CURLF - Verano: High-Risk High-Reward Name In U.S. Cannabis

2023-11-02 12:10:55 ET

Summary

- Verano Holdings Corp. is generating free cash flow and benefiting from its focus on limited license jurisdictions despite pricing pressures in the cannabis sector.

- The company's highly leveraged balance sheet poses significant risks, but the stock is trading cheaply and may offer substantial returns if price compression stabilizes and debt issues are addressed.

- There is a visible catalyst in the DEA potentially re-scheduling the plant to schedule III, which would dramatically boost cash flows and lower the cost of capital.

- I reiterate my strong buy rating for this top-tier U.S. operator.

Amidst vicious pricing pressures in the cannabis sector, Verano Holdings Corp. ( VRNOF ) is hanging on. While I wish management would take more drastic actions to resolve its debt issues, the company is surprisingly among the top in terms of generating free cash flow, assuming management can hit their full-year guidance. VRNOF is benefitting from its historical focus on limited license jurisdictions, though that obviously hasn’t insulated it from the widespread price compression. In large part due to the highly leveraged balance sheet, the risks are sky high here.

That said, VRNOF stock is trading very cheaply and may still offer stunning return potential, assuming we eventually see a bottom in price compression and the company can address its debt issues. I reiterate my strong buy rating for the stock.

VRNOF Stock Price

VRNOF came public in early 2021 as one of the most profitable multi-state operators ("MSOs"). As growth came to a standstill and margins took a plunge, the stock suffered - big time.

While the stock is very cheap here, the high debt load elevates the risk profile.

VRNOF Stock Key Metrics

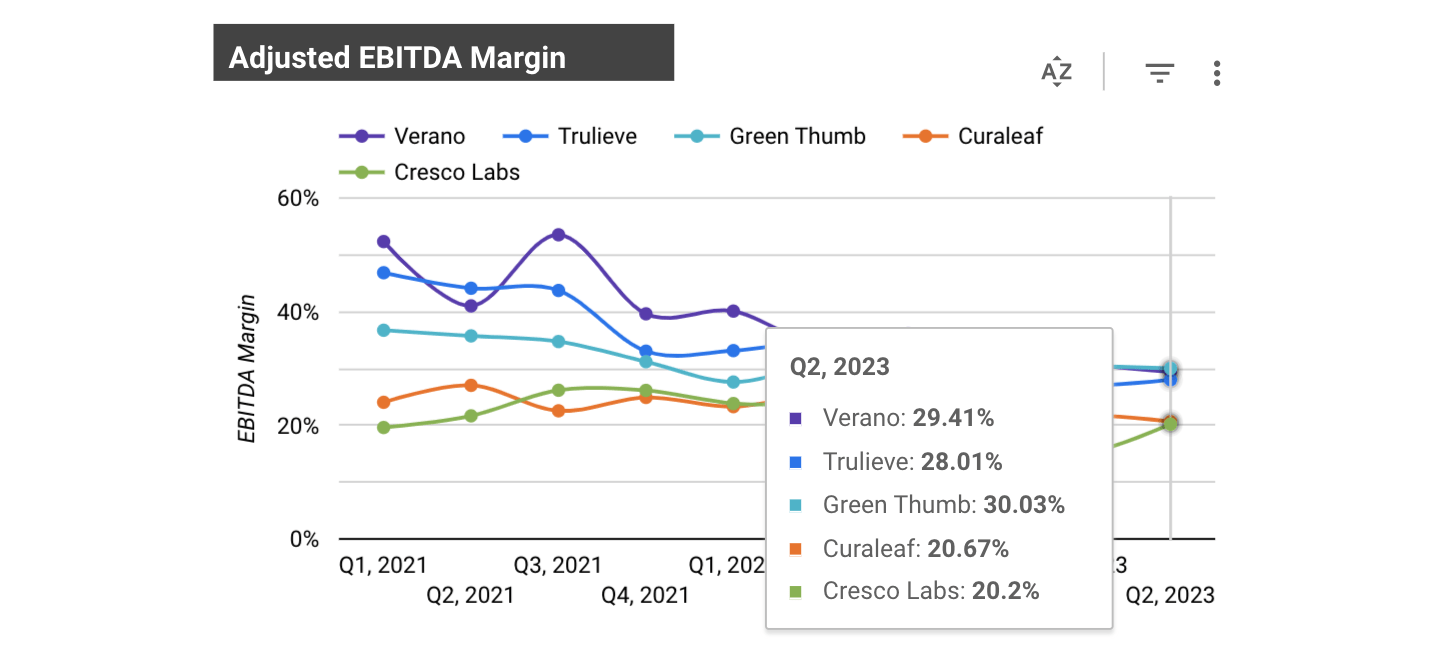

In its most recent quarter, VRNOF finally delivered some growth as the company began lapping easy comparables. Revenues of $234 million grew 5% YOY and 3% sequentially. Due to price compression, adjusted EBITDA declined YOY in spite of the top-line growth. It can be easy to forget that this is a name which once generated adjusted EBITDA margins in excess of 50% just 2 years ago. VRNOF remains near the top of the pack in terms of adjusted EBITDA margins though I note that only Green Thumb Industries ( GTBIF ) is generating GAAP net income.

{kind=link}

VRNOF’s core markets are Illinois and Florida, as these two markets have historically generated the bulk of its cash flow. VRNOF noted that pricing seems to be stabilizing in Illinois, but also noted that revenues in the state declined in spite of the dispensary count growing by over 20% year to date. Previously, many top operators had been saying that new retail dispensaries coming online would help boost their wholesale revenues, but that has not quite played out here at VRNOF (or at the very least, price compression has more than offset any wholesale gains). Management noted that they have been able to avoid “irrational discounting” in Florida and have maintained just over 10% total market share by volume. I remind readers that Florida is still a medical-only state. On the conference call , management noted that sales in Florida were “roughly flat year-over-year.”

2023 Q2 Presentation

VRNOF noted that in states recently turned on for adult-use, those being Connecticut, Maryland, and New Jersey, it was still seeing strong results. Whereas Illinois and Florida may have been the main drivers for cash flow, these markets are now the main drivers of growth. VRNOF notably saw net wholesale revenue grow by 50% in New Jersey and it is ranked as the top brand in the state, with 21% market share. It is unfortunate that price compression has spoiled the party.

2023 Q2 Presentation

VRNOF ended the quarter with $102.6 million in cash versus $420.4 million in debt. This is a highly leveraged balance sheet, though I note that VRNOF still has considerable unencumbered real estate that it can use to bring in capital through sale leaseback transactions.

2023 Q2 Presentation

Even after accounting for the high interest expenses and high corporate tax rates (280e taxes), VRNOF was still generating positive free cash flow (as defined as adjusted EBITDA minus interest and tax expenses).

2023 Q2 Presentation

Management gave guidance for up to $75 million in free cash flow this year. It remains to be seen if that confidence proves misguided, but if the company can deliver on such a goal, this would be quite impressive given the extent of price compression. I note that the stock is trading at market cap roughly 14x that number.

2023 Q2 Presentation

VRNOF generated around $24 million in free cash flow year to date, implying that the second half should see considerable strength.

2023 Q2 Release

On the call, management expressed optimism regarding their being awarded one of five vertical licenses in Alabama’s new medical program. That license would have allowed them to operate a cultivation and processing facility along with five dispensaries. But after a re-assessment of the awarded licenses , VRNOF was surprisingly left out of the licensing process. VRNOF will have to wait for the next round of licensing.

Management noted that New Jersey and Illinois removing 280e taxes at the state level has helped offset some pricing pressures. Recall that U.S. cannabis operators are unable to deduct operating expenses from the calculation of taxable income, leading to excessively high corporate income tax rates. Some operators pay income tax in spite of operating at a loss.

Management noted a goal of bringing inventory down to 90 days, with the company currently operating at around 109 days.

Regarding capital allocation, I was disappointed by the commentary on the call. Management listed M&A as their top priority, stating that they want to “have a little bit of a war chest” to facilitate potential M&A. In my view, management is out of touch with what is needed at this point, at least in this regard. With VRNOF generating a slim 5% free cash flow margin thus far in 2023 due to high interest rates and 280e taxes - all in spite of being one of the leaner operators in the industry - I find it confusing for management to be looking for more M&A. While certain tuck-in acquisitions may make sense if they can lead to reduced OpEx and increased cash flow, historically M&A has been a destroyer of shareholder capital (just look at what happened at Trulieve ( TCNNF )). Management did note paying down double-digit yielding debt and taxes as a second priority, so as a shareholder I can hope for management to eventually prioritize debt paydown. Management stated that “all options are on the table,” including share repurchases, but I am of the view that debt paydown is the only responsible option at this point.

Is VRNOF Stock A Buy, Sell, or Hold?

As of recent prices, VRNOF was trading at distressed valuations, with the stock trading just over 5x adjusted EBITDA. It makes sense that the stock trades at a discount to GTBIF as that name is GAAP profitable, but the discount to Curaleaf ( CURLF ) does not make sense, at least to yours truly.

{kind=link}

It can be hard to make an argument that this is a value stock given the negligible free cash flow generation. But I am of the view that with a lower debt position, VRNOF would not be trading as low as 5x adjusted EBITDA. While it is painful to say, I would be highly bullish if the company announced equity offerings with the aim of paying down debt, as that is arguably the most direct catalyst (under the company’s control at least) to creating shareholder value. Yes, equity offerings would dilute shareholders, but the presence of the highly leveraged balance sheet means that the company is constrained from investing in growth CapEx and the company may eventually have to issue debt or equity just to pay for interest expenses, assuming price compression continues. If the company were to “bite the bullet” and reduce debt aggressively, then it may be able to operate on a more sustainable basis. There is a notion that VRNOF can take advantage of market sector weakness due to being one of the larger operators, but I am unable to see how it can take advantage given that its balance sheet is arguably already maxed out. I can see the stock trade at 15x to 20x adjusted EBITDA at some point, but not with the debt load as high as it is.

The main catalyst on the horizon is if the DEA moves forward to de-schedule cannabis to Schedule III following a recommendation to do just that by the HHS back in August. As I wrote in a prior report , this move would in theory eliminate 280e taxes (thus dramatically boosting free cash flow), lower cost of capital, and lead to higher equity valuations. It is worth noting that VRNOF has given up much of its gains since that announcement in August.

What are the key risks? It is possible that price compressions do not ever end. The main issue is that VRNOF and other legal operators are competing with the illicit market, with the latter not having to pay the same 280e taxes as well as being able to import product from California, where it is cheaper to cultivate and process cannabis. If state governments do not act swiftly enough on the illicit market, if ever, then VRNOF may see its profit margins eventually turn negative even on a unit level basis. Another risk is that of execution - I have already discussed my view with regards to debt and balance sheet management. It is possible - if not likely - that management does not share the same views as I do and may seek to expand their business through more debt-fueled acquisitions. It is possible that some M&A can work for shareholders, but I would be concerned about the toll on the balance sheet.

Absent a painful equity raise, there aren’t catalysts in management’s control to turn things around - decriminalization of cannabis at the federal level may help to address 280e taxes and allow for institutional capital to flow into the sector, but we are all at the mercy of our politicians. The stock is nonetheless very cheap here and there is a clear path to discovering that value for shareholders (through paying down debt as discussed earlier). As one of the larger operators, VRNOF in theory should have a greater chance of surviving this storm, but there’s the risk that this is a game with no winners. I reiterate my strong buy rating but note that this is mainly due to valuation and that position sizes should be small given the elevated risk.

For further details see:

Verano: High-Risk, High-Reward Name In U.S. Cannabis