CA - Uranium: Still A Lot Of Room To Run

2023-12-11 09:23:55 ET

Summary

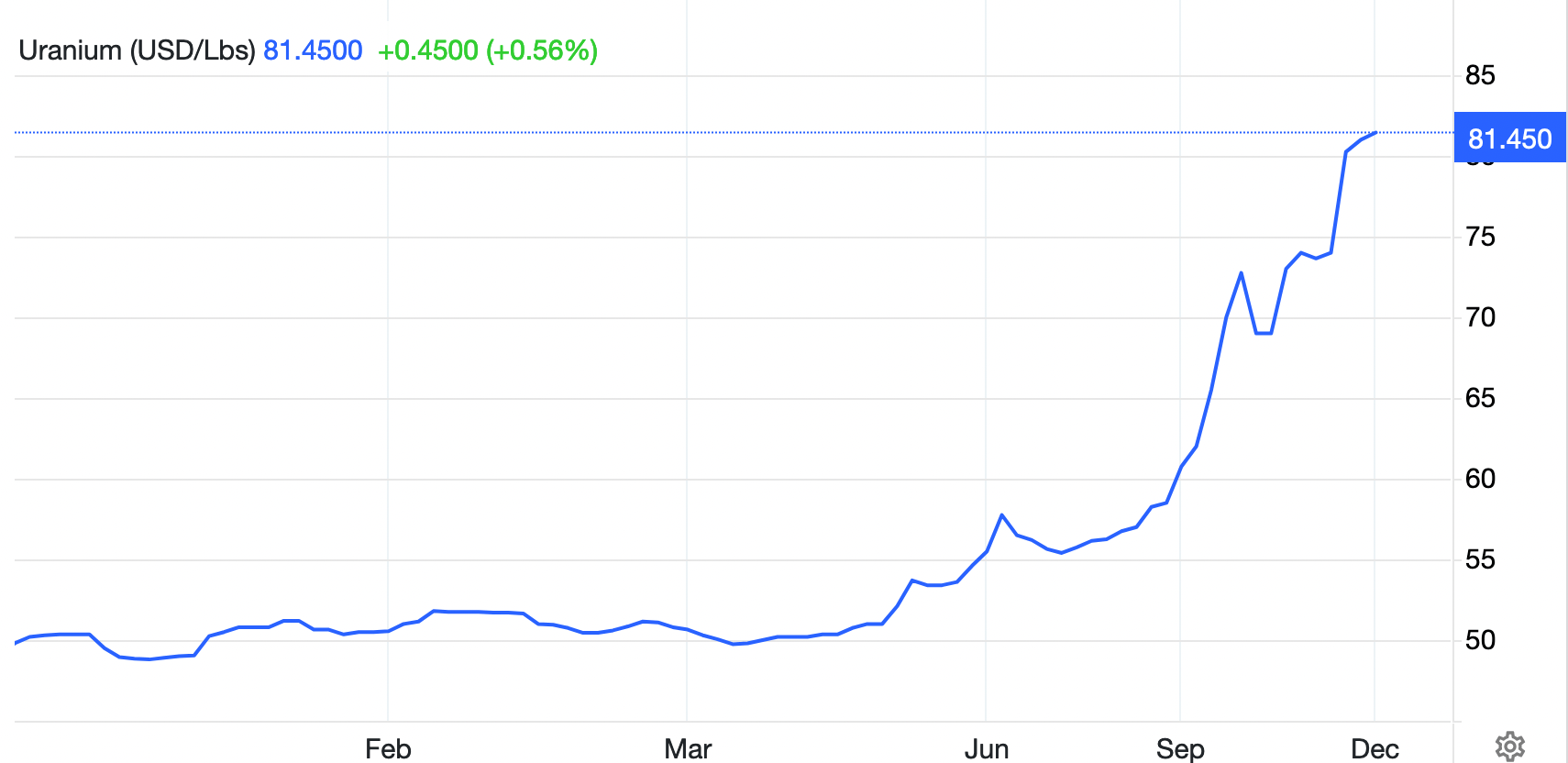

- Uranium prices have surged almost 40% this year.

- Nonetheless, uranium is the commodity I am most bullish on over the next 12 months.

- A structural imbalance between primary supply and demand, growing demand, potential supply shocks, and rising production costs: all imply the uranium price still has a lot of room to run.

- A thinning spot market and a more active long-term market are signaling that the uranium market is getting tight.

Uranium has been one of the best-performing commodities year-to-date, up almost 40%. The spot price surged above $80 per pound in November, a level not touched since January 2008, prior to the Fukushima nuclear disaster. Heightened risks to the supply, increasing demand, and a market facing a structural deficit have been the main drivers. Despite the substantial appreciation, I believe that uranium still has a lot of room to run.

{kind=link}

The dynamics of the uranium market differ significantly from other energy commodities, such as oil. While the price of oil reacts almost immediately to geopolitical events, inventory data, supply shocks, and macroeconomic forces, the same cannot be said for uranium. Only about 20% of uranium volumes are traded in the spot market. Furthermore, the spot market is relatively illiquid: the spot price is determined as the mid-point between the end-of-day bid and ask prices, even if no transactions occurred during the day. Traders, speculators, utilities, and even miners are all active in the spot market from time to time.

However, the real action takes place in the long-term market. Long-term contracts are awarded by utilities to producers. These contracts typically consist of a fixed-price component and a market-price component. They undergo extensive negotiations and span several years. This means that the long-term market moves at a slow pace. While the spot price leads to the long-term price, both prices require several years to adjust to external supply and demand forces.

Let's start by having a look at the demand side. Since the construction of a new nuclear plant is a big public project that takes years to complete, it is easy to project the number of future reactors. Currently, around 60 reactors are under construction , with an additional 110 in the planning stage. Notably, half of these planned reactors are set for construction in China . There are approximately 440 active nuclear reactors today. Amid oil volatility and escalating decarbonization targets, nuclear energy is increasingly recognized as the sole reliable, low-emission form of baseload power generation. The tides are turning.

Uranium demand is not solely contingent on the absolute number of reactors in the current global nuclear fleet. Uranium enrichers can vary their demand based on the economics of the enrichment process. Essentially, during periods of low prices, enrichers turn to underfeeding (utilizing less uranium material than average in input, to achieve the same enriched uranium in output, albeit with extended processing times). Conversely, in times of high prices, enrichers resort to overfeeding to maximize profits. The prices for enrichment and conversion have seen a significant rise following the invasion of Ukraine by Russia, which still controls a substantial portion of both markets. The shift from underfeeding to overfeeding is underway, creating an additional significant source of demand.

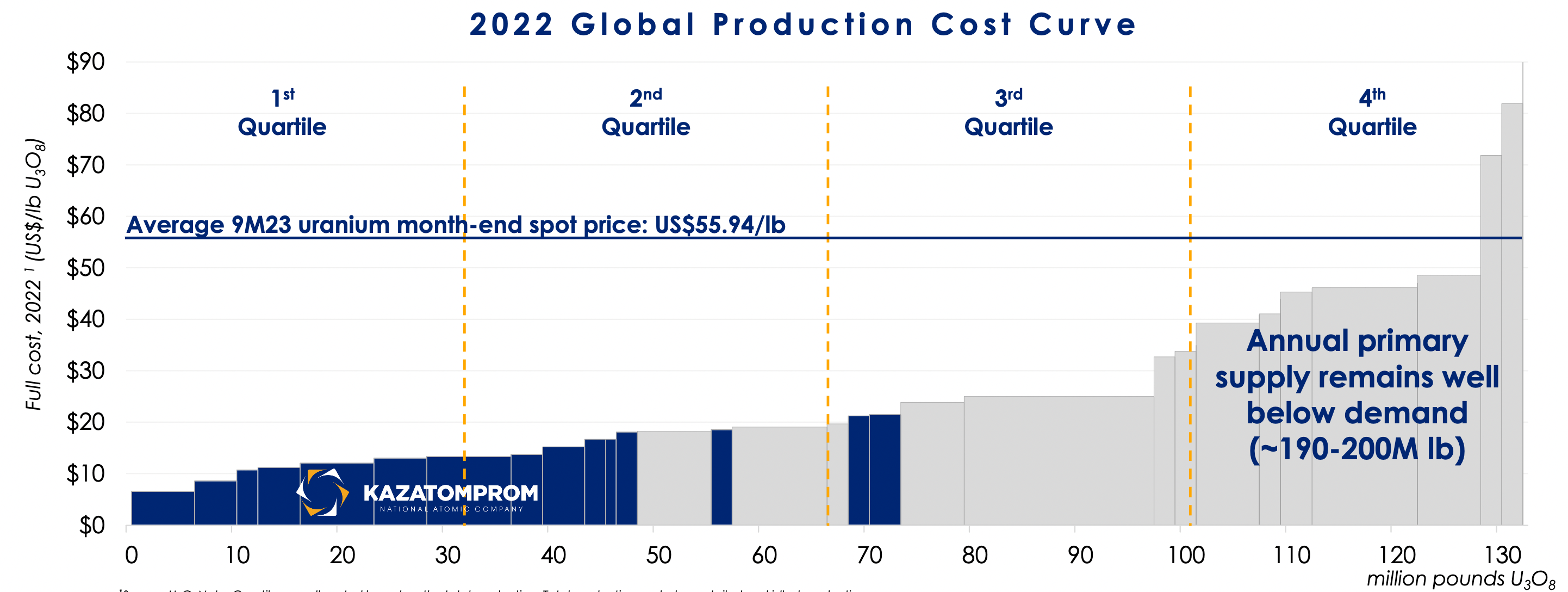

Let's now examine the supply side. Due to secondary supply sources, uranium producers such as Cameco and Kazatomprom have reduced production for several consecutive years. While this has contributed to slowly rebalancing the market, it also means that there is currently a substantial gap between demand and primary supply. Primary supply hovers around 130 million pounds, while demand is approximately 200 million pounds. New primary supply is not incentivized enough to come online: even with spot prices surpassing $80 per pound, the long-term price remains considerably lower. As a result, a significant portion of the global supply curve still falls below the breakeven price for producers.

The graph below shows the global production cost curve for uranium miners in 2022. It is reasonable to assume that another year of inflationary pressures and labor shortages has led to an increase in production costs.

Global uranium production costs (Kazatomprom's Investors Presentation)

{kind=link}

Uranium supply is also sensitive to geopolitical events. Around two-thirds of primary supply originates from the East, while two-thirds of demand is concentrated in the West. This renders the West particularly vulnerable to supply shocks. To provide two concrete and recent examples, Global Atomic Corporation is delaying the commissioning of the processing plant at the Dasa project by 6-12 months due to the military coup in Niger. Cameco has recently revised its production volume guidance for 2023 downward from 18 million to 16.3 million pounds due to technical issues. Mining is a challenging business, especially in the current geopolitical and macroeconomic environment.

For all the above reasons, uranium is the commodity I am most bullish on over the next 12 months. While I have been optimistic about oil prices (and still am for the long term), the surge in spare capacity from OPEC+ and record production from North American producers imply that the supply side is not in my favor. The demand side may also face negative impacts from a potential recession. Though I am bullish on precious metals, I doubt they will be able to break out if the Fed keeps interest rates elevated. Uranium, however, does not have any of the above problems.

Uranium does not have a supply problem: primary supply is significantly below demand. The current annual deficit of 70 million pounds can be temporarily offset by secondary supplies. However, these secondary supplies are diminishing, as the rising spot price proves. Uranium does not have a demand problem: barring another nuclear accident, demand is projected to steadily increase for many years to come. Uranium lacks the sensitivity of gold and other precious metals to macroeconomic factors, such as high interest rates.

With a sizable portion of the global cost curve still below spot prices, the downside is limited. The upside, however, remains significant. The unique dynamics of the uranium market, coupled with various potential catalysts (like a ban on Russian uranium and the shift from underfeeding to overfeeding) lead me to believe that there's a reasonable probability of the uranium price eventually overshooting the economic price significantly.

Current trends in both the spot and long-term markets appear to validate the belief that both are becoming exceptionally tight. According to a statement from Kazatomprom:

[…] spot volumes transacted over the first nine months of 2023 were about 20% lower compared to the same period last year. During the nine months of 2023, a total of approximately 32 million pounds U3O8 (12,400 tU) were transacted at an average weekly spot price of US$54.67/lb U3O8, compared to about 41 million pounds U3O8 (15,800 tU) at an average weekly spot price of US$49.67/lb U3O8 over the first nine months of 2022.

In addition:

In the term market, third-party data indicated that contracted volumes totaled to about 145 million pounds U3O8 (55,700 tU) throughout the first nine months of 2023, compared to about 85 million pounds U3O8 (32,700 tU) in the same period of 2022. The 70% increase in term contracting activity to date in 2023 led to a significant US$10.50/lb U3O8 increase of the long-term price indicator at the end of the third quarter, resulting in an average term price of US$61.50/lb U3O8 (reported on a monthly basis by third-party sources).

In summary, the spot market is experiencing increased illiquidity as volumes are withheld due to the anticipation of rising prices. Simultaneously, utilities are becoming more active in the long-term market. This bullish dynamic is possible because secondary sources are no longer as abundant.

How to speculate on rising uranium prices? Since the market is small and opaque, there is no future market. However, there are two quoted instruments: the Sprott Physical Uranium Trust ( SRUUF ) and Yellow Cake ( YLLXF ). Both maintain an inventory of physical uranium and trade close to its asset value. The main difference is that Yellow Cake is actively managed, while the Sprott Physical Uranium Trust is passively managed. Both funds can only buy uranium. They are not supposed to sell.

This raises an interesting question about the endgame for these instruments. In the event of a significant overshoot in uranium prices, how would the public react to the knowledge that there are physical inventories hoarded purely for speculation? If the Sprott Physical Uranium Trust were to trade at a premium to NAV due to an influx of new money into the sector, the trust would be forced to buy uranium at any price, thus pushing it even further. Would regulators simply stand by and watch? Would Yellow Cake and the Sprott Physical Uranium Trust eventually decide to liquidate their inventories? Would the price collapse following such an announcement? Because of these risks, I maintain an allocation to uranium equities, particularly producers like Kazatomprom.

For further details see:

Uranium: Still A Lot Of Room To Run