VFC - V.F. Corporation: The New CEO Has A Lot Of Work To Do

2024-01-16 00:17:31 ET

Summary

- V.F. Corporation has experienced margin deterioration and stagnant revenues, with a high level of debt.

- The company's financial position is concerning, with elevated debt-to-equity ratios and increased operating expenses.

- The new CEO has yet to prove their ability to improve operations, and more evidence of growth and profitability is needed before investing.

Investment Thesis

V.F. Corporation ( VFC ) has experienced margin deterioration over the last few years and the revenues have been stagnant for the last decade, while the debt is hovering over its operations as a deterrent. I wanted to take a look at the company’s financial position to see whether it would be a good time to start a position. With margins not showing any improvement as of yet, revenues started to slow down again, and the new CEO Bracken Darrell has a lot to prove, therefore I am assigning a hold rating until I get some proof of improved operations.

Briefly on the Company

The company is a large American apparel, footwear and accessories company, that owns many familiar brands like The North Face, Vans, Timberland, Dickies, and Supreme. It was founded in 1899 as Reading Glove and Mitten Manufacturing Company. The name itself (V.F Corp.) may not sound familiar to many, but their brands are known worldwide, and I’m sure many own at least a pair under their umbrella, I know I do.

Financials

As of Q2 '24 , the company had around $500m in cash and equivalents, against $5.6B in long-term debt. That is almost as much as its current market cap, which will deter many more risk-averse investors, as debt carries a lot of risks if it is not managed properly. There are a few metrics I like to use to determine this. Firstly, the company's debt-to-assets ratio is reasonable, currently sitting at 0.43, which is below the 0.6 thresholds, therefore it's acceptable. The company's debt-to-equity ratio is a little elevated and above my threshold of 1.5, however, by not too much. It is still a little more on the riskier side as it is above the industry average by a lot. The company took on more debt during the pandemic and still has yet to pay down a significant amount. Lastly, I like to look at how the company can pay off its debt obligations, which is the annual interest expense on debt. Here, many analysts look for at least a 2x interest coverage ratio, whereas I prefer to see at least a 5x, as this allows for some bad years of performance and is still able to cover its obligations on debt. VFC's coverage ratio stood at around 6 as of Q2 ´24, which passes even my more conservative estimates. So, as long as the company can pay down more of the debt, I don't think it is at any risk of insolvency for now.

{kind=link}

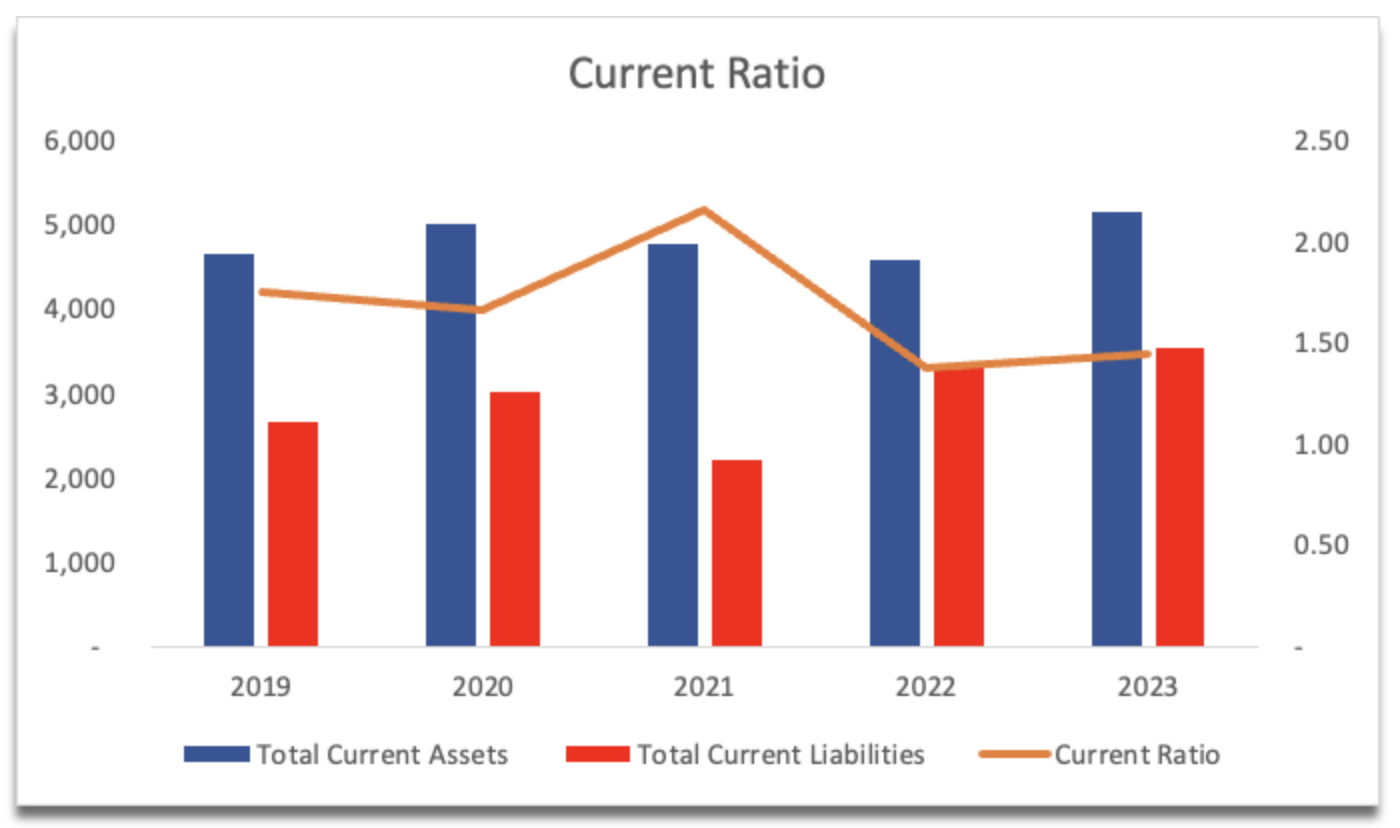

The company’s current ratio has been decent over the years, and as long as it's over 1, I consider it to be acceptable. At least the company can pay off its short-term obligations. It is close to that efficient range of 1.5 to 2.0, which means the company isn't holding too much inventory and is using its assets efficiently, therefore, VFC has no liquidity issues.

{kind=link}

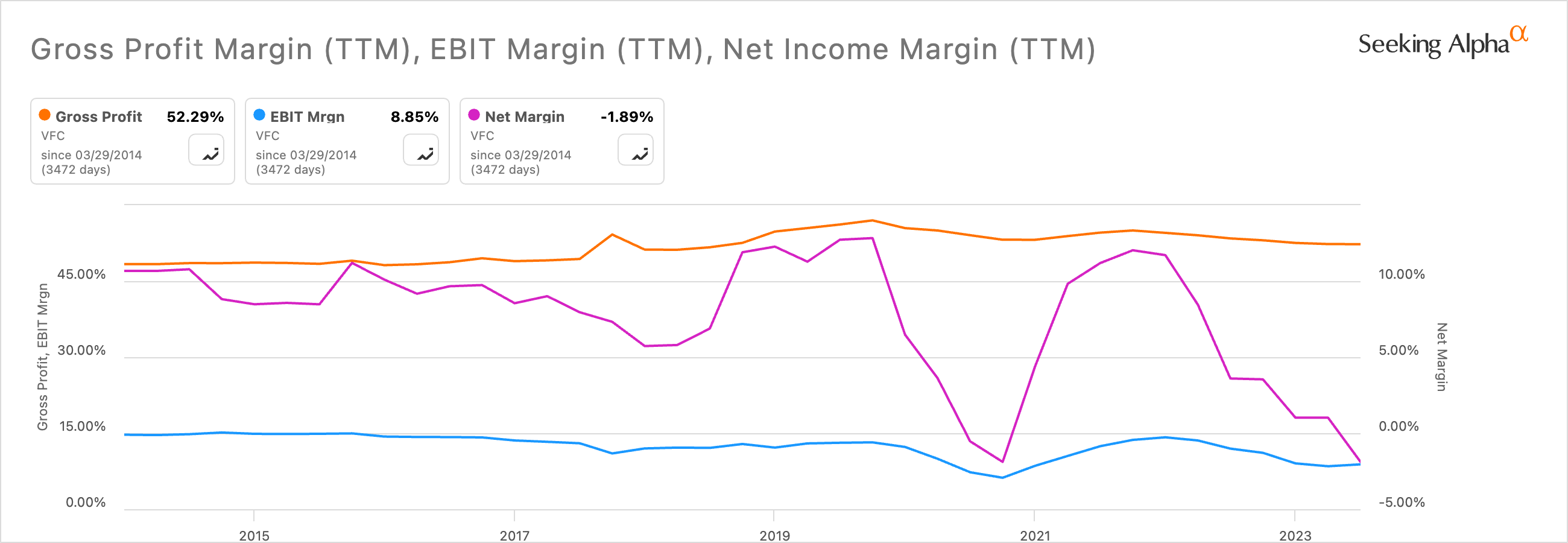

Continuing with efficiency and profitability, the margins have seen better days, and looking at the company's most recent quarter, it has not recovered yet, which is a big red flag. This is due to the company paying a massive tax bill concerning its Timberland acquisition, which ruled in favor of the IRS. That is on a GAAP basis, as this was a noncash expense of around $690m. I would expect this to not repeat over the coming quarters, and the company should see its margins improve. It is also worrying to see that the cost of goods sold and total operating expense as a percentage of revenue has increased by over 250bps and 270bps respectively from FY22 to FY23, and it doesn't seem to have improved a lot this year. Total operating expenses as a percentage of revenues have improved this quarter, however, if we look at the last two-quarter results, it is still elevated to around 45% of total revenues, while COGS stood at around 48%.

{kind=link}

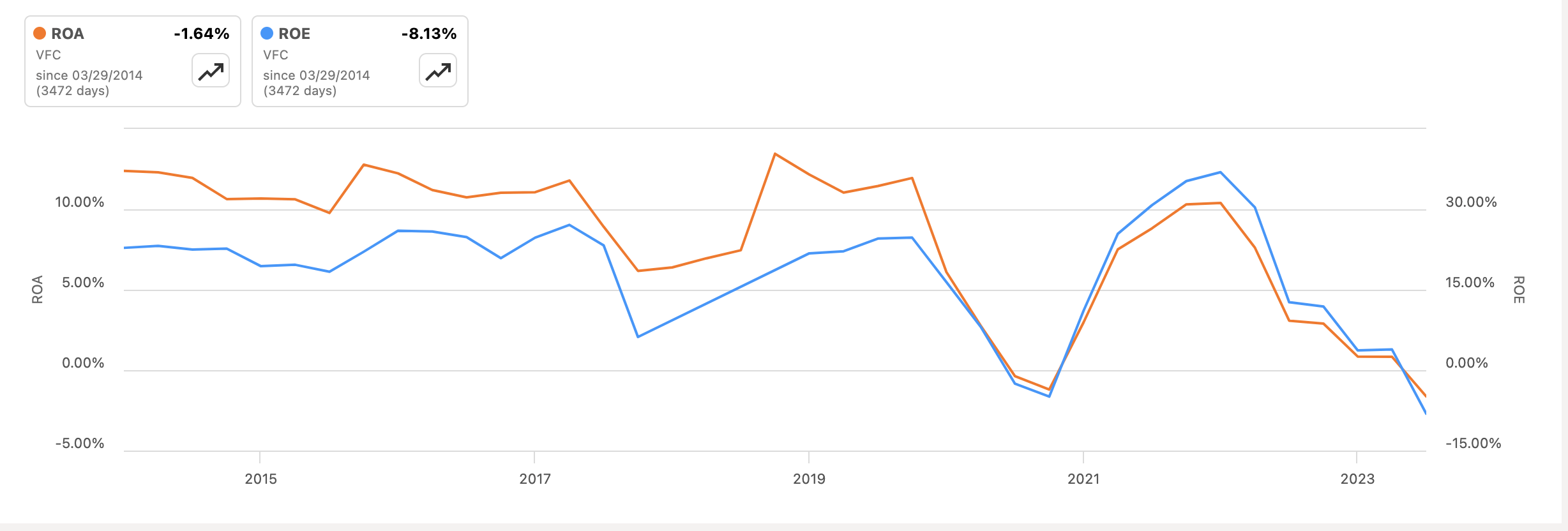

VFC's ROA and ROE have taken a plunge due to the company's poor performance so far this year. There is still no sign of improving profitability, however, once the company records a positive bottom line, these returns will improve also. I am looking for at least 5% on ROA and 10% on ROE if I am to consider the company worthy of investment. So far, the decrease in margins and negative ROA and ROE will demand a higher margin of safety in my valuation analysis section.

{kind=link}

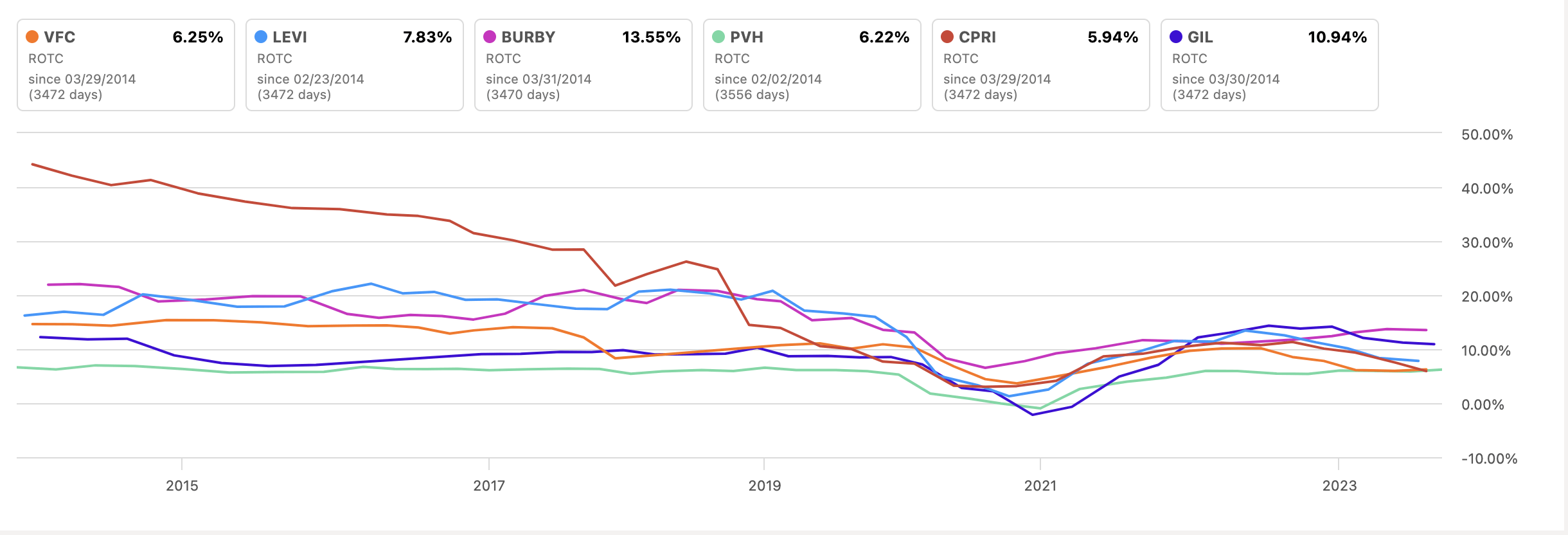

A similar story can be observed in the company's return on total capital, which measures how efficiently the capital is employed for profitable projects. Here, the company is somewhere on the bottom end of the competition, which is not ideal. That means the company may be lacking some competitive advantage and a moat. Furthermore, I think the management is not allocating capital to the best of its abilities. The company could double down on direct-to-consumer or DTC, while also prioritizing improving some of the laggard brands like Vans, which the company said were " not where we should be ".

{kind=link}

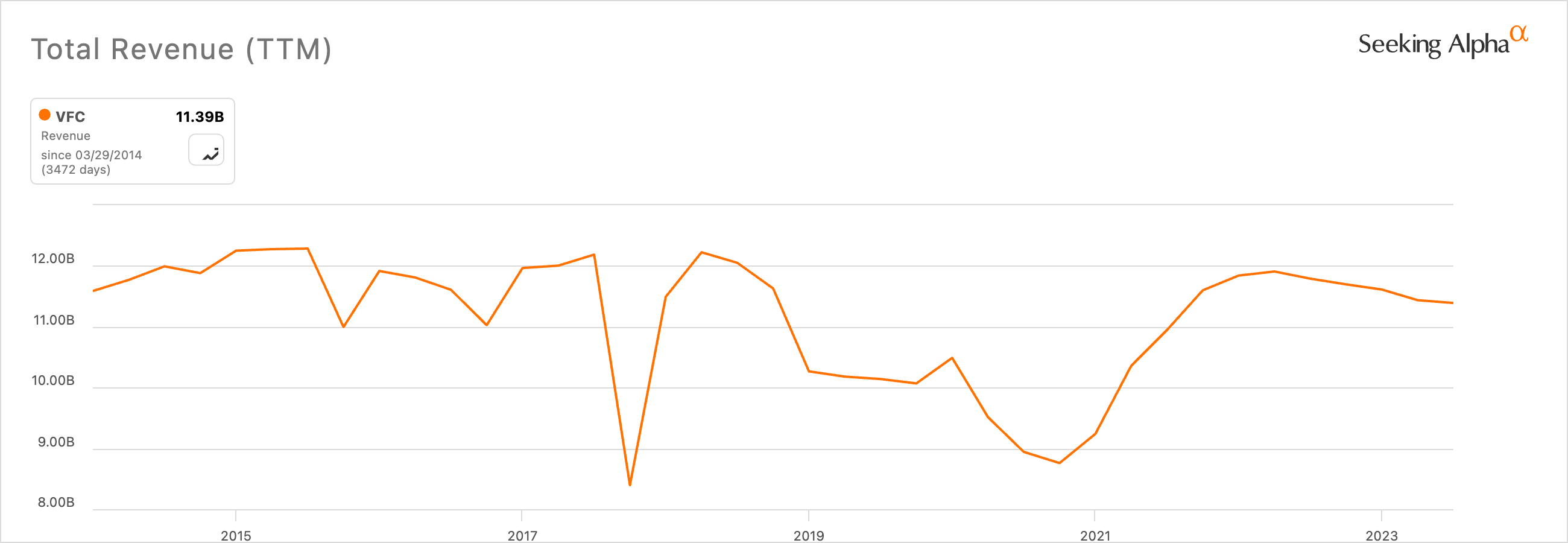

In terms of revenue, the company saw basically no growth over the last decade, which is not a very exciting discovery. The last three years saw around 12% CAGR, but that was due to the pandemic lockdowns easing and the pent-up demand. As you can see in the chart, that growth was not sustained, and the revenues saw a slight dip once again. Analysts estimate that the company will see decent growth after FY24, which is much more optimistic than what the company managed to achieve over the last decade, so I will be taking these estimates with a grain of salt.

Revenue Growth (Seeking Alpha)

{kind=link}

Overall, I see a company that is in quite a bit of a hole in terms of debt, with poor performance in recent quarters not showing a turnaround, and is not growing. I would be okay with stagnant revenue growth as long as margins are improving and the company is becoming more profitable, however, that is not the case right now with VFC, which means I will have to add more margin of safety to my valuation analysis in the next section.

Valuation

I approach my valuation analysis with a conservative mindset. This way, I am more neutral on the outcome of where the company is going to go, and will give me a lot more room for error in my estimations. For revenues, I decided to go with around 3% CAGR over the next decade, as I find it hard to believe that the company will manage to grow at a much faster pace than it did before without any catalysts in play. To cover my basis, I also modeled a more conservative and more optimistic outcome. Below are those assumptions and their respective CAGRs.

{kind=link}

In terms of margins and EPS, I assumed that the company would eke out a profit at the end of the year, which may not be very conservative, however, there are still two more quarters to go. The new management did not give guidance on where the company is going to be in terms of revenues, but I like the initiative I observed. Below are those assumptions. Do note that these numbers are slightly on the more conservative side than what the analysts are estimating.

Margins and EPS Assumptions (Author)

{kind=link}

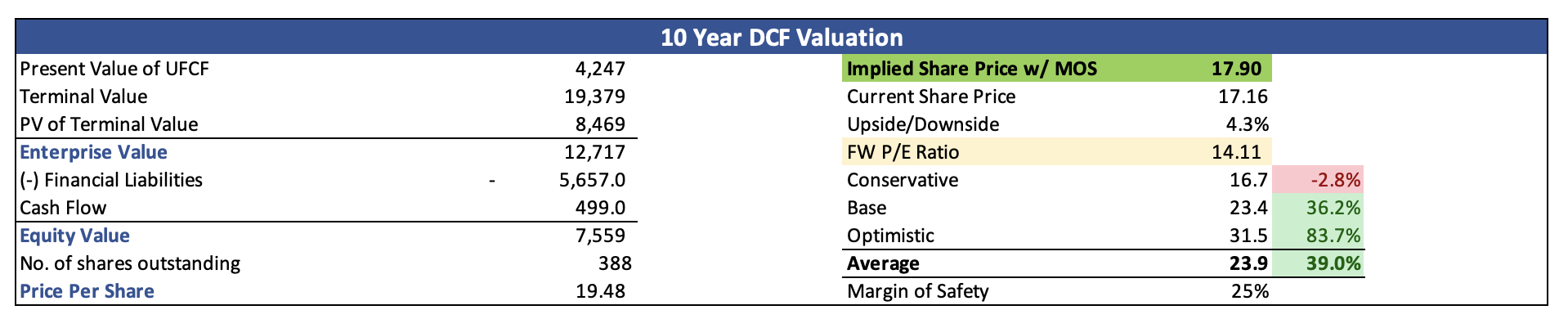

For the DCF analysis, to give myself even more margin of safety, I went with around 8.6% as my discount rate instead of the company's 7.6% WACC, and a terminal growth rate of 2.5%. The more conservative I am with the estimates, the better my chances of profit in the long run. Furthermore, to completely beat down the valuation, I added another 25% margin of safety to the intrinsic value calculation. With that said, VFC’s intrinsic value is around $18 a share, which means the company is trading at a slight discount to its conservative fair value.

{kind=link}

What’s stopping me from investing?

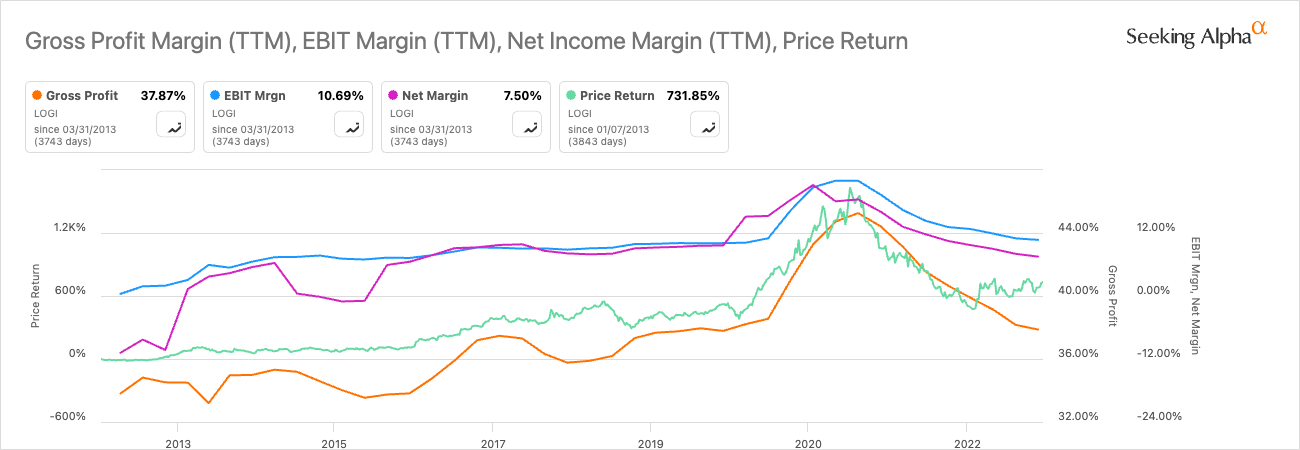

Even though the company seems to be good on paper, I would need to see proof that the revenues are growing, and the profitability and efficiency are improving. The new CEO has a lot to prove but looking at his previous position at Logitech (LOGI), the company became much more profitable, operating margins doubled and the share price skyrocketed also. So, it seems that he can turn the ship around, however, before I commit any capital, I would like to see actual results, and that will take a couple of quarters to develop.

Margins and Share Price of Logitech (Seeking Alpha)

{kind=link}

I would like to see the company make a dent in its large outstanding debt. It has reduced a little bit, but that will not attract the investors who are more debt-averse, and that is quite a lot of investors. The valuation estimates above are also not what the company has shown recently, and I am hoping that the company will return to profitability in the next couple of quarters with the help of the new CEO. If that doesn’t happen, I will be adjusting my model accordingly to reflect the current situation more accurately.

Closing Comments

The company comes with a lot of uncertainties, which keep me from committing any capital right now. If the company does manage to become profitable, and if the numbers are as close to what I have modeled above, then the company looks rather cheap compared to its competitors and would be a decent buy, however, I am not very certain of the macroenvironment we are going to see over the next half a year to a year, which will bring a lot of volatility, especially if inflation continues to linger and the US economy continues to perform well, which is the opposite of what the Fed is hoping for. This would open to more interest rate hikes but that could be a farfetched idea, not out of the realm of possibility, however.

For now, I will continue to monitor the economy and how the new CEO is going to perform over the next couple of quarters and decide whether or not I should commit some capital for the long haul. I just need some proof that the management is starting to turn this ship around.

For further details see:

V.F. Corporation: The New CEO Has A Lot Of Work To Do