NOC - US Defense 2024: Promising Triad Of Geopolitical Tensions Budget Growth And Uncaptured Buyback Potential

2024-01-13 02:22:31 ET

Summary

- I view the US Defense Primes as a strong investment case in 2024 given a 9% rise in defense budgets and an additional ~7% upside from Biden's supplemental aid request.

- After underperforming in 2023, I see the sector as attractively valued, trading at an 11% discount to the market compared to an average of 4% for 2022/2023.

- I prefer GD on the back of currently uncaptured buyback potential (~1/3 of historical average priced in) and see ~9% upside to consensus FY25 EPS.

- Underpinned by an undemanding valuation and the strongest estimated total return potential, I am Overweight GD/ Equalweight NOC/Underweight LMT.

I like the US Defense Primes ( GD , LMT , NOC ) for 2024 due to further growing US defense budgets and relative undervaluation vs the broader market. Current global conflicts and a 9% in the US defense budget should spur demand for both placement of new orders and procurement of replacements and ammunitions while recently launched platforms (F-35, B-21, Virginia-Class) provide multi-year earnings visibility for the Primes. With the Fed's hinting at a soft landing, defense has underperformed in 2023 versus riskier sectors, currently trading at a ~7% greater discount to market than historical average since the onset of the Ukraine war (Primes/SPX at 0.89 vs average of 0.96), making the sector relatively cheap.

Among the Primes I prefer GD given the potential for c.9% FY25 EPS upgrades on the back of share buybacks and undemanding current valuation vs peers and recent average (Overweight, PT $307). I also see some upside in NOC with c.3% FY25 EPS headroom from buybacks but remain cautious on ~17% valuation premium to GD and LMT (Equal weight, PT $539). I am slightly less constructive on LMT given flattish near-term EPS outlook and lack of further buyback upside (Underweight, PT $487).

Key risks remain in slower than expected supply chain recoveries leading to lowered profit expectations for the Primes and political standstill in Washington which could delay appropriated funding. However, with elections coming up and no end to the Ukraine War and Middle East tensions in sight, I believe National Security discourse will see significant tailwinds in the second half of the year.

[NOTE: Ratings are relative to each other and on a 12 month timeframe, hence Underweight LMT does not indicate a "Sell" recommendation]

2024 Defense Budget looks attractive with 9% YoY Growth and Potential for ~7% additional Allocation for Ukraine and Israel

Approved on December 14 , the 2024 US defense budget will reach $886bn, representing its highest ever and growing ~9% YoY amid ongoing global conflicts affecting both its allies and the US directly. Next to the ongoing war in Ukraine which is still without any clear end in sight, the Middle East has reemerged as a source of serious geopolitical turmoil. An open war turned border incursion between Israel and the Hamas with the potential to escalate into neighboring Lebanon, attacks on global shipping lanes by Iran-backed Houthi rebels in Yemen and bombings in Iran have caused US allies in the region to place their militaries on highest alert .

US Defense Budget (US Congressional Office)

Next to the 9% growth in the official defense budget, President Biden has also placed a supplemental aid request of ~$106bn, of which $65.8bn (~62%) are proposed for military use. In detail the request seeks ~$46bn in additional funding for the US military aid program to Ukraine, mainly focusing on ammunitions and maintenance-related products next to replenishment of US stockpiles. Given its "combat-ready" character, I see this benefitting GD the most given their portfolio skew towards ammunitions and combat vehicles which contribute the majority of US military aid to Ukraine. Next to ~$14bn for Israel and $2bn in support of US allies in the Pacific (including Taiwan), the bill also seeks $3.4bn in additional funding to improve availability of the Virginia-Class submarine which is manufactured by GD's Electric Boat division and has seen significant production issues due to supply chain problems recently.

If passed, the request could provide an additional 7.4% to US 2024 defense spending. However, as of current the bill is still heatedly debated in congress with Republican lawmakers aiming to secure additional funding for border security as part of the request.

Supplemental Aid Request Split (Bloomberg)

While the Sector is not cheap, current Multiples are below L2Y Average relative to Market after 2023 Underperformance

Defense Primes have significantly underperformed in 2023 with LMT and NOC ending the year lower at -7% and -14% and GD just barely closing positive as opposed to a 24% gain for the SPX . With concerns around a potential government shutdown in H1 and growing risk appetite on the back of increasing likelihood of 2024 interest rate cuts, investors rotated into higher beta sectors such as technology despite what I believe are still excellent underlying prospects for the Primes. Global tensions have not diminished but grown and thus much of the initial investment thesis on Defense is still intact, best evidenced by the sharp rise in Primes' share prices following the Israel/Hamas incursion in early October.

On a valuation basis, the Primes currently trade at 18.2x blended forward ("BF") P/E, a slight ~2% premium to their average valuation over the last 2 years while the SPX trades at a ~10% premium. I view the last 2 years as an appropriate time frame given it broadly reflects the period since Russia invaded Ukraine. Driven by their 2023 underperformance, the Primes therefore currently trade at just 0.89x SPX on a BF P/E, a 7% discount to the L2Y average ratio of 0.96x Primes/SPX making the sector historically cheap on a relative basis.

Current vs Historic Multiples (Bloomberg)

NOC is currently valued at the largest multiple premium (4%) relative to historic average, trading at a current BF P/E of 20.2x vs a L2Y average of 19.4x. Notably, NOC also trades at a ~17% premium to LMT and GD on the back of its alignment to key DoD strategic priorities in space and nuclear deterrence (B-21 bomber, Sentinel ICBM). LMT is in line with the sector at a 2% premium to historical at 17.3x BF P/E as its F-35 Joint Strike Fighter program is partially offset by ongoing supply chain problems driving lower expected deliveries.

GD is the only one of the Primes to trade at a discount relative to history with current valuation of 17.2x giving a ~1% discount to L2Y average. While the company has seen significant issues with its supply chain over the past year forcing it to revise expectations for both its defense and commercial aerospace businesses, I see a lot of strength in its "combat-ready" portfolio. With a large part of revenues derived from ammunitions and vehicles, which constitute the majority of US military aid to its allies, I see GD as the positioned to further capitalize on ongoing wars in Ukraine and the Middle East and the US' military aid spending.

Current vs Historic Multiples (Bloomberg)

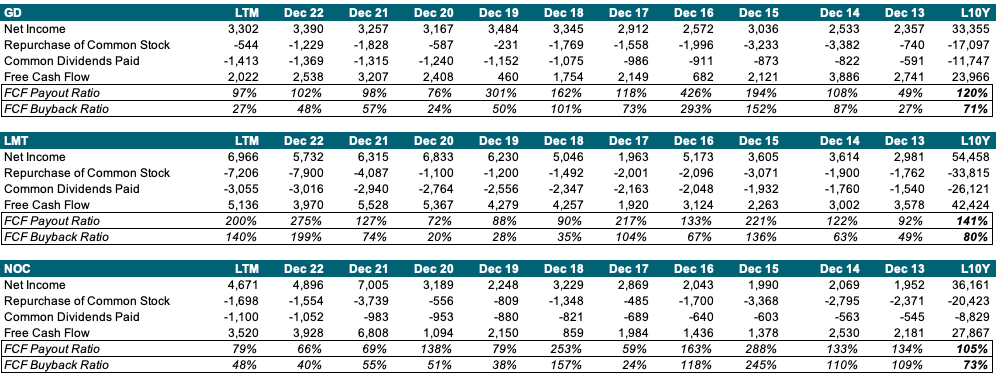

Shareholder Return Potential based on L10Y Buyback/FCF Ratio priced in to various Degrees, I see ~9% Upside to GD FY25 EPS

Over the last 10 years, Primes have spent ~70-80% of their FCF on buybacks for total shareholder yields incl. dividends of >100%.

{kind=link}

This shareholder-friendly cash allocation has on average reduced share count by ~26% with GD and LMT both buying back around 20% and NOC retiring more than 30% of shares.

Looking at consensus implied ratios of estimated buybacks to estimated FCF generated, while LMT and NOC are largely in line with their historical allocations, I see a significant diversion for GD . Consensus currently only prices in ~24% of total FY23-25 FCF to be used for buybacks which I see as significantly mispricing given both the company's and management's history of retiring shares.

% of FCF Allocated to Buybacks (Company Information, Bloomberg Consensus)

Assuming historical ratios of buybacks to FCF for each of the Primes, I estimate GD could retire up to 11% of its shares until year end FY25, around 3x of what consensus implies at 4%. I also see some upside for NOC with ~7% vs ~5% while LMT's buyback potential is well priced in. I note that this is likely a result of the already fixed authorization of $13bn over the period, recently raised by $6bn which roughly corresponds to my calculated potential.

FY23-25 Buyback Potential (Bloomberg Consensus)

Given GD's potential for significantly higher buybacks than currently priced in, I see ~9% upside to FY25 EPS consensus should it return to its historically implied FCF allocation. NOC offers around 2% with LMT being largely priced according to its historical buyback ratios. Across the group I see ~3% FY25 EPS upside, largely driven by GD .

Upside to FY25 EPS on Historic Buyback/FCF Ratio (Author's Projections)

Assuming L2Y Average Multiples and full Buybacks, Primes could offer on Average ~16% Total Return through 2024

Applying a target P/E multiple equal to the last 2 years' average on my FY25 EPS estimate for each of the primes I derive target prices of $307, $488 and $539 for GD , LMT and NOC respectively.

US Primes Target Price Calculations (Author's Projections)

{kind=link}

Adding current implied forward dividend yields to my calculated 2024 price upsides I estimate an average of ~16% total return potential across the group. GD tops return potential on the back of its currently underestimated buyback capacity and slightly depressed valuation with LMT below group average and NOC roughly in line. I therefore assign GD an Overweight rating, NOC an Equal weight and LMT an underweight.

Potential 2024 Total Returns (Author's Projections)

For further details see:

US Defense 2024: Promising Triad Of Geopolitical Tensions, Budget Growth And Uncaptured Buyback Potential