VFC - V.F. Corp.: A Closer Look At Yet Another Dividend Cut

2023-10-31 09:35:58 ET

Summary

- Consumer sentiment remains subdued, with only the top third of incomes driving any improvement.

- V.F. Corp, a leading apparel manufacturer, has cut its dividend by 70% and is facing significant challenges in the market.

- While there is potential for a recovery, the risks and uncertainties make investing in VFC stock a risky proposition.

Introduction

One of the biggest macro topics this year is consumer health. It seems that many investors believe that the consumer is resilient. They may be right, at least when it comes to comments from the world's largest credit card companies, Mastercard (MA) and Visa (V).

Mastercard CEO: "On your question around how we see Q4 shaping up, it's actually very much in line with what I shared which is our base case scenario continues to be one of where the consumer remains resilient ."

Visa CEO: "Throughout the year, we have seen resilient consumer spending , ongoing recovery of cross-border travel spend versus 2019 and continued growth across our new flows and value added services businesses"

My opinion is different. I believe the consumer is in a very bad spot. The only reason why the consumer may seem strong is because higher-income and wealthier consumers are still spending.

The bottom 80% of households have run out of excess savings this year.

Bloomberg

Comments from credit card companies make sense, as I believe that many consumers are forced to use credit for basic goods, which makes it look like spending is in a great place.

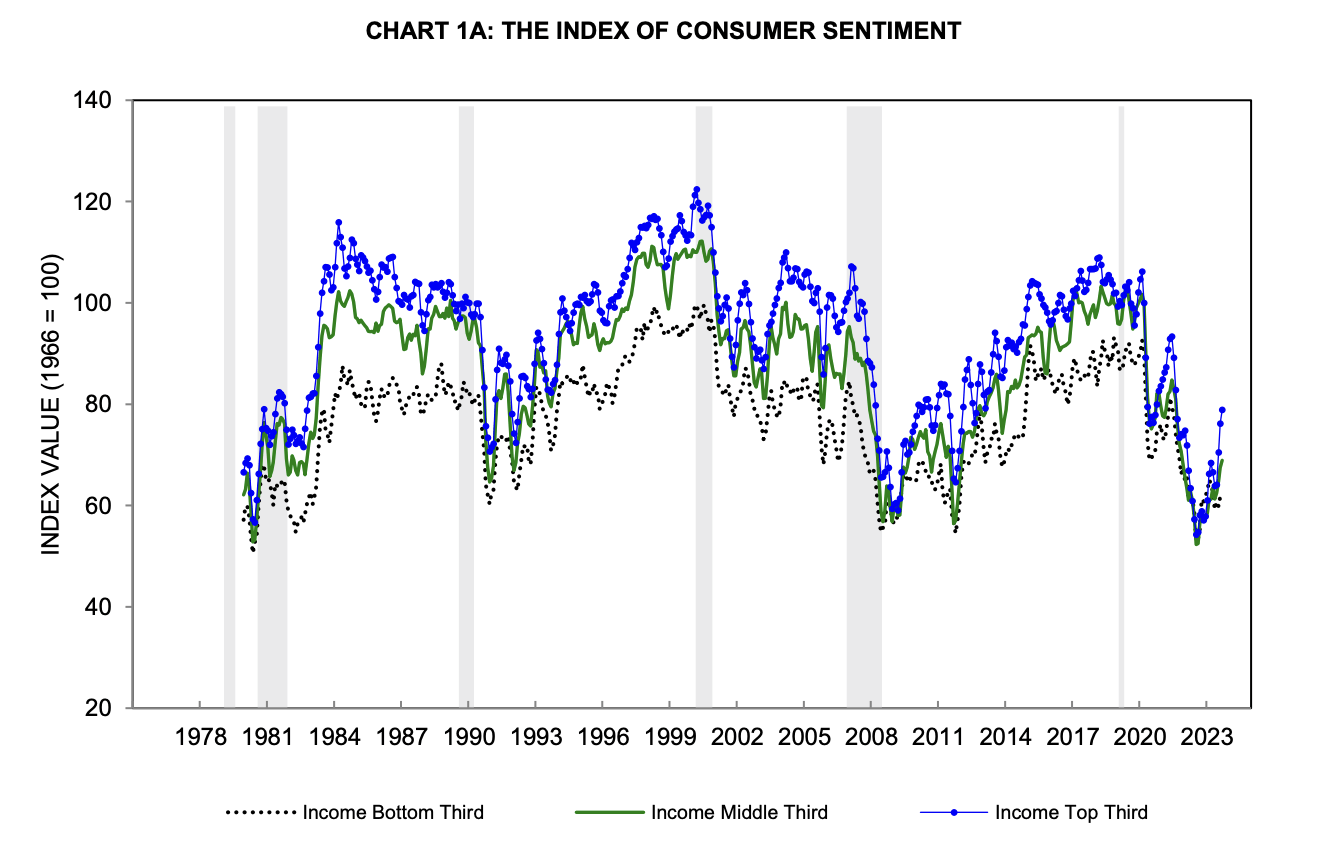

Looking at consumer sentiment, we see two things:

- Although consumer sentiment has rebounded somewhat, it's still at subdued levels.

- Consumer sentiment has been driven by the top-third of incomes. The bottom two-thirds are stuck close to the Great Financial Crisis bottom levels.

{kind=link}

The reason I'm bringing this up is V.F. Corporation ( VFC ) , one of the world's leading apparel manufacturers, which just cut its dividend by 70%. That's the second cut this year.

VF Corp is in a very tough spot. While it did well during the pandemic, it entered a massive downtrend, sending shares down from $90 in 2021 to currently less than $17.

The company is dealing with post-pandemic inventory issues and a horrible market environment.

Now, it's looking to improve its business. Pressured by activist investors , the company is working on a global initiative to streamline its business, improve its brands, reduce costs, and strengthen its balance sheet.

While I have to say that I think VFC looks like a total dumpster fire now, I believe the company is still one of the best global apparel manufacturers, and I'm hopeful it will trade at a much higher market cap a few years from now.

The question is if we want to bet on that.

So, let's get to it!

VFC's 2Q24 Was Tough

As one can imagine by looking at its stock price or consumer sentiment, VFC experienced weak overall performance in the second quarter of its 2024 fiscal year.

Total revenue declined by 2%. The revenue decline was 4% in constant currency terms.

Interestingly enough, contraction only came from the company's Americas operations, which account for roughly half of its sales. The other two regions saw growth.

- Americas : Revenue was down 11% in the quarter, primarily due to challenges in the wholesale segment, particularly for Vans. However, excluding Vans, direct-to-consumer ("DTC") was up 5% in the Americas, with positive performances from other brands.

- EMEA (Europe, Middle East, and Africa) : EMEA returned to growth, up 6%, achieving its first $1 billion quarter in the company's history, driven by wholesale and DTC growth.

- APAC (Asia-Pacific) : Revenue in the APAC region was up 6%, led by Greater China's 14% growth, driven by strong brick-and-mortar store sales.

{kind=link}

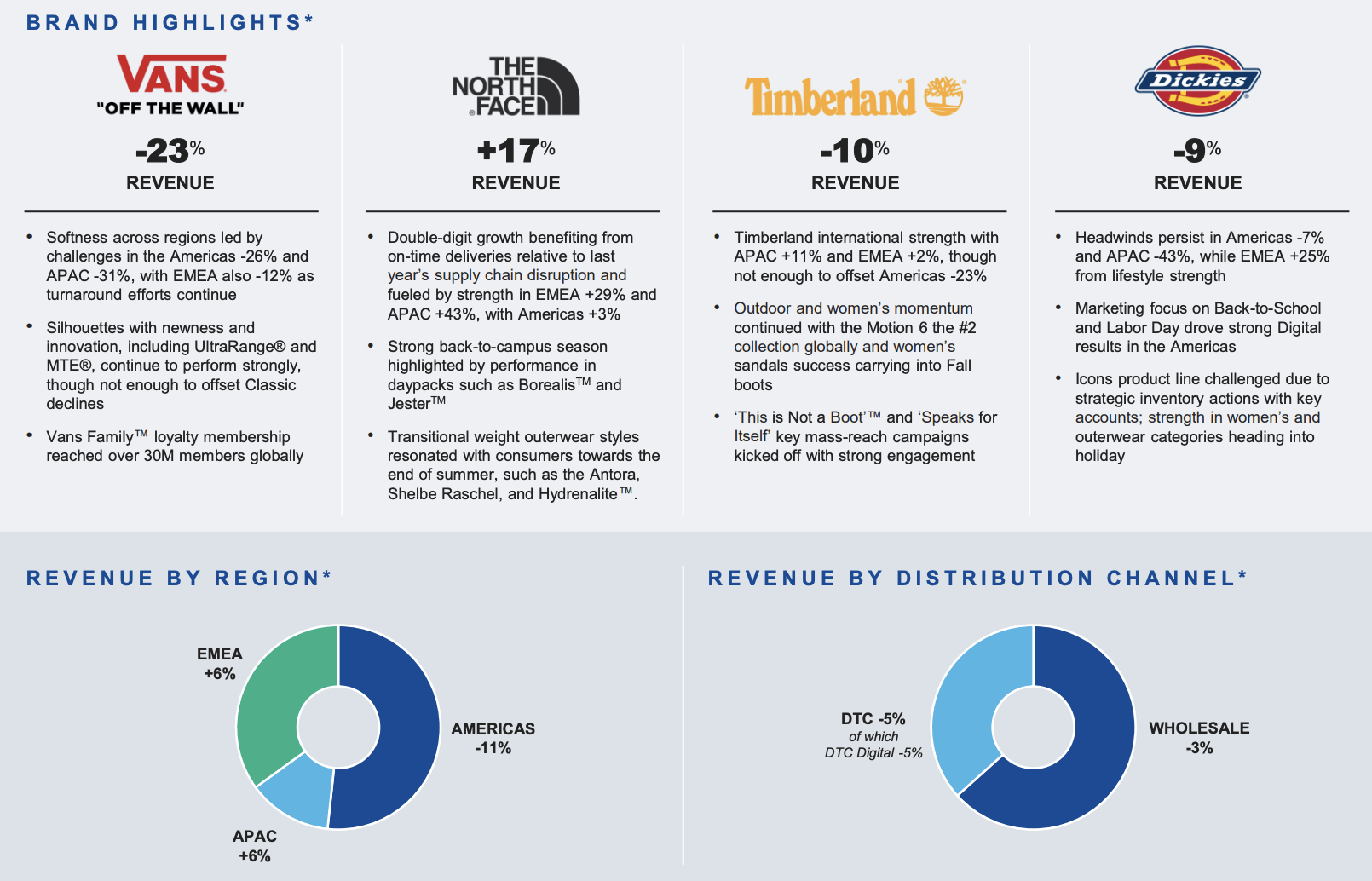

Also, as the overview above shows, not all segments were performing poorly.

- The North Face : This brand had a strong quarter, with revenue up 17%. DTC performance was up 12%, and the brand performed well globally, with strong performances in bags and packs.

- Vans : Vans had a disappointing quarter, with revenue down 23%. Slow sell-through rates and challenges in both wholesale and DTC were the key reasons for this decline.

- Timberland : Q2 revenue declined 10% due to softness in America's wholesale. However, outdoor and women's categories performed well.

- Dickies : Revenue declined 9% due to pressure from the value-conscious consumer in the core work business.

- Supreme : Supreme had double-digit revenue growth in the quarter and saw success with its new store in Seoul.

{kind=link}

Adding to that, margins continued to be a problem.

Gross margins were at 51.3%, down 20 basis points year-over-year, primarily due to product cost and FX headwinds. For what it's worth, the gross margin would have been up 30 basis points when excluding additional inventory reserves in Dickies.

Operating margin was 12% in the quarter, down 30 basis points year-over-year, reflecting a small gross margin decline and slight SG&A deleverage.

So, What's Next?

I left out a number of important data in my 2Q24 review.

Some issues need to be discussed in the context of the company's restructuring plans.

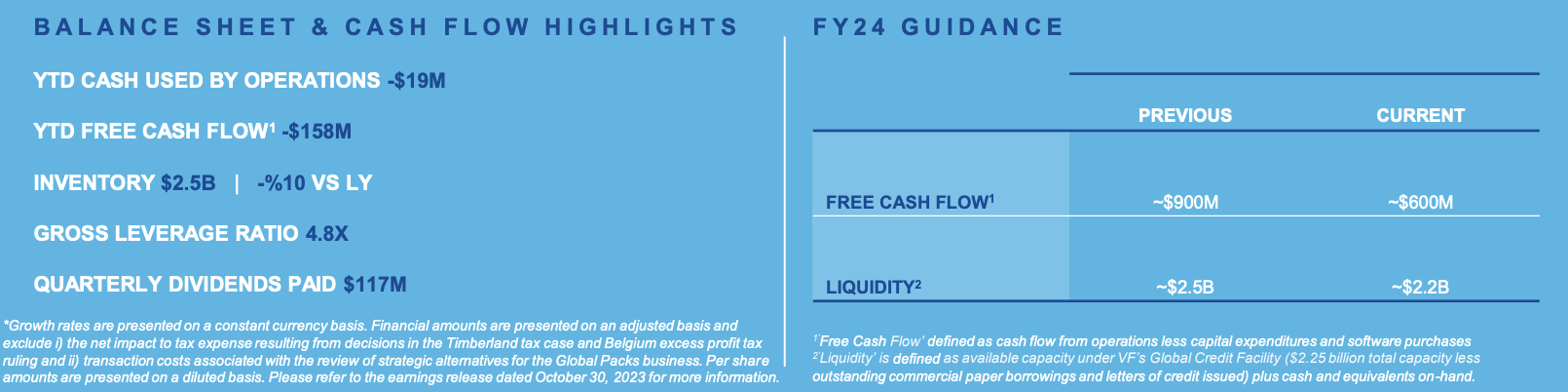

For example, with regard to inventories, the company has been actively working to reduce its inventory levels. They initially set a goal of reducing inventory by at least 10%, but the new guidance suggests a more moderate decrease in the range of mid to high single digits, which isn't great news.

This adjustment is primarily attributed to the challenges faced by the Vans brand and the U.S. wholesale market.

Generally speaking, reducing inventory when demand is weakening is a strategic move to manage working capital and align supply with demand.

Managing inventories effectively can help the company improve its cash flow and financial health.

Speaking of financial health, VFC anticipates having approximately $2.2 billion in liquidity by the end of the fiscal year. Deleveraging the balance sheet is the top financial priority.

During its earnings call , the company mentioned that it plans to end the year with slightly higher leverage compared to the previous year due to expected impacts on revenue and profit in the second half of the year.

Analysts believe the company is able to lower net debt to $5.4 billion this year, lowering its leverage ratio to 4.3x EBITDA. The company has a BBB credit rating, which is an investment grade rating.

{kind=link}

Furthermore, the company is committed to addressing both the numerator and the denominator in its financial equation. This involves a $300 million annualized cost reduction through the Reinvent program and a reduction in the dividend, resulting in approximately $325 million in cash savings on an annualized basis.

As a result, the company cut its dividend by 70% to $0.09 per share per quarter. This translates to a yield of 2%.

Speaking of the dividend cut and related cost reductions, this is a part of the company's restructuring plan.

During its earnings call, the company emphasized that its challenges are largely the result of its own actions, underscoring that the company has the potential to overcome them.

While I would argue that VFC would be doing much better if the economy were stronger, I'm obviously not objecting to its four key areas of potential improvement.

- Global Commercial Organization: VF is establishing a global commercial organization, including an Americas region, to facilitate the fast transfer of best practices and execution excellence.

- Brand Presence and Product Innovation: The new operating model will enhance brand presence and the ability to get closer to customers, create consistent product pipelines, and build excitement around brands, especially Vans.

- Cost Optimization: VF aims to reduce costs by $300 million across the business, investing a portion of savings in brand-building and product innovation while improving profitability.

- Balance Sheet Strength: Reducing debt levels and deleveraging are the top financial priorities, with a commitment to maximizing shareholder value. Acquisitions will be on hold until debt levels are reduced, which makes sense, as I believe the company has the right product portfolio for success. It just needs to improve its existing assets.

As a result of so much uncertainty, the company announced that it would not provide revenue and profit guidance for the remainder of the year. The focus will be on updating free cash flow and projected liquidity levels at year-end.

In the guidance chart above, we can see that both these numbers were downgraded.

The Risk/Reward

What a mess. Sales were down, the dividend was cut by 70%, guidance was cut, and all eyes are now on internal business improvements.

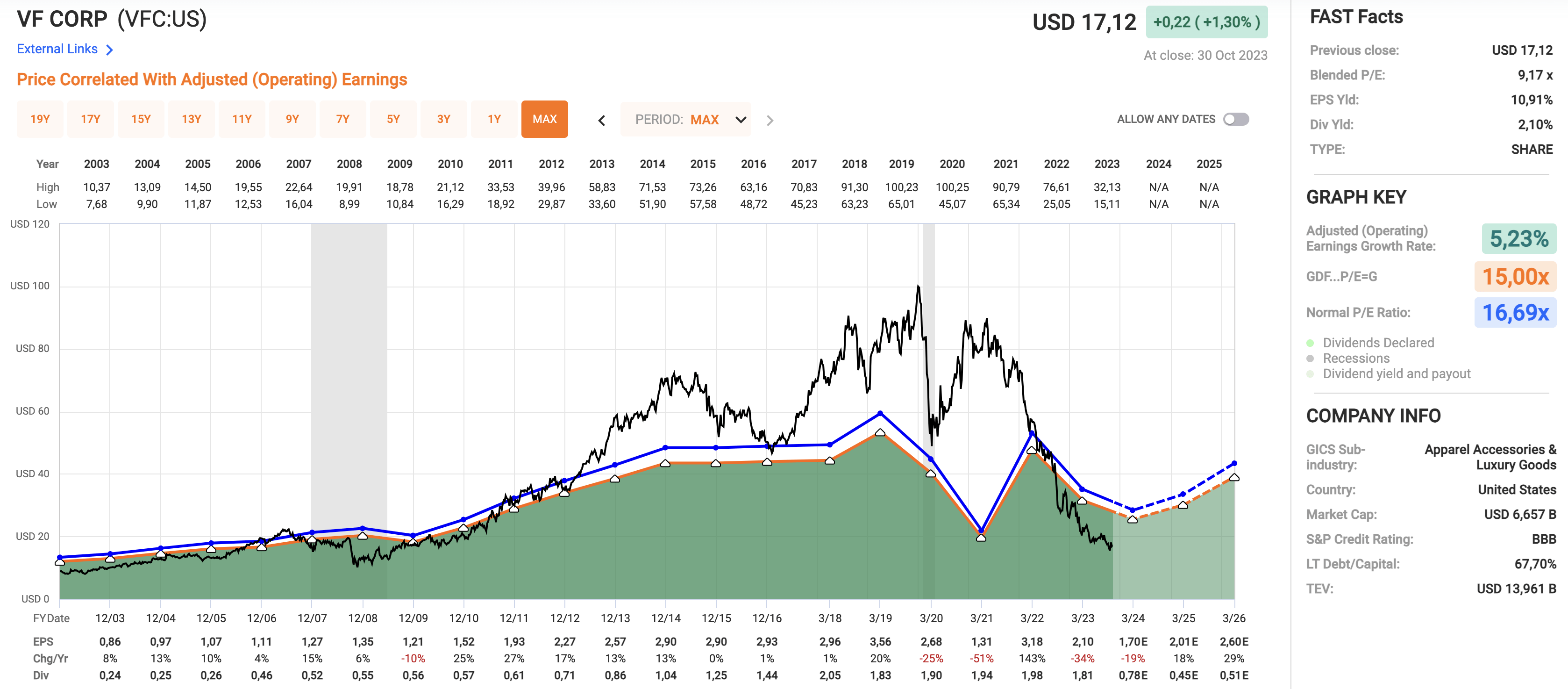

Despite all of the bad news, the risk/reward isn't that bad in my view. The company is now trading at a blended P/E ratio of 9.2x. This is well below the two-decade normal P/E ratio of 16.7x.

{kind=link}

This year, analysts expect EPS to decline by 34%, followed by another decline of 19% in 2024.

In 2025, the company is expected to see an upswing, with an expected EPS growth rate of 29%.

While these numbers are subject to change, I do believe that the market has priced in a lot of weakness, especially because VFC is down another 7% after earnings (pre-market).

Based on a normalized valuation and EPS growth expectations, the company has a (theoretical) fair value of roughly $42 per share. That's almost twice the current consensus price target of $22.

Although there's a case to be made that the stock could more than double in the next three to four years (maybe earlier, depending on the economy), we also need to be aware of the significant risks the company is dealing with.

If it is unable to execute its plans or if it encounters even more economic weakness, it could fall even further.

On top of that, I have to say that I'm not a fan of owning cyclical consumer stocks, at least not so far down the supply chain.

In other words, in light of severe uncertainty, I'm giving the stock a Neutral rating. There's potential for a recovery, but I'm not buying it, nor am I comfortable getting investors into this risky investment.

When it comes to betting on a potential consumer recovery, I prefer intermodal railroads like Norfolk Southern ( NSC ), home improvement stores like Home Depot ( HD ), or self-storage companies like Extra Space Storage ( EXR ). All of these stocks come with a history of consistent dividend growth.

Takeaway

Consumer sentiment, though showing some signs of improvement, remains subdued, with only the top third of incomes driving this uptick. The rest are still stuck at Great Financial Crisis levels.

V.F. Corp, a once-thriving apparel manufacturer, is a prime example of the harsh reality. They've cut their dividend by a staggering 70%, and their stock price has plummeted. While they're attempting a turnaround, it's not an easy road ahead.

Despite the gloom, there's a glimmer of hope. V.F. Corp. could potentially bounce back, but it's a gamble I'm not willing to take. I prefer investments with a more solid foundation and consistent dividend growth.

For further details see:

V.F. Corp.: A Closer Look At Yet Another Dividend Cut