VERA - Vera: New Kidney Data May Be A Potential Next Big Pharma M&A Target

2023-07-04 09:42:14 ET

Summary

- Vera Therapeutics revealed 36-week efficacy and safety findings of its Phase IIb ORIGIN clinical study of atacicept for IgAN at the 60th European Renal Association Congress.

- The study met its primary and secondary objectives, showing significant reductions in proteinuria and eGFR stabilization, leading to plans for a Phase III trial in June 2023.

- With the positive data and low valuation (after the sell-off), we believe Vera now looks like an attractive SMID-cap biotech for high-risk investors to play the red-hot IgAN space.

- We upgrade Vera stock to a buy (speculative buy to be precise) from a Sell rating.

Key update: ERA 36 weeks presentation

On June 17th, during the late-breaking discourse at the 60th European Renal Association Congress, Vera Therapeutics ( VERA ) unveiled the company's 36-week efficacy and safety findings of its Phase IIb ORIGIN clinical study of atacicept for IgAN. The bottom line of the results indicates that the Phase IIb ORIGIN trial of atacicept for IgAN management met its primary and secondary objectives, showing statistically and clinically consequential reductions in proteinuria and eGFR stabilization through week 36. Building on this, the management showed intention to kickstart a Phase III (ORIGIN 3) clinical trial in June 2023.

To give a more detailed background of the trial :

ORIGIN is an international, placebo-controlled, double-blind, randomized study set to appraise the impact and safety of atacicept in IgAN patients who have continued proteinuria and remain susceptible to disease progression despite current ACEi or ARB therapy. The main objectives entail assessing atacicept's influence on proteinuria and renal function preservation against placebo, thereby establishing optimal dosages for subsequent clinical progression.

In the 36-week blinded treatment period, the ORIGIN Phase IIb trial assessed three doses of atacicept in comparison to placebo, dispensed weekly via prefilled syringes. Following this phase, all patients are presented with open-label atacicept 150 mg for an added 60 weeks.

The primary goal revolves around proteinuria changes, gauged by the urine protein to creatinine ratio (UPCR) at week 24, with a secondary focus on UPCR alterations at week 36. UPCR is a marker of kidney function decline; more damaged, more leakage of protein will be detected in urine.

Similar to other trials in IgAN, additional exploratory endpoints include UPCR deviations at weeks 12, 48, and 96, modifications in estimated glomerular filtration rate (eGFR), and serum immunoglobulin levels, plus serum Gd-IgA1 levels.

Results: decent placebo-adjusted reduction shown

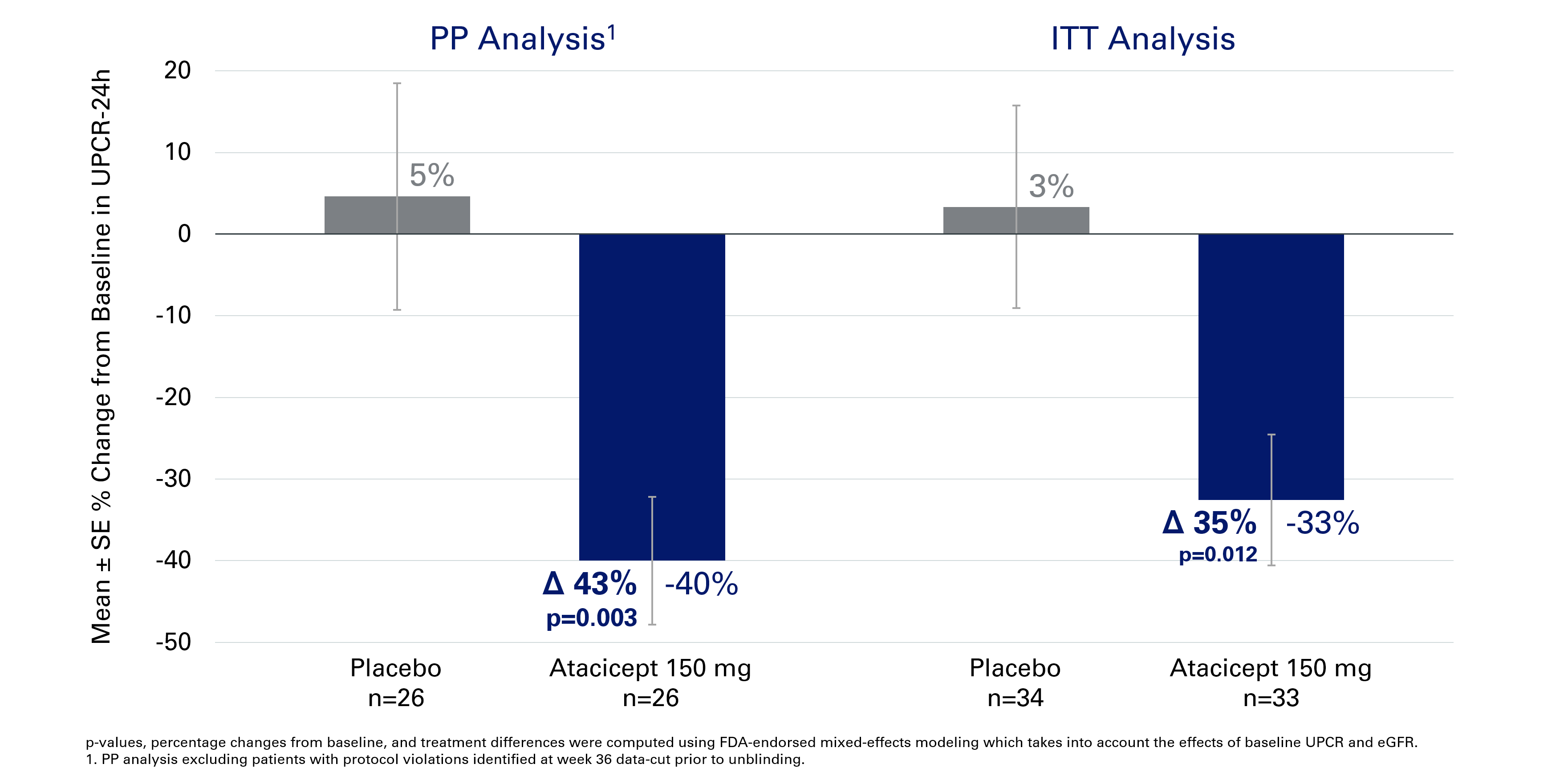

We highlight that as per the 36-week results , the atacicept 150 mg dosage group exhibited a substantial 43% placebo-adjusted reduction from the initial proteinuria level, a higher reduction rate than the 35% observed in the intent-to-treat analysis published previously.

Figure 1. UPCR % Change With Atacicept 150 mg at Week 36 (Company source)

{kind=link}

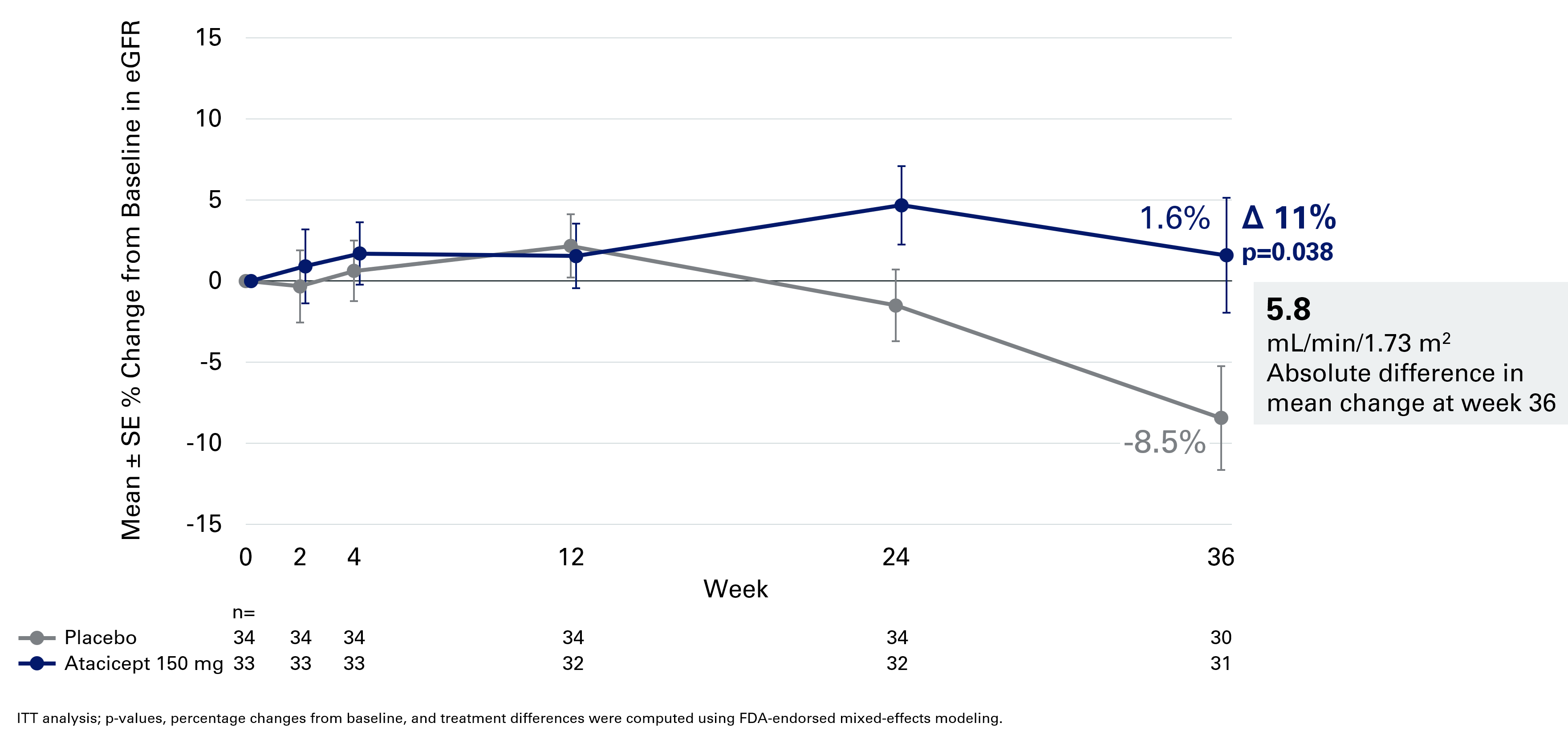

In the latter, patients on placebo displayed an anticipated drop in kidney function, while those on atacicept 150 mg retained stable eGFR up to week 36 - which is a statistically and clinically significant difference. As we have repeatedly highlighted in our IgAN disease coverage universe, the benefit of EGFR will be the key focal point in the space, where the FDA will concentrate on the magnitude or onset of the benefit. Therefore, we find the atacicept's statistically significant benefit on EGFR at week 36 vs. placebo highly compelling (5.8mL/min/1.73m2 placebo adjusted delta - atacicept's eGFR stable and placebo patient's condition declining).

eGFR % Change With Atacicept 150 mg Through Week 36 (Company source)

{kind=link}

In terms of safety, Atacicept's safety data imply general tolerability, aligning with previous safety observations (and previous safety data in the drug's use in other indications). Most importantly, there were no increased infection rates compared to the placebo, a meager 2% rate of serious adverse events overall, and no discontinuations or interruptions attributed to hypogammaglobulinemia.

Net-net, although the trial was a small trial, these updated results give some degree of comfort around the candidate's safety, as safety was a potential hesitation amongst investors due to its dual mechanism of action vs. Chinook's anti-April platform.

IgAN market landscape

Drug Company Description Status Reduction in proteinuria Tarpeyo Calliditas Oral formulation of budesonide Approved (accelerated); eGFR data reported Mar 2023 34% (31% pbo-adjusted) in ph3 Nefigard Filspari (sparsentan) Travere Oral endothelin type A & angiotensin II type 1 inhibitor Approved (accelerated); eGFR data due Q4 2023 50% (35 points adjusted for irbesartan control) in ph3 Protect Narsoplimab (OMS721) Omeros Anti-MASP2 antibody Ph3 Artemis-IgAN ; proteinuria data due mid-2023 64% (no control arm) in ph2 Atrasentan Chinook Oral endothelin A receptor inhibitor Ph3 Align ; proteinuria data due H2 2023 55% (no control arm) in ph2 Affinity Iptacopan (LNP023) Novartis Oral complement factor B inhibitor Ph3 Applause-IgAN ; proteinuria data due H2 2023 23% pbo-adjusted in ph2 * Sibeprenlimab (VIS649) Otsuka Anti-April antibody Ph3 Visionary ends Dec 2026 43% pbo-adjusted in ph2 ** *At highest dose (200mg BID); **pooled data with IV doses 2mg, 4mg & 8mg monthly. Source: Evaluate Pharma & clinicaltrials.gov . Source: Evaluate Pharma

Risks

-

Clinical Trial Uncertainty: The results of the Phase IIb trial were positive, but it's important to remember that there's no guarantee subsequent trials, such as the upcoming Phase III (ORIGIN 3) trial, will yield similar results. Clinical trials are inherently unpredictable, and there's always a risk that the drug may not meet its primary or secondary endpoints in future trials.

-

Drug Approval Risk: Even if the results of the clinical trials are positive, there is always the risk that regulatory bodies (like the FDA) may not approve the drug for sale. Approval hinges on a thorough evaluation of not just the drug's efficacy, but also its safety profile, cost-effectiveness, and comparisons to existing therapies.

-

Market Adoption Risk: Assuming atacicept gets approval, it must still be adopted by medical practitioners and be accepted by patients. This process is influenced by a range of factors, including drug pricing, insurance coverage, and competition with other treatments.

-

Financial Health Risk: Despite the robust cash runway indicated by its current financials, Vera Therapeutics is still a smaller biotech firm with substantial costs associated with clinical trials and potential drug commercialization. If the cash burn rate increases or if there are unexpected expenses, it could put a financial strain on the company.

Conclusion

We find the recent data publication that showed more meaningful placebo-adjusted proteinuria reduction (43% vs. 35% from what we have seen in ITT analysis) and no new concerning treatment-related adverse events (one of the key overhangs considering the dual mechanism of action), a net positive for the stock. Furthermore, the stock sold off previously after the disappointing proteinuria endpoints and the current valuation (EV of $543m attractive considering Chinook's recent $3.5Bn M&A). Furthermore, we believe the recent acquisition of Chinook ( KDNY ) by Novartis (NVS) ($3.5bn deal) should add more enthusiasm (or M&A fantasy) around the anti-April platform, considering that potential mid/late stage IgAN candidates to acquire (for big pharma) have been thinning out. Furthermore, with the low valuation of Vera at this point and robust cash runway (enterprise value of $543m and cash of $197m (cash burn around $30m)), we upgrade to a buy rating. We believe Vera is now an attractive SMID-cap biotech that we may consider adding an optioned size position to play the enthusiasm around the rare kidney disease space.

For further details see:

Vera: New Kidney Data, May Be A Potential Next Big Pharma M&A Target