VFC - V.F. Corporation: Too Soon To Count On Restructuring

2024-01-13 09:59:45 ET

Summary

- VF Corporation's stock price has dropped by 46.5% in the past year on weakening financials. But there's potential for improvement going forward.

- Its EMEA sales are strong, and the APAC region has picked up too. One off charges have affected earnings recently, but this can normalise.

- A restructuring plan underway can also revitalise VFC. However, for now, weak US consumer demand and discouraging past trends make it a wait-and-watch rather than a Buy.

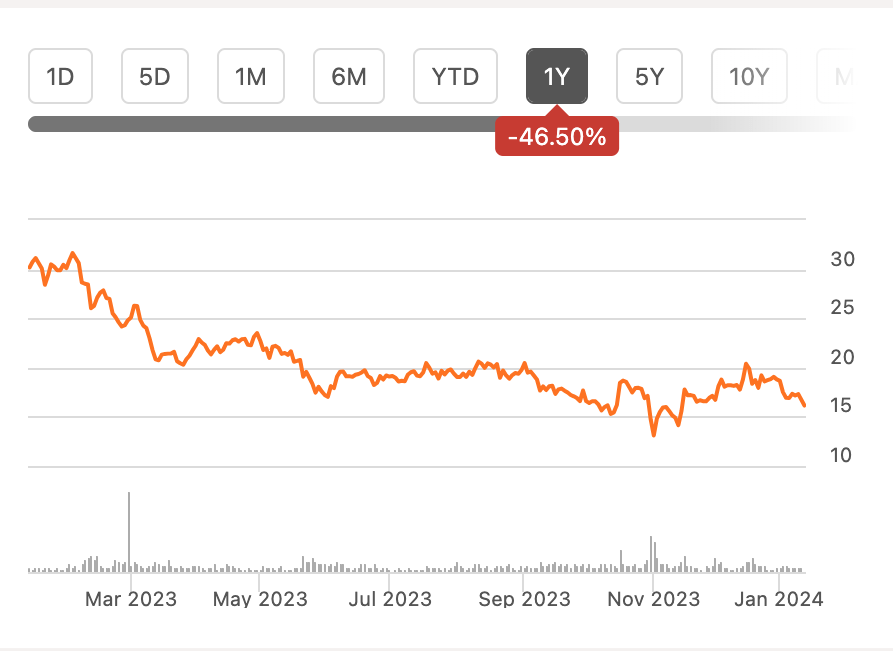

At first glance, the owner of outdoor apparel and accessories brands like The North Face and Timberland, VF Corporation ( VFC ) looks like a write-off. In the past year, its stock price has dropped by 46.5% as its revenues and earnings shrank. The company’s 2024 earnings estimates are discouraging too.

{kind=link}

But there’s more to it. For one, the company’s forward earnings estimates are encouraging. It’s also trading at a competitive forward price-to-earnings (P/E) ratio to the consumer discretionary sector and there’s something to be said for its sector beating 5.7% trailing twelve months [TTM] dividend yield. And it’s expected to see an earnings upswing from 2025 onwards as per analysts’ projections.

In a nutshell, there are arguments on both sides for VFC. Here I take a closer look at its fundamentals and what’s holding it back to assess what’s next for it, especially as it readies for its third quarter (Q3 FY24, quarter ending December 2023) results later this month.

What's holding VFC back?

Demand impacted by slowing US market

A look at the company’s revenues, which declined by 4% for the first half of the current financial (H1 FY24), reveals that the current demand challenge needs to be seen in a macroeconomic context. 58% of VF Corporations’s revenues came from the US market in FY23, which is seeing weak demand across the board for consumer discretionary companies. From the luxury fashion brand and company Christian Dior (CHDRF), which has already seen weakening US demand to the pre-loved clothing company ThredUp (TDUP), which expects slowing sales on weaker US demand in 2024, the trend is clear.

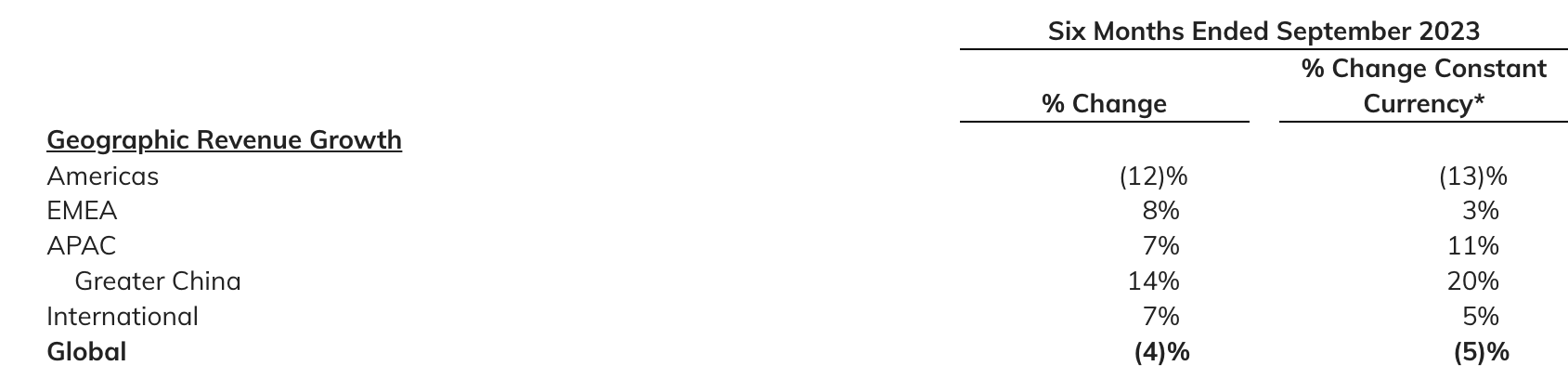

While some apparel companies have been cushioned from the US demand downturn as Chinese demand picked up in the past year, VF Corporation has been unable to benefit from that as well. As it happens, the APAC region accounts for just 13% of the company’s total revenues, with EMEA contributing to the remaining 29% as of FY23.

{kind=link}

There has been a re-adjustment of the geographical market share in H1 FY24 as faster demand growth of 7% in reported terms for the APAC region inched up its share to 14%. In a positive, and perhaps even unexpected turn, revenue growth for the EMEA accelerated even more to 8% at this time, increasing its share to 32%. But these increased shares have come at the cost of a sharper contraction in the Americas market by 12% (FY23: 2%).

This discussion indicates that there's definite hope for improvement. The international revenue, which is ex-Americas, grew by 7% indicating that as the US consumer economy picks up, VFC can get back on the growth

One-off earnings impact

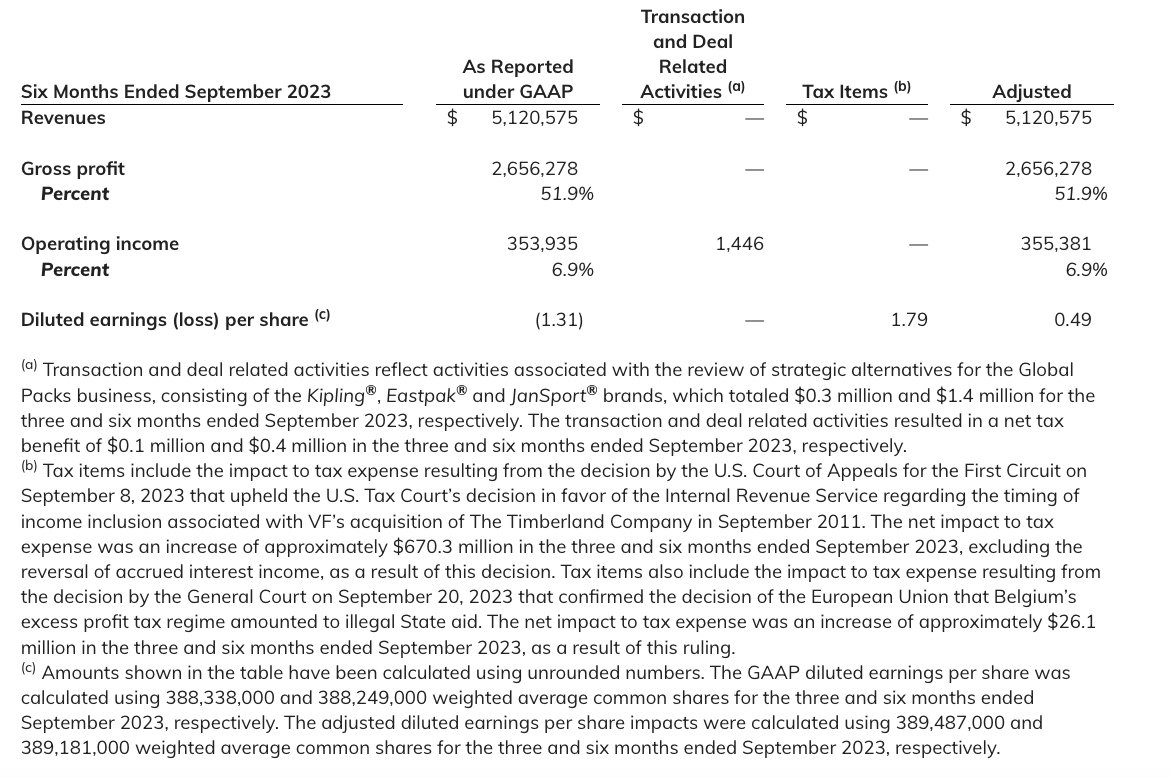

Adding to the company’s demand woes, is the big one-off tax impact, as a result of court rulings related to VFC’s acquisition of Timberland in 2011. The rulings came in September 2023, increasing the tax payable by USD 696 million, which is a substantially higher amount than that paid by the company annually over the past 10 years. This has had an earnings impact of USD 1.79 per share in H1 FY24, resulting in a loss per share of USD 1.31 during the period.

But there are two facts to consider here. First, its adjusted earnings, which exclude the tax impact, is a positive figure of USD 0.49. Even though this is a substantial 39.5% YoY decline, essentially due to smaller revenues, it's still positive profits.

Reconciliation of GAAP and non-GAAP earnings (Source: VF Corporation)

{kind=link}

Second, in reported terms, there has been far less stress on reported operating income compared to last year. In H1 FY22, the company reported an operating loss largely due to impairment and pension settlement charges, which weren’t there in H1 FY23 resulting in healthy operating profits with a margin of 6.9%.

This suggests, much like in the case of revenues, there’s potential for improvement in the company’s earnings, which have been significantly affected by one-off charges for some time now.

Restructuring underway

Moreover, VFC is bringing about some significant changes too. Last June, it brought in a new CEO, Bracken Darrell, who was earlier the CEO of the computer peripherals and software company Logitech, which saw expansion and increased market share under his leadership according to the company’s press release .

VFC has since withdrawn its earlier FY24 guidance and put forth a restructuring program called ‘Project Reinvent’ along with its latest earnings release. This includes changes to the operating model for the Americas in line with the, at least recently, more successful international business.

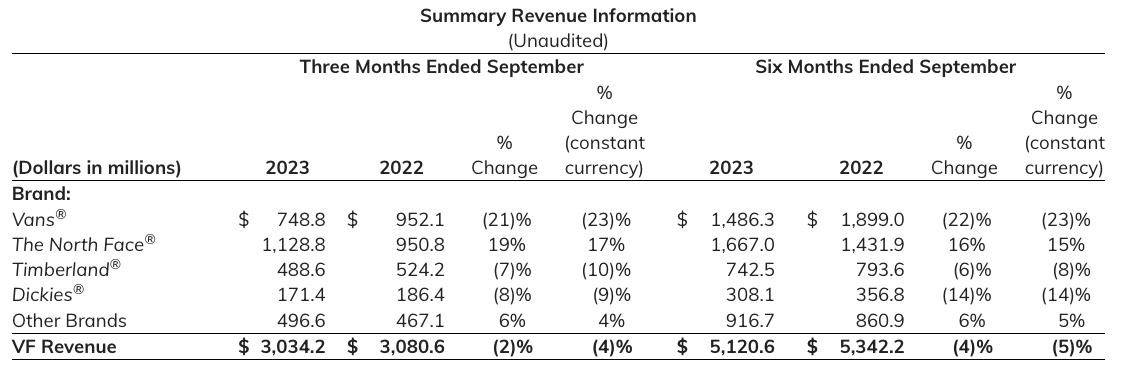

The company also intends to increase focus on the Vans brand, which has seen waning popularity after seeing double-digit growth each year from 2004 to 2019. This is particularly important since Vans was the company’s biggest revenue generator in FY23, but has been losing ground with a 22% revenue decline in H1 FY24.

{kind=link}

The company also intends to reduce fixed costs by USD 300 million. While it doesn’t mention the timeline for this initiative, just to get a sense of what it means, assuming that all of it is implemented in H2 FY24, there would be an 85% increase in operating income, if the income were at the same level as in H1 FY24.

Importantly, VFC also plans on improving its balance sheet. While its net debt to assets ratio at 0.56x isn’t alarming, it wouldn’t hurt to reduce the number. This is especially so since one way of doing this is by reducing the dividend payouts.

With an average dividend payout ratio of 200% over the past five years, it’s unsustainable and a dividend reduction is a step in the right direction. This is even more so considering that VFC’s dividend yield is far higher than the industry average. It has already moved forward on this, with a 70% dividend cut.

Attractive forward P/E

For all its challenges, the stock’s forward non-GAAP P/E for FY24 still looks rather attractive. At 11.3x, it's lower than that for the consumer discretionary sector at 15.8x. It’s also lower than its own past five years’ average of 27.1x. For FY25, it gets even more competitive at 8.8x, as analysts expect a substantial 29% increase in the EPS.

What next?

However, I’d be vary of buying the stock right now. Instead, I’d wait to see the developments when it releases its earnings later in January as it works through its challenges. In particular, I’d look out for any more one-off expenses dragging down the numbers. They have affected earnings in the past two years, and if continued, may well reflect that there’s something more fundamental to the company that needs better management.

I’d also look specifically for how its EMEA sales are progressing. The euro area is in a slump and expected to remain so this year, so if it continues to be the bright light in VFC’s sales figures, clearly the company is getting something right. Next, how far it’s moved forward with the cost savings plan would also be significant, and can reflect in its operating income.

There are positive signs for VFC with its restructuring underway, and good explanations for why it has underperformed recently. But it’s best to wait for some proof of a turnaround before buying the stock. I’m going with a Hold rating.

For further details see:

V.F. Corporation: Too Soon To Count On Restructuring