OUST - Velodyne Lidar: Better With Ouster

Summary

- Velodyne Lidar and Ouster agree to a merger of equals.

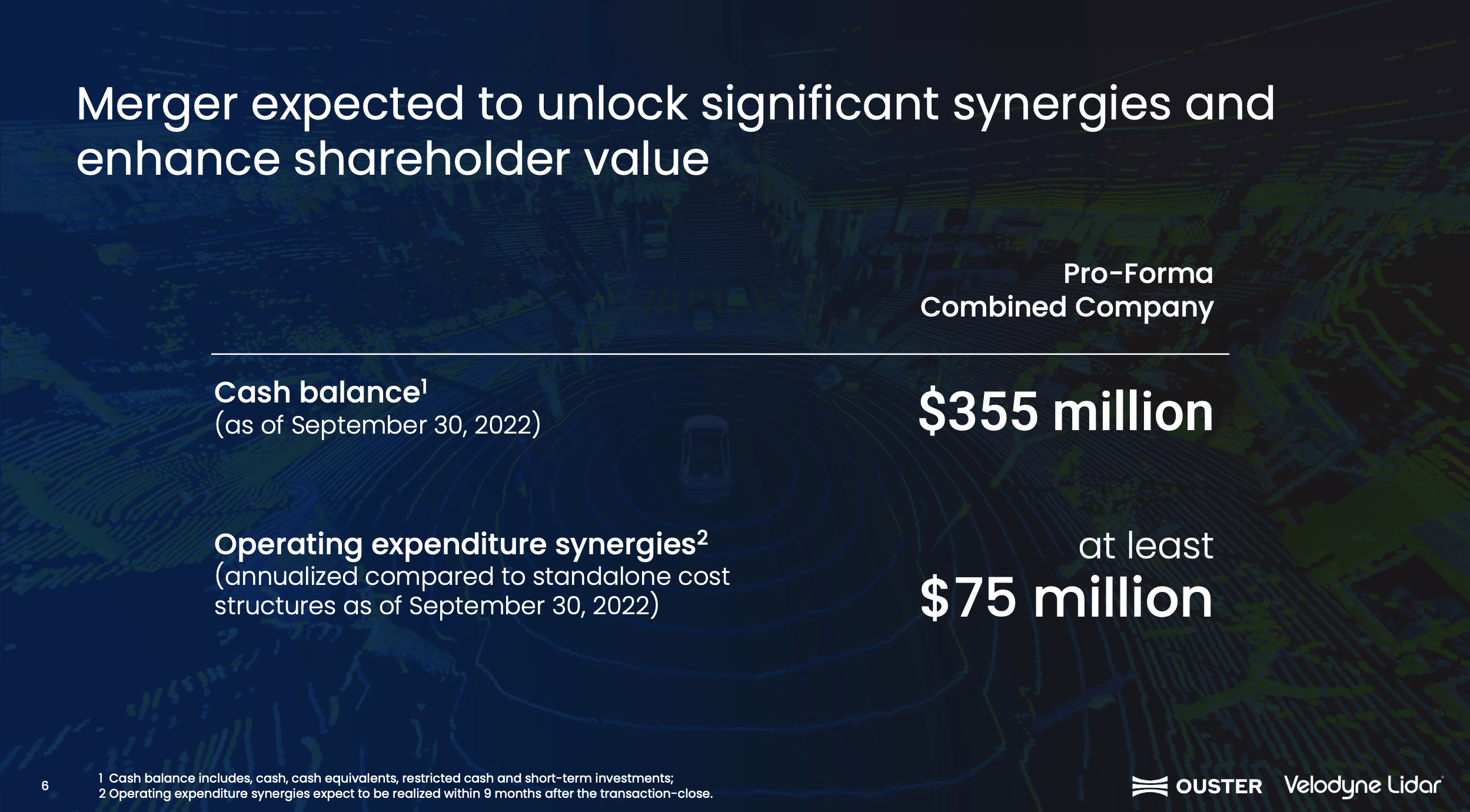

- The combined company will have $355 million in cash and slash $75 million in costs to speed up the path to breakeven.

- The stocks are a bargain trading at ~1x '24 sales targets, but risks are elevated in the sector.

In a rather surprising move, Ouster ( OUST ) agreed to a deal with Velodyne Lidar ( VLDR ) in a merger of equals. The Lidar sensor space offers substantial potential with the biggest risk to any investment in the sector being the participants surviving long enough to thrive. My investment thesis on Velodyne Lidar is far more Bullish with the combination with Ouster to eliminate the downside risk on the high expense structure leading to a negative outcome.

All About The Synergies

Prior to reporting Q3'22 earnings , Velodyne Lidar agreed to a deal accepting 0.8204 shares of Ouster in a deal of equals. Both shareholder bases will own 50% of the new company.

Velodyne Lidar has been through a dramatic struggle with the former founder and the company has failed to meet most financial metrics during the process. The stock currently trades below $1 despite the merger agreement and signs new CEO Ted Tewksbury has stabilized the business and set the company on a solid track to grow going forward.

While Lidar sensors have a massive TAM opportunity in the years ahead and both companies at one point had plans for revenue approaching $1 billion in the next 5 years, the companies have to survive the mounting losses of the next few years. In addition, Lidar adoption can and will probably take longer than expected.

Velodyne reported another quarter of revenues (billings) around $12.5 million, but most importantly the company reported a massive loss of $27.6 million with negative gross margins. The company has been in the process of shifting production to Thailand, but the costs never seem to improve with negative gross margins of 34%.

On the flip side, Ouster reported a quarter with similar revenues of $11.2 million with positive gross margins of 33%. The company produced similar revenues, but the gross profit picture was vastly improved with a divergence of $7.0 million.

The prime key to the merger is the unlocking of significant synergies. Velodyne Lidar was burning too much cash and Ouster was recently diluting shareholders via an ATM. Both companies were already in the process of cutting expenses.

The deal promises an impressive $75 million in reduced operating costs. Remember, Ouster had recently cut costs by 15%, so this move is almost entirely about stripping out the extra and duplicate costs of Velodyne Lidar.

{kind=link}

Source: Ouster/Velodyne merger presentation

In addition, the new company will have $355 million in cash entering Q4 to fund cash burn for another couple of years. The company cutting $75 million out of the cost structure while turning gross margin positive next year will make a leap forward towards profitability.

For Q3, Velodyne cut operating expenses by $6.7 million to $25.1 million. Ouster actually had higher quarterly operating expenses at $30.1 million.

The combined quarterly operating expense base appears around $55 million or $220 million annually. The new company stripping out $75 million in expenses leaving ~$150 million in annual expenses is a huge step forward. With positive gross margins, the new Ouster now has the cash to survive into 2026 without generating positive gross profits.

Big Revenues

Both companies have pulled back from providing backlog type figures, but the numbers weren't entirely helpful in the first place. Ouster had previously provided a $575 million contracted revenue figure through 2026, but the number only included SCAs for 80 customers over the contracted period.

Similarly, Velodyne Lidar had last listed a contracted revenue potential of $800 million through 2025 with an additional $4.2 billion potential from the pipeline. The combined company easily has over $1 billion in contracted revenues through 2026 at this point, but the management team no longer wants to report the numbers for competitive and legal reasons.

Ouster wasn't providing anything close to an actual revenue target. In Q3'22 alone, Ouster added 80 new customers lifting the total customer account in the last year to 700 with just about 10% of their customers signing SCAs.

The SCA total increased 4 to 84 in Q3. The company now has over 600 customers buying sensors without any commitment. These customers weren't factored into the previous contracted amounts and the contracted amount of course only included amounts that might just be 2 to 3 years, not up to 5 years as suggested by the 2026 timeline.

Ouster kept the 2022 revenue guidance for the year at $40 to $55 million. The number suggests the Q4'22 revenue total could reach $25 million and the CFO was very positive on the revenue boost for the quarter with the new REV7 chip launch.

Based on current analyst estimates, the combined company would have the following financial targets for 2023 and 2024 as follows:

- 2023 - $165 million (Ouster - $103 million, Velodyne - $65 million)

- 2024 - $367 million (Ouster - $242 million, Velodyne - $125 million)

The Velodyne Lidar amount doesn't appear the actual revenue total reflected in the billings amount provided by the company. The company guided to Q4 billings of $14.0 million after reporting $12.5 million in the prior quarter. The company is likely on the same revenue path of Ouster once the current supply chain issues are resolved by early next year.

Either way, the combined company is forecast to produce at least $165 million in 2023 revenues and $367 million in 2024. The combined market cap of the stock is below $400 million now highlighting the attractive valuation equation.

Elevated Risks

The combined company has exited the pre-revenue phase with Q4 revenues possibly approaching $40 million, but the Lidar market is still in infancy. Any slower development than expected will push out the path to profits and could require the new Ouster to ultimately raise additional cash and dilute shareholders despite the combined cash balance.

In addition, the adoption of Lidar remains a major risk to sector participants. Tesla ( TSLA ) is moving forward with a self-driving solution that doesn't even utilize Lidar. As well, a competitor could develop a better Lidar solution causing the combined company to lose future orders and limited cash could leave the company without the funds to improve their technology to obtain contracts.

In essence, an investor in the stock has to realize a loss of capital is a real possibility. Naturally, the stock wouldn't trade below $1, if risk of loss of capital didn't exist in the view of the market.

Takeaway

The key investor takeaway is that the combination of Velodyne Lidar and Ouster creates a powerhouse in the non-automotive Lidar market. The combined company will have a large customer base with impressive revenues set to top $30 million in Q4. The market doesn't appreciate the opportunity here, but the risk is definitely elevated.

For further details see:

Velodyne Lidar: Better With Ouster