REPX - USO: Crude Oil Spike Usually Appears At End Of Economic Cycle (Rating Upgrade)

2023-07-15 06:28:42 ET

Summary

- I am shifting from a neutral to bullish stance on oil/gas assets, with the potential for shortages in crude oil supply by the summer of 2024.

- Risks to oil supply include any disruptions from geopolitical events caused by the ongoing Russia/Ukraine war, potential Chinese invasion of Taiwan, or possible Israeli attack on Iran's nuclear facilities.

- United States Oil Fund could be a smart play due to overly-bearish futures player positioning, the backwardation of futures, and beneficial interest rates earned on cash holdings.

- Dwindling U.S. Strategic Petroleum Reserves for future emergencies, production cuts from OPEC+, plus a better demand outlook during a soft landing in the economy may reverse 2023's crude oil price slide.

I have been moving from a correctly bearish stance on oil/gas assets (following the Russian-related spike in prices over a year ago) toward a reasonably bullish outlook of late. The reason: typical end-of-cycle patterns for the world since the early 1970s usually include an oil shock that pushes economic growth into reverse, after years of underinvestment in producing assets is matched against expanding demand for energy.

The most direct and cost-effective way for retail investors to buy crude oil in regular brokerage accounts is through United States Oil Fund, LP ETF ( USO ). Why consider USO now?

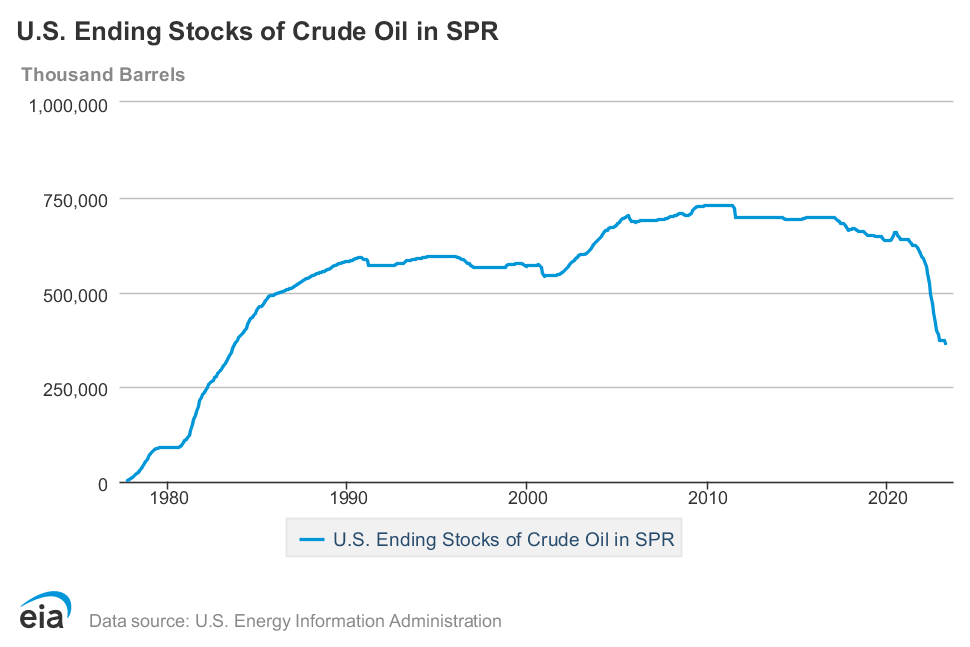

If we can escape with a "soft landing" for the economy in the second half of the year, demand trends will almost certainly beat current forecasts. Then consider OPEC+ production cuts during 2023 have been extended, U.S. production levels of 12.3 million barrels a day remain below the 2019 highs of 13+ million, and the U.S. emergency release of Strategic Petroleum Reserves could soon be exhausted. [The bad news is SPR supplies are back to 1984 ranges, at half the level of 2010, leaving little help from this storage depot in another supply crunch.]

EIA Website - U.S. SPR Monthly Totals, Since 1979

{kind=link}

Putting all the variables together, after returning to normal inventory levels worldwide in the summer of 2023, energy experts are again looking ahead to a shortage situation possibly redeveloping by next summer in crude oil. Below is an inventory graph from a July article presented by the U.S. Energy Information Administration .

EIA Website - Global Inventory Data, 2024 Forecast

My research suggests a short-term equilibrium for crude oil supply/demand could give way to a much tighter market, unless we experience a serious recession to slow demand growth.

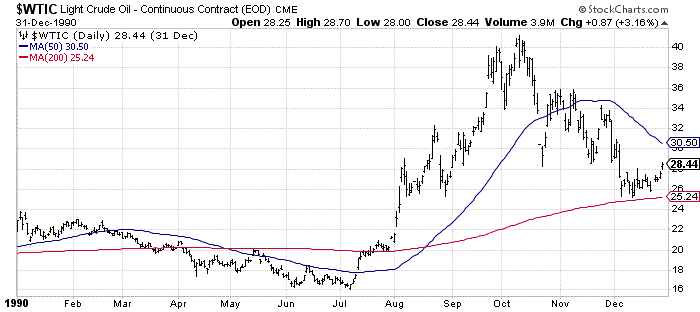

My main worry is any unexpected supply disruption could easily generate an oversized price advance above US$100 a barrel quickly. Such an outcome would really throw a monkey-wrench into Fed plans to halt interest rate hikes, as inflation could ramp past 5% YoY again. [You can read more about how a sizable upmove by crude into 2024 could reverse inflation rates in the wrong direction here , a story I wrote days ago.] In particular, I am increasingly concerned we are sitting in a similar financial spot as the summer of 1990, before Saddam Hussein invaded oil-rich Kuwait .

1990 Similarities

The U.S. experienced an inverted Treasury yield curve from the middle of 1989, while the stock market was able to hold in place for a good year, despite weak performance from smaller caps and banks. Breadth participation overall was horrible, as a select number of blue chips held up the market averages. Sound familiar?

Of course, crude oil prices spiked from US$16 a barrel in July to $41 in October. America engineered a coalition of nations to respond militarily and push Iraq out of Kuwait, as fears Saudi Arabian oil fields would be next to be conquered. The 1990-91 Persian Gulf War scared the world into recession and sent the S&P 500 down -20% between late summer and early winter.

StockCharts.com - Daily Crude Oil Price, Nearby WTIC Futures, 1990

{kind=link}

My view is something akin to this period in history could repeat (or at least rhyme). The number one potential "black swan" catalyst/risk today for the energy markets to be roiled, equities hit, and economy tripped into recession may come from an out-of-the-blue Israeli air bombing run on Iran's nuclear facilities. It's an issue crude oil players do not rank highly on their watch list, but we might not get any warning when/if it happens. For sure, the re-election of conservative and fierce Iran-critic Benjamin Netanyahu in late 2022 has dramatically shifted the odds of a war between the two nations.

Present estimates for the number of days for Iran to reach breakout levels for its uranium enrichment , enough to build a nuclear device, range from days to weeks, if and when such a political decision to proceed is made. In terms of good news, as far as U.S. intelligence can tell , Iran has not yet put together a workable weapon.

Other risks to supply include the ongoing Russia/Ukraine war and repercussions to oil/gas flows to Europe, plus the potential for China to shut down shipping routes in Asia in the event of an invasion of Taiwan.

United States Oil Fund

I did mention supply-chain risks for crude oil when I upgraded my United States Oil Fund outlook from Sell to Neutral in September 2022 here . Unfortunately for aggressive bulls and bears, USO in the middle of July is trading at almost exactly the same price from my last article 10 months ago. As a consequence, market players are now being lulled to sleep by low-volatility trading action.

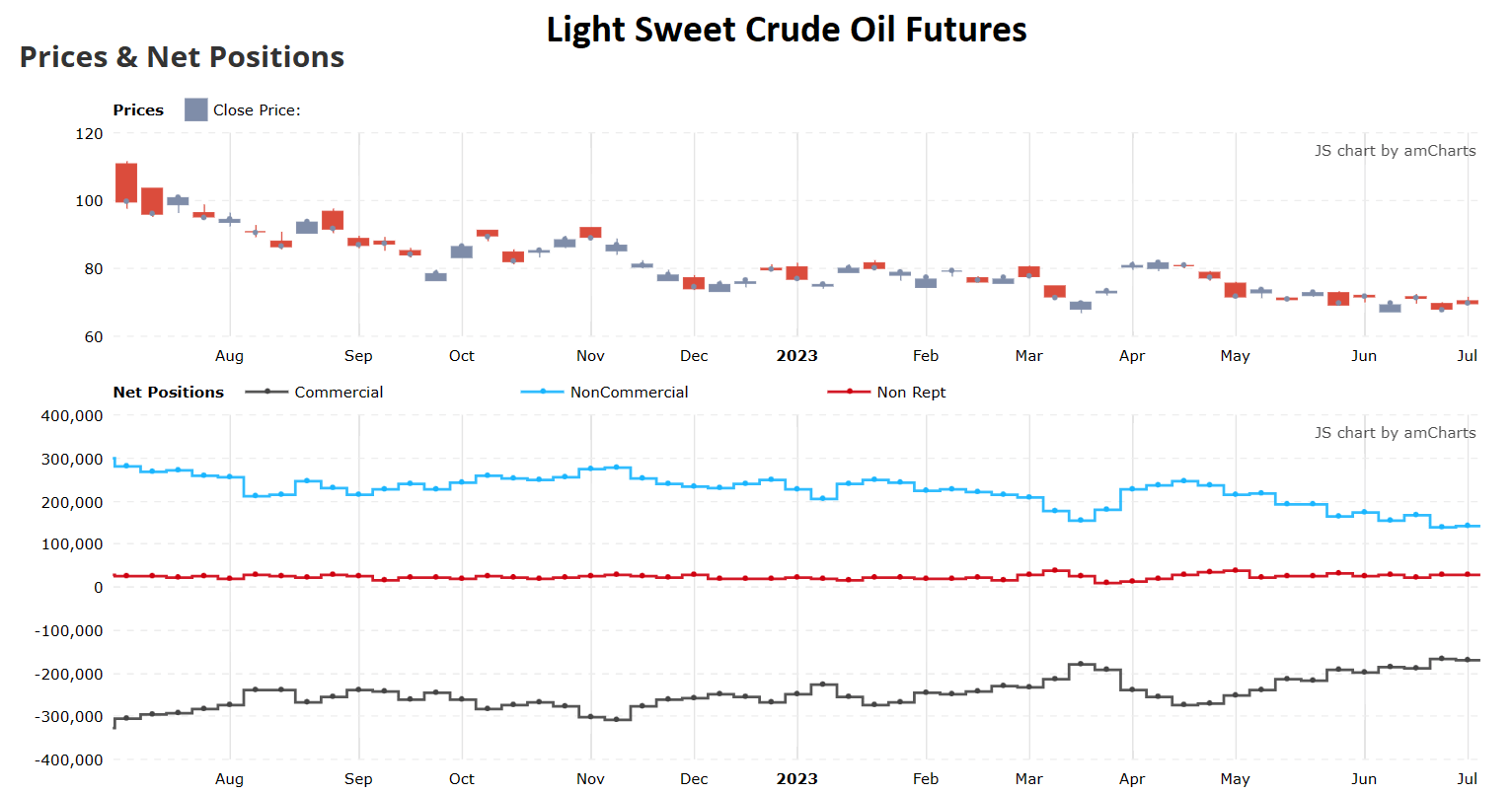

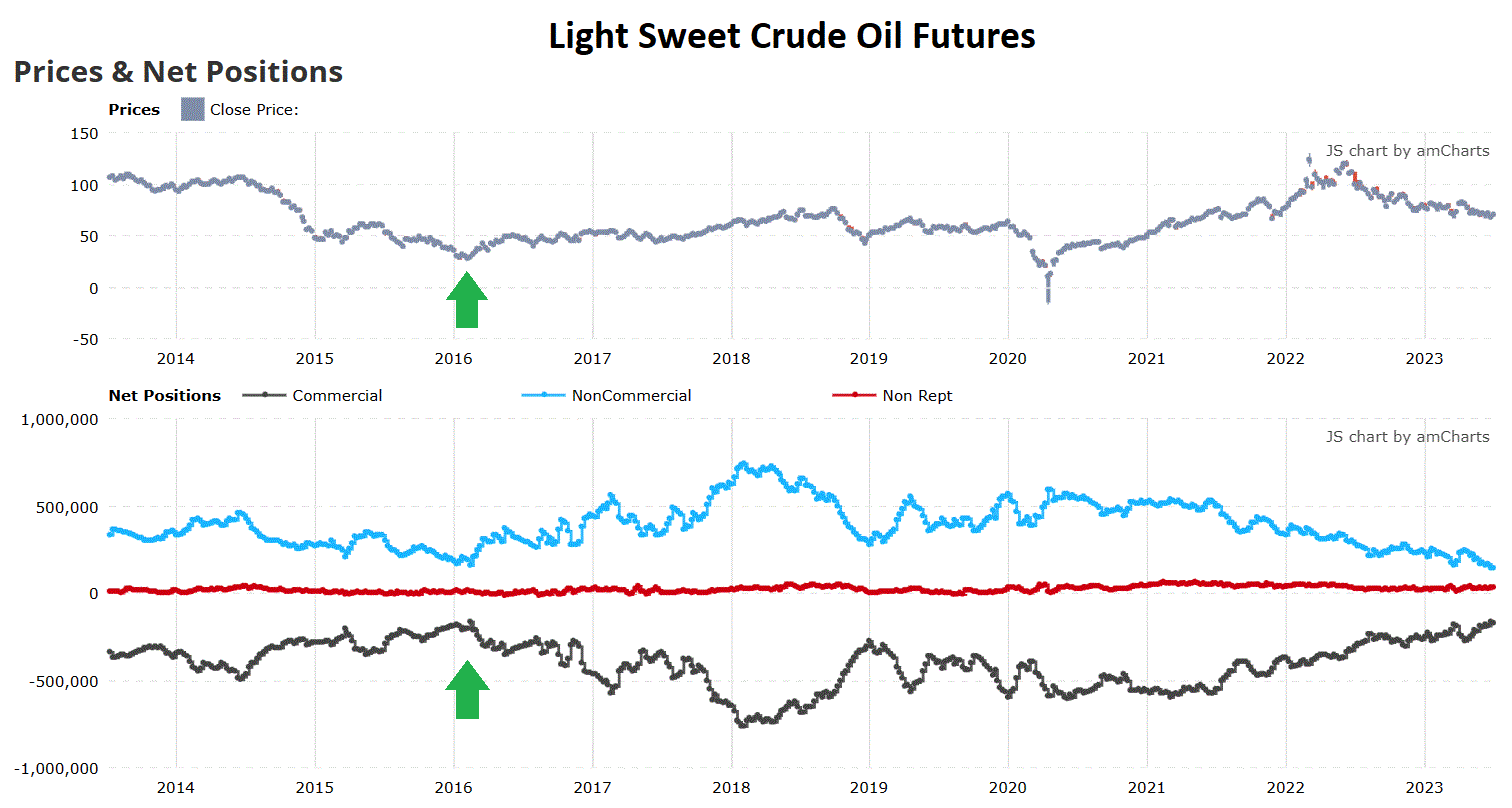

Outside of supply/demand balance worries into next year, another reason to like crude oil is futures market positioning may be the most bullish setup in 10 years right now. Commercial accounts (oil producers, exporters, refiners) have largely eliminated their net-short position, while hedge funds and retail investors own the lightest net-long stake in recent memory (on recession fears). For contrarian investors, the futures positioning story holds a slightly better long-term investment foundation than even the important early 2016 price bottom (highlighted with green arrows below).

Tradingster Website - NYMEX, July 3rd, 2023 COT Report - Light Sweet Crude Oil, 1 Year Tradingster Website - NYMEX, July 3rd, 2023 COT Report - Light Sweet Crude Oil, 10 Years

{kind=link}

{kind=link}

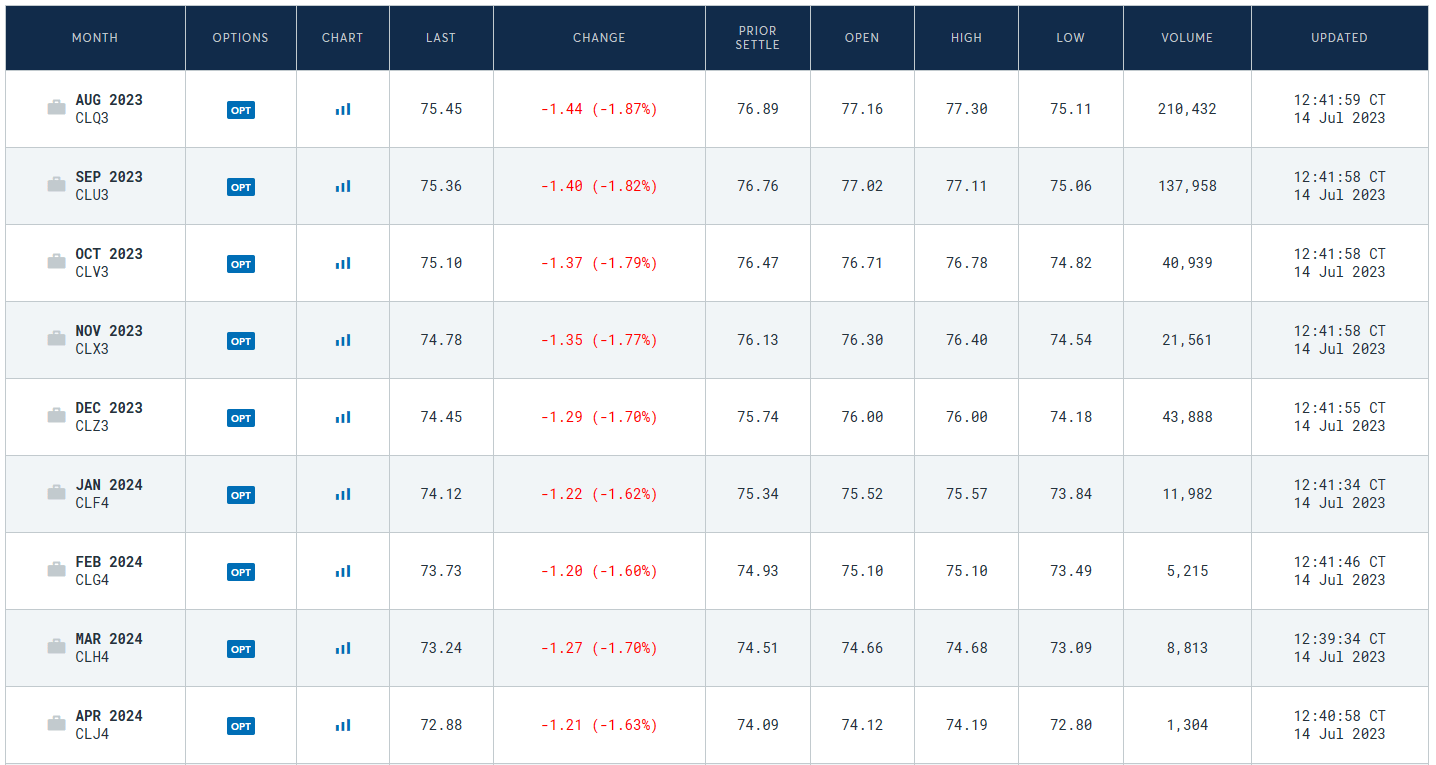

A third bullish reason to like USO specifically is the added kicker for price supported by the backwardation of futures. Backwardation is a financial condition where future contract prices are LOWER than current quotes. The positive effect for USO is any price rise from today will be amplified by owning crude oil futures at even lower cost than spot.

Crude Oil Futures Quotes - CME Group Website - July 14th, 2023

{kind=link}

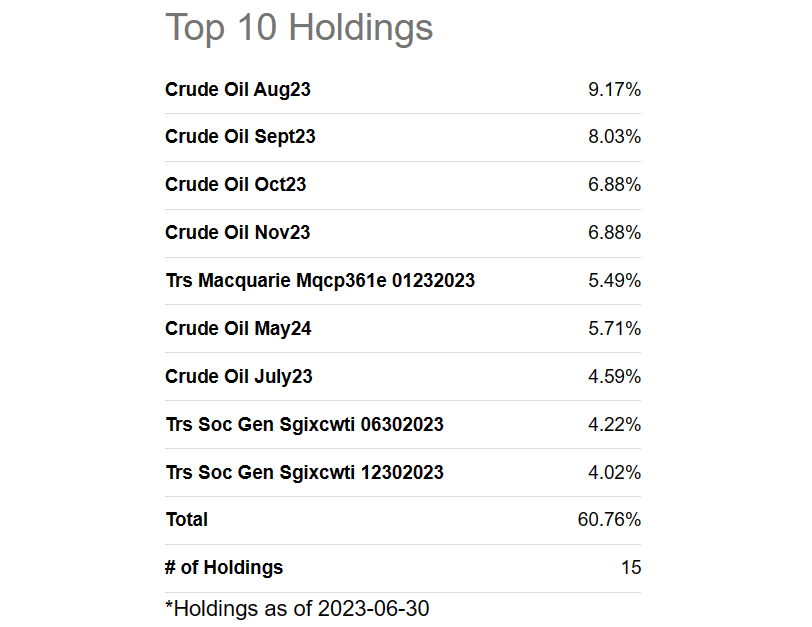

Seeking Alpha - USO, Top 10 Holdings, June 30th, 2023

{kind=link}

Backwardation has helped USO to "outperform" the price changes in related spot crude oil and rolling nearby futures for this critical commodity.

But that's not all. A new boost (fourth bullish reason) of late and going forward is large cash holdings are usually owned alongside leveraged forward contracts/futures in the trust. Where a few years ago no real interest was earned on cash, today's 5% savings rates for money-market assets held a year or less is very beneficial for trust owners (more than offsetting the 0.6% annual management expense).

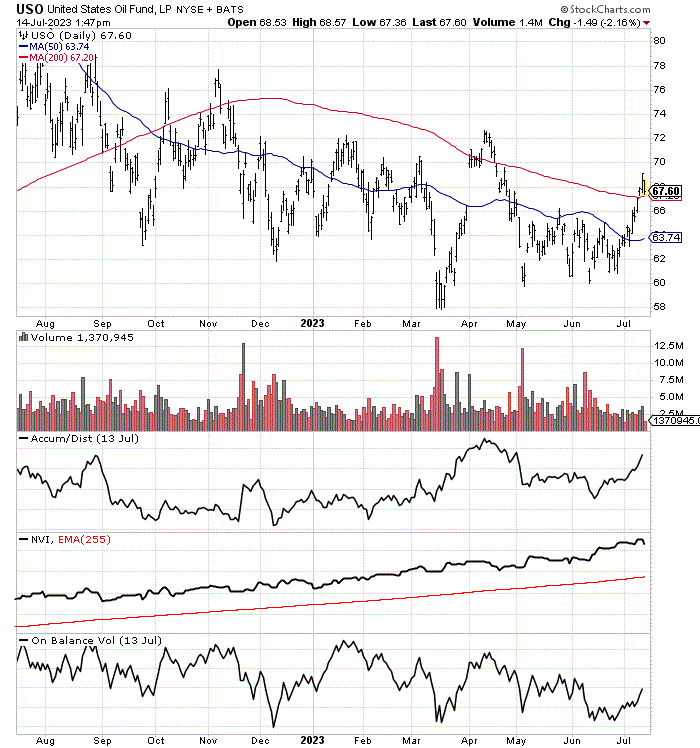

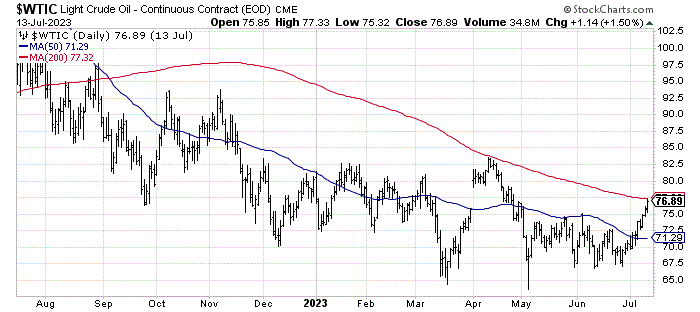

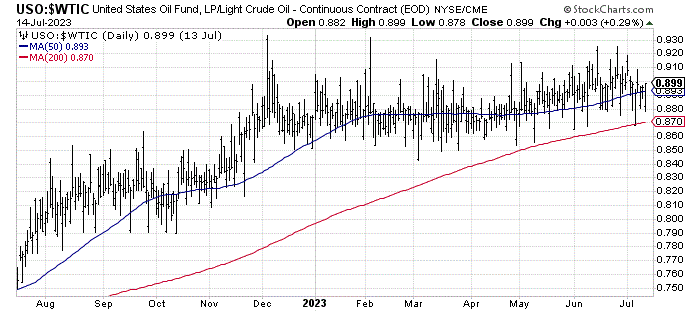

Below are charts of USO trading over the past year, alongside nearby crude oil futures changes, and a positive performance comparison of the two in favor of this trust product.

StockCharts.com - USO, 1 Year of Daily Price & Volume Changes StockCharts.com - Light Sweet Crude Oil Nearby Futures, 1 Year of Daily Price Changes StockCharts.com - USO vs. Light Sweet Crude Oil Futures, 1 Year of Relative Daily Price Changes

{kind=link}

{kind=link}

{kind=link}

Final Thoughts

I am planning to buy USO trust units next week, assuming price stays around $67. The risk-reward odds strongly favor gains, absent a recession, in my opinion. If we do find ourselves in a minor economic contraction soon, it remains a distinct possibility crude oil will still be able to rise, assuming Saudi Arabia and OPEC+ commit to substantial new production cuts. The outlier idea to own crude oil assets is we may see some sort of unexpected supply disruption, compound the rising likelihood of tightening supply/balance into next year (as part of a soft-landing scenario).

However, on Friday (July 14th), I did take advantage of the selloff in several smaller Texas oil/gas producers to buy some starter positions. If geopolitical trouble in the Middle East, Europe, and/or Asia are next, owning exploration & production companies far away in America makes sense to me.

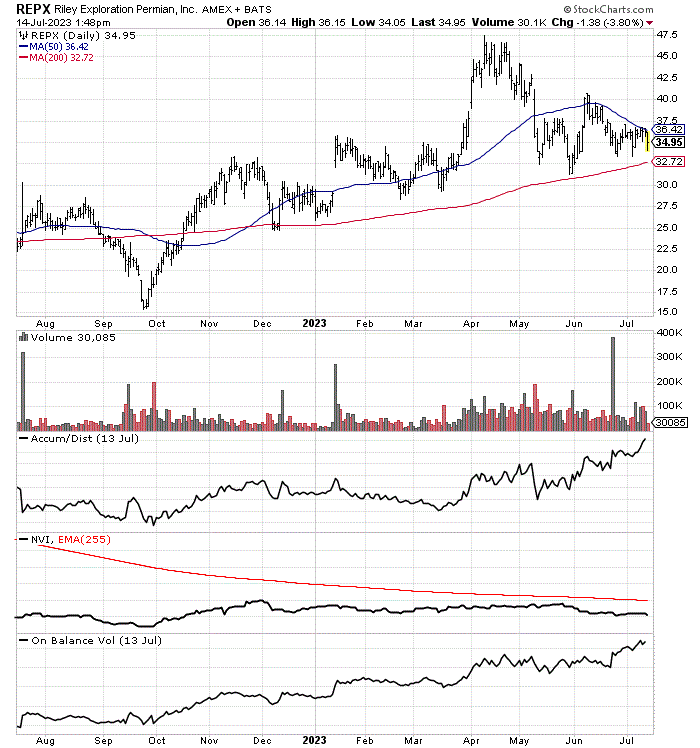

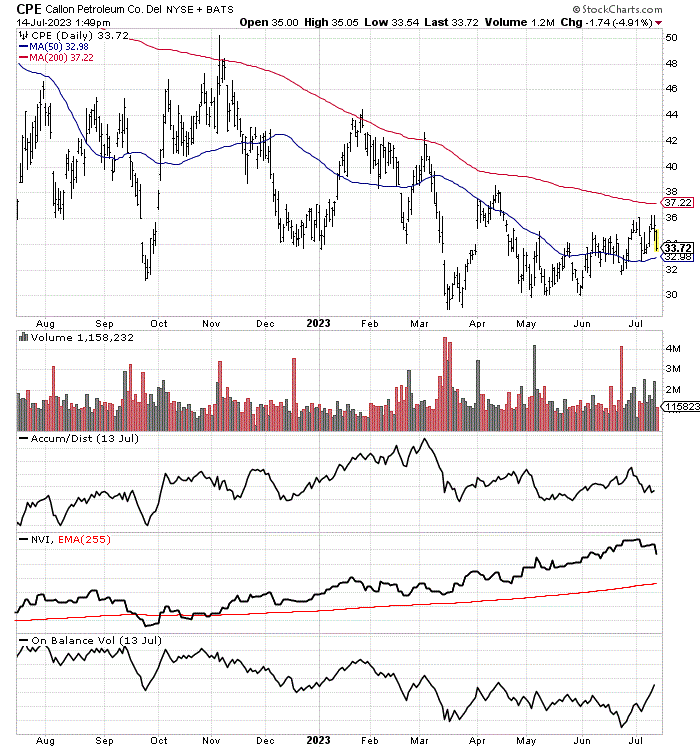

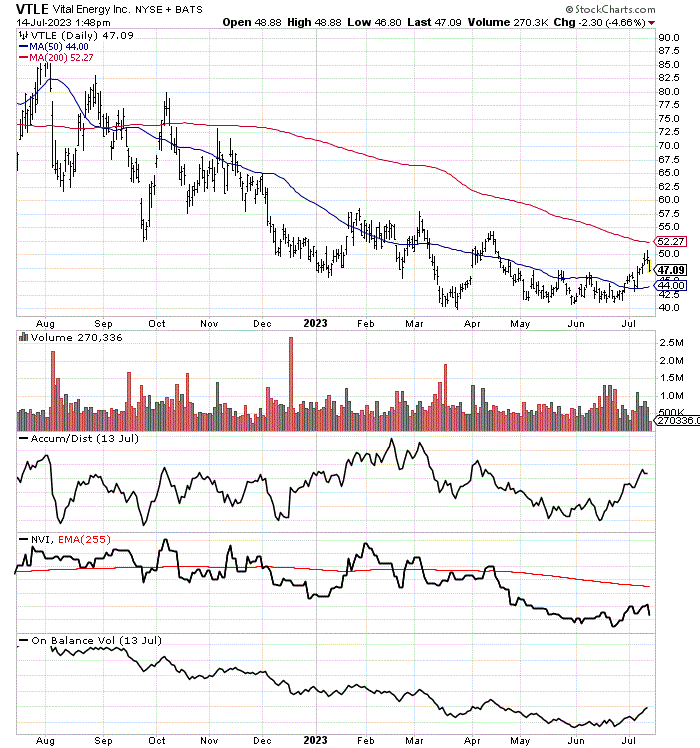

I repurchased a stake in Texas-asset Riley Exploration Permian ( REPX ), which I discussed in an article during March here , plus bought heavily-shorted peers Callon Petroleum ( CPE ) and Vital Energy ( VTLE ). Current price to analyst projections for earnings during 2024 are in the 2x to 5x multiple range, using today's "low" Wall Street expectations for crude oil and natural gas fluctuations over the next 12-18 months. Any material jump in crude oil (or natural gas) will only make them more valuable over time and cheaper to own today. At $100 crude oil and $4 natural gas (in America), all three should at least double in price.

StockCharts.com - Riley Petroleum, 1 Year of Daily Price & Volume Changes StockCharts.com - Callon Petroleum, 1 Year of Daily Price & Volume Changes StockCharts.com - Vital Energy, 1 Year of Daily Price & Volume Changes

{kind=link}

{kind=link}

{kind=link}

And, if you were wondering... Yes, I do go to YouTube and play the theme song from the 1980s hit television show " Dallas " on a loop, while I am buying Texas oil names ( link to my favorite clip ). This musical-investment process worked well for me in early 2020 during the historic pandemic bust when I purchased Callon, and about 10 other oil/gas names near their low points.

What's the downside risk? A severe global recession would not help out industrial commodity, cycle dependent USO or the vast majority of related petroleum producers. I am using a potential -50% price drop for USO and Riley as my worst-case "risk" scenario in a prolonged economic contraction, with even greater losses possible in Callon and Vital, as heavy debt loads would pose a thorny cash flow problem in a low-energy price environment.

Match this theoretical downside projection to potential best-case upside of +50% or better for USO to +200% for the small Texas producers, in terms of both price appreciation and total returns during a severe shortage development that launches crude oil above $100 a barrel to as high as $150. Just remember, these oil-related investments are cyclical in nature. You need to lock-in gains incrementally over time to derisk the roundtrip trade/investment idea.

Note: USO does send out a K-1 tax form each year to holders of the trust.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

For further details see:

USO: Crude Oil Spike Usually Appears At End Of Economic Cycle (Rating Upgrade)