XOM - Valero: The More It Drops The More I Buy

2023-05-12 12:08:18 ET

Summary

- Valero shares are in a downtrend as a result of economic weakness and accelerating global refinery supply.

- The good news is that Valero's business continues to be strong. Volumes and margins are high and new investments expand long-term growth potential.

- The company has a healthy balance sheet, which means it can now prioritize dividend growth and buybacks over debt reduction.

- I expect Valero to turn into an outperforming total return star the moment economic growth bottoms. Until that happens, I will accumulate shares on weakness.

Introduction

In January, I wrote my most recent article covering Valero Energy ( VLO ), one of my largest energy investments. Back then, I wrote that the company was a hold, given economic headwinds.

[...] I wouldn't recommend anyone to rush in at current prices - despite its valuation, positive outlook, and high likelihood of the return of dividend growth.

Economic growth is going down south quickly, and I believe that the market is way too dovish when it comes to estimating what the Fed is up to in 2023 and 2024.

Since then, VLO shares have lost a fifth of their value as investors have started to price in a recession, which usually hurts cyclical companies like refiners the most.

The good news is that this comes with opportunities. VLO has a fantastic balance sheet, its business is still generating high profits, and the dividend seems to be extremely safe.

In this article, we'll discuss all of this and assess the risk/reward of this energy dividend beauty.

So, let's get to it!

Headwinds Are Building

Supply and demand headwinds have emerged.

Valero Energy is one of the big-three pure-play refinery companies in the United States. Given the cyclical nature of refined product demand, VLO shares have been under pressure for months.

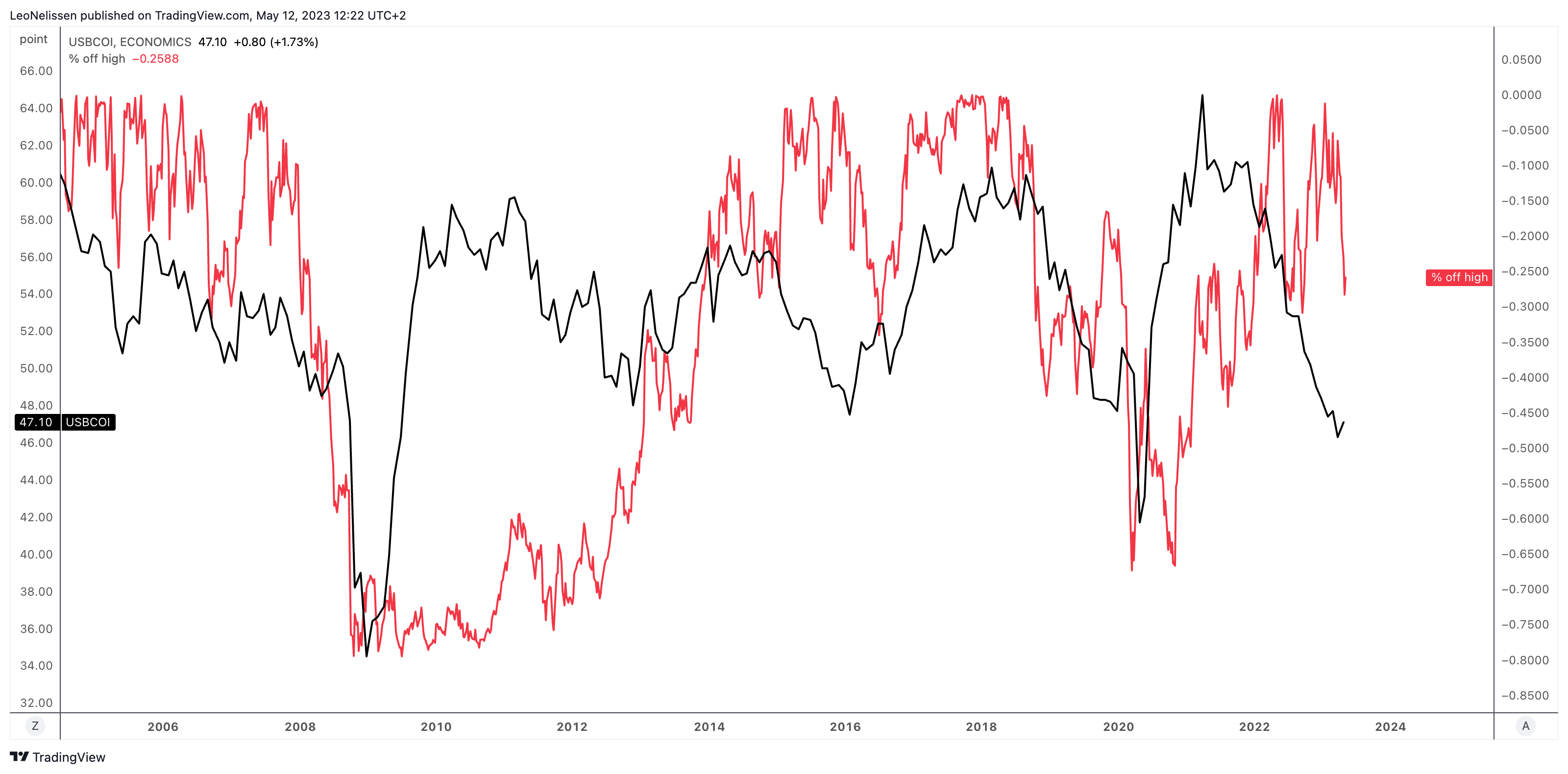

The chart below compares the ISM Manufacturing Index (black line), one of my favorite leading economic indicators, to the performance of the VLO stock price. In this case, it shows the total sell-off from VLO's all-time high.

{kind=link}

TradingView (ISM Manufacturing Index, VLO)

While the correlation isn't perfect, we see that declining economic growth is weighing on VLO shares.

VLO shares are currently down 26% from their 52-week high and down 13% on a year-to-date basis.

FINVIZ

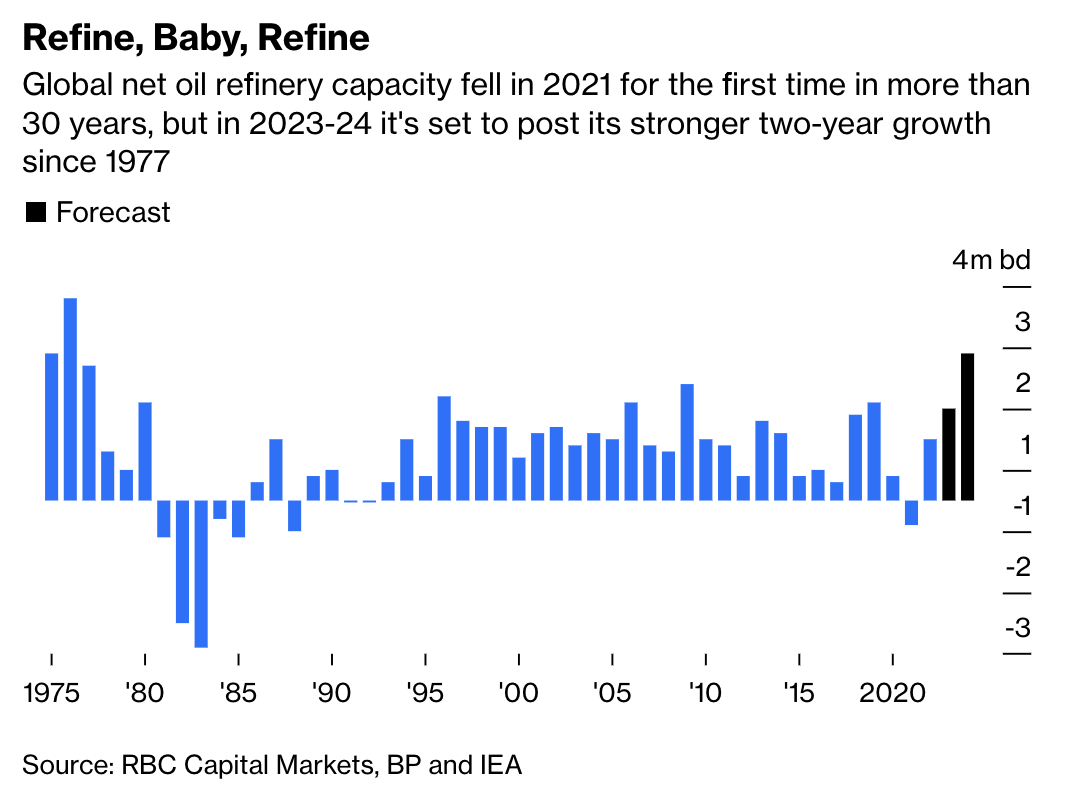

In addition to slower economic expectations and high risks that the situation could get worse, we're dealing with rebounding refining supply growth.

As reported by Bloomberg's Javier Blas , the world is now building new refineries and expanding older ones at a pace unseen in nearly two generations.

{kind=link}

Bloomberg

Net global refinery capacity is expected to increase by 1.5 million barrels a day this year and by another 2.4 million next year, according to RBC Capital Markets LLC.

This is the largest two-year increase in net global refining capacity in 45 years.

Exxon Mobil ( XOM ) is a part of this new trend, as it recently fired up the expansion of its plant in Beaumont, Texas, which has 250,000 barrels a day of extra capacity, the largest addition in the US in more than ten years.

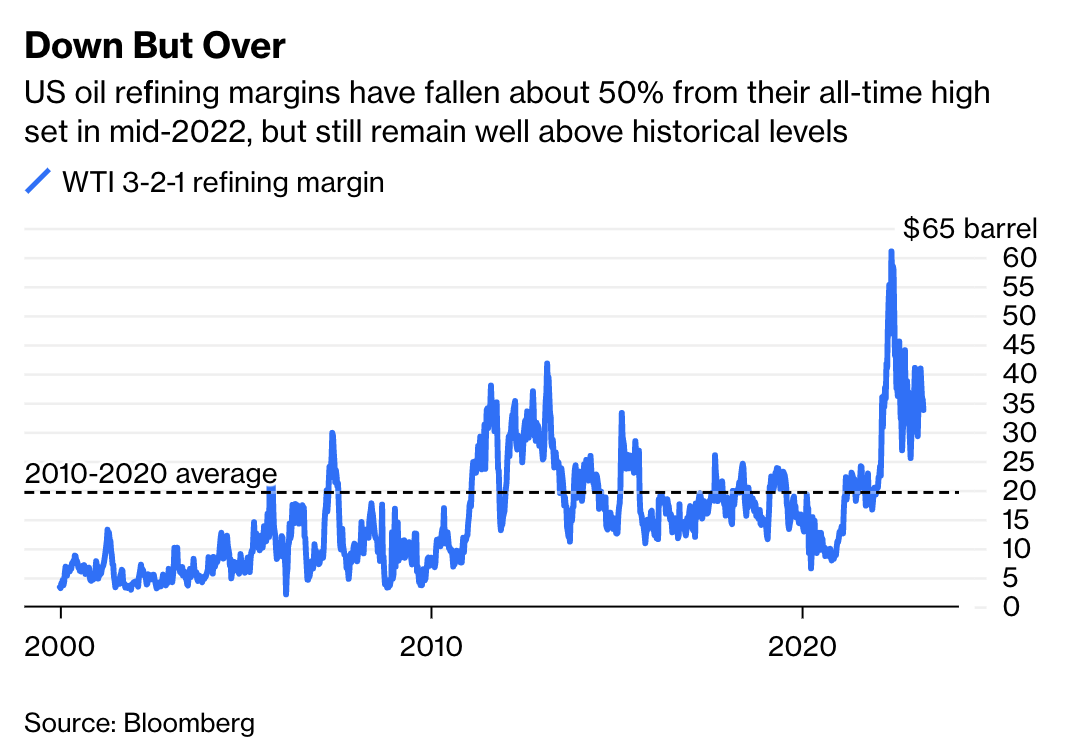

Although petroleum demand growth remains healthy, refiners are unlikely to repeat the super-charged profits of last year.

While I agree with that, it needs to be said that the surge in refining output comes after two very slow years during the pandemic. When looking at the bigger picture, we're basically just seeing a continuation of the expansion trend that started in the mid-1990s.

Furthermore, refining margins remain strong.

{kind=link}

Bloomberg

Also, new additions were predictable. They were announced and not a surprise to companies like VLO - or major investors in the industry.

So, what about Valero?

Valero Shareholders Remain In A Good Spot

While shares are down, business fundamentals remain strong.

As the industry margins chart above might have suggested, Valero is still doing well.

In 1Q23, Valero reported strong results across all of its segments. The company’s refineries operated at a 93% capacity utilization rate despite planned maintenance at several facilities. 93% is very high. Numbers higher than that are not sustainable due to maintenance requirements.

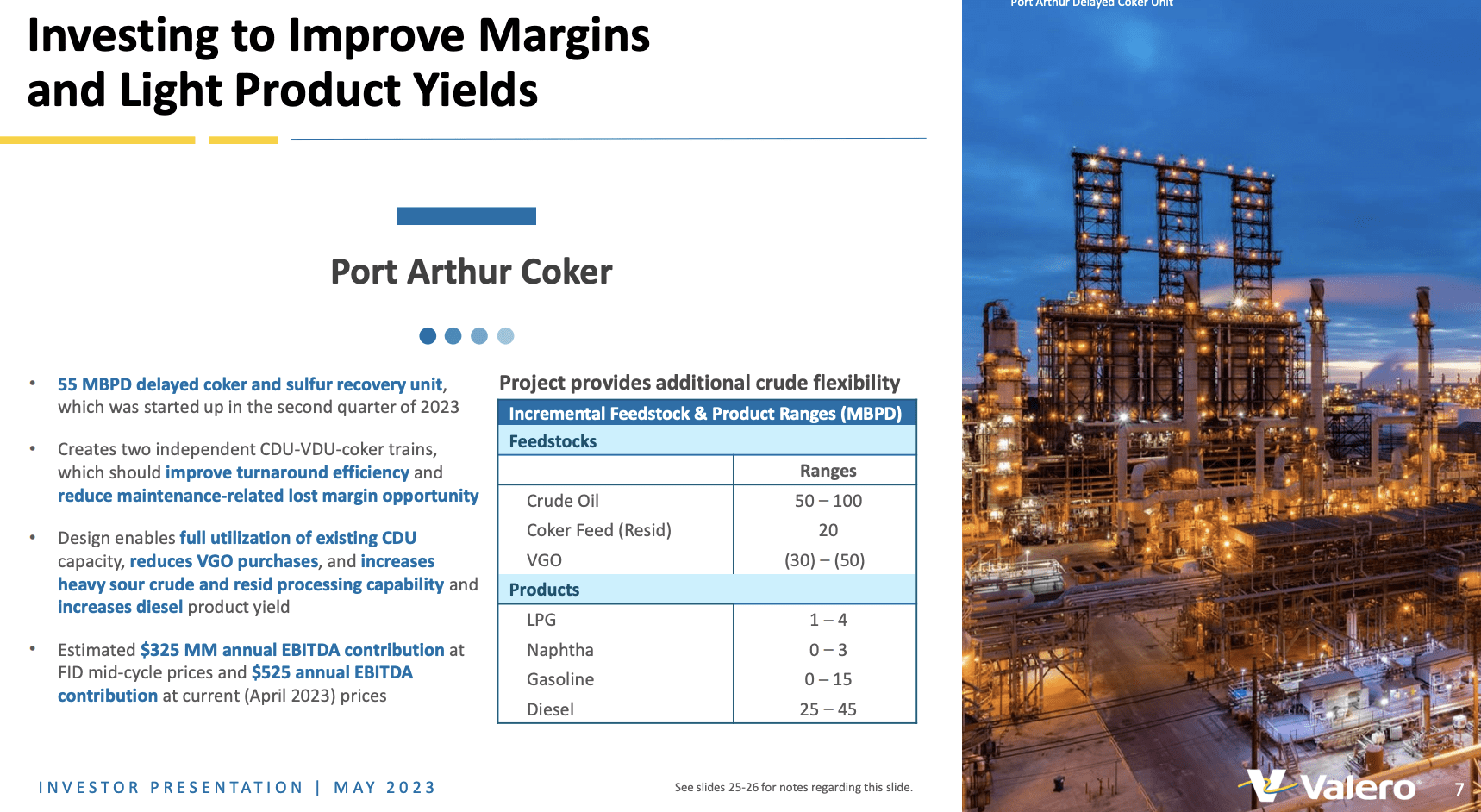

The company’s Port Arthur coker project was completed in March and successfully started up in early April. The project is expected to increase the company's throughput capacity and ability to process incremental volumes of sour crude oils and residual feedstocks while improving turnaround efficiency.

{kind=link}

Valero Energy

Based on that context, the Refining segment generated $4.1 billion in operating income in 1Q23. Refining throughput volumes averaged 2.9 million barrels.

Refining throughput volumes were up 130,000 barrels per day compared to the prior-year quarter.

Furthermore, the segment's Refining cash operating expenses were lower than guidance at $4.78 per barrel, primarily due to higher throughput and lower natural gas prices.

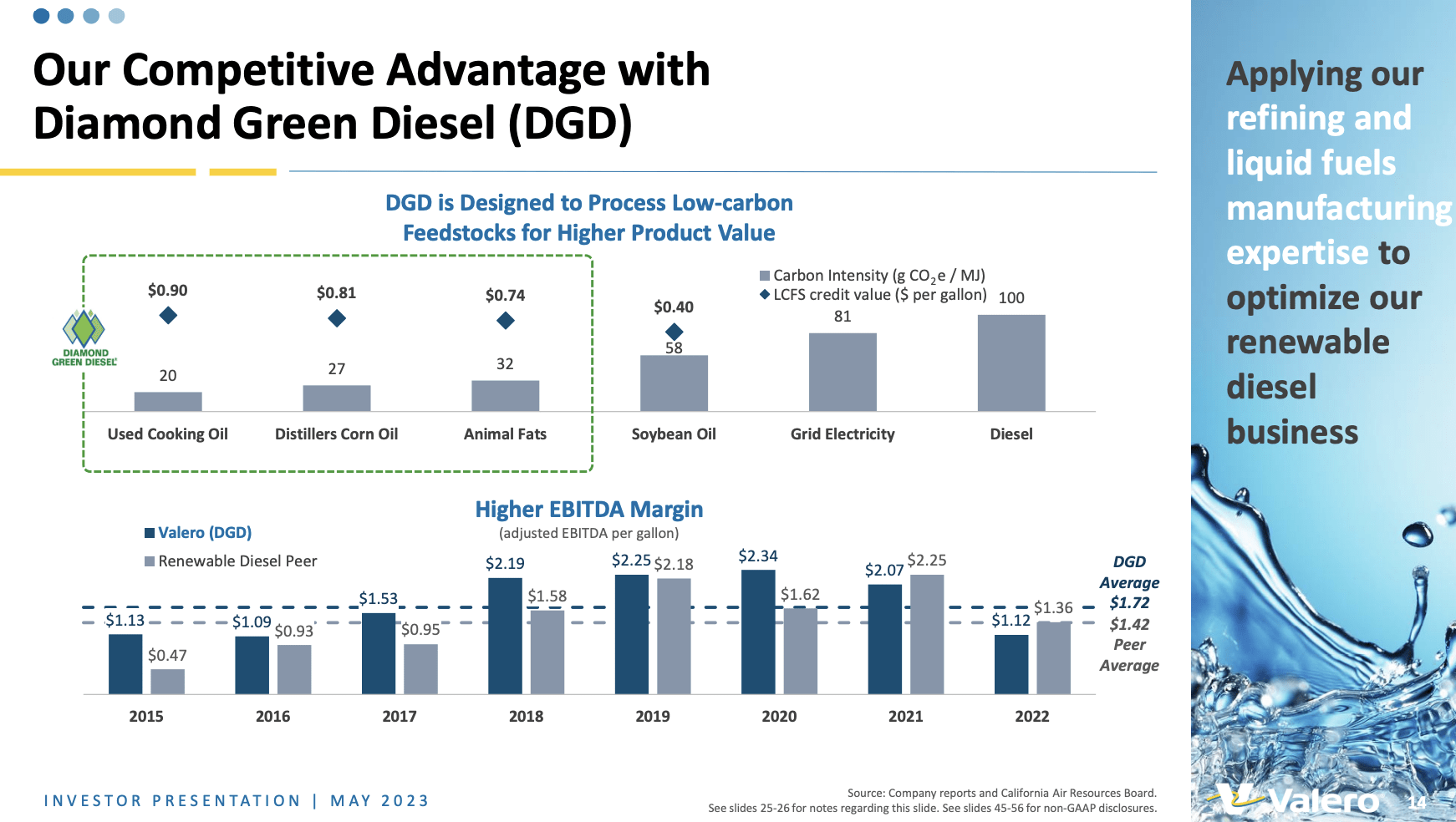

The Renewable Diesel segment generated an operating income of $205 million, with renewable diesel sales volumes averaging three million gallons per day in Q1 2023. This was due to the impact of additional volumes from the start-up of the DGD Port Arthur plant in the fourth quarter of 2022.

{kind=link}

Valero Energy

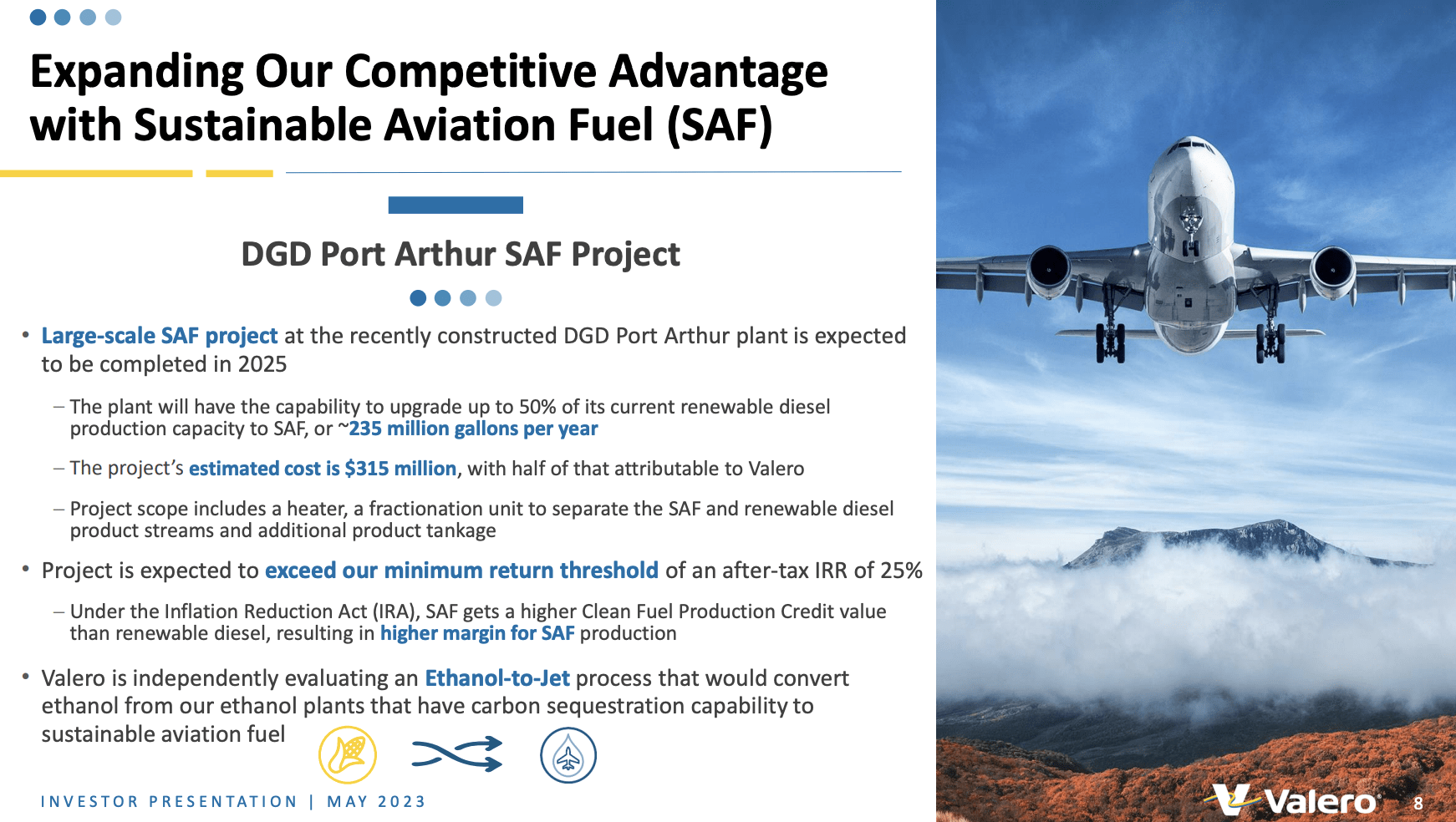

Related to this, the company announced that DGD approved a sustainable aviation project at Port Arthur, Texas. The DGD Port Arthur plant will have the capability to upgrade approximately 50% of its current 470 million-gallon annual renewable diesel production capacity to sustainable aviation fuel or SAF. The project is expected to be completed in 2025 and is estimated to cost approximately $315 million, with half of that attributable to Valero. With the completion of this project, DGD is expected to be one of the largest manufacturers of SAF in the world.

{kind=link}

Valero Energy

The smallest segment, Ethanol, production volumes averaged 4.2 million gallons per day, generating an operating income of $39 million for the Ethanol segment.

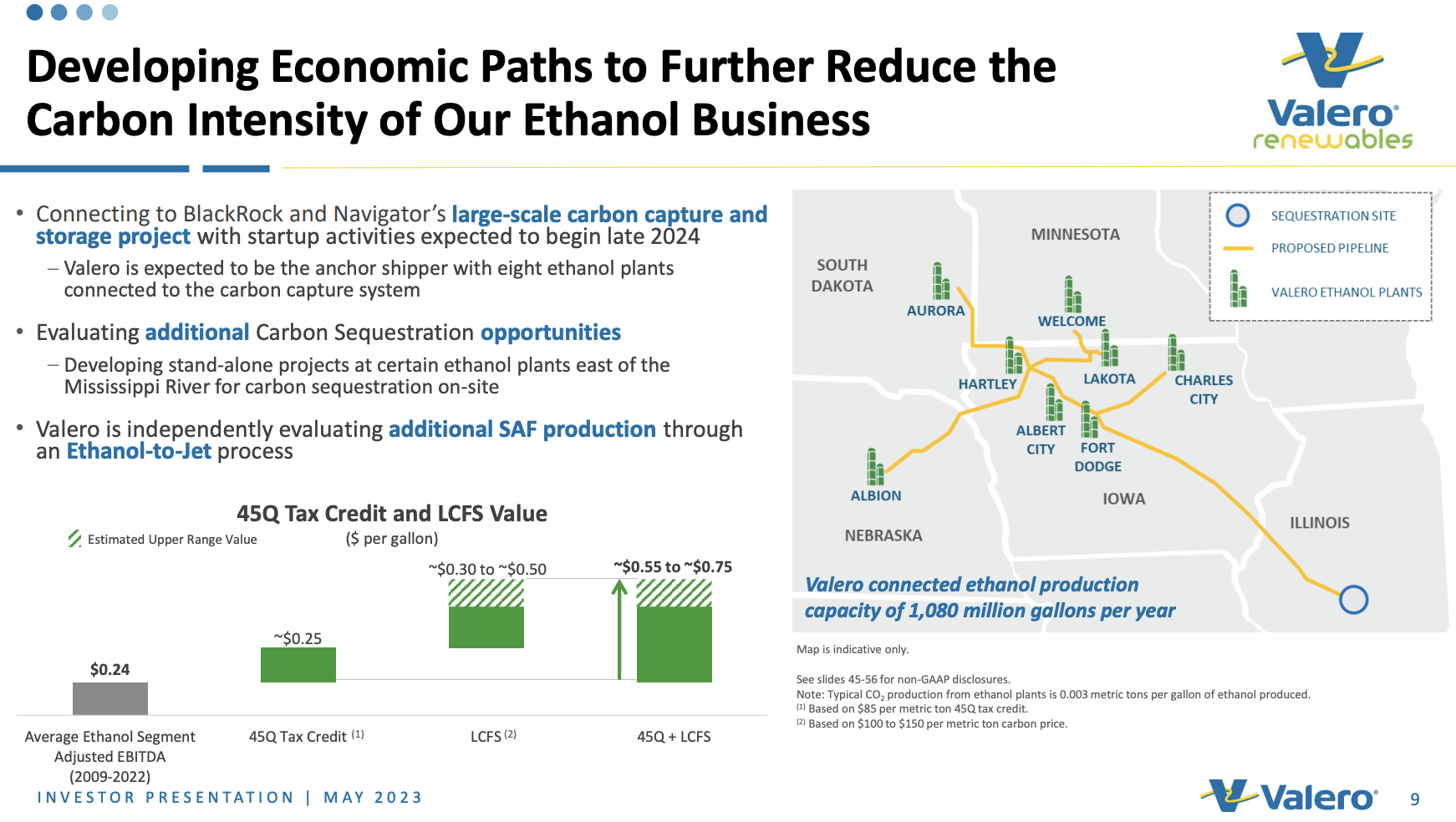

While its ethanol business is small compared to its refining business, the segment is progressing with BlackRock and Navigator's carbon sequestration project.

{kind=link}

Valero Energy

The project is expected to begin start-up activities in late 2024. Valero expects to be the anchor shipper with eight of its ethanol plants connected to this system which will allow it to produce a lower carbon-intensity ethanol product and significantly improve the margin profile and competitive positioning of its Ethanol business.

Going forward, the company expects refining fundamentals to remain supported by a mix of low global light product inventories, tight product supply, demand balances and continued increase in product demand as it approaches peak air travel and summer driving season.

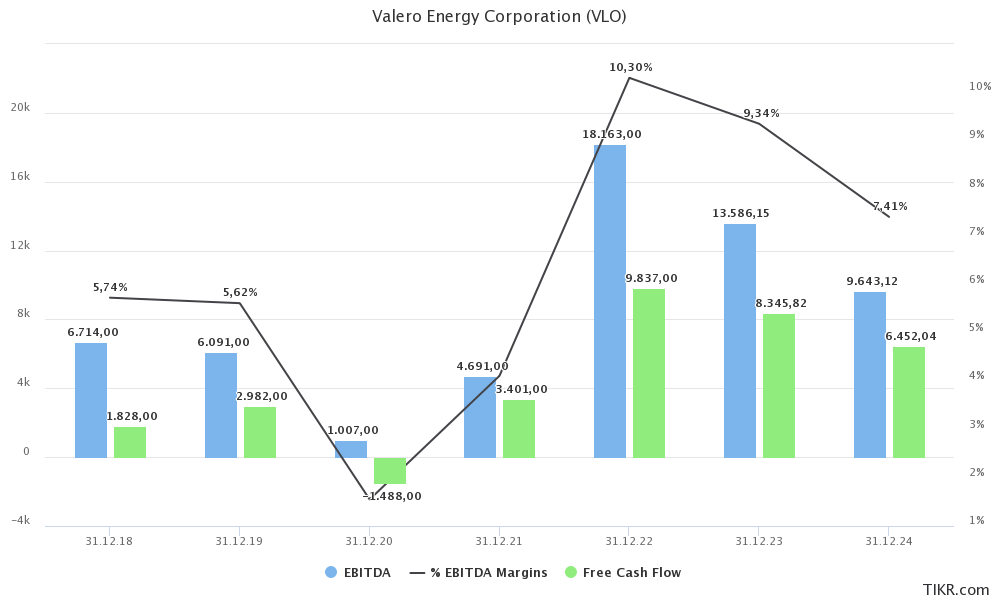

Sell-side analysts seem to agree, as the company is expected to maintain strong EBITDA and margins, which comes with strong free cash flow.

{kind=link}

TIKR.com

While these numbers haven't kept investors from selling VLO stock, they do protect investors because the company is in a much better spot compared to prior recessions.

The Valero Dividend

Dividend investors remain in a great spot.

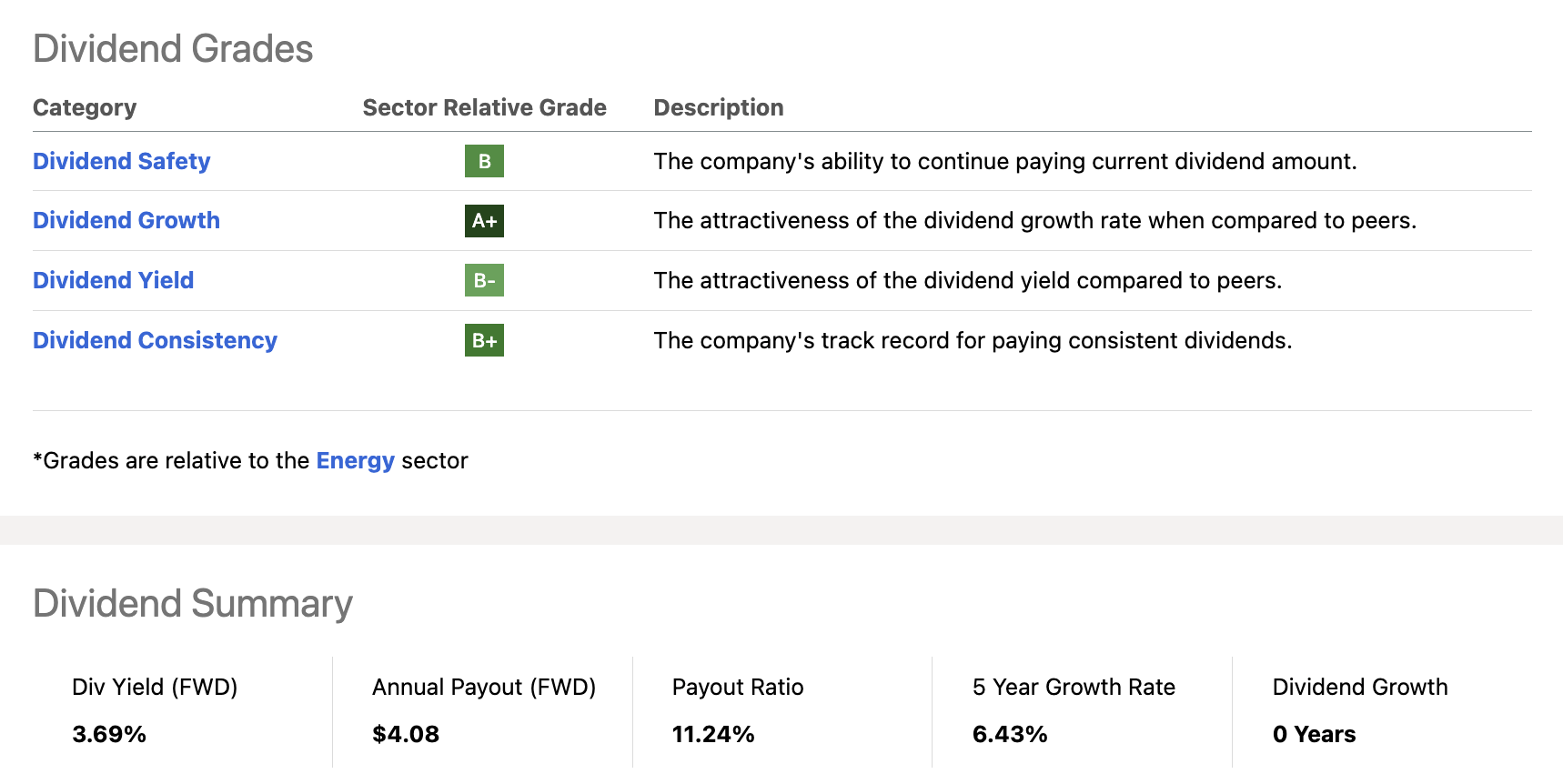

After cutting its dividend during the Great Financial Crisis, Valero has been one of the strongest dividend growth stocks in the energy sector.

Despite not hiking its dividend for roughly two years after the pandemic, Valero, the company still has an average annual dividend growth rate of 6.4% over the past five years. Its payout ratio is now a mere 11%, thanks to the post-pandemic rebound in margins and volumes.

{kind=link}

Seeking Alpha

Now, the company is yielding 3.7% after management hiked the dividend by 4.1% in January.

This was allowed by a much healthier balance sheet. Using 2023 estimates, the company has a 0.3x net debt ratio.

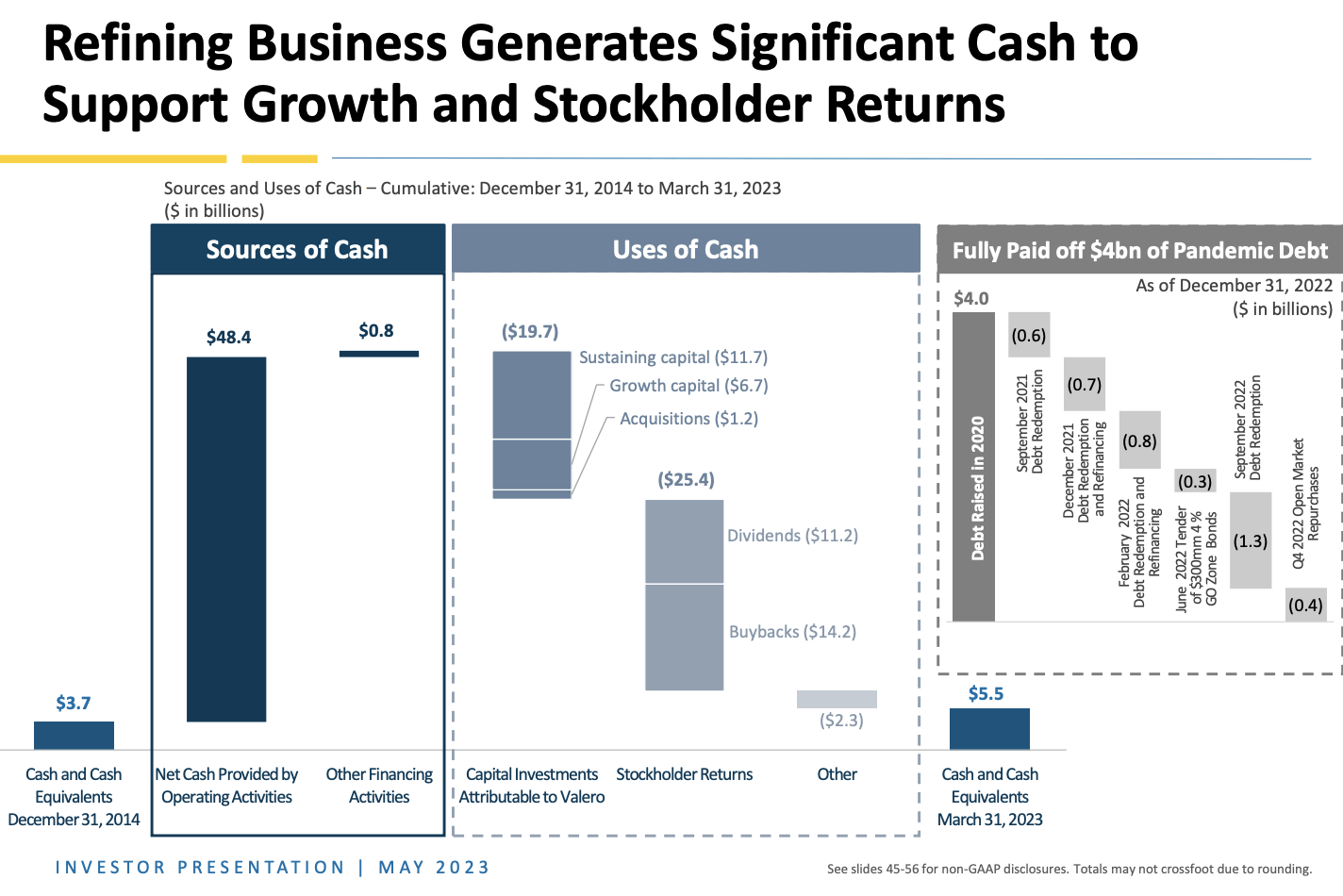

Furthermore, as the overview below shows, the company has paid off all of its pandemic-related debt.

{kind=link}

Valero Energy

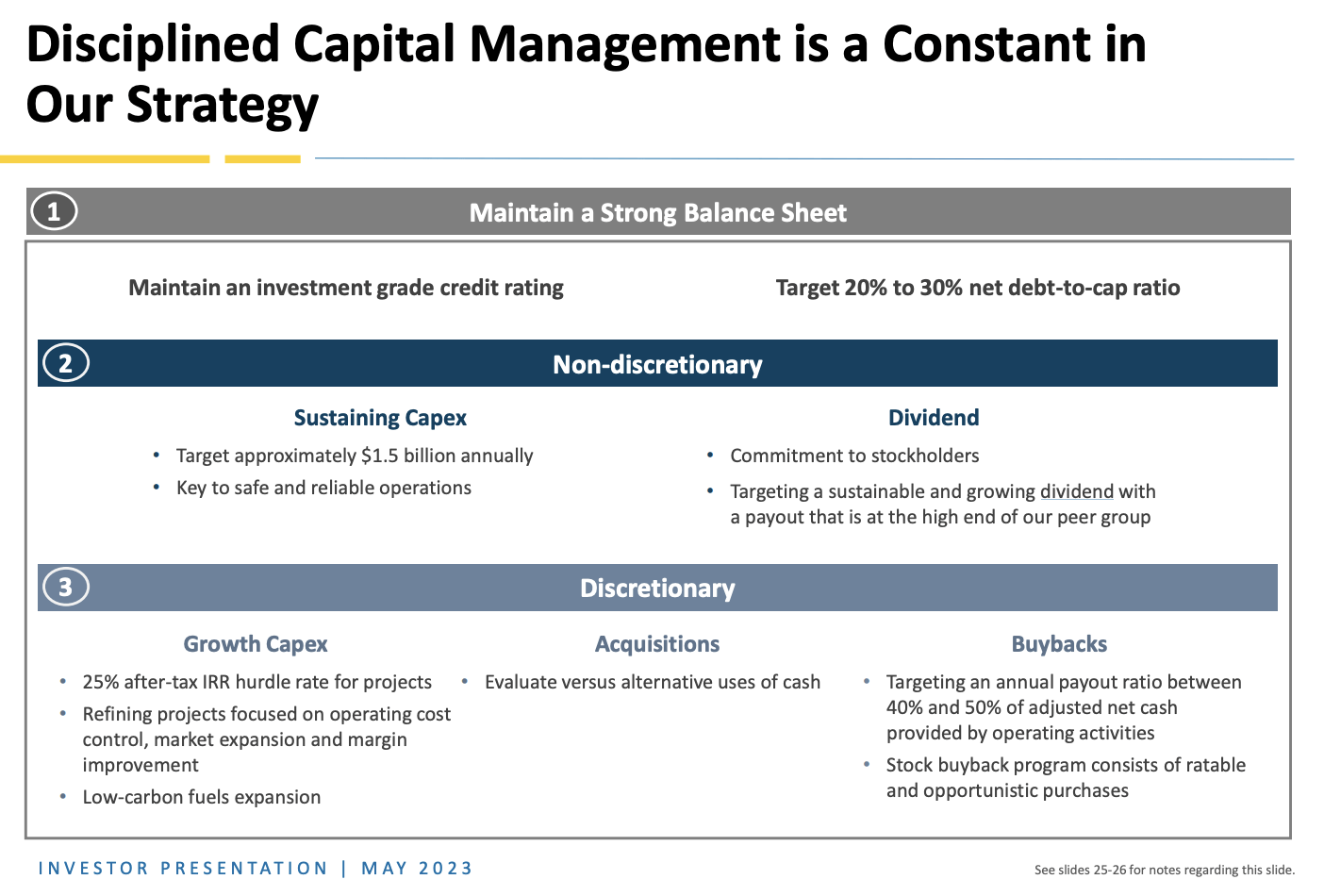

In the first quarter, the company continued to strengthen its balance sheet, reducing debt by $199 million and ending the quarter with a net debt-to-capitalization ratio of 18%. This debt ratio is below its target range, which means it can prioritize non-discretionary spending, like boosting its dividend.

{kind=link}

Valero Energy

While management didn't comment on any future hikes, we should assume that dividend growth is likely to remain subdued until the company sees a bottom in economic demand.

I am convinced that the company hiked by only 4% this year, as it was aware of the cyclical risks on the horizon.

The company could have easily hiked by 20% to 30% if it wanted to.

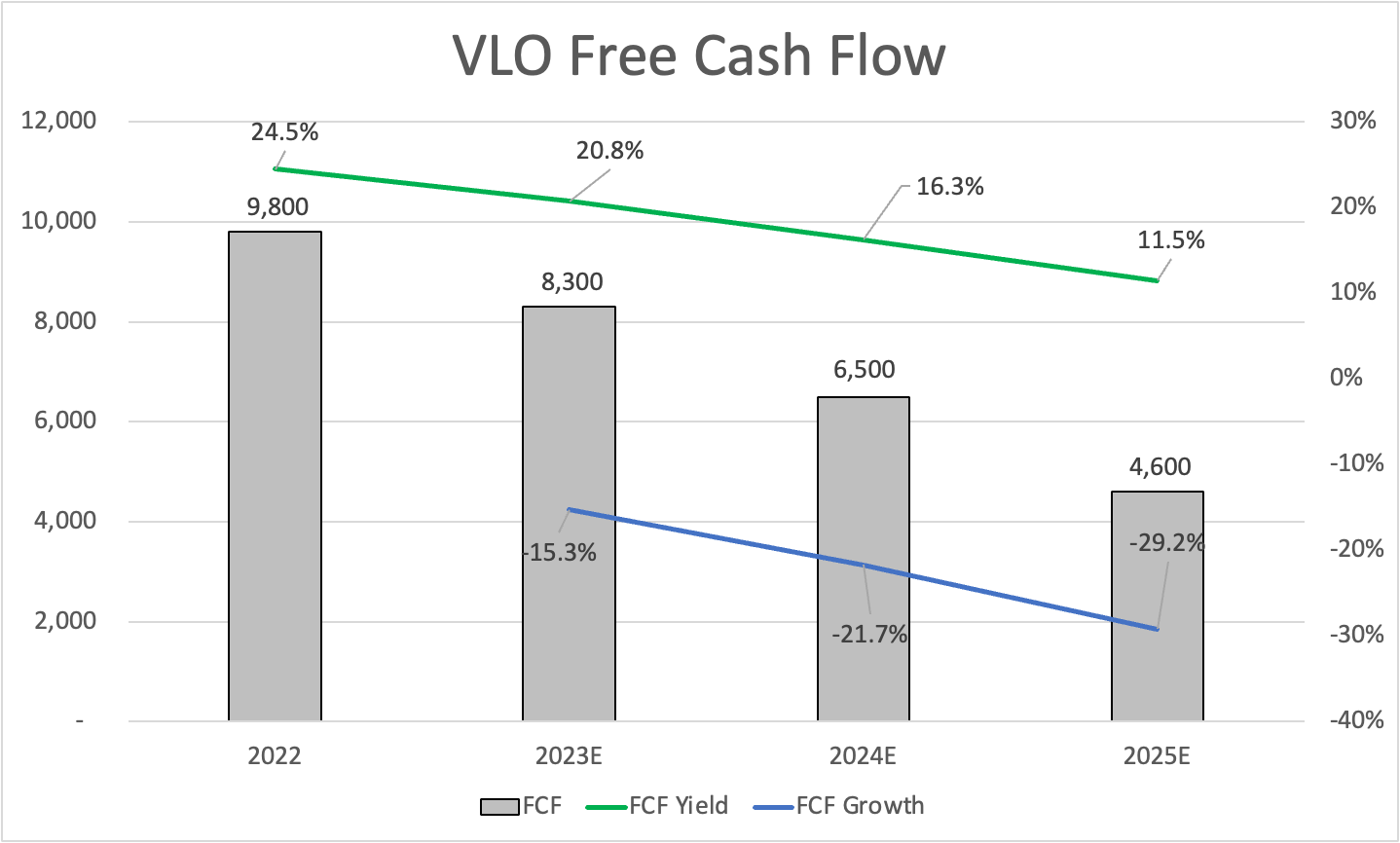

As we can see below, while analysts expect free cash flow to moderate as new supply comes online, the company is set to benefit from a double-digit free cash flow yield for many years to come. This means that unless the company was to suddenly encounter a spike in its net debt, it is in a good situation to boost dividends on a long-term basis.

{kind=link}

Leo Nelissen

This is the main reason why I'm adding to my VLO position during price corrections.

Valuation

The numbers above also indicate that VLO is attractively valued, as investors are not overpaying to get access to its cash. Even using 2025 numbers, the company is trading below 9x free cash flow.

Between the Great Financial Crisis and the pandemic, VLO used to trade close to 10x free cash flow.

The current consensus price target is $155 (40% upside from current prices).

While I agree that VLO should not trade anywhere below $155, I do not expect the stock to start a sudden uptrend. The macroeconomic environment is simply too weak.

If anything, we could see more weakness if investors continue to price in a deeper recession.

However, as a long-term investor, I am far from worried. I look forward to boosting my position, as I am convinced that VLO will become a dividend growth star the moment economic conditions bottom.

At that point, I expect multiple years of outperforming capital gains and aggressive dividend growth.

Takeaway

Valero Energy has faced headwinds due to the economic slowdown and the emergence of supply and demand headwinds in the refining industry. However, while shares are down, business fundamentals remain strong. The company has a fantastic balance sheet, its business is still generating high profits, and the dividend seems to be extremely safe.

I expect VLO to turn into a total return star the moment economic growth expectations bottom.

For now, I will accumulate shares on stock price weakness.

For further details see:

Valero: The More It Drops, The More I Buy