CA - Utility Stocks Should Beat The Market: My 3 Top Buys

2023-09-06 08:00:00 ET

Summary

- Utilities are currently cheap compared to their historical average valuation (as well as compared to the broader market) and offer both growth potential and stock price upside.

- Federal legislation incentivizing decarbonization and electrification will fuel massive growth in the utility sector.

- I highlight my three favorite utilities and utility-adjacent stocks to buy during the current dip in utility stock prices.

Utilities are cheap.

They are cheap not just based on past performance but also based on future growth prospects .

If you like utility stocks and believe in their long-term growth potential, as I do, now is a great time to accumulate shares, in my opinion.

Below, I'll discuss my three favorite buys in the utilities space right now, only one of which is actually a pure-play regulated utility. But first, let's look at the big picture situation for utilities.

Solid Compounders On Sale

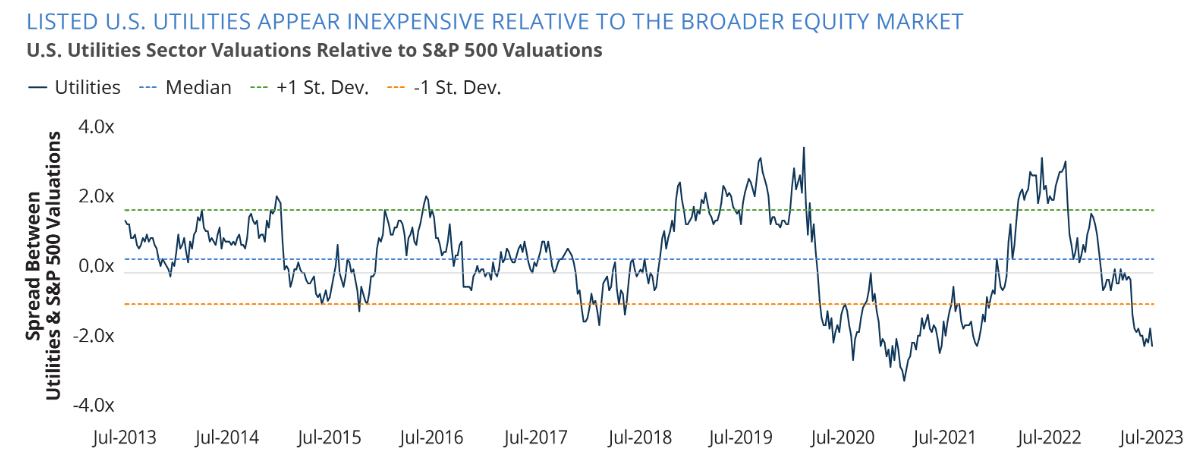

Utilities ( XLU ) have massively underperformed the broader stock market ( SPY ) over the last year, and that performance gap only seems to be widening.

The magnitude of this divergence is relatively rare. In fact, over the last decade, utilities have only been this cheap compared to the S&P 500 during the middle of the COVID-19 pandemic.

Currently, utility stock valuations are about two standard deviations below the broader market compared to their historical average.

{kind=link}

Although debt-heavy utilities do face headwinds from refinancing maturing loans at higher rates and issuing new debt at relatively high rates, perhaps the bigger hindrance to utility stocks today is the comparison with short-term bond or cash equivalent yields.

I hear the objection all the time. "Why would I buy a utility yielding 3-4% when I could invest in a safer CD yielding 5.5%?"

My answer can be summed up in one word: Growth .

A 5.5%-yielding CD does offer higher short-term income but zero income growth and zero upside. Plus, assuming inflation of 3%, your real total return from that CD is about 2.5%.

Utilities, on the other hand, offer growth of dividends (often more than sufficient to outpace inflation) plus huge stock price upside.

If interest rates decline in the next year, as they are widely expected to do, then your income from rolling over money from one CD to another (or from cash sitting in a money market account) will go down, while your dividend income and stock prices in utilities will go up.

Why not buy CDs today and wait until interest rates start going down to buy utilities? That strategy rests on your ability to time the market. Maybe it will work as you envision, or maybe you will miss your opportunity to buy utilities while they are cheap because you waited too long.

(Of course, this decision depends heavily on your time horizon, or when you need the money. If you need it next year, the CD is probably the better choice. If you don't need it for 5 or 10 years, I'd go with the utilities.)

The above thinking rests on the idea, though, that utilities will be able to generate significant growth going forward. Is that true? Aren't utilities just sleepy, low- or no-growth bond alternatives?

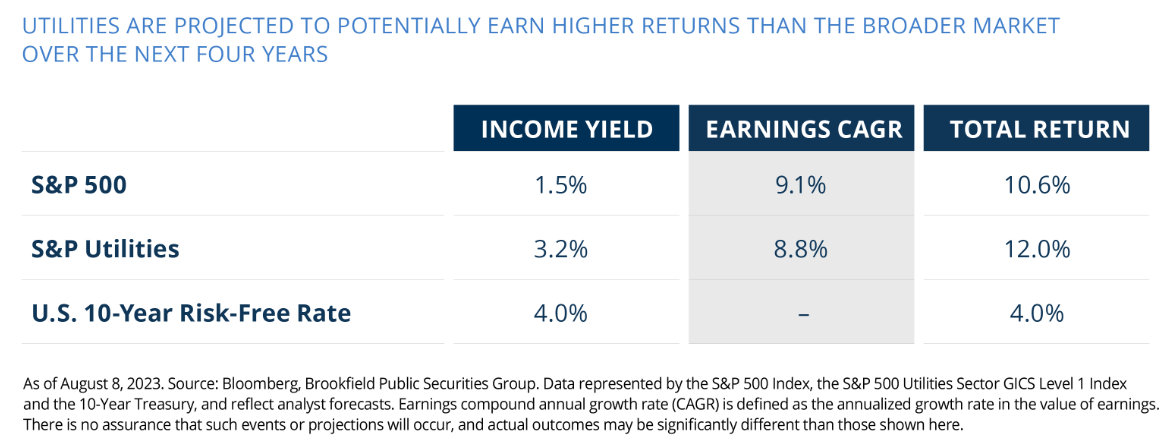

I don't think so. Primarily because federal legislation has massively incentivized the decarbonization of the utility sector, utility stocks actually sport strong growth prospects as well as market-beating total returns projections.

{kind=link}

Although the broader market is still expected to generate slightly stronger earnings growth than utilities, having more than double the dividend yield is enough to push utilities to a better projected total return performance going forward.

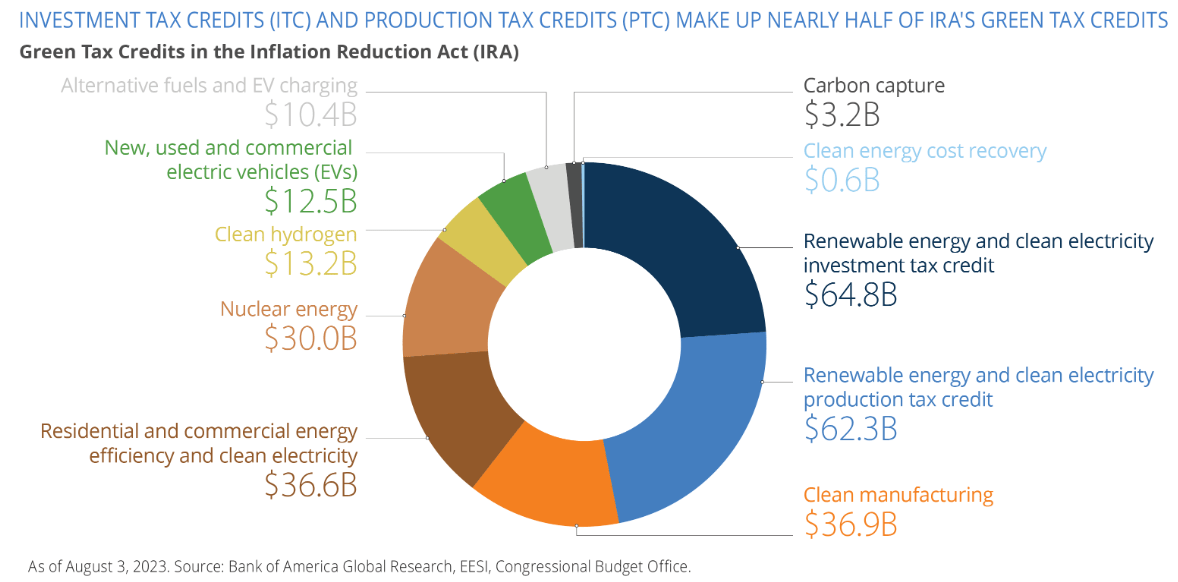

One might think that, without significant population growth or opportunities to expand utilities' rate bases, growth should be harder to come by in the future. But this ignores the huge investment opportunities in decarbonization and electrical distribution afforded by the "Inflation Reduction Act," which promises to dole out hundreds of billions of dollars in incentives.

{kind=link}

Utility companies are positioned to capture a huge share of these federal dollars through clean energy tax credits as well as increased electricity demand due to the electrification of the economy.

With more electric vehicles on the road, for example, there should be more demand for electrical power from the grid.

What makes the IRA such a significant tailwind for decarbonization and electrification is its staying power. Before the passage of the IRA, tax credits typically lasted only a few years at a time. Now, tax credits have not only been meaningfully expanded but are also scheduled to last decades.

{kind=link}

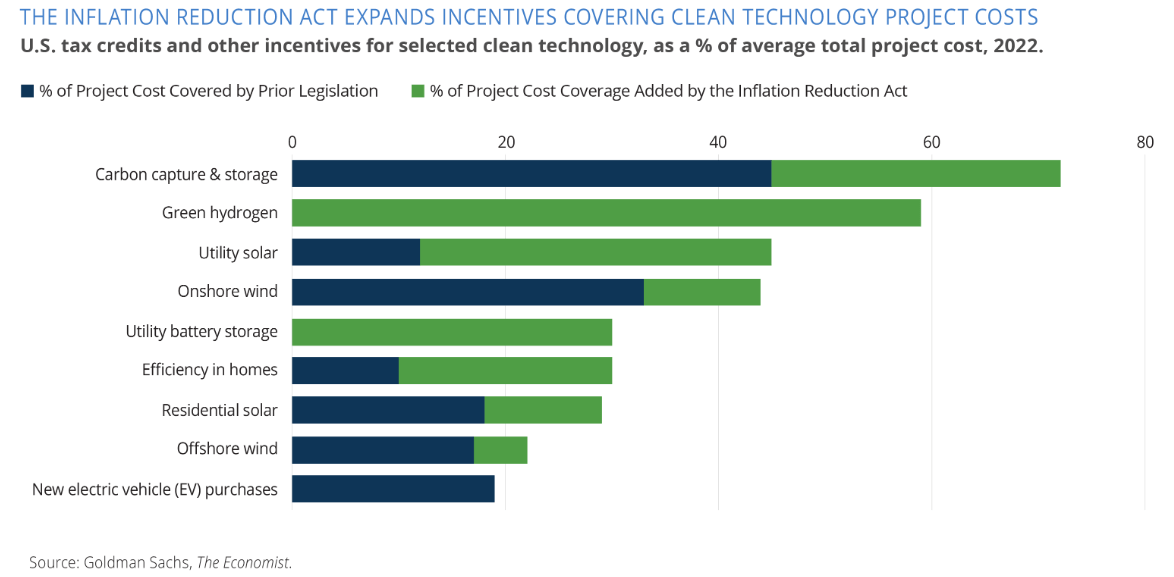

Over 70% of the project costs of carbon capture & storage is eligible for federal tax credits, as is almost 60% of green hydrogen projects. These two have higher incentives likely because the economics of these fledgling technologies is not good enough to make them profitable on their own yet.

Meanwhile, utility-scale solar, wind, and battery storage projects are eligible for federal tax credits equal to 30-45% of their total project costs.

This is a massive boon to the regulated utilities that develop and own these clean energy projects!

Let's look now at my three favorite ways to take advantage of utilities' cheapness.

1. American Electric Power ( AEP )

AEP is my favorite regulated utility, and it now yields about 4.4%. That is a full 100 basis points above its 5-year average dividend yield of 3.4%!

Plus, AEP now trades at a P/E ratio of about 13.5x, compared to 16x for the utilities sector more broadly. So, AEP is a cheap option within a cheap sector. Does it deserve to be so cheap?

I don't think so.

As I explained in a July article covering AEP's recent results, the Midwestern and Southern electric utility still expects long-term EPS growth to average 6-7% per year, which should fuel a continuation of its recent record of 6% annual dividend growth.

What gives management confidence in this growth target? A few things:

- Mostly favorable and stable regulatory environments

- Strong, investment grade credit ratings of BBB+, BBB, and Baa2

- A huge existing portfolio of transmission & distribution assets as well as ample transmission & distribution investment opportunities to expand its regulated rate base

In a world much more reliant on renewable power (wind and solar), which is typically produced significantly outside of population centers, electricity transmission assets (power lines) are highly valuable. AEP's expertise and market position in this area is a huge and underappreciated strength.

The combination of a 4.4% yield and 6-7% EPS growth should produce total returns of at least 10-11%. Add in about 35% upside to its historical valuation multiple and you've got the recipe for a powerhouse investment.

2. Brookfield Infrastructure ( BIP , BIPC )

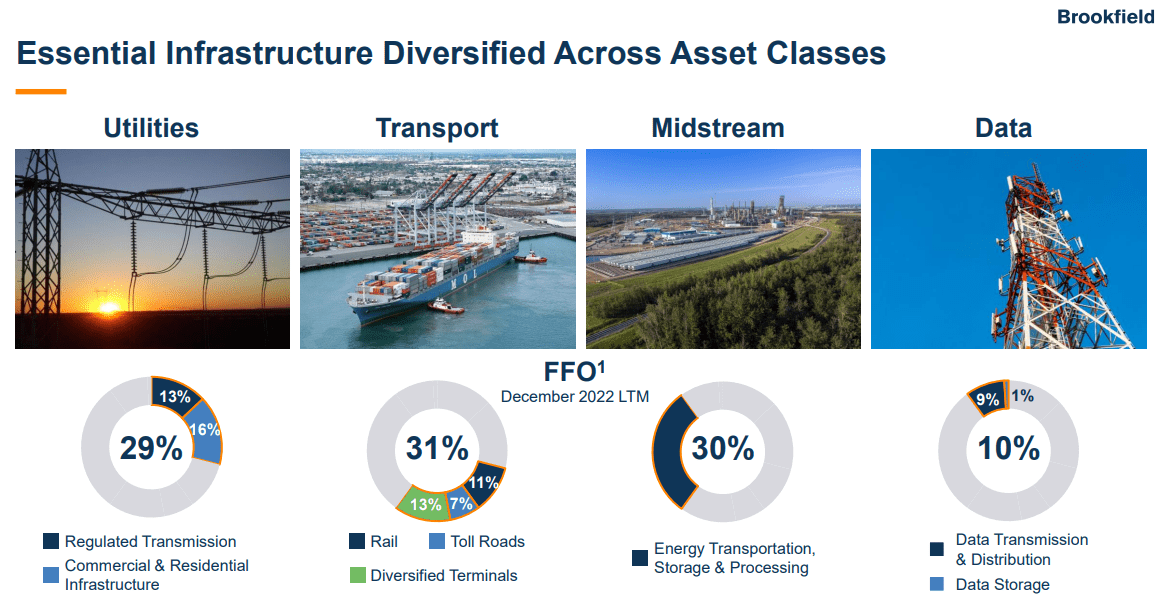

BIP isn't a pure-play utility, but it owns utilities. It is a globally diversified owner/operator of various infrastructure assets, with its portfolio split roughly evenly between regulated and unregulated utility assets (~30% of cash flow); transportation assets such as ports, railroads, and toll roads (~30%); and midstream energy (~30%). The remaining 10% of cash flows come from data centers and telecommunications infrastructure.

{kind=link}

Obviously, with such a portfolio, BIP is a hybrid between multiple types of businesses: utilities, midstream energy companies, telecom REITs, and data center REITs.

I love BIP because its portfolio boasts 90% of its cash flows deriving from regulated or contractually fixed sources, rendering strikingly stable results over time. Plus, over 80% of its cash flows are tied in some way to inflation, offering protection during inflationary environments.

Its fee contracts offer a weighted average duration of about 11 years, compared to its weighted average debt maturity of about 7 years. And speaking of debt, BIP is well-positioned on the balance sheet side with 90%+ fixed-rate loans and investment grade credit ratings of BBB+.

BIP has the unique ability to use its stable cash flows from its traditional, "boring" business segments like utilities, transportation, and midstream energy to invest heavily in "new economy" technology infrastructure such as data centers and fiber lines. This is what makes its data segment BIP's fastest growing area of investment.

For example, BIP owns over 250 data centers, which should greatly benefit from the explosion of data expected from the artificial intelligence megatrend.

This is one of the primary channels by which management expects to grow FFO per share by at least 10% per year going forward. And this growth should allow BIP to continue hitting its target of 5-9% annual dividend growth. Its historical average dividend growth rate from 2012 through 2022 is 9%.

3. Reaves Utility Income Trust ( UTG )

Leveraged closed-end funds ("CEFs") like UTG have gotten pummeled over the last year by rising interest rates. But I would argue that it is perhaps the best managed and well-positioned for total return outperformance among peers.

UTG hasn't performed as well over the last year as its unleveraged peer, BlackRock Utilities, Infrastructure & Power Opportunities Trust ( BUI ), but it has slightly outperformed its leveraged peer Cohen & Steers Infrastructure Fund ( UTF ):

While UTG is about 20% leveraged (debt to AUM), UTF is about 30% leveraged.

UTG's portfolio of underlying holdings is made up of about 2/3rds utilities as well as some communications companies, REITs, and a few others sprinkled in.

I explained the case for UTG in greater detail in my article, " UTG: Top-Notch Infrastructure CEF To Benefit From Lower Interest Rates ."

Given UTG's ~8.8% dividend yield, which I believe is sustainable even amid high interest rates, plus 30-40% upside if and when interest rates decline, UTG should easily turn in double-digit total returns from here.

If you believe, as I do in both the lower-interest-rates-within-a-year narrative and the utilities-have-better-growth-prospects-than-people-think narrative, UTG looks like a good high-yielding pick.

Bottom Line

These aren't your grandfather's utility stocks. They've got solid growth prospects plus significant upside if and when interest rates decline. Plus, they're recession-resistant.

If the economy does dip into a recession sometime soon, and if interest rates come down following that recession, then I believe each of these three utilities or utility-adjacent stocks should outperform the market going forward.

For further details see:

Utility Stocks Should Beat The Market: My 3 Top Buys