VFC - V.F. Corporation: The Reasons Why We Do Not Want To Own The Stock In 2024

2024-01-16 11:23:23 ET

Summary

- V.F. Corporation has lost about 60% of its market value since our previous article.

- Consumer confidence and inflation are improving, which is promising for VFC and other firms in the consumer discretionary space.

- VFC's profitability, dividend safety, and valuation are unattractive, and for these reasons, we believe that it's not worth owning the stock. The recent incidents related to cybersecurity are also troubling.

- We would like to see improved profitability, a safe dividend and a more attractive valuation, before we would consider turning more bullish on the firm.

V.F. Corporation ( VFC ), together with its subsidiaries, engages in the design, procurement, marketing, and distribution of branded lifestyle apparel, footwear, and related products. It sells its products under well-known brand names like The North Face, Timberland, Vans and Supreme, just to mention a few.

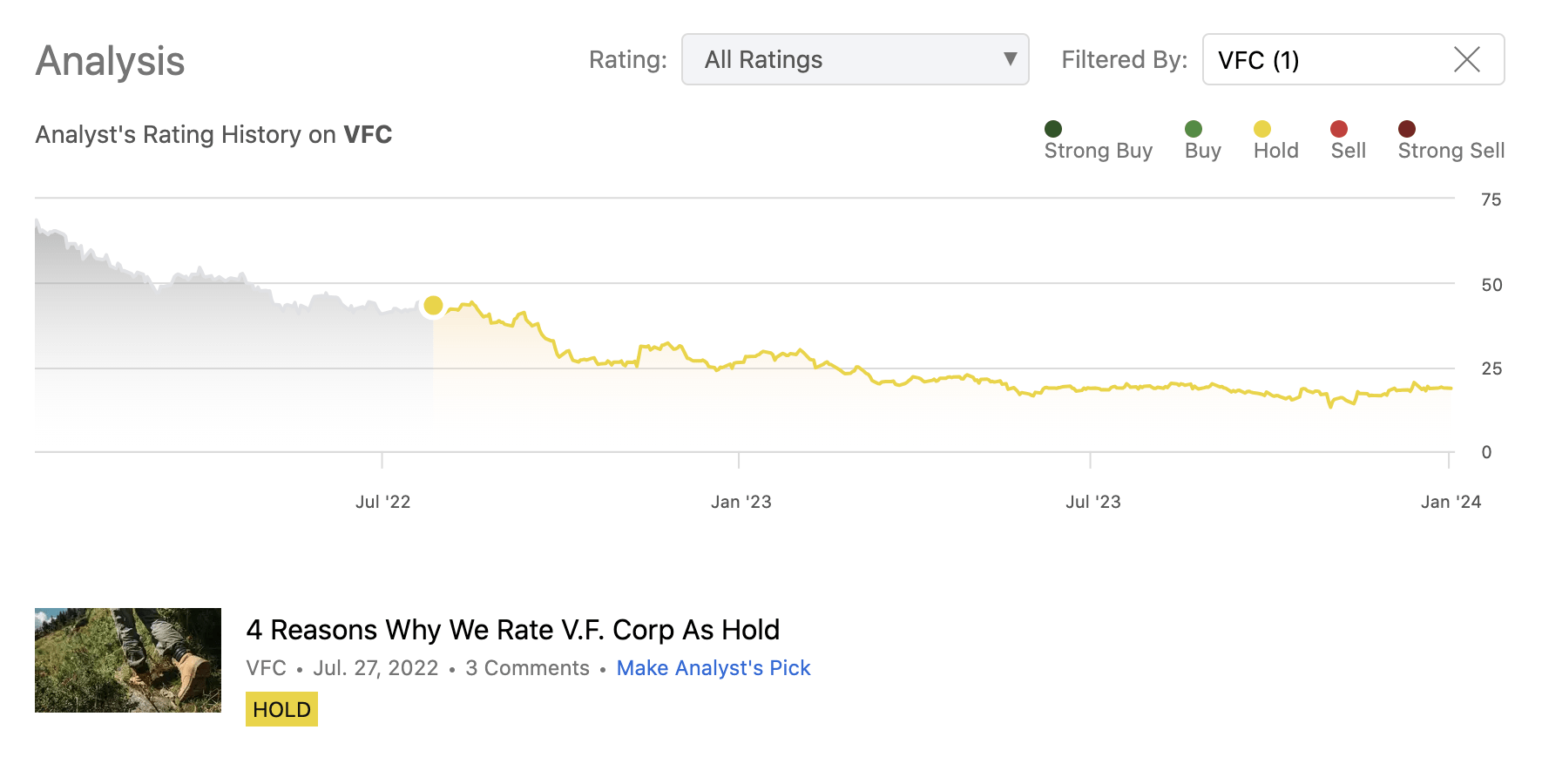

We have written an article about the firm in July 2022, assigning it an initial hold rating. Our primary arguments for the neutral view have been the following:

- VFC has performed well during periods, characterized by low consumer confidence

- Currency headwinds

- Elevated inflation putting downward pressure on margins

In fact, we have underestimated the significance and magnitude of these headwinds as the firm has lost about 60% of its market value since our previous writing.

{kind=link}

Lately, the firm's stock price has been also under pressure due to various reasons, including: cybersecurity incidents , the plunge of sales of Vans sneakers , or the 70% dividend cut .

The aim of our article today is to revisit our investment thesis and assess, whether our previous established hold rating is still valid, and essentially to conclude whether it is worth holding the stock in the near future.

To kick off our discussion, we are going to first take a look at the macroeconomic environment.

Macroeconomic environment

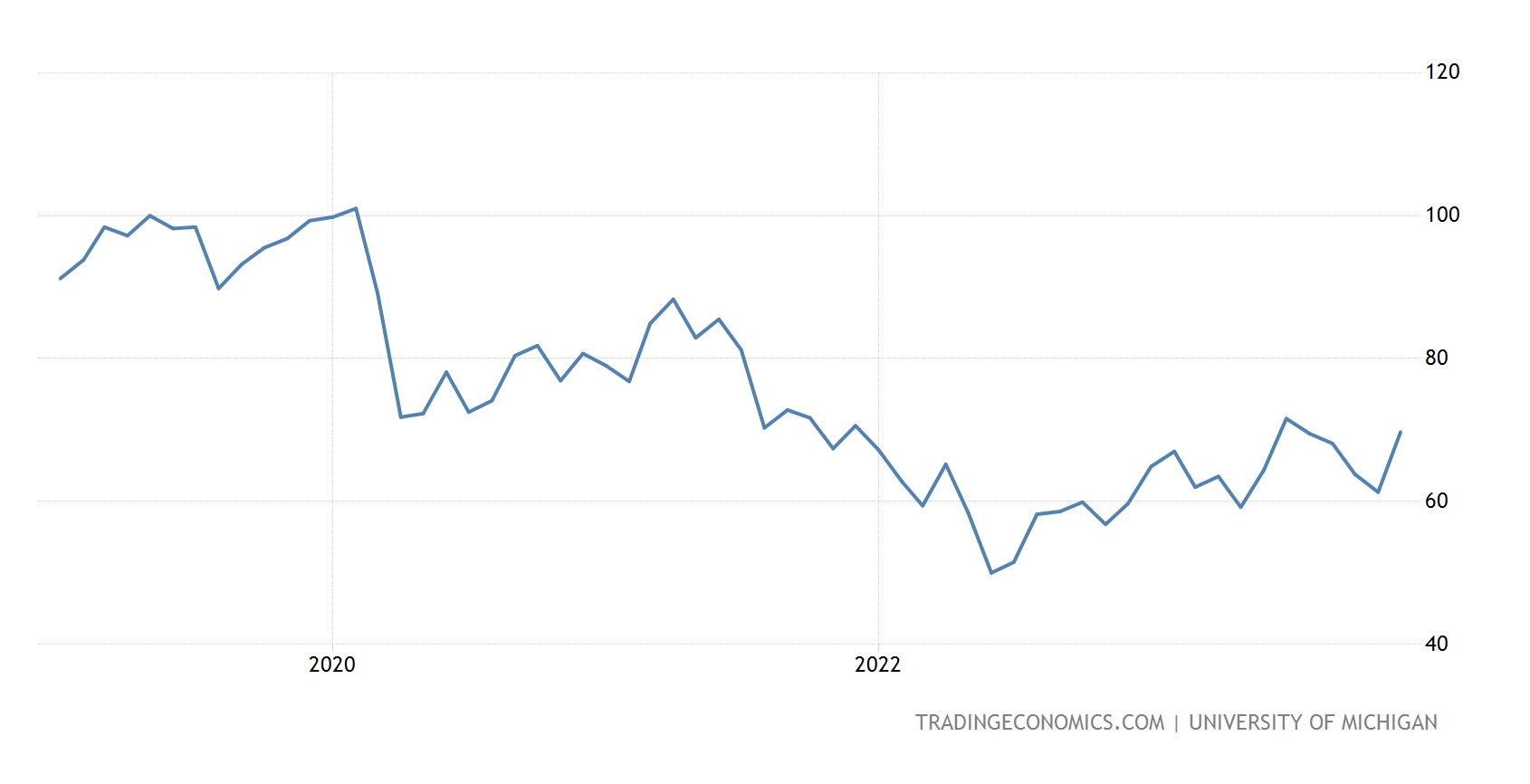

Consumer confidence

When writing about firms in the consumer discretionary sector, we often like to assess the level of consumer sentiment first, as this is often regarded as a leading economic indicator. The demand for discretionary products and services is naturally linked to how confident the consumer is feeling. During times of financial uncertainty, when people are less certain about their near-term financial outlook, they are less likely to spend on items, which are not necessities - e.g. items that VFC also sells. Depending on the level of confidence, we can get an indication of how the demand for these products may develop in the near future. The chart below shows how consumer confidence in the United States has changed in the past 5 years.

U.S. Consumer confidence (Tradingeconomics.com)

{kind=link}

We can see that the sentiment has been the worst in the first half of 2022 and has significantly improved since then, even if still being far away from pre-pandemic levels. In our view, this relatively steady improvement is promising not only for VFC but also other firms in the consumer discretionary space.

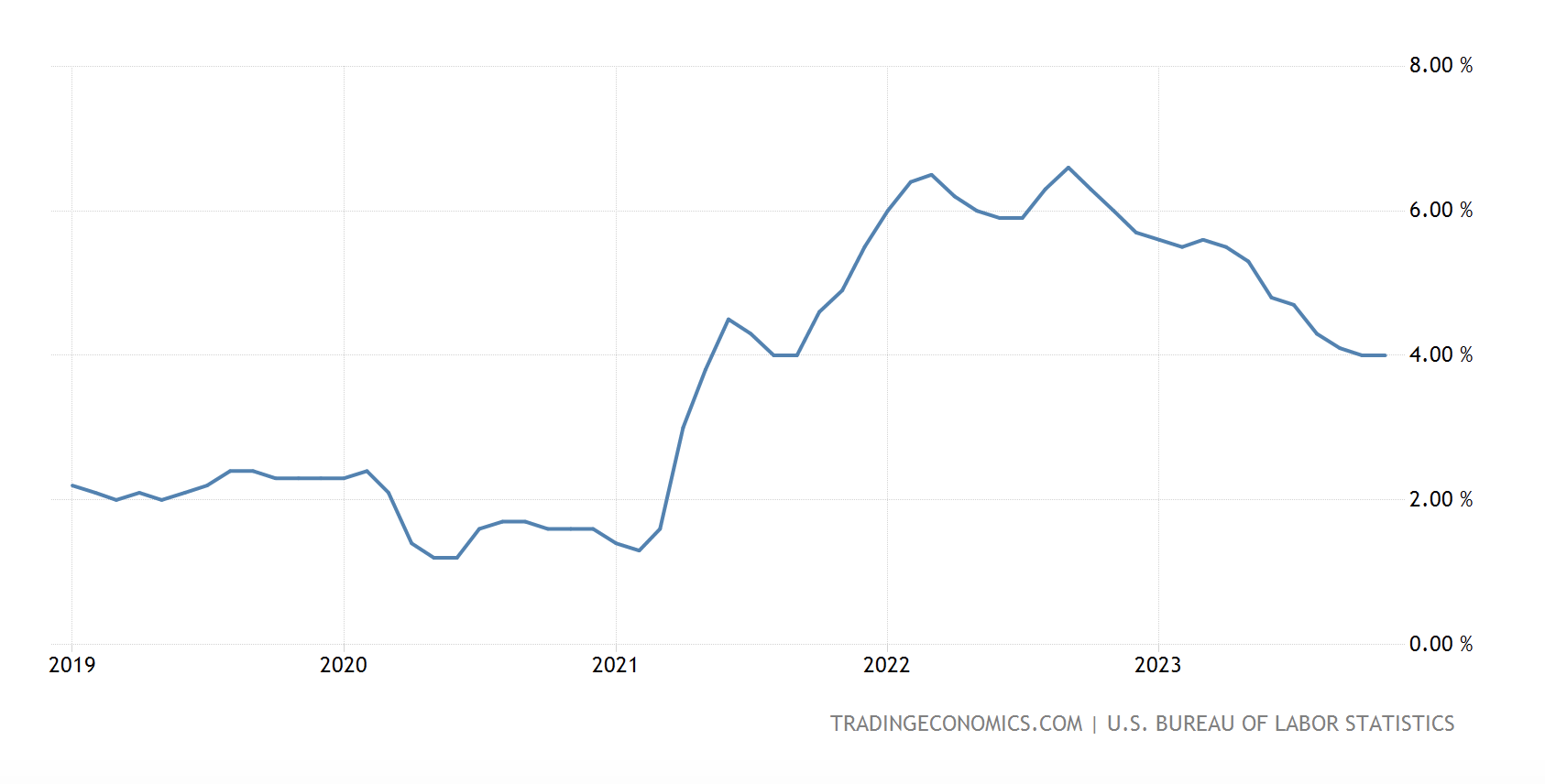

Inflation

The next item on our list to assess is inflation. Inflation plays a significant role in how costs are developing, and therefore, how margins are developing. Potentially, it is giving an indication, whether the firm is able to pass its elevated costs to the consumers, at least partially, to avoid significant margin contractions.

The following chart shows the core inflation rate in the United States.

U.S. Core inflation rate (tradingeconomics.com)

{kind=link}

We can see that inflation has been improving gradually as well, since its peak in 2022. This again is a positive sign for VFC and its peers, as they less likely to have elevated pressure on the cost side, and therefore less likely to experience severe margin contractions in the near term.

For these reasons, from a macroeconomic perspective, we believe it is worth holding VFC in a diversified portfolio for 2024.

Company-specific considerations

We continue our discussion focusing on company-specific issues, including, but not limited to the development of profitability, the sustainability of the dividend and last, but not least, the current valuation.

Profitability

The following chart shows the development of the gross margin, the operating margin and the profit margin over the past five years.

It is clearly visible that in 2022 and 2023 has been struggling with staying profitable, as indicated by the negative profit margin. While the operating margin has recently ticked up, we would like to see the net profit margin staying above zero for an extended period, before we would be confident in assigning a bullish rating to the stock.

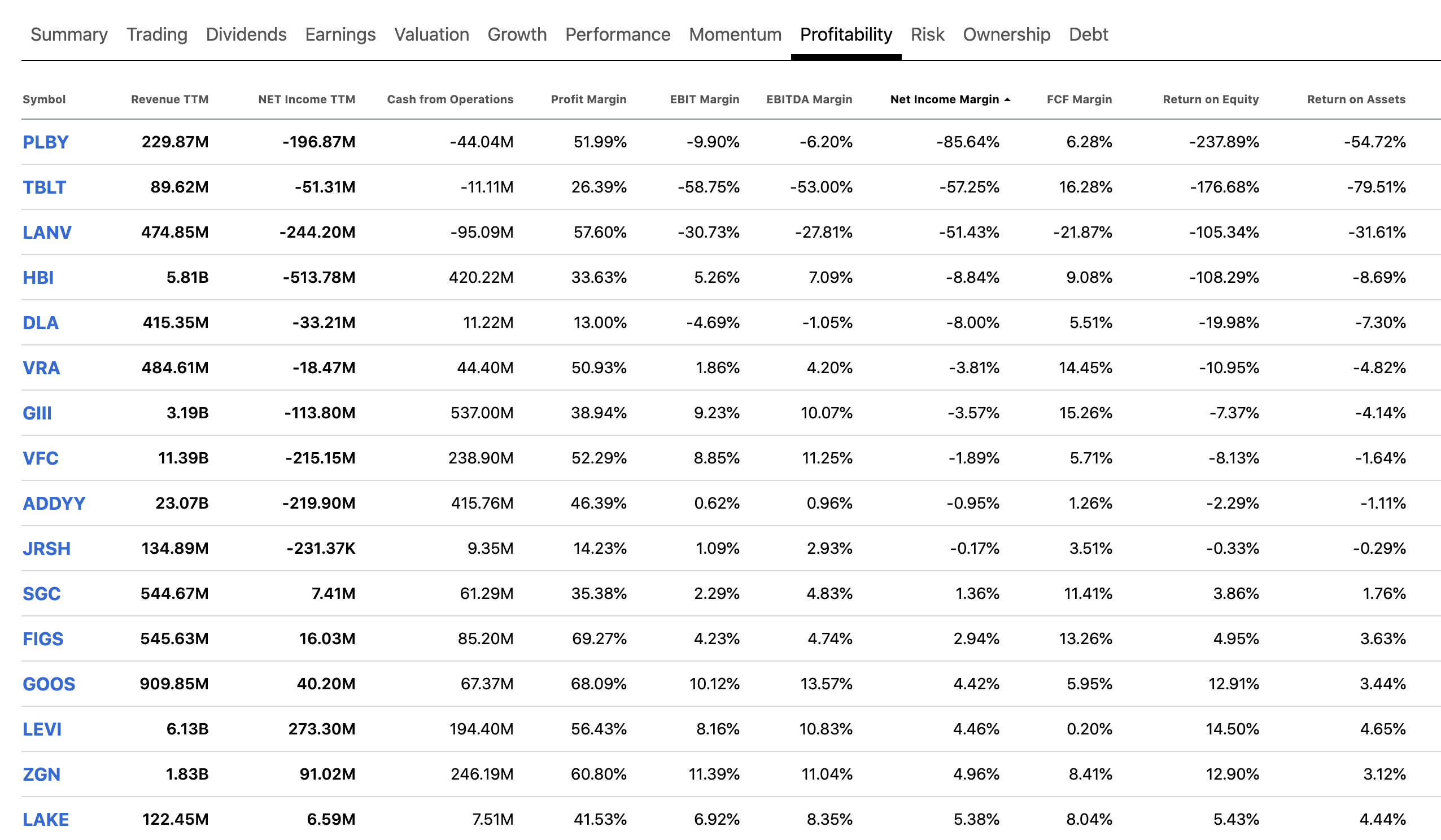

When comparing these metrics with those of VFC's peers in the Apparel, Accessories and Luxury Goods industry, it is clearly visible that VFC is quite unattractive from this perspective. The following table shows the worst companies from a profitability perspective in the industry, and VFC belongs to this group.

{kind=link}

Dividend

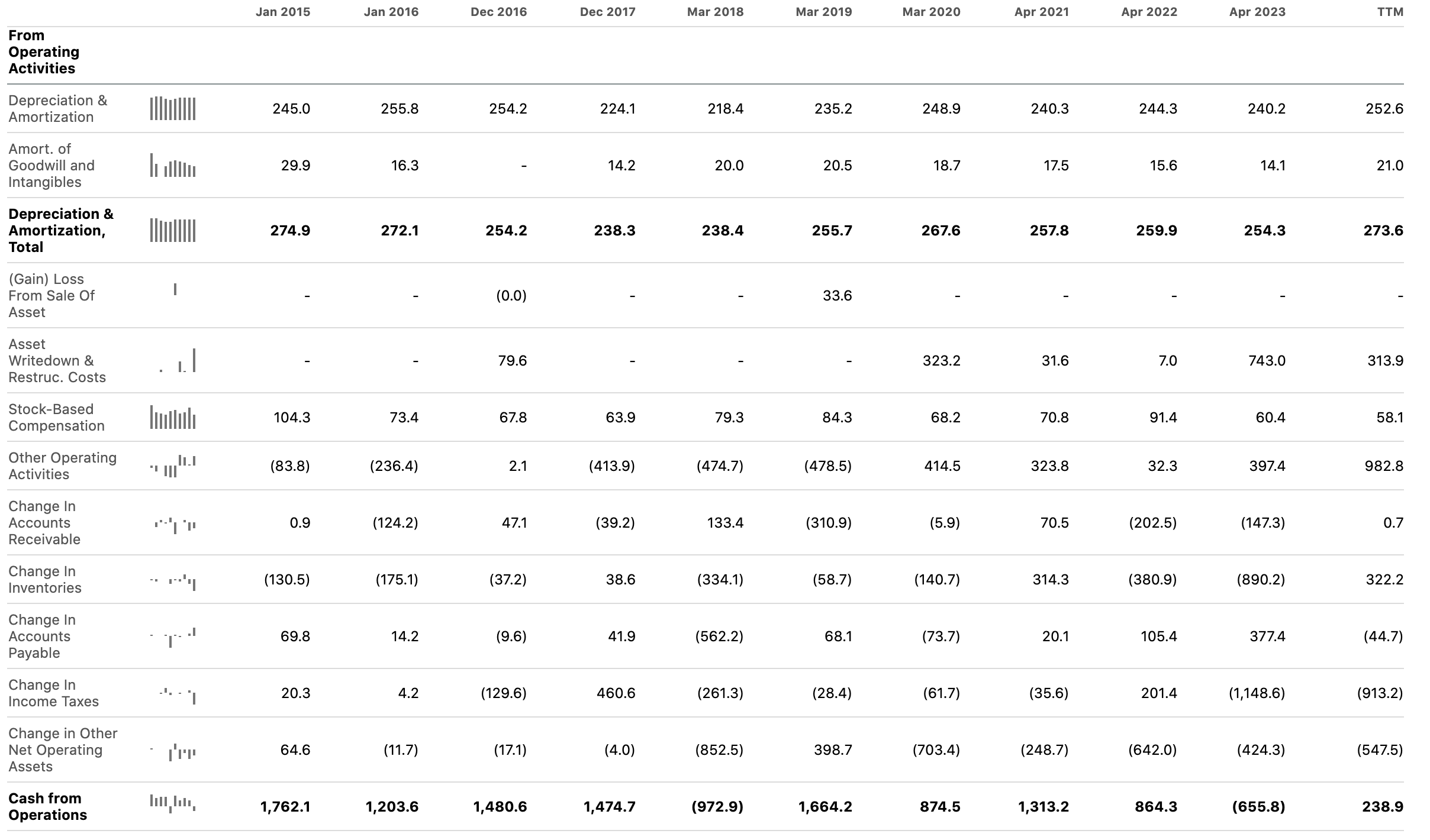

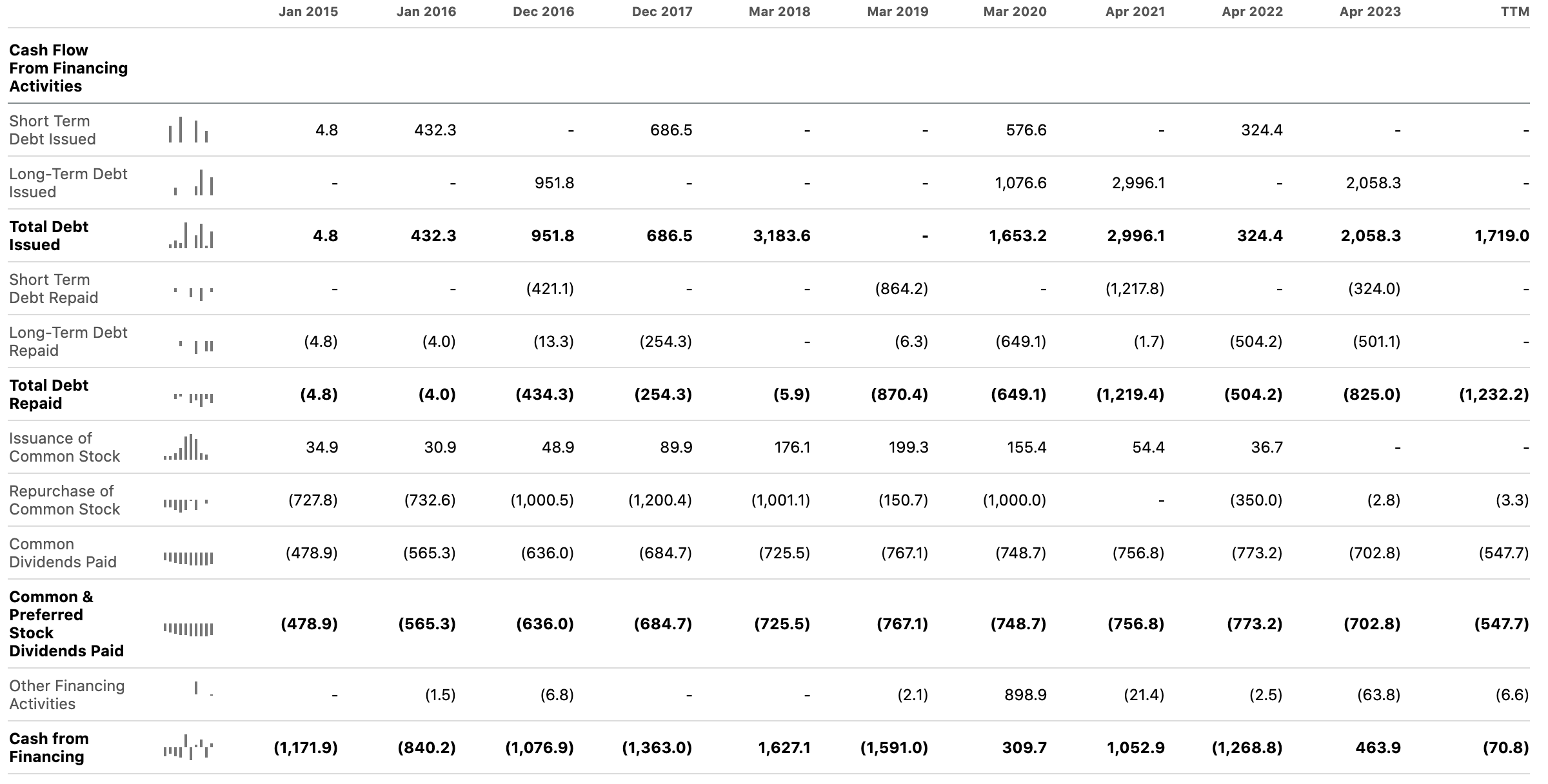

As briefly mentioned before, VFC has just recently cut its dividend significantly. While it may not be the best news for the existing shareholders, we believe it was a necessary step. If we look at the cash flow from operation/ free cash flow figures, as well as on how much the firm has been spending on dividends and share buybacks, it is clear that the policy has not been sustainable in the recent past.

Cash flow from operations (Seeking Alpha) Cash flow from financing (Seeking Alpha)

{kind=link}

{kind=link}

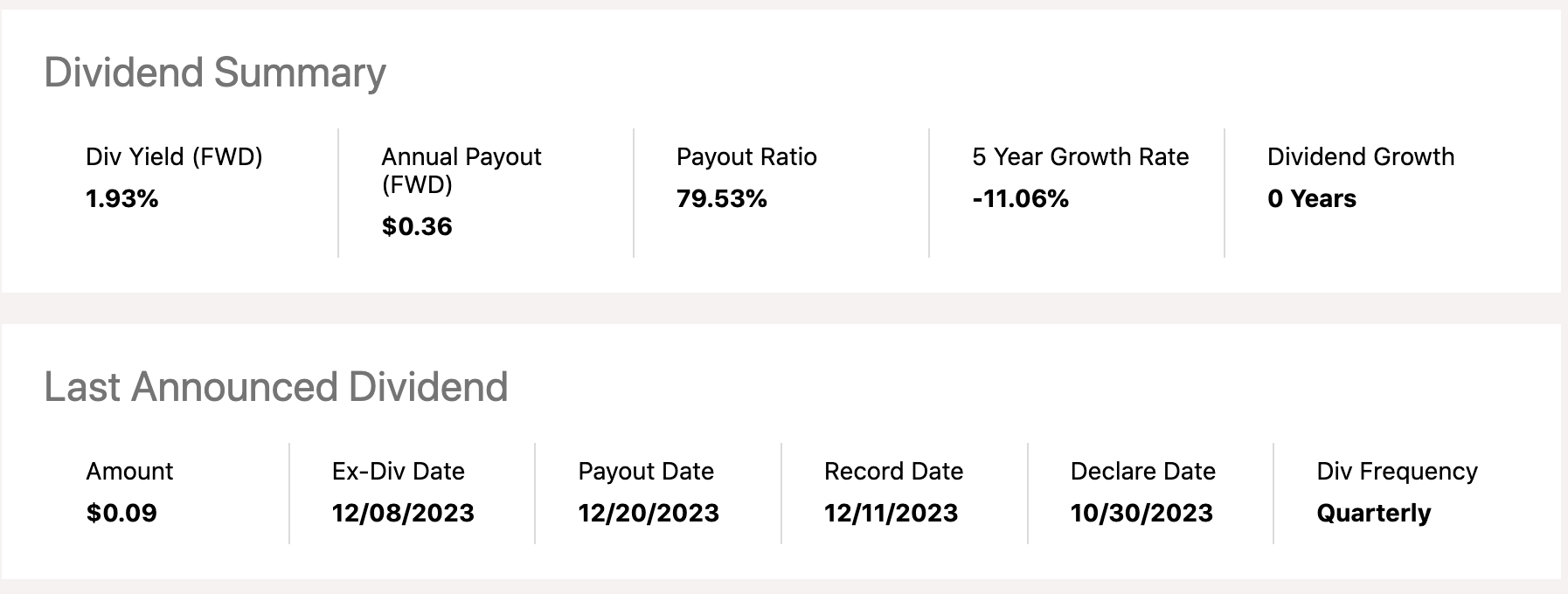

While the firm still pays a modest dividend of $0.09 per share on a quarterly basis, we do not believe that it is particularly appealing for dividend investors. Especially, when we consider that the payout ratio remains around 80%.

{kind=link}

Once again, we would like to see the profitability improve, in order to be more sure that the dividend is sustainable in the near term. Until then, we cannot assign a bullish rating to the firm from a dividend investing perspective.

Valuation

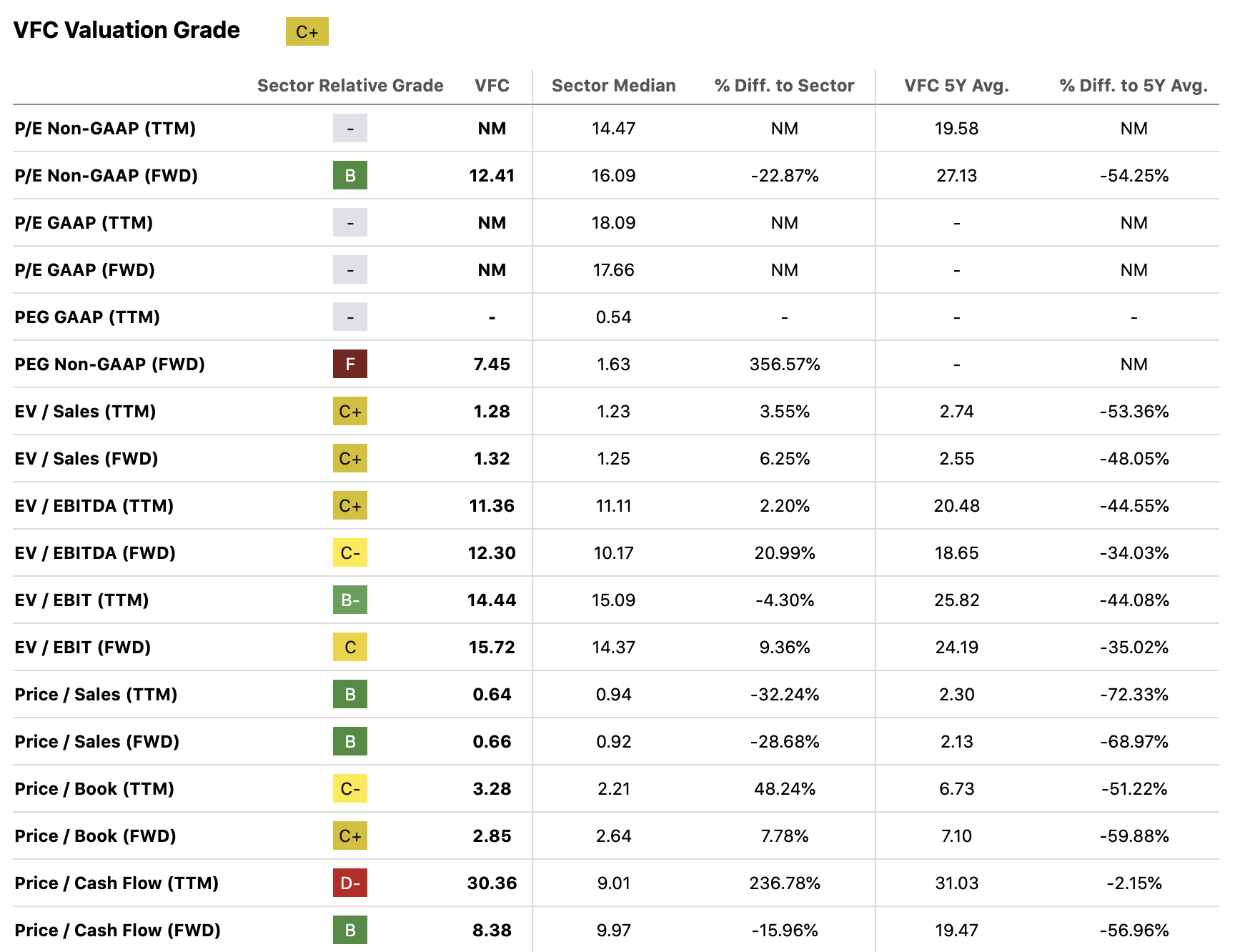

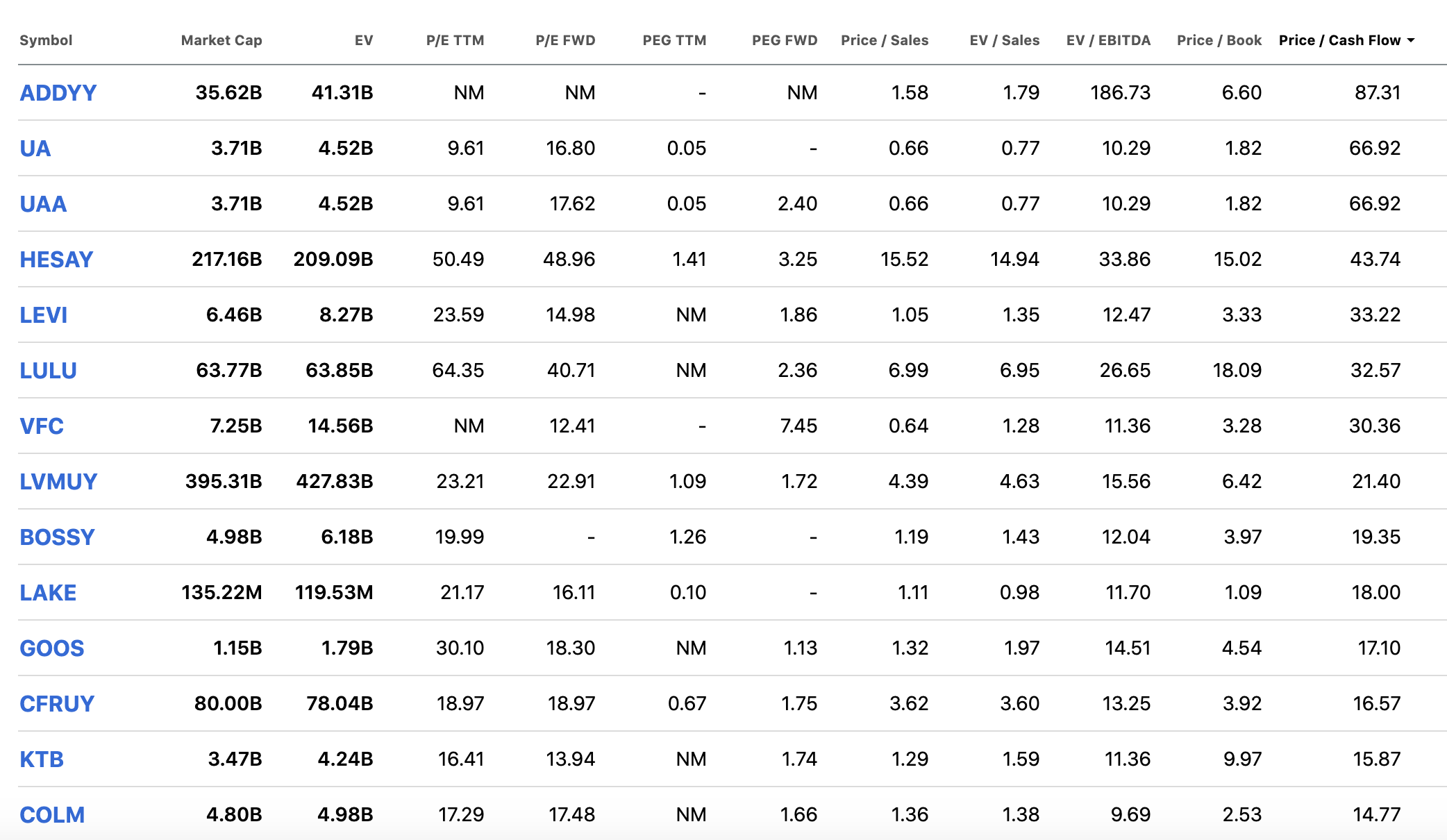

In this section, we are going to take a look at a set of traditional price multiples to determine, whether the firm is priced attractive compared to its peers and its own historic averages.

The following table compares selected valuation metrics between VFC and the consumer discretionary sector median as well as VFC's current figures with its 5yr historic averages.

{kind=link}

While compared to its own historic averages, the current valuation looks reasonable, compared to the respective sectors' medians, the numbers are not appealing to us. Considering the recent cyberattacks, the poor profitability and the - in our opinion - questionable sustainability of the dividend, we would like to see VFC trading at a clear discount compared to the sector median across most metrics.

When we narrow down the comparison to selected firms in the industry, VFC's stock still does not appear to be attractively priced.

{kind=link}

In our opinion, an additional share price drop of 10% to 15% could bring the stock into a territory, where there could be enough margin of safety to reconsider a potential investment.

Summary

While the macroeconomic environment is clearly showing signs of improvement, VFC remains unattractive from a company-specific perspective.

The firm is struggling with achieving a positive net income margin. The dividend safety remains questionable even after the dividend cut not so long ago. The valuation, in our opinion, still does not provide enough margin of safety to consider a value investment.

For these reasons, we believe that it is not yet worth owning VFC's stock.

Before becoming more bullish on the firm, we would like to see clear profitability improvements, with net profit margins maintained in the positive territory for an extended period, as well as improved dividend safety and more attractive valuation.

For further details see:

V.F. Corporation: The Reasons Why We Do Not Want To Own The Stock In 2024