BKR - Valaris Stock: Revenue And Profit Growth Trends Indicate Undervaluation

2023-07-12 10:26:29 ET

Summary

- It's time to consider investing in offshore drilling service providers, to benefit from the unfolding upcycle, which is still in the early innings. Importantly, another newbuild cycle appears unlikely.

- Leading offshore drilling contractor Valaris may appear expensive when viewed solely through the static lens of traditional valuation multiples such as the P/E and P/B ratios.

- However, the P/E and P/B ratios are ineffective indicators of Valaris' valuation because this is a hyper-cyclical business.

- By focusing on the growth trend of revenue and profits in the foreseeable future, we are able to show that Valaris may actually be significantly undervalued.

Offshore E&P

Although there are still a few remaining under-developed onshore pockets, such as the Alaska North Slope, there is no question that offshore oil provinces, particularly those in deepwater like the Orange Basin in offshore Namibia and South Africa, and the Guyana-Suriname Basin , represent the frontiers for petroleum exploration and development (E&P).

With record free cash flow generated in 2022 by E&P companies, offshore project sanctions are poised to rise in the next two years to the highest level in more than a decade, and offshore upstream capital expenditures (or CapEx) are expected to increase at a compound annual growth rate (or CAGR) of 11% over the next couple of years, as illustrated in Figure 1.

Fig. 1. Offshore upstream CapEx and new project sanctioning (Valaris)

{kind=link}

Offshore drilling

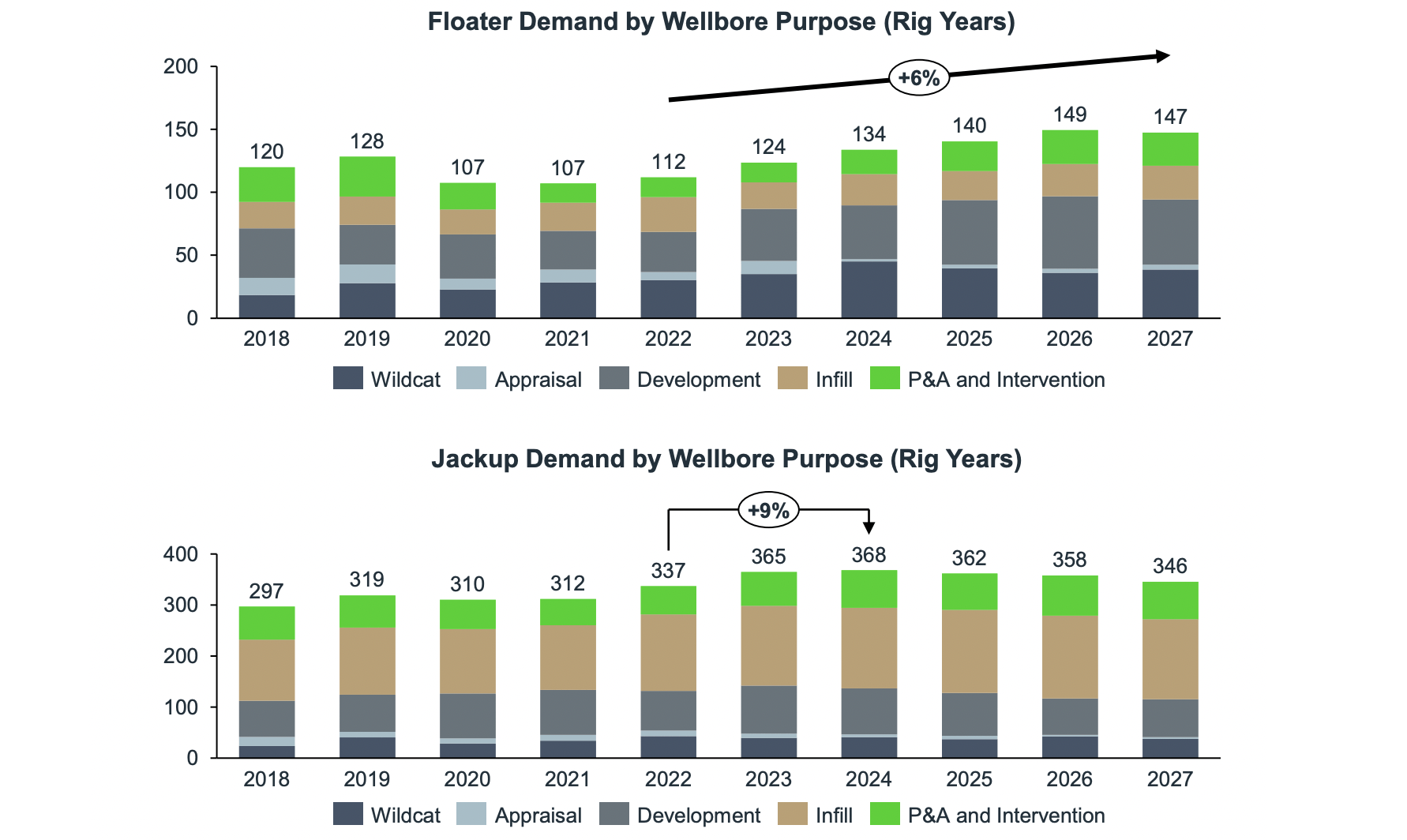

The CapEx of offshore E&P companies represents the revenue of offshore drillers. It is projected that floater demand will increase at a CAGR of 6% over the next five years, while jackup demand is anticipated to increase further in 2023 and 2024 as operators develop shorter cycle barrels, as evident in Figure 2.

Fig. 2. Demand for offshore drilling over the next several years (Valaris)

{kind=link}

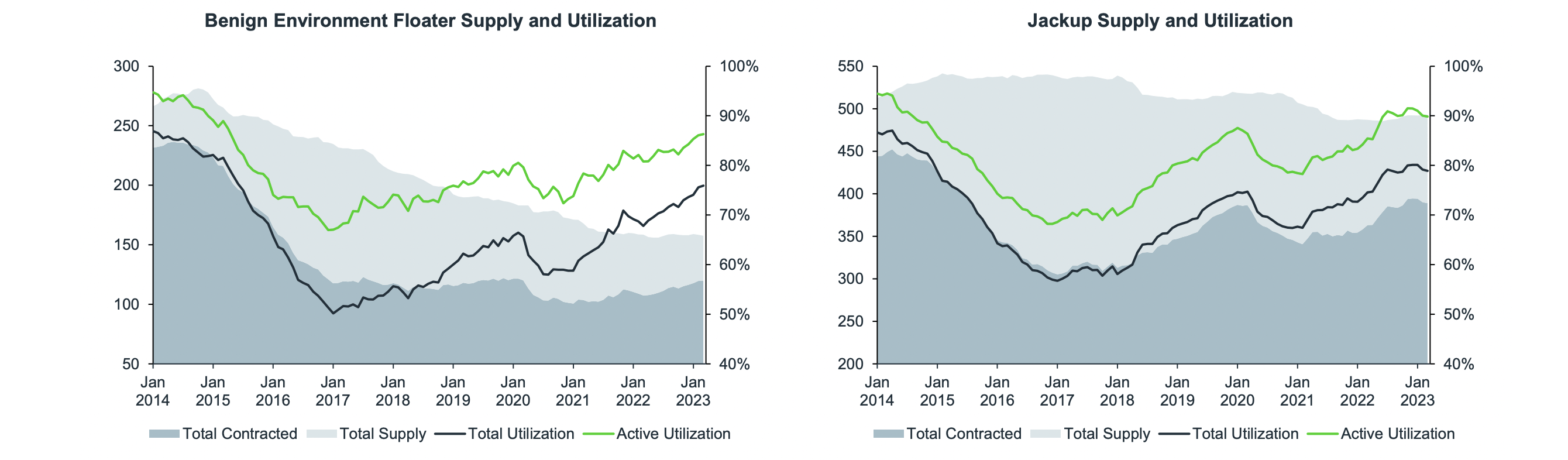

On the supply side, the capacity of offshore drilling has reached a low level after nine years of decline since the end of the previous oil peak in 2014. As demand has risen since the Covid bottom in early 2020, contracted rigs have continued to increase, leading to a continual rise in utilization, as shown in Figure 3. The active utilization rates for drillships, benign environment semi-submersibles, harsh environment jack-ups, and benign environment jack-ups have reached 94%, 77%, 85%, and 91%, respectively. The supply-demand dynamic appears to be extremely bullish for offshore drillers.

Fig. 3. Offshore rig supply and utilization, benign environment floaters and jack-up rigs (Valaris)

{kind=link}

Offshore driller's newbuild cycles

A laudable approach to capitalize on the deepwater E&P trend, therefore, would be to invest in a pick-and-shovel play, such as a deepwater drilling service provider.

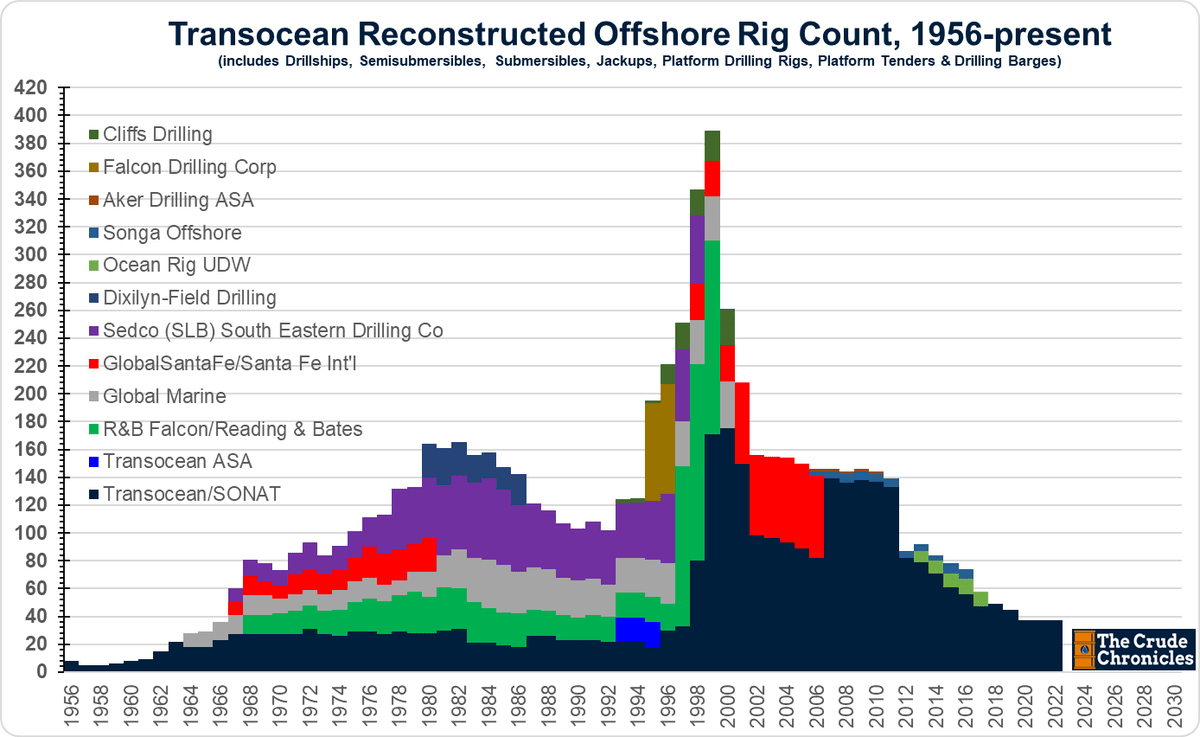

However, offshore drillers have gained notoriety for their newbuild cycles, which have periodically disrupted the industry's capital efficiency and profitability, leading to occasional bankruptcies. This pattern is evident in the reconstructed history of Transocean's ( RIG ) offshore rig count, particularly during the last oil up-cycle from the late 1990s to 2014, as shown in Figure 4.

Fig. 4. The reconstructed offshore rig count of Transocean, 1956 to date (The Crude Chronicles)

{kind=link}

As an investor, you may adhere to the belief that " there is nothing new under the sun " in this cycle. However, you may have also heard the saying, " No man ever steps in the same river twice, for it's not the same river and he's not the same man. "

The inevitable truth is that offshore drillers have not been investing heavily in reactivating stacked rigs or in newbuilds, which suggests that another newbuild cycle is unlikely.

- There are only 10 competitive warm or cold stacked drillships remaining, and eight newbuild drillships are still in South Korean shipyards. These 18 floaters are expected to enter the market in a staged manner.

- Out of approximately 100 warm or cold stacked jack-ups, 65 are older than 30 years, and 60 have been stacked for longer than three years, leaving only a small percentage of them as competitive future entrants into the market. Among the 18 newbuild jack-ups in shipyards outside of the ARO newbuild program, about 13 are located in Chinese shipyards and are most likely intended for future use in the local market.

Therefore, the likelihood is high that the offshore drilling market will favor service providers. This justifies an investment by retail investors in offshore drillers.

Offshore drillers: the competitive landscape

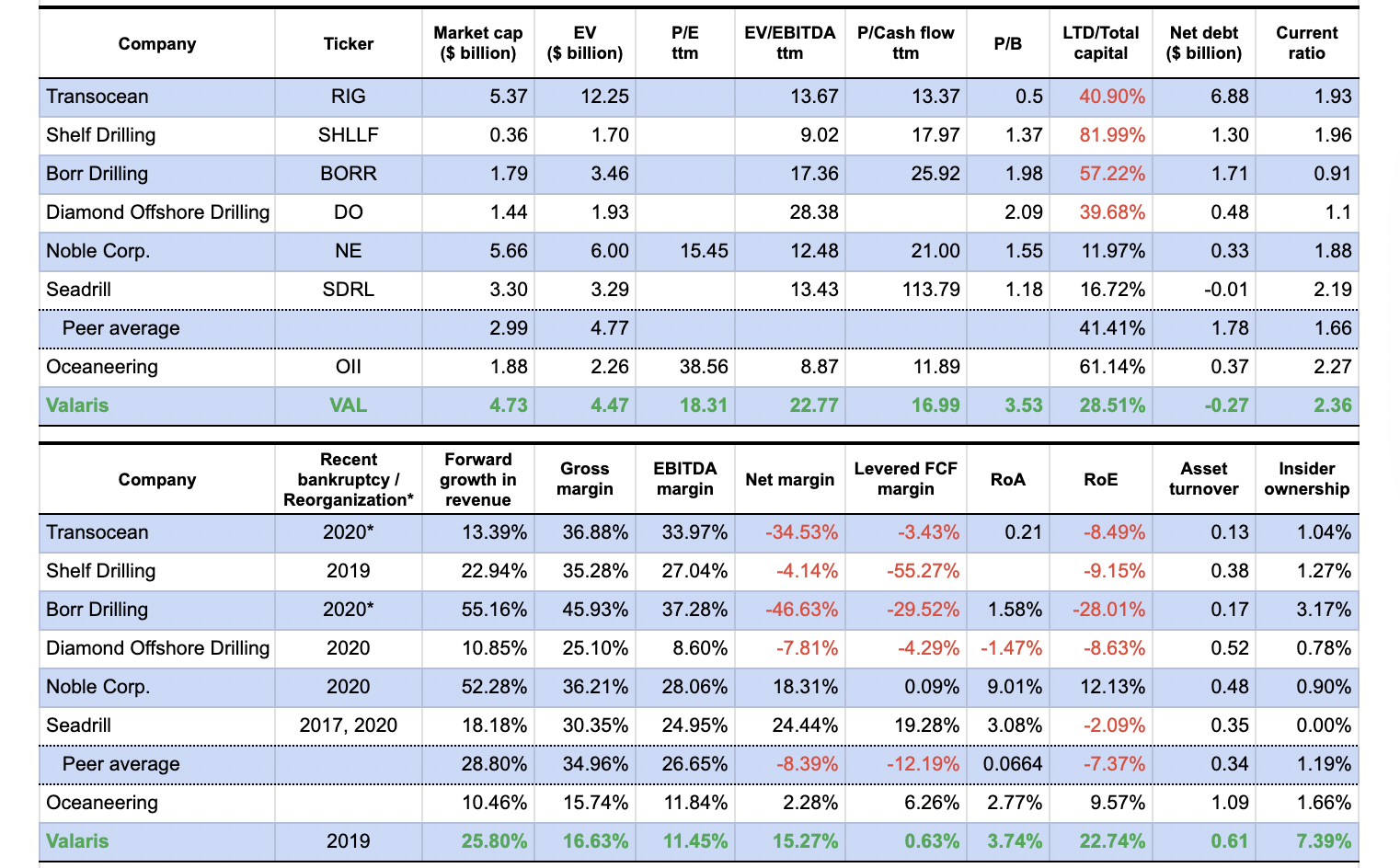

The offshore drilling industry is highly competitive, with seven major players. The list includes Noble Corp. ( NE ), Transocean ((RIG)), Valaris ( VAL ), Seadrill ( SDRL ), Borr Drilling ( BORR ), Diamond Offshore Drilling ( DO ), and Shelf Drilling ( SHLLF ), arranged in descending order of market capitalization as presented in Table 1. Additionally, for the purpose of comparison, Oceaneering ( OII ), the leading provider of remotely operated vehicles (ROVs) which I recently covered, is also included.

Table 1. Basic information on major offshore drilling contractors, with Oceaneering included for comparison purposes (compiled by Laurentian Research for The Natural Resources Hub based on Seeking Alpha data)

{kind=link}

I especially like Valaris among the offshore drillers for reasons detailed below.

Valaris business overview

Headquartered in Houston, Texas, and incorporated in the UK, Valaris is an offshore drilling contractor. In 2019, the company, formerly known as ENSCO, merged with Rowan Companies and rebranded itself as Valaris. In August 2020, Valaris filed for a prearranged bankruptcy and successfully emerged from bankruptcy in May 2021.

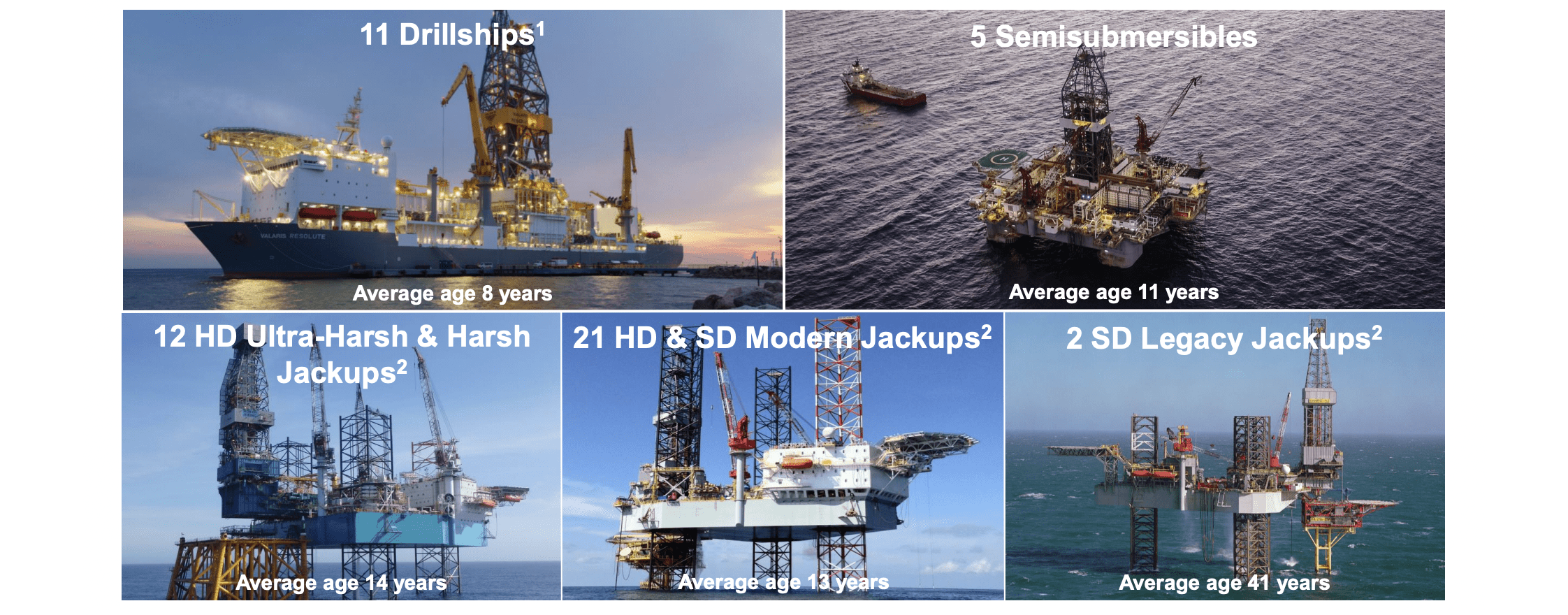

Fleet

Valaris has a fleet that includes 11 drillships with an average age of 8 years, 5 semisubmersibles with an average age of 11 years, and 35 jackups (33 heavy-duty with an average age of 13-14 years and two standard-duty with an average age of 41 years), as shown in Figure 5. The fleet has a gross asset value of over $9 billion as of April 2023.

Fig. 5. The fleet of drilling rigs of Valaris (modified from Valaris)

{kind=link}

Valaris currently has two high-specification drillships (Valaris DS-7 and DS-11) that are stacked. Additionally, Valaris has the option to purchase two newbuilds (Valaris DS-13 and DS-14) before the end of 2023, with an approximate purchase price of $119 million and $218 million, respectively.

Valaris also holds a 50% stake in ARO Drilling, a joint venture with Saudi Aramco. ARO currently operates a fleet of 15 jackup rigs, with eight owned by Valaris and leased to ARO through bareboat charter agreements. ARO plans to construct 20 additional jackup rigs over the next 10 years, with two newbuild rigs set to be delivered in 2023.

Valaris, a cyclical business

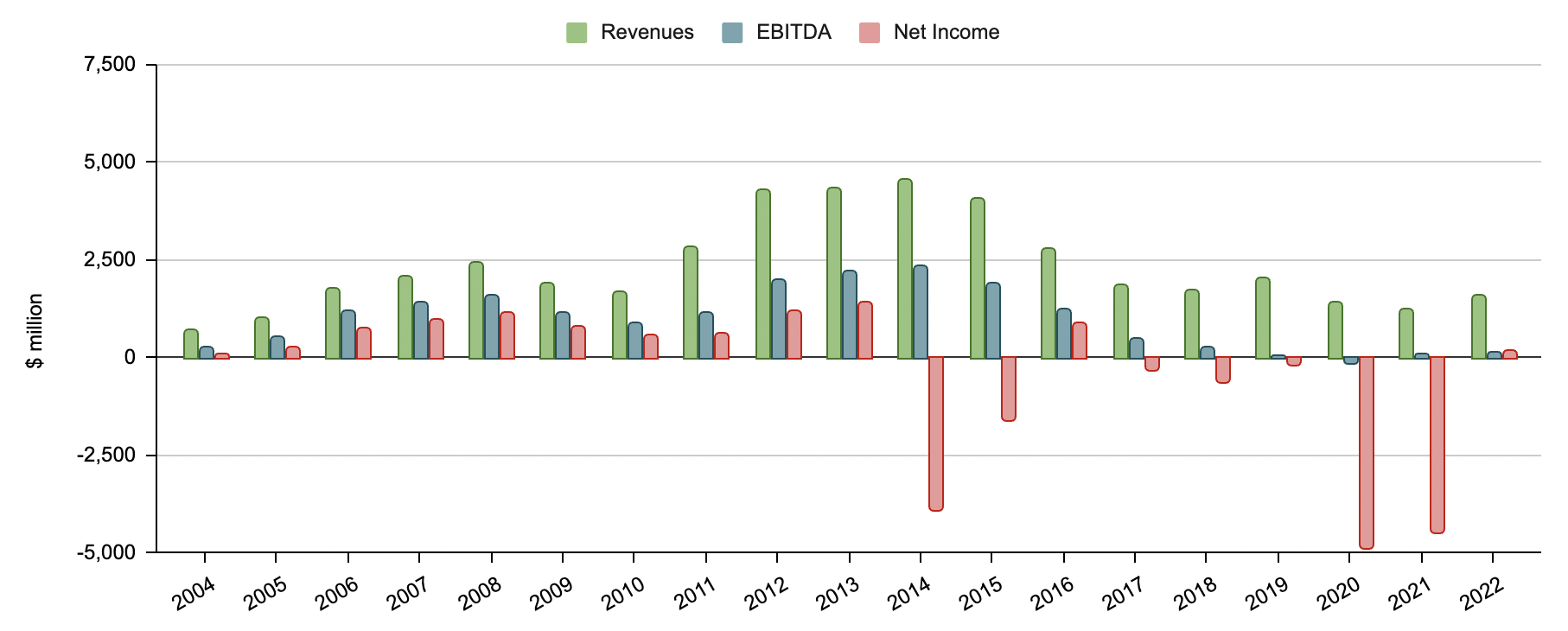

Offshore drilling is a quintessential cyclical industry, and Valaris experiences cyclical fluctuations in revenue and profit in line with the state of the offshore drilling industry. During the previous upcycle from 2004 to 2013, its revenue multiplied by 6.1X, EBITDA by 8.8X, and net income by 15.2X, as illustrated in Figure 6.

From 2013 to 2021, during a severe downcycle in the offshore drilling industry, Valaris experienced a substantial decline in revenue by 71.5%, EBITDA by 96%, and net profit from a positive $1.4 billion to a loss of $4.9 billion. It is evident that the offshore drilling industry reached its cyclical bottom between 3Q2020 and 1Q2022, and has started to recover since then, albeit still in the early stages. This recovery is supported by data presented in Figure 7.

Fig. 6. Revenue, EBITDA and net income of Valaris and its predecessor (Laurentian Research for The Natural Resources Hub, based on data from Valaris and Seeking Alpha) Fig. 7. Quarterly revenue, adj EBITDA and net income of Valaris (Laurentian Research for The Natural Resources Hub, based on data from Valaris and Seeking Alpha)

{kind=link}

{kind=link}

P/E ratio

According to Peter Lynch, for successful investment in cyclicals, one should "invest in cyclicals at their nadir" and then, "just when it seems that things can't get any worse with these [cyclical] companies, things begin to get better." He particularly emphasized that the price/earnings ratio of a cyclical business can significantly mislead an investor.

" Conversely, a high p/e ratio, which with most stocks is regarded as a bad thing, may be good news for a cyclical. Often, it means that a company is passing through the worst of the doldrums, and soon its business will improve, the earnings will exceed the analysts' expectations, and fund managers will start buying the stock in earnest. Thus, the stock price will go up. "

As of July 7, 2023, Valaris had a P/E multiple of 19.38X and an EV/EBITDA multiple of 24.18X on a trailing twelve-month basis. These multiples may seem extremely high, as pointed out by some fellow Seeking Alpha authors. However, as Lynch indicated, such high multiples may actually be good news because they are a precursor indicator of business improvement and share price appreciation.

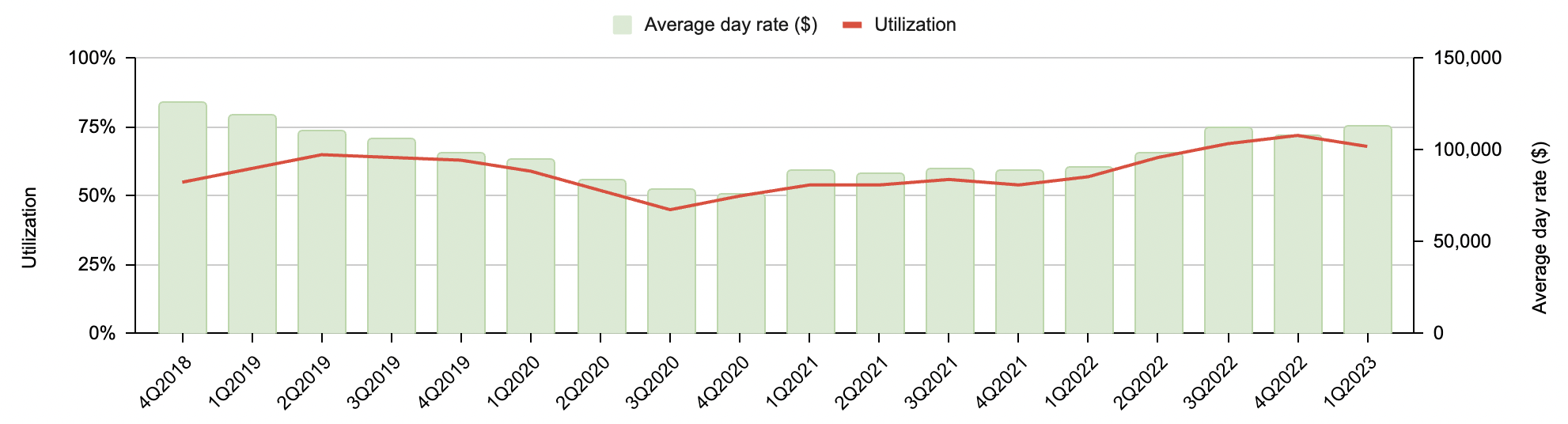

Indeed, rig utilization has been trending towards improvement since the 3Q2020, as depicted in Figure 8. The recent decline in utilization from the 4Q2022 to the 1Q2023 appears to have been caused by heavy-duty ultra-harsh and harsh jackups alone, as floaters and all other jackups continued to show a general uptrend in rig utilization, as seen in Figure 9. The increase in utilization has been accompanied by a steady improvement in average day rate. It seems that the business has just come out of a "nadir" and is in the early phase of a cyclical improvement.

Fig. 8. Quarterly average day rate and utilization of Valaris (Laurentian Research for The Natural Resources Hub, based on data from Valaris and Seeking Alpha) Fig. 9. Valaris' utilization by rig type (Laurentian Research for The Natural Resources Hub, based on data from Valaris and Seeking Alpha)

{kind=link}

{kind=link}

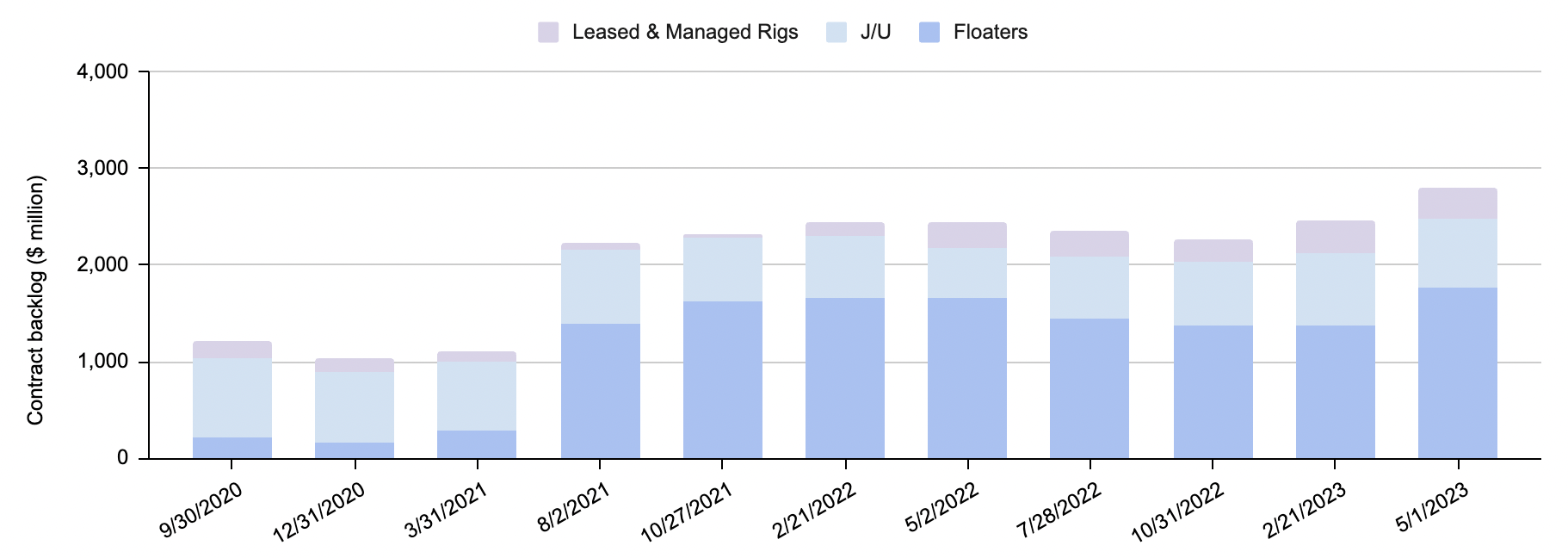

Contract backlog confirms that offshore drilling market has begun to improve, as shown in Figure 10. As of May 1, 2023, Valaris stated that it had accumulated $2.8 billion of contract backlog, which can support 1.6 years of operation on a 1Q2023 run rate basis. Therefore, it appears that now is a time that Peter Lynch would buy offshore drilling stocks.

Fig. 10. Contract backlog of Valaris, for floaters, jackups and leased and managed rigs (Laurentian Research for The Natural Resources Hub, based on data from Valaris and Seeking Alpha)

{kind=link}

P/B ratio

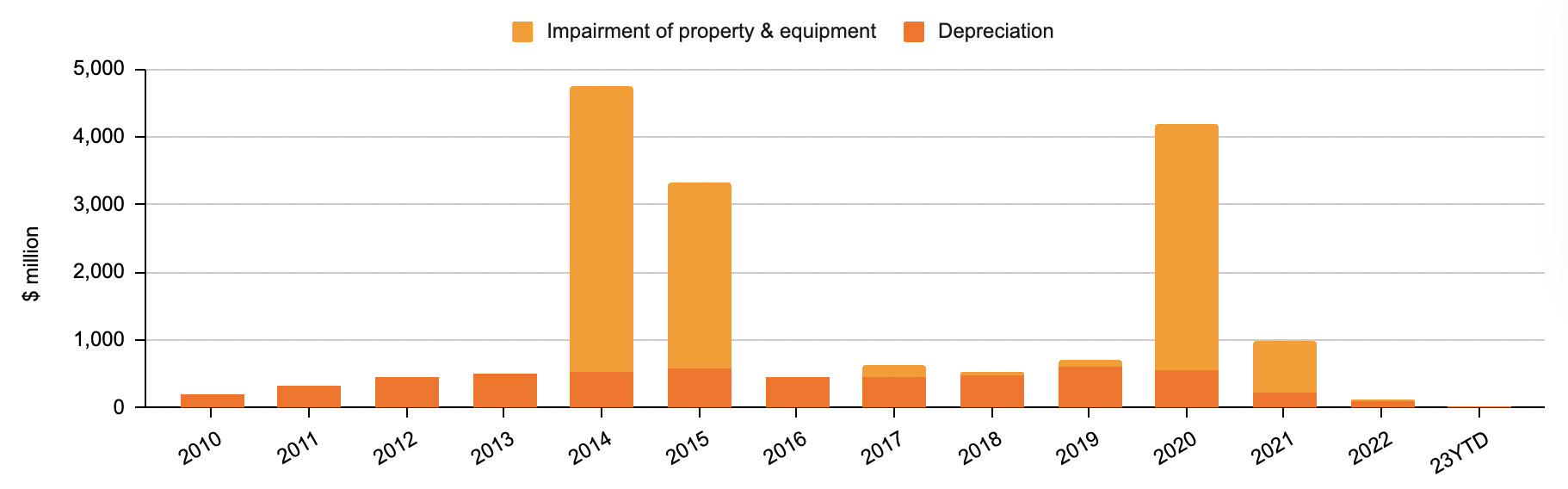

Since 2014, Valaris has recorded pre-tax, non-cash losses on impairment of long-lived assets totaling approximately $9.0 billion. In the first two years (2014 and 2015) following the previous oil bull market, around $7.0 billion in pre-tax, non-cash impairments related to rigs were recorded. In the first half of 2020, an aggregate of approximately $3.6 billion in pre-tax, non-cash impairments related to floaters, jackups, and spare equipment were recorded, as illustrated in Figure 11. These substantial pre-tax, non-cash impairments resulted in significant changes in total equity and total assets, as shown in Figure 12.

Fig. 11. Impairment of property and equipment, and depreciation (Laurentian Research for The Natural Resources Hub, based on data from Valaris and Seeking Alpha) Fig. 12. Total equity and total assets (Laurentian Research for The Natural Resources Hub, based on data from Valaris and Seeking Alpha)

{kind=link}

{kind=link}

Such significant fluctuations in long-term assets and equity diminish the usefulness of another valuation multiple, the p/b ratio. As of July 7, 2023, Valaris had a P/B ratio of 3.73X, which may make the stock appear expensive compared to oilfield service giants Schlumberger ( SLB ), Halliburton ( HAL ), and Baker Hughes ( BKR ), with ratios of 4.21X, 3.81X, and 2.28X, respectively.

However, as the offshore drilling upcycle continues, the asset value of Valaris is expected to be significantly revised due to the reactivation of stacked rigs and revaluation of property and equipment, which is the opposite of the pre-tax, non-cash impairments recorded during the bear market.

Currently, Valaris has a book value of only $1,342 million. However, the company is estimated to have a gross asset value of over $9 billion. This results in a forward P/B ratio of 0.57X, which is not considered expensive anymore.

Investor takeaways

A multi-year offshore drilling upcycle appears to be unfolding, driven by increased investment in offshore exploration and production, coupled with limited rig supply and the absence of a newbuild cycle. Therefore, it is now an opportune time for resource investors to consider investing in offshore drilling contractors.

A survey of selected offshore drillers suggests that Valaris stands out with a promising growth outlook, ample liquidity, no long-term debt, and a net cash position of $257 million (Table 1).

This study has demonstrated that traditional valuation multiples such as the P/E and P/B ratios are ineffective indicators and should not be relied upon. Instead, by focusing on the growth trend of revenue and profits in the foreseeable future and their impact on forward valuation multiples, Valaris appears to be extremely undervalued. Investors may want to consider purchasing Valaris stock around $60 per share (Figure 13).

Fig. 13. Stock chart of Valaris, dividend back-adjusted, as compared with VanEck Oil Services ETF ((OIH)) (modified from Barchart and Seeking Alpha)

{kind=link}

For further details see:

Valaris Stock: Revenue And Profit Growth Trends Indicate Undervaluation