STLD - Vale: Brazilian Mining Giant Potentially Undervalued And Offering +8% Dividend Yield

2023-07-21 13:41:09 ET

Summary

- Despite facing logistical challenges in Q1 2023, Vale S.A.'s production exceeded expectations, indicating strong potential for future growth.

- The company's low leverage ratio, strong cash generation, and exposure to China's recovery make it an attractive investment opportunity.

- The low P/E ratio and potential for EPS and multiples expansion in the near term also indicates that the stock may be undervalued.

- The net debt to EBITDA ratio of 0.5x is significantly low, enabling high dividend distributions. Over the past 4 years, Vale has maintained an average dividend yield of 8%.

Investment thesis

Despite facing logistical issues in the first quarter of 2023, which impacted sales and revenue, the production of Vale S.A. ( VALE ) actually exceeded my expectations and now indicates a strong potential for future quarters. In my view, the combination of the company's solid revenue generation capacity, low leverage ratio, and attractive valuation make it a great opportunity at the moment.

Even though Vale's business is directly and mostly related to iron ore, which naturally poses volatility risks to the company, it's doing a great job diversifying its portfolio by including other commodities. Regardless of that, I feel that its business model is rock solid (pun intended) and that investing in it still has more pros than cons, especially at the current share price.

Thesis enablers

My bullish view on Vale is also supported by the following factors:

1. Production Recovery: Vale's production is expected to recover throughout the year, and the company has maintained its production guidance of 315 million tons. The period of operational difficulty caused by logistical issues in the Sistema Norte is likely to be resolved, setting the stage for increased sales volume and revenue.

2. Exposure to China's Recovery: Vale is well-positioned to benefit from China's recovery, as the country has reopened and is expected to continue its investments in construction and industrial parks. This favorable environment supports the sale of Vale's main product, iron ore, which continues to trade at a high price.

3. Strong Cash Generation: Vale's low level of debt and robust cash flow generation contribute to its financial strength. The company's net debt to EBITDA ratio of 0.5x is significantly low, enabling high dividend distributions. Over the past four years, Vale has maintained an average dividend yield of 8%, and it is expected to continue rewarding shareholders in 2023.

4. Attractive Valuation: Vale has a price-to-earnings (P/E) ratio of 4.35x, lower than both Vale's 5-year average and the sector median, indicating that the stock is possibly undervalued. A valuation forecast also shows that the stock has potential for EPS and price multiples expansion.

5. Diversification and Decarbonization: Vale's diversification into other minerals, such as nickel and copper, positions the company to benefit from the transition to a greener economy. As decarbonization measures increase the demand for high-quality ore, Vale's status as a major producer of these essential minerals seems to be going unnoticed by the market, offering additional growth potential.

{kind=link}

A brief description of Vale's strengths and weaknesses

Vale S.A. is a Brazilian multinational mining company headquartered in Rio de Janeiro, Brazil. It is one of the largest mining companies in the world and a significant player in the global mining industry. Vale primarily focuses on the extraction and production of iron ore, but it is also involved in the mining of other minerals, including nickel, copper, coal, and precious metals. This diversification helps mitigate risks associated with fluctuations in commodity prices and allows Vale to leverage its expertise and operational capabilities across multiple segments of the mining industry.

One of Vale's primary strengths lies in its extensive reserves of high-quality iron ore. The company operates large-scale mines in Brazil, including the Carajás complex, which is considered one of the world's richest iron ore deposits. This abundant resource base enables Vale to maintain a significant market share and meet the growing demand for iron ore, particularly from emerging economies like China.

The company has established strategic relationships with global customers, including steel producers, who rely on its reliable supply of iron ore. Moreover, Vale has developed an extensive logistical infrastructure, including railroads, ports, and terminals, facilitating the efficient transportation of its products to global markets.

Vale's operations have not been without controversy. In January 2019, one of its iron ore tailings dams, known as the Brumadinho Dam, collapsed in Brazil, leading to a tragic disaster with a large number of fatalities and significant environmental damage. This incident raised concerns about the safety and environmental practices of the mining industry in Brazil and led to increased scrutiny of Vale's operations.

To address its weaknesses, Vale has taken steps to improve its safety and environmental practices. It has invested in strengthening its dam infrastructure, implementing stricter safety protocols, and enhancing environmental monitoring systems. Vale is also engaging with stakeholders and communities to rebuild trust and improve its social and environmental performance.

Assessing last quarter's results

According to the results of the last quarter (Q1 2023), Vale had a profit of R$ 9.5 billion, a good outcome but below market expectations. The reported numbers were impacted by logistical issues that occurred in the company's Sistema Norte, specifically at the Porto da Madeira. Due to heavy rains in the region, the company was unable to fully realize its sales potential, as previously disclosed in the sales and production report on April 18, 2023. However, the production exceeded expectations, which creates solid ground for high figures in the coming quarters. The result was in line with what I was expecting, with the company reporting a net profit of R$ 9.5 billion and a strong generation of operating cash flow.

The company's revenues amounted to R$ 43 billion, a 22% decrease compared to the first quarter of the year before, a result that, in my opinion, was primarily influenced by two factors. Firstly, as previously mentioned, the volumes of iron ore sold were 10% lower than in Q1 2022. Secondly, the average price of iron ore during the period was US$ 108.6 per ton, lower than the US$ 141.4 per ton recorded in the first quarter of the previous year. Despite these lower figures compared to 2022 and not selling its full production capacity during the period, I truly believe this situation will be resolved throughout the year as the company demonstrates a robust revenue generation capacity.

A concern to me is that the cost of goods sold by the company has increased by 5% (for a total of R$ 25 billion) in Q1 2023, compared to the same period last year. The rise in costs per ton is primarily attributed to reduced sales from the Sistema Norte, which faced issues with Porto da Madeira. It is worth noting that this region is supposed to have lower production costs for Vale, being a newer operation. However, it is somewhat reassuring to see that overall expenses remained in line with the same period last year, at R$ 2.5 billion, indicating some level of cost control within the company. Nonetheless, it will be important for Vale to address the issues affecting sales and production in the Sistema Norte to ensure more stable and efficient operations moving forward.

As a result, Vale's operating cash flow (EBITDA) for the period was R$ 18.4 billion, 42% lower than Q1 2022. I feel it's important that I mention that Vale's figures include a backlog of iron stock due to logistical issues that prevented the company from completing its sales entirely. However, just like I stated my optimism before, this is expected to be resolved throughout 2023. Nonetheless, the result is still pretty good, leaving the company trading at around 4x EV/EBITDA for 2023. Furthermore, what stands out the most is that, despite the challenges faced, the organization continues to generate significant cash flow.

In my view, it comes as good news to me that the company's net debt remained consistent at R$ 42 billion compared to the previous year, indicating a stable leverage position. With a net debt to EBITDA ratio of 0.5x, Vale maintains a very low level of leverage, which provides the flexibility for generous dividend distributions. It is also worth mentioning that the company's capex remained unchanged at R$ 6 billion year-over-year, reflecting a consistent investment strategy. Additionally, there was a variation of R$ 2 billion in depreciation, which may indicate adjustments in asset values.

The free cash flow generated by the company was R$ 18.3 billion, 38% higher than the previous period's figure, which is somewhat surprising considering the logistical issues mentioned. According to Executive Vice President of Finance Gustavo Pimenta , it "was positively impacted by working capital as we had a strong cash collection from Q4 sales, as we anticipated last quarter. This effect was partially offset by transitory inventory build-up and seasonal disbursements related to profit sharing in the first quarter."

As we can see from the graph below, the company's working capital had a positive balance of R$ 4.5 billion this quarter, also impacted by a variation in accounts receivable of R$ 9 billion.

{kind=link}

Finally, the company reported a net profit of R$ 9.5 billion, 58% lower than the same period last year, which had very high iron ore prices. In my view, this decline was already expected by the market, but the numbers are still solid.

My forecasts and share valuation

Vale's production was above expectations and is expected to achieve a higher sales volume throughout the year, a recovery that was not fulfilled in the first quarter due to logistical issues. The production guidance of 315 million tons was maintained, and I feel that the period of greatest operational difficulty for the company has already ended. Additionally, it is important to remember that the first quarter is marked by heavy rainfall, which makes the company's activities more challenging.

The logistical issues in Vale's Sistema Norte affected the results of the first quarter of 2023, and for that, the figures presented were slightly below what I was expecting. Anyway, I take this result as a good one, considering that the company had a strong cash generation and maintains a low level of debt.

Considering all that, I maintain my opinion that Vale's shares are a great buy at the moment. The company is exposed to China's recovery, as the country has recently reopened and is expected to continue its investments in construction and industrial parks to accelerate growth. This favors the sale of Vale's main product, iron ore.

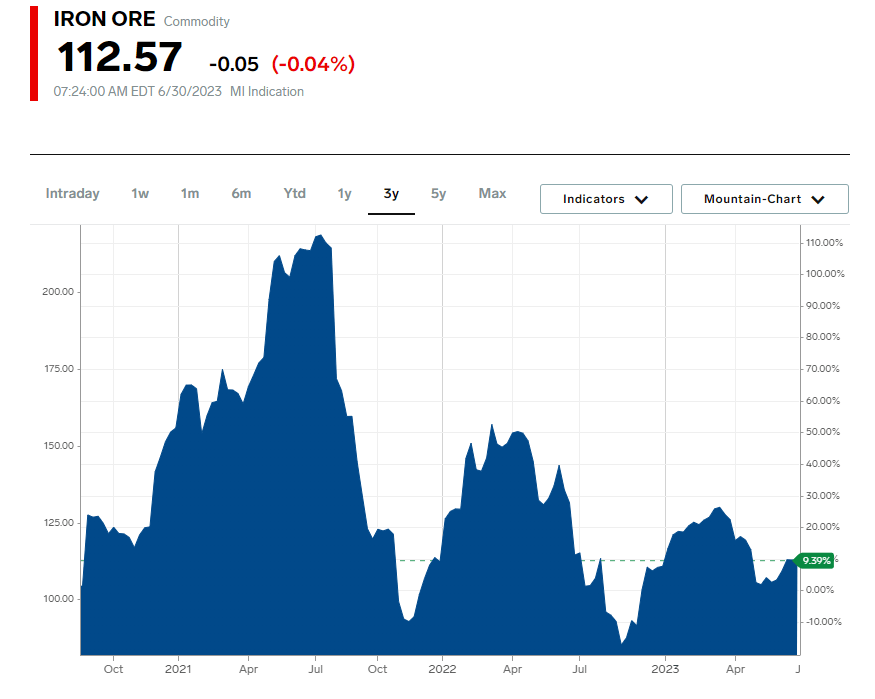

On the other hand, iron ore continues to trade at a high price, sitting around US$112.57 per ton, as I write this article. Also, the combination of the commodity curve and the USDBRL pair at around R$ 4.79 allows Vale to maintain strong cash generation. Additionally, in a world struggling to control inflation, leading companies in the commodities space with dollar-denominated revenues offer good portfolio protection.

Iron Ore price chart (markets.businessinsider.com)

{kind=link}

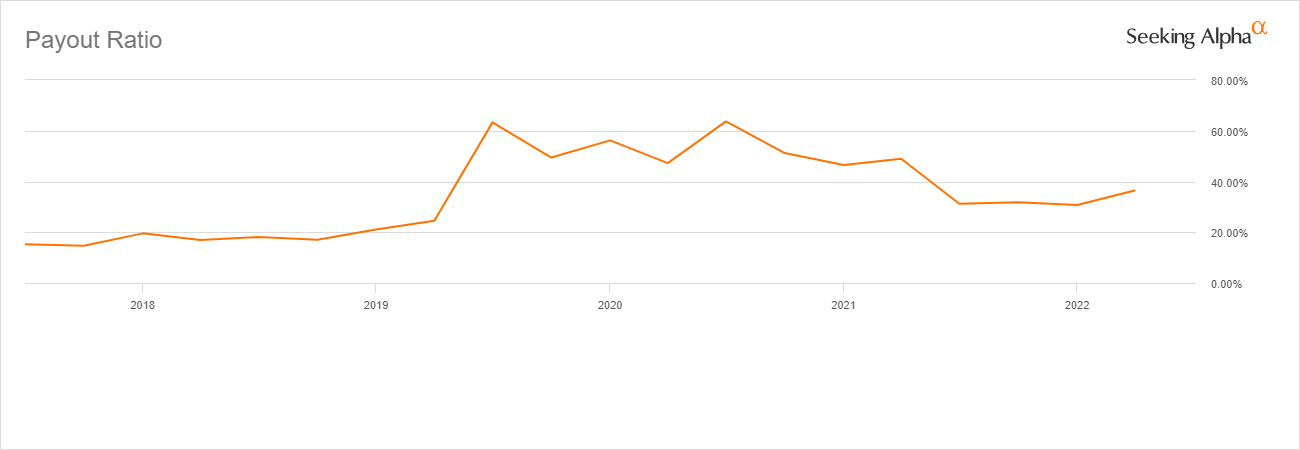

As Vale has low debt, it is expected to be among the major dividend payers. Based on the current market price, the average Dividend Yield of the company over the past four years has been 8%, and my expectation is that shareholder remuneration for the few years ahead will be at least around that figure. This is because the company's payout ratio is currently sitting at 36% and in the past it barely went above 60%. So, even if Vale maintains the same payout level as now, the prospects of increasing EPS will guarantee that investors will have their fair share of dividends.

Vale's payout ratio history (Seeking Alpha)

{kind=link}

Regarding the company's valuation, for the calculations, I'll consider a conservative and realistic long-term ore price of US$ 80 and a discount rate of 15%. This discount rate is taking into account two risk-free rates from the Brazilian Treasury , which are the Selic rate sitting at 13.75% and the rate for the bond expiring in 2026 at 10.19%, thus a premium above both rates for the medium term. Below is a quick forecast of the major indicators:

| 2022 |

| 2023 |

| 2024 |

| 2025 |

| EV/EBITDA |

| 2.1x |

| 3.4x |

| 3.7x |

| 3.6x |

| P/E |

| 3.0x |

| 5.0x |

| 5.5x |

| 5.6x |

| Div. Yield |

| 18.8x |

| 9.2x |

| 8.9x |

| 8.0x |

| EPS |

| R$ 0.95 |

| R$ 2.80 |

| R$ 2.52 |

| R$ 2.50 |

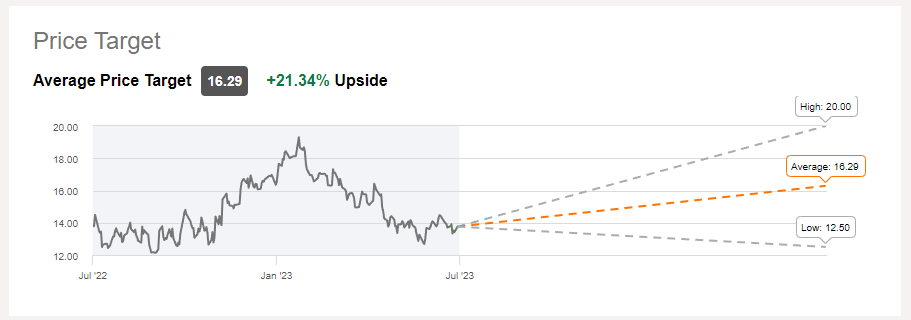

Now, considering that the stock is currently trading at approximately 4x EV/EBITDA, cheaper when compared to peers in the sector, and that the projections show a significant EPS expansion, I keep my buy recommendation for Vale. This estimate is also in line with Wall Street analysts, who set an average target price of US$ 16.29 and an optimistic share price of US$ 20 for the company, providing both +21.43% and +49%, respectively.

Wall Street analysts' price targets for Vale (Seeking Alpha)

{kind=link}

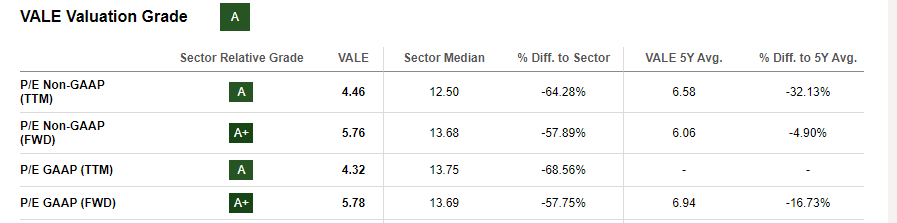

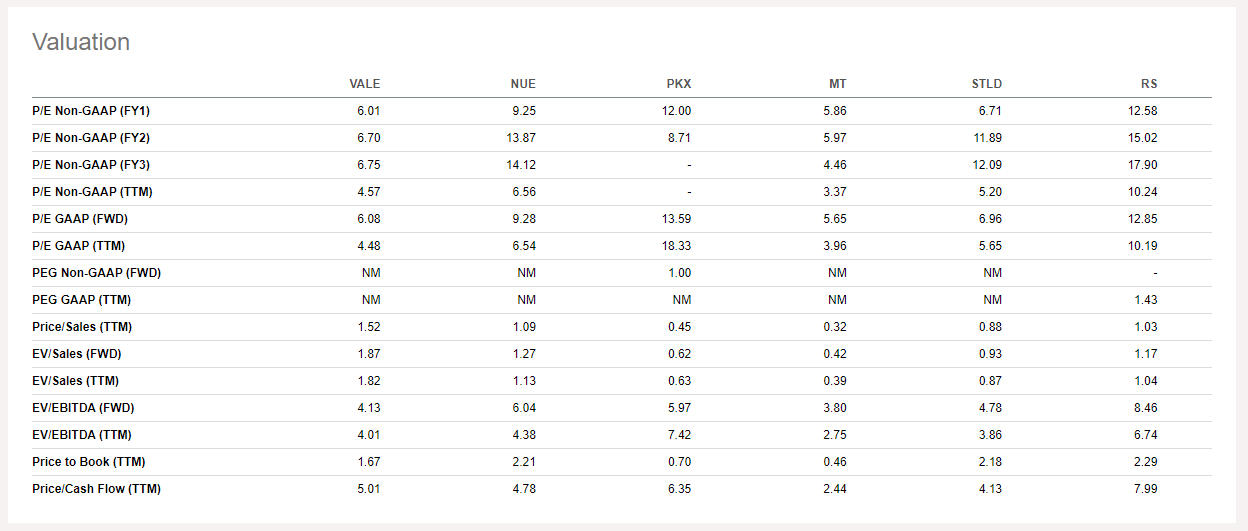

On top of that, the company currently has a low P/E ratio ((FWD)) of 5.76x, which is lower than both Vale's 5-year average and the sector median (see images below), indicating that the share might be undervalued and that the market is also expecting EPS growth for the next fiscal year. For the sector median, as we can see from the second table below, we are comparing those price ratios to companies such as Nucor Corporation ( NUE ), POSCO Holdings Inc. ( PKX ), ArcelorMittal S.A. ( MT ), Steel Dynamics, Inc. ( STLD ), and Reliance Steel & Aluminum Co. ( RS ).

Seeking Alpha Vale's valuation ratios against peers in the sector (Seeking Alpha)

{kind=link}

{kind=link}

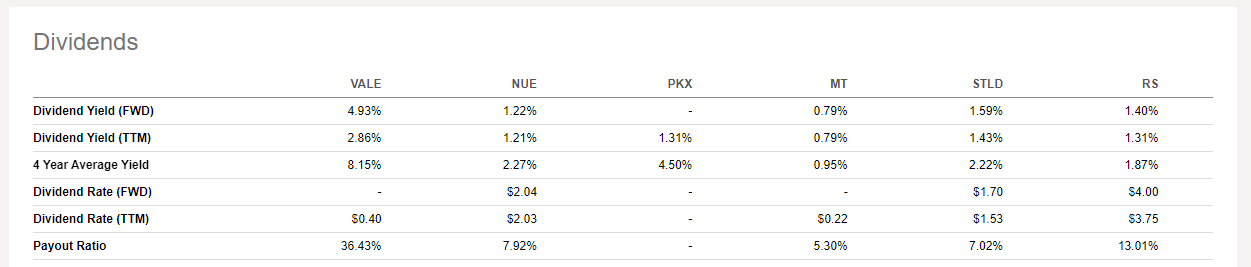

On top of that, we have to remember that dividends are also a crucial part of investment return. Again, if we compare dividend multiples against the same peers as before, we see that Vale is also winning the race of distributions, with a Dividend Yield ((FWD)) of 4.93% and a 4-year average of 8.15%, both 3 to 4 times higher than the others. We also have to remember that the Dividend Yield indicator can also be approached as a price multiple, after all, sometimes a company is not necessarily distributing more, but its share price is relatively cheaper than the amount of dividends paid. The table below shows again that, whether you are looking for discounted or high-paying stocks, Vale might be a great option now.

Vale's dividend ratios against peers in the sector. (Seeking Alpha)

{kind=link}

In summary, I believe Vale has an upside potential in the medium term and that it's a top pick in its sector in Brazil because of its high-quality ore, production costs below the global industry average, and low debt.

The main risk for the investment thesis

Apart from the natural risk inherent to Vale's business, which is related to the volatility of commodities, there is also the China problem. China, the company's largest importer, uses iron ore mainly for real estate development. The thing is, China still hasn't recovered and fully reopened after Covid, so the country's economy is still slowly getting back on track.

Considering the uncertainties about Chinese growth and a weakened global economy, which directly impact the iron ore price, there is a chance of Vale having a lower annual revenue in 2023. So, the scenario we want in order to mitigate these risks and make sure Vale delivers a great result involves an improvement in Chinese demand, which might happen if the government manages to stimulate the economy, mainly through interest rate cuts. On top of that, a faster-than-expected slowdown in inflation in other major economies would definitely be beneficial, as those economies would also drive the iron ore price up to meet their demands.

Final words

In conclusion, Vale S.A. remains a strong contender in the global mining industry despite facing challenges and setbacks. The company's extensive reserves of high-quality iron ore, strategic relationships with global customers, and robust logistical infrastructure provide it with a competitive advantage. Furthermore, Vale's diversification into other minerals helps mitigate risks associated with commodity price fluctuations.

Analyzing the last quarter's results, Vale experienced logistical issues that impacted sales and revenue, primarily due to heavy rains in the region. However, the company's production exceeded expectations, indicating the potential for strong figures in the upcoming quarters. Despite lower figures compared to the previous year, Vale's solid revenue generation capacity, cheap valuation, and low leverage ratio position it well for future growth, which is why I consider it a strong buy at the moment.

In the short term, its share price will probably move according to Chinese perspectives, alternating between a possible reopening and lockdowns. However, I believe that the commodity's price has found support around $80, even with significant pessimism regarding China's economy. Furthermore, with few investments to be made and strong cash generation, the company has become a good dividend payer.

In the medium/long term, decarbonization measures are expected to benefit the company by increasing premiums for high-quality ore. Additionally, Vale is a major producer of nickel and copper, essential minerals for the transition to a greener economy, and we believe that the market seems to overlook this segment.

For further details see:

Vale: Brazilian Mining Giant Potentially Undervalued And Offering +8% Dividend Yield