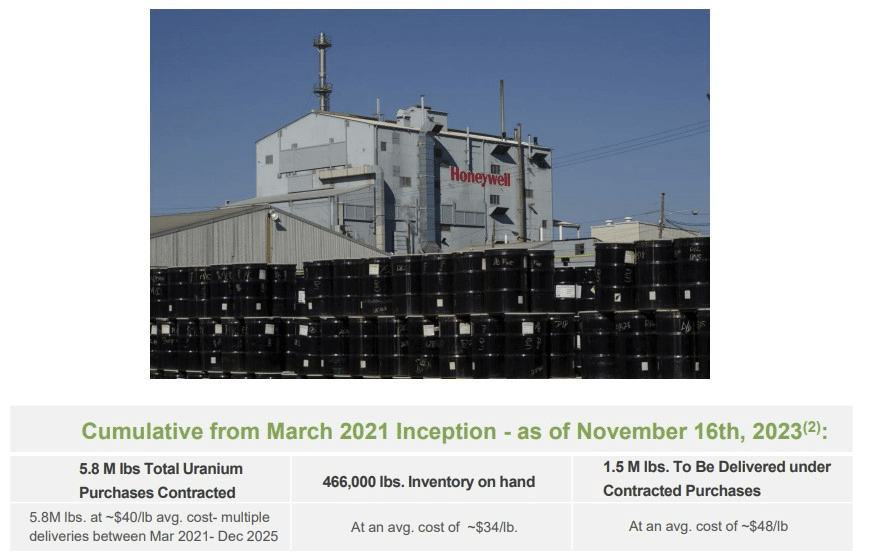

A stock like UEC is very well-positioned to profit from this momentum, as currently, a predominant share of the topline is driven by spot sales of uranium concentrates (for the year ending July 2023 alone, it sold 3.15m pounds of uranium in the spot market). A couple of years back, UEC got involved in a strategic program, that enabled them to purchase drummed warehoused uranium at spot prices that are well below average industry mining costs. As of Nov 2023, the company currently had procured 466k lbs of this inventory at an average cost of just around $34/lb. With some experts suggesting that spot prices could hit the triple-digit mark soon enough, it's fair to say that UEC will get to pocket a tidy profit when it cashes in on the inventory held on its books. Looking ahead, as part of its contractual purchase commitments through FY25, UEC could continue to beef up its inventories at a rather compelling cost of $48/lb.

{kind=link}

In an environment where the general cost of debt has been ramped up over recent years, it is also heartening to note that UEC does not carry any debt on its balance sheet.

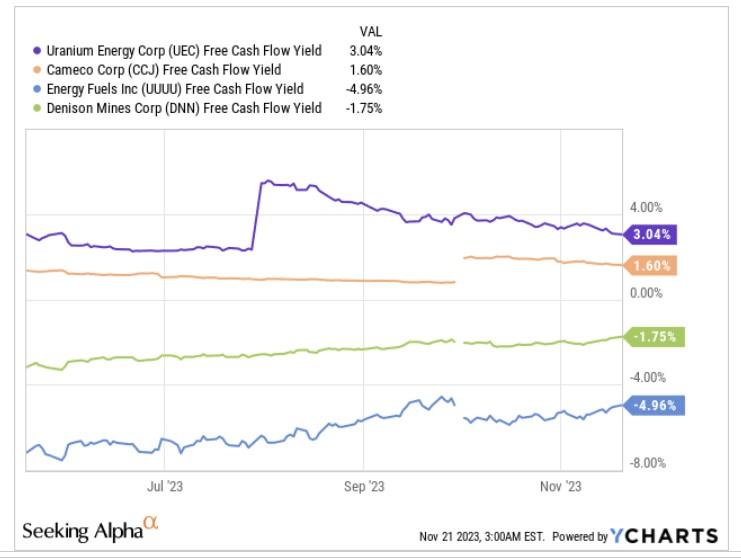

Also note that, whilst over time, some of UEC's in-development uranium projects may have to rely on the more capital-intensive conventional mining techniques, as things stand, its existing mines rely on the In- situ recovery (ISR) method which is a lot more economical to operate. Thus, the impact of strong spot prices (the drop through to the EBIT level is a lot stronger), coupled with low capital intensity means that UEC is one of the few uranium plays that currently offers a decent enough free cash flow yield (this is twice as much as Cameco Corp's associated figure, and infinitely better than the likes of Denison Mines and Energy Fuels that have negative FCF).

{kind=link}

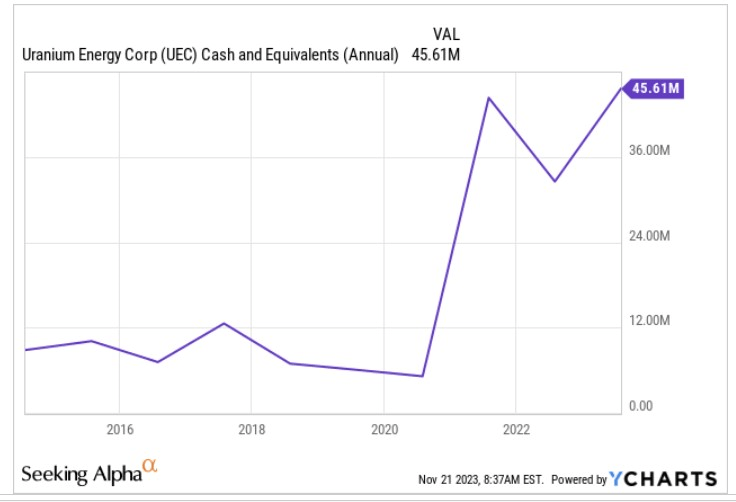

Healthy FCF generation of late has also helped lift UEC's cash balance to record highs of $46m. If UEC can keep up its cash-generating prowess, it could also translate to reduced dependence on its ATM (at-the-market) offering which of course had raised the risk of dilution for existing shareholders.

{kind=link}

The Bad

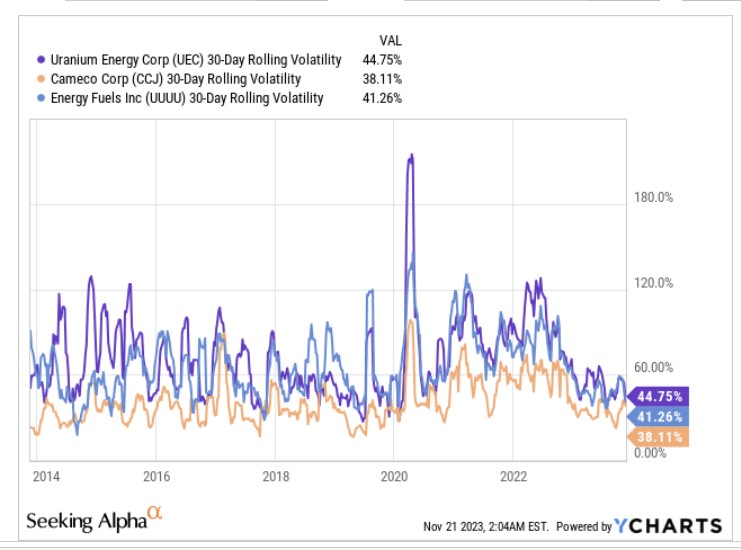

Currently, with uranium spot prices the way they are, no one can deny that UEC is in a good way, but being heavily reliant on the spot market, with no offtake agreements whatsoever, also dampens the revenue visibility and makes the business model quite vulnerable to external volatilities. This filters through to the stock's own volatility profile as well, compared to the likes of Cameco Corp ( CCJ ), or Energy Fuels ( UUUU ) peers which also have a healthy chunk of long-term supply offtake agreements with comforting price floors.

{kind=link}

As we saw a few months back, even a slight whiff of negative news flow linked to the demand-supply balance in the uranium market can leave a pronounced mark on the UEC stock. Note that when the Kazatomprom production news dropped in late September, uranium stocks took a beating across the board, but UEC saw the biggest impact (-8%).

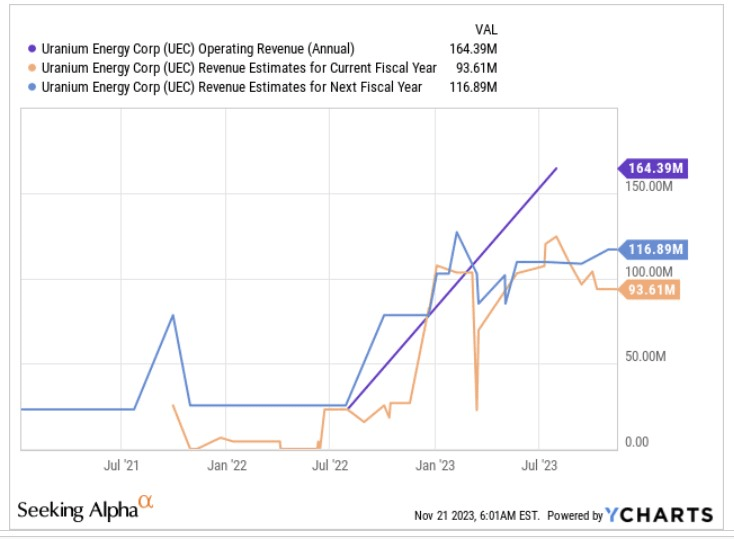

Nonetheless, when one reviews consensus estimates for UEC over the next three years, it's not too comforting to see the degree of topline volatility on offer. After delivering over $164m for the fiscal ending July 2023, consensus believes that revenue will compress by -43%, before growing by 25% the following year. As things stand, the July 2025 expected revenue could still be around $48m short of what was delivered in the most recent fiscal year.

{kind=link}

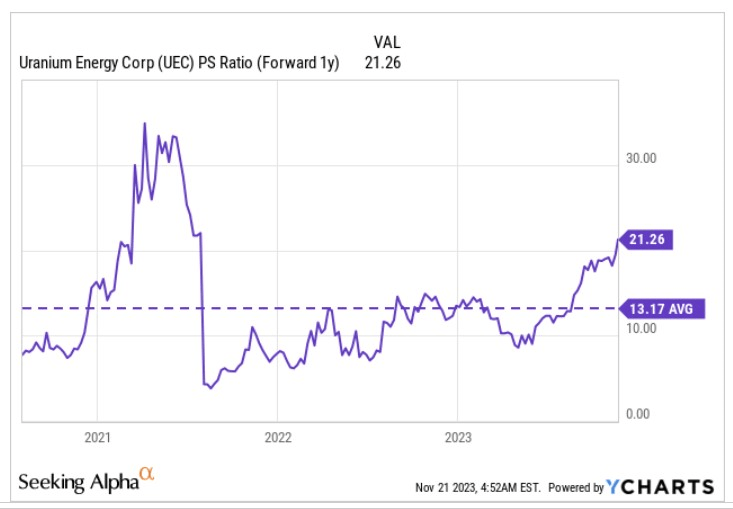

Considering the haphazard revenue profile, it doesn't make a great deal of sense to shed out a forward price-to-sales multiple of 21.2x, which also incidentally represents a massive 61% premium over the stock's long-term average.

{kind=link}

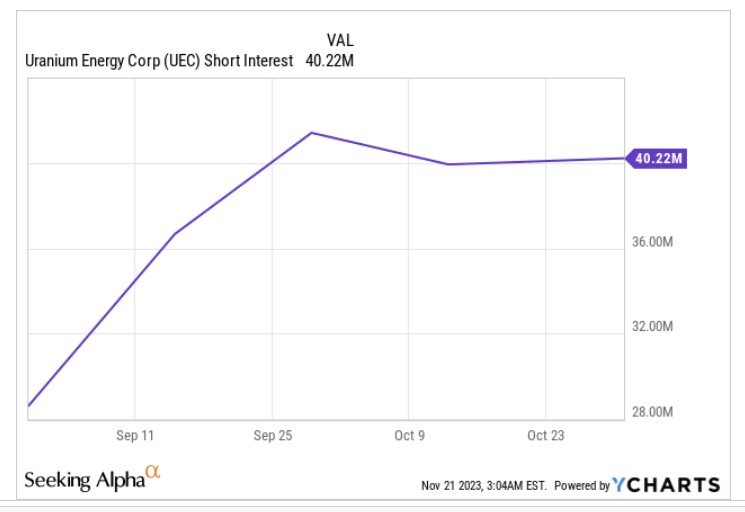

The bears also appear to have taken a fancy to UEC in recent months with the short interest on the stock rising by over 40% in recent months. In light of this some of you may also point to the prospect of increased short-covering, but to counter that we'd say the days-to-cover ratio is still quite low at only five days or so.

{kind=link}

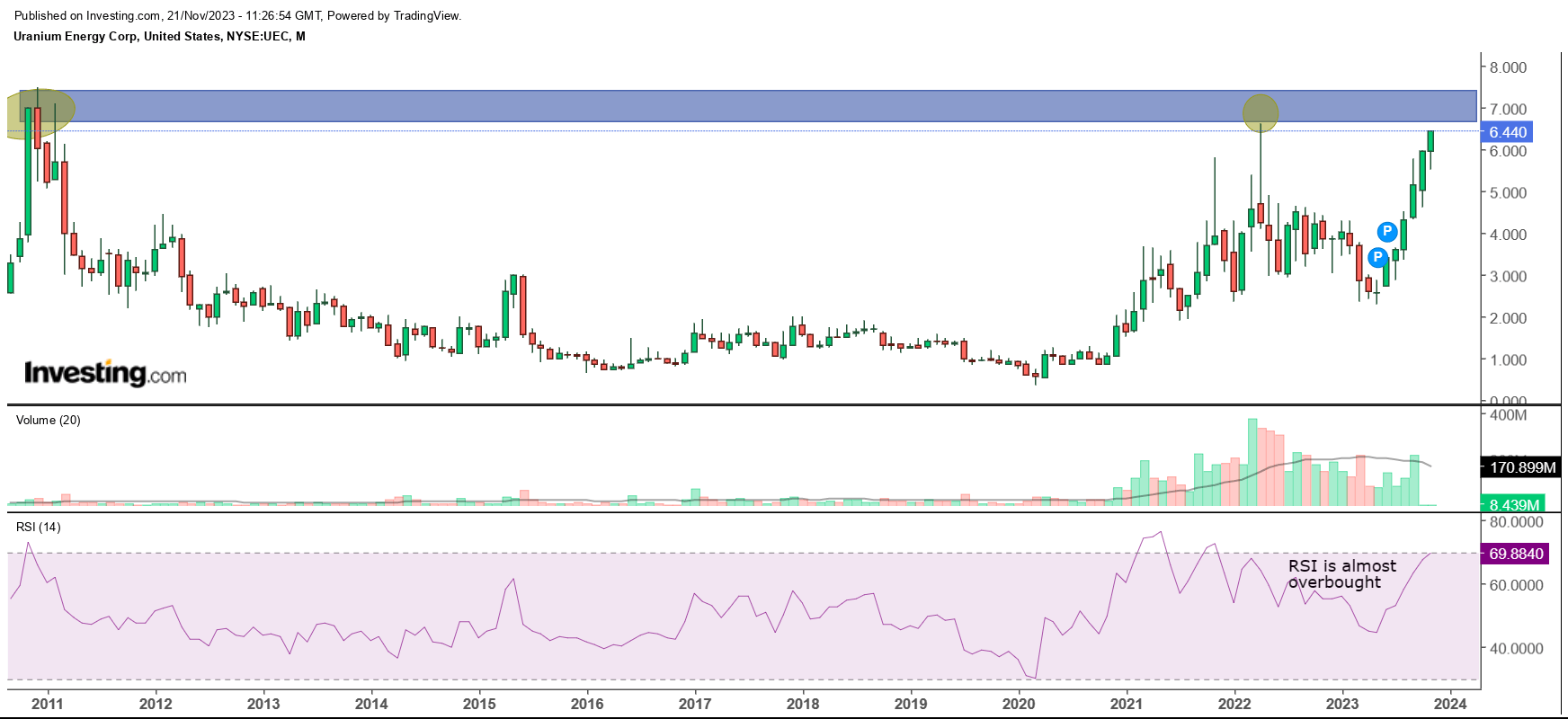

Then when it comes to the charts, UEC appears to look overbought in the short-term at least. Since June, we've seen six straight monthly candles where the opening price has been higher than the closing price, and now the stock is on the verge of hitting the $6.60-$7.50 range; we've seen previously how this terrain has worked as a pivot zone on two separate occasions; back in late 2010, and in April 2022, so don't be surprised to witness some profit booking around these levels.

In fact, you'd also be interested to note that after months of no insider activity, in recent weeks, the CFO of UEC has chosen to trim his position in the stock. It's also worth considering that the default 14-period RSI is now almost on the cusp of hitting overbought levels, something which has traditionally failed to persist on the monthly chart.

{kind=link}

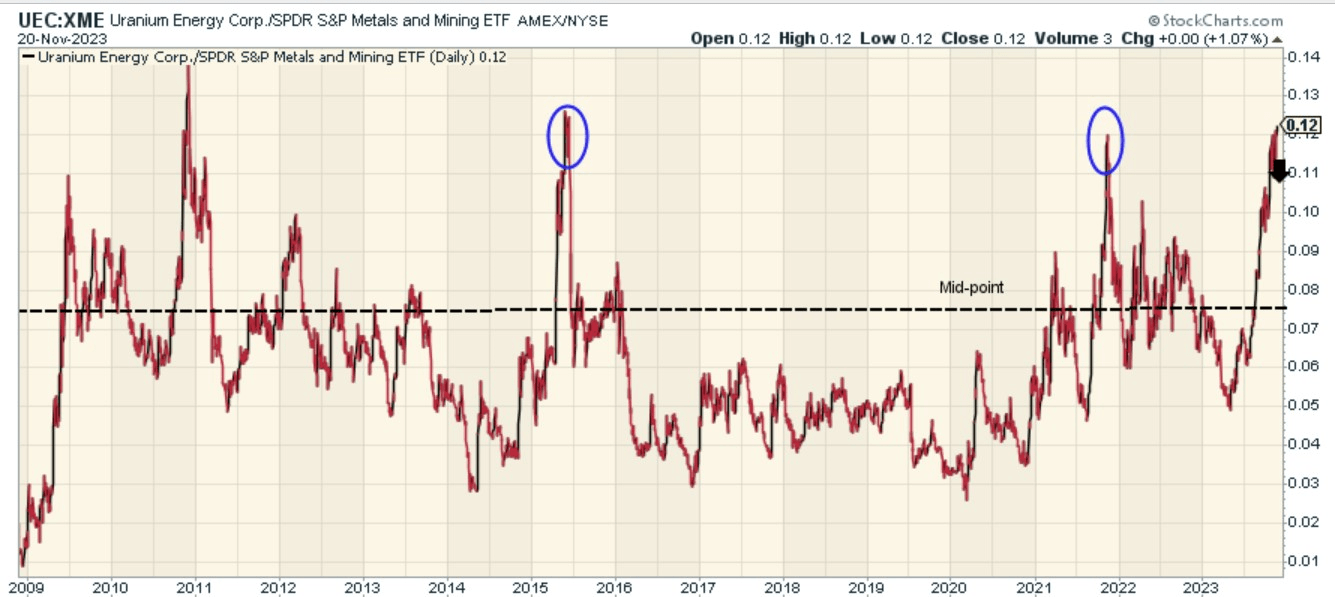

Finally, also note how UEC is positioned relative to its peers from the broader metals and mining universe. It's difficult to make the case for UEC benefitting from further rotational momentum as its relative strength ratio versus its peers from the SPDR Metals and Mining ETF is trading around 60% higher than the mid-point of its long-term range. Crucially the relative strength ratio is not far from hitting the 2015 and 2021 levels from where we've previously seen a shift.

{kind=link}

For further details see:

Uranium Energy Corp.: The Good And The Bad