VFC - V.F. Corp: Potential For A Brand-Driven Renaissance

2023-04-23 07:04:36 ET

Summary

- V.F. Corporation designs, produces, and distributes lifestyle apparel and footwear. It owns leading brands such as Supreme, North Face, Vans, and Dickies.

- China opening up should present natural tailwinds to the business, which has weighed on the company's performance in the last year.

- Management has struggled to respond to changing trends and successfully market its brands, failing to consistently achieve growth.

- The company's financial performance has been marred with problems, but its profitability profile does have the opportunity to be attractive relative to its peers.

- Based on VFC's current valuation, we see an upside of 25-36%. Analysts are equally as bullish with a target upside of 29%.

Investment thesis

With the company's stock price trending down, we are seemingly faced with two realities. Either, investors face catching a falling knife or the stock has been oversold and now presents an attractive proposition for investors. We will seek to assess this by considering what is wrong with the brand and what management is doing to rectify this. The most important factor will be looking at how the company's financials currently shape up and how the short term is looking, as this will dictate if the stock will continue to trend down.

Company description

V.F. Corporation ( VFC ) designs, produces, and distributes lifestyle apparel, footwear, and related products for men, women, and children under various brand names. It operates in three segments: Outdoor, Active, and Work, and offers a wide range of products in these segments. Brands within their umbrella include North Face, Timberland, Smartwool, Icebreaker, Altra, Vans, Supreme, Napapijri, Dickies, and Timberland.

VFC is one of the largest Apparel companies in the world, ranking 10th by market cap according to Seeking Alpha.

Share price:

VFC's share price has had a tumultuous 10 years, with the company making seemingly impressive gains before COVID-19, with things going downhill since then. The initial period was driven by improving financial performance but cracks began to grow. The lockdown and post-lockdown period displayed what are inherent issues in the business.

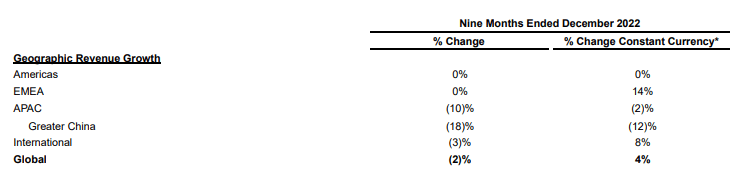

China

One of the major factors driving demand in the Apparel industry is China. The Chinese are major players in the fashion industry, representing an outsized level of demand. The country has been struggling with COVID-19, owing to its stubbornness in maintaining a zero-COVID approach. This has now been lifted and following a spike in cases, the country may be finally seeing the end of the virus. This should mean demand domestically and internationally picks up from their citizens, as travel and employment ramp up toward a normal level again. VFC has struggled with the loss of Chinese sales, experiencing an 18% decline in the L9M. There is no certainty that this will all return but there will be a natural uptick due to the lack of lockdowns.

Sales by Geography (VFC)

{kind=link}

The portfolio

VFC own some of the leading brands in their segment. Supreme is arguably the king of "Hype" fashion, remaining one of the prominent streetwear brands. Vans is a staple in the skater/casual segment, and North Face and Napapijri have successfully won over customers in the outdoor and casual segment. Further, Dickies is a classic choice for workwear, with the other brands listed here generally having good market awareness.

Key VFC brands (VFC)

I am a big fan of fashion and have followed trends for many years. These brands that VFC owns are genuinely leading in the market and have the legs to continue growth. The issue I see is that the Management has failed to sell the relatability of the brands. There is no passion communicated. Now more than ever, consumers are looking for brands that have value and that they can relate to and I feel like this is lacking here. Browsing through Dickies website, I see nothing but massive discounts plastered all over the website, it looks more like a fast-fashion retailer than an actual brand. Many in the streetwear industry, for example, consider Supreme to be "corporate" now and not "about the culture". You can see this in the hype, it's fallen off a cliff. I remember the days not too long ago when every product on the Supreme website would sell out within 30 minutes of landing on the page. Having just visited, the majority of the products are still listed and in the coveted Small size. The following, a neutral-colored product that clearly says Supreme, would be sold in less than a heartbeat.

{kind=link}

The good news for VFC is that fashion is usually cyclical and those brands that fall out of favor have a good chance of returning. Further, management has acknowledged that the key lies in their execution, specifically calling out Vans as a brand they need to refocus on. This does not happen overnight or without the chance of failure.

Changing trends

VFC is experiencing changing trends as consumers seek more Outdoor products and less Workwear. This makes sense as the working-from-home trend has encouraged people to seek more casual wear as they are in the office. Further, the company has done a good job of selling NF and Napapijiri as lifestyle brands, beyond just Outerwear. This places pressure on Management to better position its Workwear brands to respond to this. A company that has done a fantastic job of this is The Gap ( GPS ) with Banana Republic. As the following illustrates, demand for Workwear is consistently declining.

L9M Sales (VFC) L3M Jun Sales (VFC)

{kind=link}

{kind=link}

Again, this is not a fundamental issue with the business and requires investment in its marketing and development teams to better position its brands.

Financials

VFC Financials (Seeking Alpha / Tikr Terminal)

VFC has achieved zero growth in revenue in the last 10 years, experiencing a decline from FY13 to FY20. The company has actually done well to re-invigorate growth in the last 3 periods, returning to >$11.5BN for the first time since FY14. A large part of this has been driven by the consumer binge post-COVID but also reflects the strength of their underlying brands, as consumers have chosen them among many.

Unlike revenue, however, the company has achieved margin expansion across the historical period. This is important to see as stagnation is something many large companies experience but it can be efficiently navigated if the company can improve profitability as they figure out how to kickstart growth.

The next big issue we see is below the GP line. EBITDA margin has trended down, with the post-COVID bump not contributing to any improvement. The company looks to have normalized at the 14-16% level. Management has taken steps to cut costs, including 1.2% of their workforce.

Workforce layoffs (BOF)

This makes it difficult to assess the company's normalized NI margin, as the company has seen significant volatility in recent years. If the company can achieve 4-8% consistently, it would be a good performance.

Moving onto the balance sheet, the company is certainly feeling the slowdown. Its inventory turnover has significantly declined and its CCC is up. This suggests inventory has begun to pile up and VFC is struggling to sell. This does come with the risk that VFC must discount the products to sell them, causing a short-term decline in margins.

Dividends had been climbing for several years but now is the time for this to significantly come down. The company needs to get its finances in order and cut back on avoidable expenditures to reinvest within the business. The company's current payout ratio shows this, having been at an unsustainable level for much of its underperforming period.

From a credit perspective, the company has taken on a substantial amount of debt in recent years, funding dividends and underperformance. Thankfully for investors, our view is that this has not yet reached a problematic level. Our default view is that 3x ND/EBITDA is good, with the company only marginally above this, suggesting some speculation but not an immediate issue. Moody's has given the company's most recent proposed unsecured note a Baa2 rating.

Overall, we certainly see potential here. The company has made good improvements and can achieve sustainable results if it can tighten up its operational side. The issue once again is that Management is seemingly getting in their own way, making missteps when running a struggling company like this requires perfection.

Outlook

Wall Street outlook (Tikr Terminal)

Presented above are analyst consensus numbers for VFC. Unsurprisingly, a decline in sales is forecast for FY23, on the back of what will be continued tough trading conditions. Based on the most recent quarterly performances, this looks reasonable.

From then on, steady growth is forecast, with margins slowing improving. Our view aligns on both an EBITDA and NI level, with VFC yet to show the ability to increase EBITDA margins, although should have less non-trading noise below this.

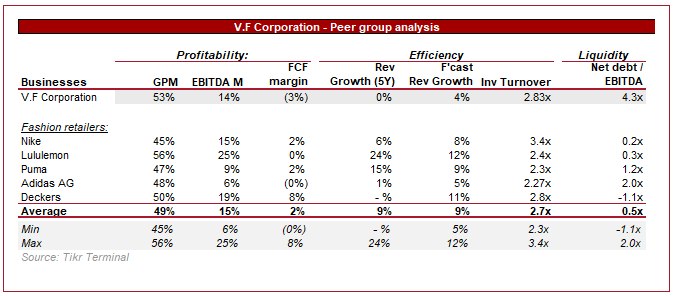

Peer group comparison

Peer group analysis (Tikr Terminal)

{kind=link}

Presented above is a cohort of brand-led fashion retailers. Although VFC has had a disastrous few years, the coming remains within view of these businesses. it has lifted GPM to a comparable level, with EBITDA in line if LULU is removed. The company's misstep in accumulating inventory has contributed to the FCF margin negativity, which they will pay for, but on a normalized level is not this bad. Growth and leverage are the key outliers here, and they go hand in hand. If growth can be kickstarted, their leverage ratio will come down.

Valuation

Peer group analysis (Tikr Terminal)

As this paper suggests, we do see potential in this business. The financials are slowly moving toward an attractive territory but questions will remain around growth. It is very easy for me to talk about Management's missteps, but it is far more difficult to address them. For this reason, rather than speculating on growth returning, investors should seek a discount in the valuation to reflect it.

VFC is currently trading at a 121% discount to its peers on an EBITDA multiple basis, a large amount given they are comparable on a profitability basis. In order to assess a relative valuation of the business, we have applied a 30% discount to Puma's ( PMMAF ), adidas' ( ADDYY ), and Deckers' ( DECK ) valuations. These are the weaker members of the cohort, allowing for a conservative view of VFC. This suggests an upside of 36%.

Further, we have conducted a DCF valuation, making the following assumptions:

- A marginal decline in FY24, followed by a bounce back to growth in the region of 3-5%. This reflects the assumption that improvements in brand positioning can be made in the coming year.

- An improvement in FCF conversion from 4% in FY24 to 6-7% in the following years.

- A perpetual growth rate of 2.5%, exit multiple of 12x, and a discount rate of 8%.

Our cash flow assumptions are more conservative than analysts' but still suggest an upside of 25%, above our relative view. Analysts are highly bullish on the business, forecasting 29% gains from here. Insiders concur with this it seems, suddenly turning extremely bullish on the business.

Insider trades (Darqube)

Final thoughts

VFC is far from an attractive investment on paper, with the company having many issues. There is potential here, however, the financials are comparable to the market and the business has the resources needed to reinstate growth. We covered The Gap several months ago and rated the stock a sell because we saw no hope for growth. The biggest difference with VFC is that it owns some genuinely fantastic brands. This makes Management's life far easier. The coming year will not be easy and VFC will face growing negative sentiment, but the scope for alpha is here. Based on the company's current valuation, we consider it a soft buy.

For further details see:

V.F. Corp: Potential For A Brand-Driven Renaissance