VFC - V.F. Corp.: Setting Realistic Expectations (Rating Downgrade)

2023-10-31 18:25:13 ET

Summary

- Management has issued cautious guidance for the remainder of FY2024, reducing free cash flow projections by 50% for the full year and cutting the quarterly dividend by 70%.

- Vans brand to continue struggling in the second half of 2024.

- Despite the decrease in revenue, V.F. Corporation managed to maintain stability in its adjusted gross margins, which only saw a slight decline of 20 basis points.

- Evaluation of V.F. Corporation's investment potential includes bear, base, and bull case scenarios, with a focus on market sentiment and long-term value.

Dividend & Guidance Cut

V.F. Corporation (VFC) shares initially plunged 10% but rebounded to close down 5% in after-hours trading following the release of its fiscal second quarter 2024 earnings report.

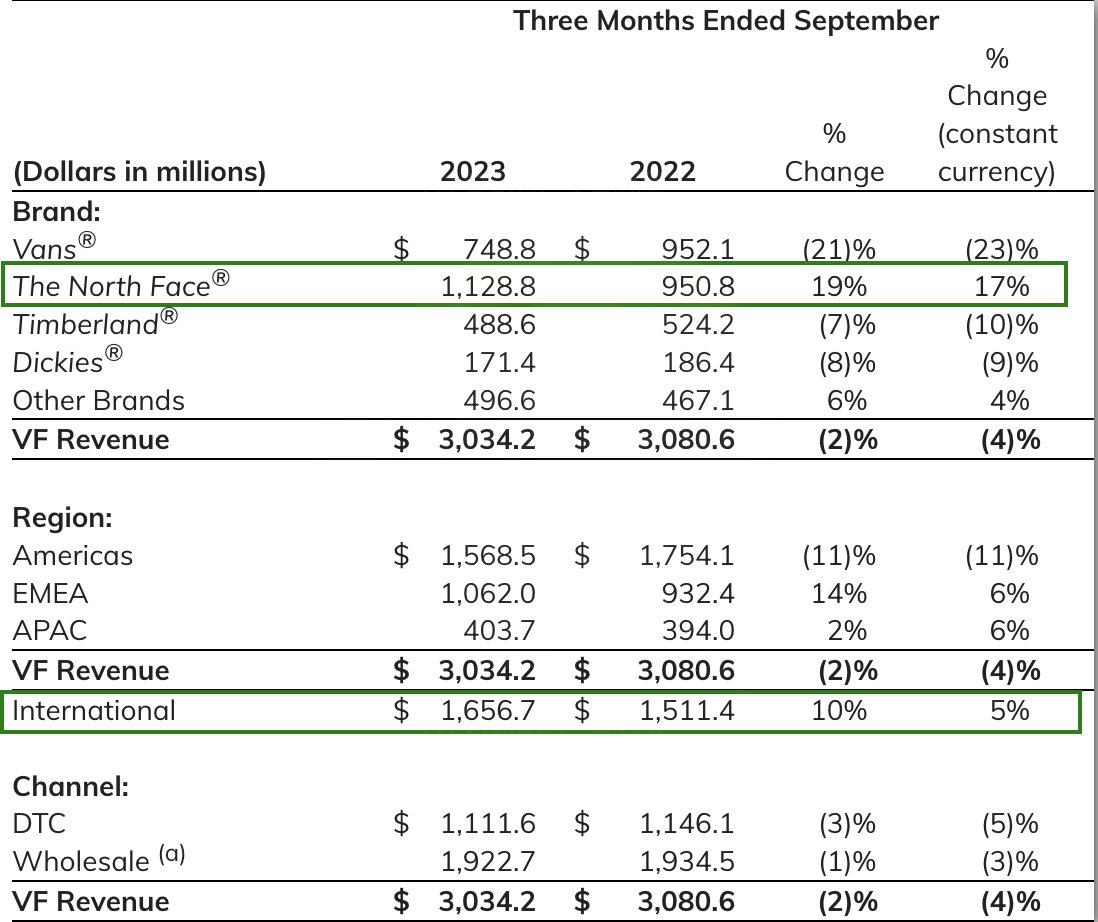

The company posted a 4% revenue decline on a constant currency basis as continued strength in its The North Face brand helped offset headwinds facing other brands like Vans. Despite the ongoing revenue deleveraging, VF managed to stabilize its adjusted gross margins, which declined just 20 basis points, and its adjusted operating margins fell 30 basis points compared to last year.

{kind=link}

However, management issued cautious guidance for the remainder of FY2024. They reduced free cash flow projections by 50% for the full year and cut the quarterly dividend by 70%. VF warned that the Vans brand in particular would continue to perform poorly in the second half of 2024.

FY24 Outlook

- The company withdraws its previous FY24 revenue and earnings guidance and updates its free cash flow projection:

- Free cash flow for FY24 is expected to be approximately $600 million compared to the previous guidance of approximately $900 million

- The following factors are now assumed to significantly impact revenue and profit negatively in 2H'FY24

- Vans' performance is not anticipated to improve in 2H'FY24

- A more difficult US wholesale environment

- Reinvent will likely result in charges including cash and non-cash items

Along with debt reduction, the new CEO unveiled a restructuring plan to cut costs and revitalize the brand.

Our transformation plan, Reinvent, directly addresses these areas in particular and importantly, commits to lowering our cost structure by $300 million. Through this effort and our ongoing evaluation of all aspects of our business, we remain laser-focused on cash generation and debt reduction, with the intent to return to growth, drive higher ROIC and reduce leverage.

Evaluating V.F. Corporation's Investment Potential

We will evaluate the risk-reward profile of V.F. Corporation stock based on bear, base, and bull case scenarios to form an investment recommendation.

The bear case examines the company's ability to avoid a distressed valuation in the near term. The base case looks at potential realities and valuation impacts in the next fiscal year. Finally, the bull case analyzes V.F. Corporation's value proposition from a long-term perspective based on cyclical trends. After assessing the likelihood and valuation impacts of each scenario, we will determine if the risk-reward profile supports a compelling investment case for V.F. Corporation at the current valuation.

Bear Case: Avoiding a Distressed Valuation

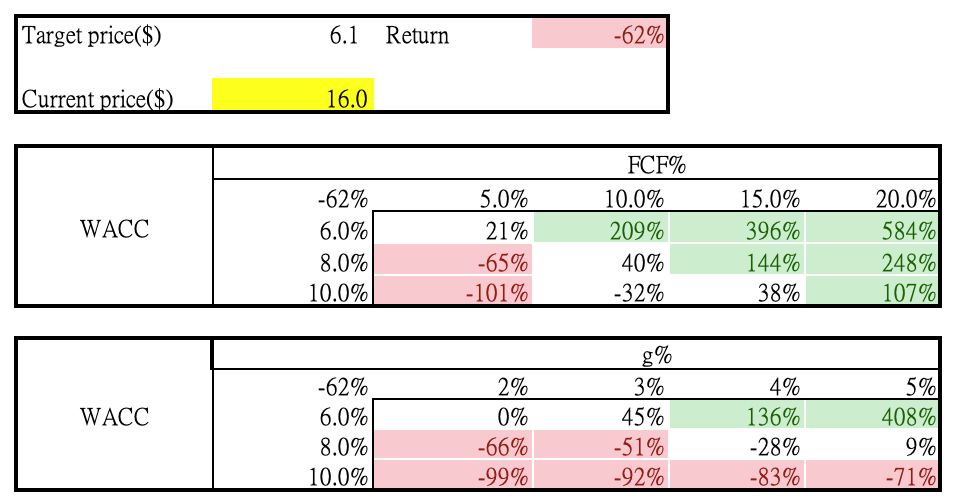

Despite the fact that the company reduced its free cash flow guidance, the company now expects to grow free cash flow flat compared to fiscal year 2022. This was not really as bearish as it first looked. It means that the company expects to generate around $770 million in free cash flow in the second half of 2024. This should avoid a valuation drop to a distressed case. It avoids the market pricing using book value, which is only around $2.2 billion. Hence, despite piling up debt and cutting dividends, at least in the short term, a bear case valuation is avoided.

Realities of the Base Case

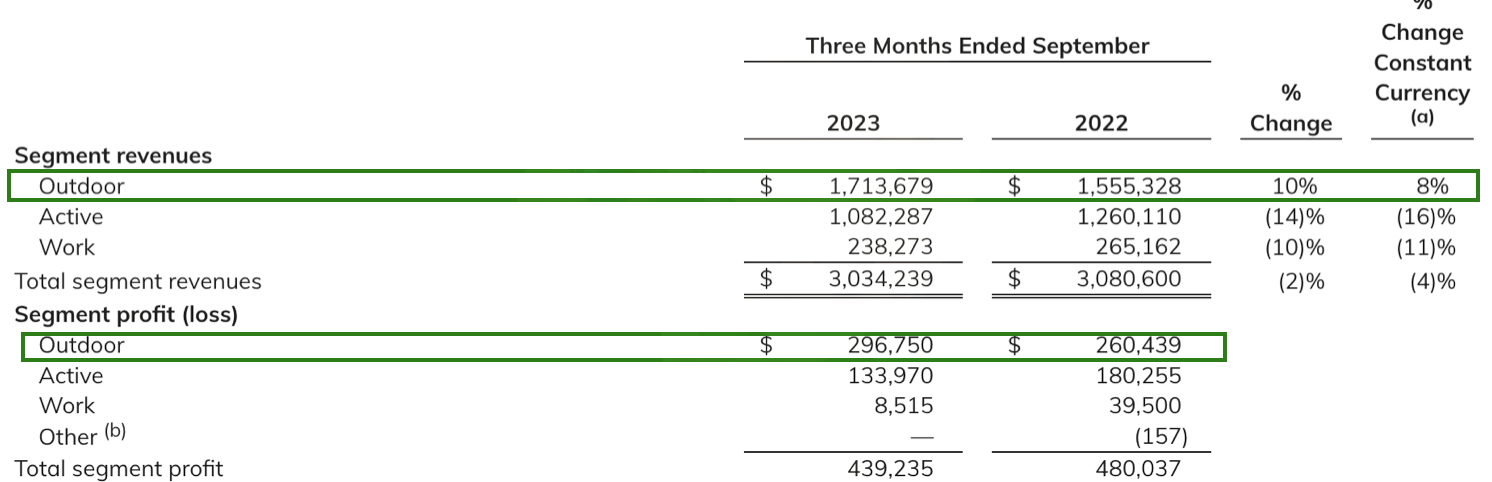

Given that the company expects a more difficult wholesale environment and lack of improvement in Vans, we see that the optimistic assumption in the base case is to assume flat growth in fiscal year 2024 as its Outdoor segment, which still grew at 8% constant currency in the quarter and accounted for 56% of revenues and 67% of the profits, was offsetting most of the headwind in the Active and Work segments.

{kind=link}

However, even under this assumption, this reduced our price target from $30 to $6 based on the free cash flow cut. Our new price target, which is 60% lower than the current price, assumes flat growth for the fiscal year 2024 and 3% terminal growth under an 8% weighted average cost of capital.

{kind=link}

Cyclical Trends and Long-Term Value: Building the Bull Case

Our bull case is from a cyclical point of view and evaluates the company's value proposition from a longer-term perspective. Long-term investors who are fans of the brands are probably going to assess the business from this angle as well.

We view the current weakness in the US market as temporarily driven by inflation disproportionately impacting lower-income consumers. As a brand targeting teens who tend to be lower income, Vans is suffering from cyclical headwinds rather than a deterioration of its underlying brand value. This assumption is somewhat supported by the fact that Vans maintained a relatively healthy operating margin despite significant operating deleverage. Specifically, while Vans' Active segment revenue was down 16% in the quarter, its operating margin was 12.3%, only a 200 basis point contraction from 14.3% in the same period last year.

In contrast, we view the Work segment as having become more commoditized, evidenced by its operating margin collapsing to 3.5% from 14.8%. Hence, we will exclude the Work segment from our long-term valuation analysis. We will assume the company divests this segment and reallocates resources to higher growth, higher margin segments like Vans and Outdoor.

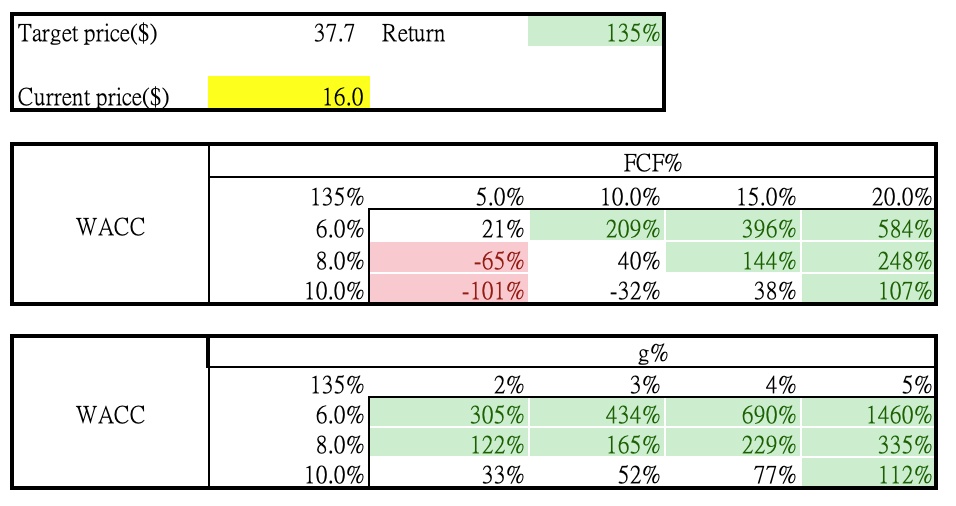

Our bull case assumes it takes 10 years for Vans to recover to FY2019 profitability levels after the current cyclical downturn. This reversion to peak profitability by FY2029 would improve Vans' free cash flow margin by an additional 1% to 16%. Applying a DCF model with these assumptions, we arrive at a bull case valuation implying a 135% 10-year return, equivalent to 13.5% annually.

{kind=link}

However, the bull case requires Vans to reenter a phase of margin expansion, which seems unlikely in fiscal year 2024 given management's guidance. Therefore, we expect the market to continue pricing V.F. Corporation based on the base case over the next 1-2 quarters. With risks skewed to the downside in the near term, we don't find the current valuation sufficiently attractive.

Risks and Catalysts

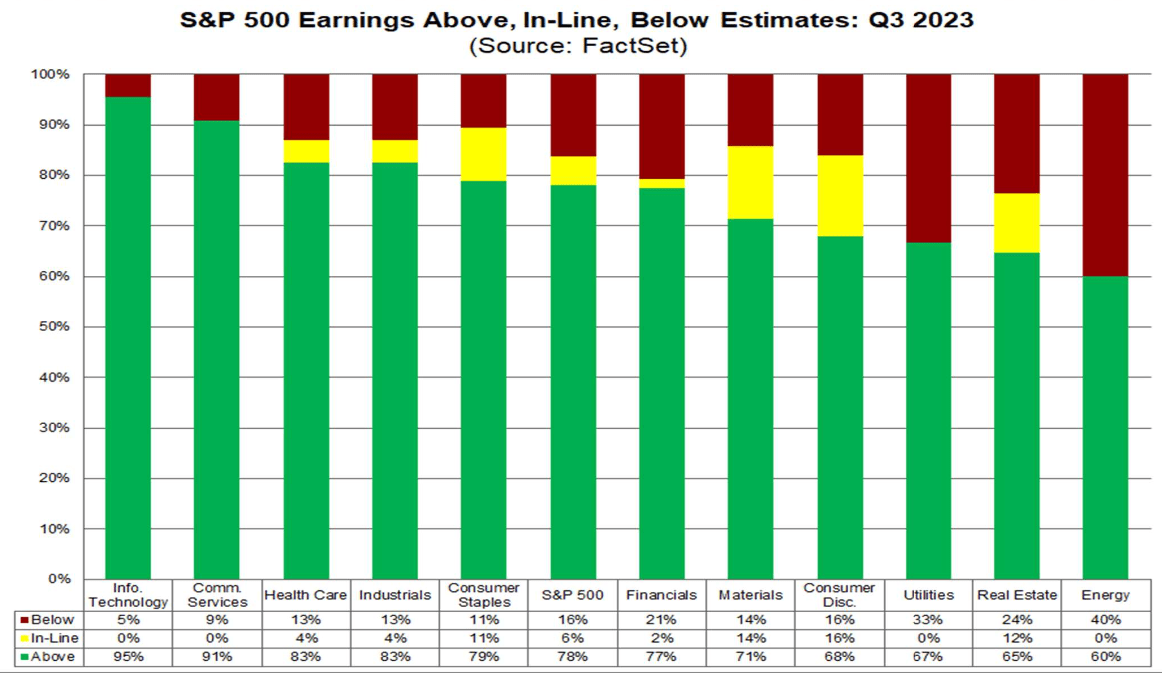

As of today, with 49% of companies reporting earnings so far, based on FactSet's data, 68% of companies in the consumer discretionary sector beat earnings. V.F. Corporation was actually underperforming the group. Hence, it is not surprising to see that the market should have more negative sentiment toward this stock.

{kind=link}

Compared to other sectors, consumer discretionary also ranked at the bottom in terms of earnings performance compared to analyst estimates. This can further lower the market's attention to this sector, which can put further pressure on valuation in the near term.

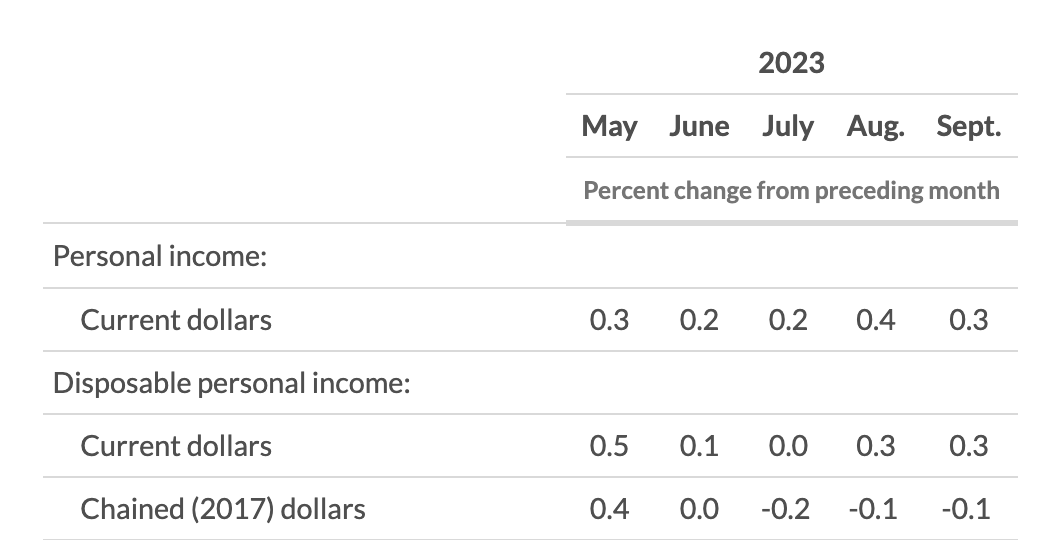

However, we see there are short-term upside scenarios where consumer spending may continue to surprise the market despite continued headwinds in the macro environment. As suggested by US Q3 GDP , consumer spending accelerated to 4% from 0.8% in Q2 while the US personal saving rate decreased to 3.4% in September 2023. This may be explained by the fact that consumer spending is currently supported by strong credit card spending because the real disposable personal income (chained 2017 dollars below) was actually in decline, which many experts see as not sustainable. Hence, investors should be cautious about the current consumer environment.

{kind=link}

Conclusion

Although Vans' double-digit declines appear severe, its margin resilience demonstrates brand strength versus the Work segment. The resilient Outdoor segment now generates over half of sales and two-thirds of operating income, instilling some confidence after dividend and cash flow cuts. However, base case valuation suggests a 60% downside, likely weighing on near-term sentiment. With V.F. Corporation also underperforming consumer discretionary peers amid missed estimates, negative sentiment could persist. Given the unattractive risk-reward profile under the base case, which appears the most probable scenario, we are downgrading to a Hold rating.

For further details see:

V.F. Corp.: Setting Realistic Expectations (Rating Downgrade)