CRLBF - Verano Holdings Faces A Challenge

2023-03-20 11:37:52 ET

Summary

- I have followed Verano Holdings Corp. since it went public in early 2021, close to the market peak for the cannabis sector.

- I like the company, but I don't include it right now in my model portfolios.

- I think that there are better options for cannabis investors than Verano Holdings right now.

I have been following cannabis stocks for 10 years now, and I like the cannabis industry's growth prospects ahead. I find the stocks to be very beaten up and attractively priced, but this past year or so has left me cautious about prices improving quickly.

I really like Verano Holdings Corp. ( VRNOF ) and find it to be cheap, but I don't include it in either of my two model portfolios at this time after exiting my positions in both the Beat the Global Cannabis Stock Index model portfolio and the Beat the American Cannabis Operator Index model portfolio.

In this piece, I explain why I think Verano Holdings could go lower near-term and how other stocks are more attractive to me right now.

Operations

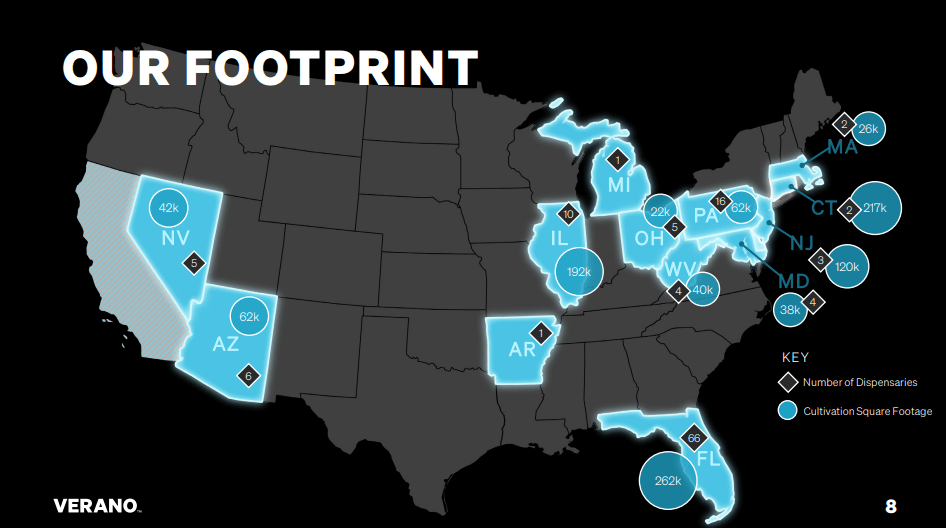

Verano, the last of the 5 largest multi-state operators, or MSOs, to go public, is based in Illinois, like Cresco Labs ( CRLBF ) and Green Thumb Industries ( GTBIF ). Right before going public, the company merged with a big private operator in Arizona and Florida, AltMed. The company doesn't break down revenue by state, similar to its peers, but it's pretty clear that its footprint is very similar to Trulieve ( TCNNF ), with big exposure to Arizona, Florida and Pennsylvania. The investor deck from early March shows that it is broader:

{kind=link}

Overall, the company operates 14 cultivation and production facilities and 125 open dispensaries in the U.S. 66 of those dispensaries are in Florida, where its chain of stores ranks second behind Trulieve with a 12% share of the total 546 open stores. Florida is medical-only currently, but Arizona is medical and adult-use. It operates 6 stores there. Pennsylvania, which is also medical-only, has 16 Verano stores currently.

Clearly, Verano Holdings is focused on the big states for Trulieve, which also doesn't break down revenue geographically. Trulieve is in several of the other states in which Verano operates, including Connecticut, Maryland, Massachusetts, Ohio (no revenue yet) and West Virginia. The states in which Verano operates outside of the Trulieve states are Arkansas (1 store), Illinois, Michigan (1 store), Nevada and New Jersey.

The company's brands are designed to cover all formats and formulas, and the company has a reputation for doing well in premium flower. It sells its own products in 11 of the 13 states in which it operates (not in Michigan or Arkansas).

Management

CEO George Archos is unlike his peers among large MSO CEOs, as he has run a business before. The others tend to be financial types, like the CEOs of GTI and Curaleaf ( CURLF ), or lawyers, like Cresco Labs or Trulieve. Archos is a seasoned restaurateur, starting as a young man in 2001 after graduating college. He co-founded a chain of 4 Wildberry Pancakes and Cafe locations in the Chicago area. Later, he launched the predecessor for Verano in 2014. He owns about 57 million shares . Archos serves as Chairman of the Board as well.

Archos was helped by Sammy Dorf, a lawyer in Chicago who isn't a director or an officer of the company. He served as President until early 2021. His stock ownership isn't disclosed. The current President is John Tipton, who came from AltMed and owns 2.3 million shares. Brett Summerer joined the company near the beginning of 2022 to serve as CFO. His worked as U.S. CFO for Kraft Heinz before joining Verano, and worked as a Division Controller at Corning before that. The COO is Darren Weiss, who also serves as General Counsel. He joined the firm in 2017.

I don't have a strong view one way or the other on this management team. The company has discussed that it didn't spend enough to upgrade its team. So, the high margins I discuss below may be at risk, but the company could also fail to execute well. On the last conference call, the CFO talked about adding to the finance and accounting teams.

Financials

Verano filed its Q3 10-Q with the SEC in November. During the quarter, it saw sales rise 10% from a year ago to $227.6 million. This was up 2% sequentially. The gross margin improved from 47.6% to 54.0%. Operating income expanded by 61% to $37.1 million. Adjusted EBITDA was reported at $82.1 million, a leading margin of 36.1%. The company generated $21.7 million from its operations.

For the first three quarters, revenue of $653.5 million has increased 18% from a year earlier. The gross margin of 48.9% has increased from 42.1%. Operating income has increased 30% to $45.8 million. Adjusted EBITDA has gained just 1% to $244.9 million, a very high 37.5% margin. Cash flow from operations has been $65.3 million. The company spent $109.7 million on capital expenditures in the first three quarters and guided to spend another $20 million in Q4. For 2023, it has guided to $25-50 million. This guidance was conveyed in the conference call for Q3 financials .

For 2023, analysts currently project that the company, which will report its Q4 financials near the end of March, should generate revenue of $1.01 billion, up 14%. Adjusted EBITDA is expected to increase 9% to $348 million.

The Chart

Verano is down the least of its peers in 2023:

YCharts

The performance is in line with GTI and slightly better than Cresco Labs. The worst is Curaleaf, which I pointed out as overvalued relative to peer s two months ago (it still is). The performance of Trulieve, which I really like and include in both my model portfolios, has been almost as bad. These 5 names that represented 20% of the New Cannabis Ventures Global Cannabis Stock Index at year-end, are down an average of 11.5% so far in 2023, while the index has dropped 9.0%.

Juxtaposed against the returns from 2022, the year-to-date returns look like a reversal, as Verano was the worst and Curaleaf was the best large MSO last year:

YCharts

I have discussed previously the fact that AdvisorShares Pure US Cannabis ETF ( MSOS ) owns so much of Curaleaf and GTI that it creates a lack of diversity and risk for not only the exchange-traded fund ("ETF") but for the entire market. Currently, MSOS holds 25.7% of its portfolio in GTI and 20.0% in Curaleaf. The ETF, which has seen the redemption of 12.8% of its shares since mid-December, likely will not be adding to large MSOs, which total 79.1% of the fund currently. If it receives more redemptions, it could need to sell some of these names. Verano is the 4th-largest holding currently at 10.8%.

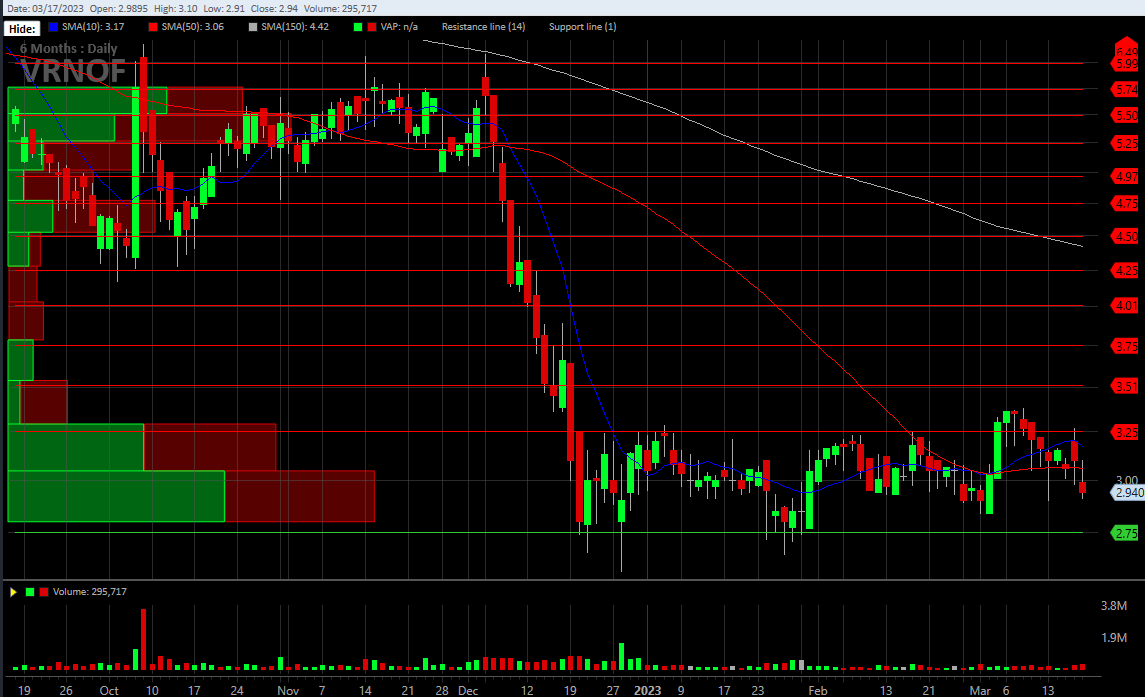

Looking at the chart of Verano, I am very concerned that the bottom may not be in:

Charles Schwab StreetSmart edge

{kind=link}

It's down a lot since the spike in December, but the volume has been very low in the name (and the sector).The stock is currently a little below the falling 50-day moving average of $3.06 and has support at $2.75 in my view. I am not counting on that level holding if it breaks down.

Valuation

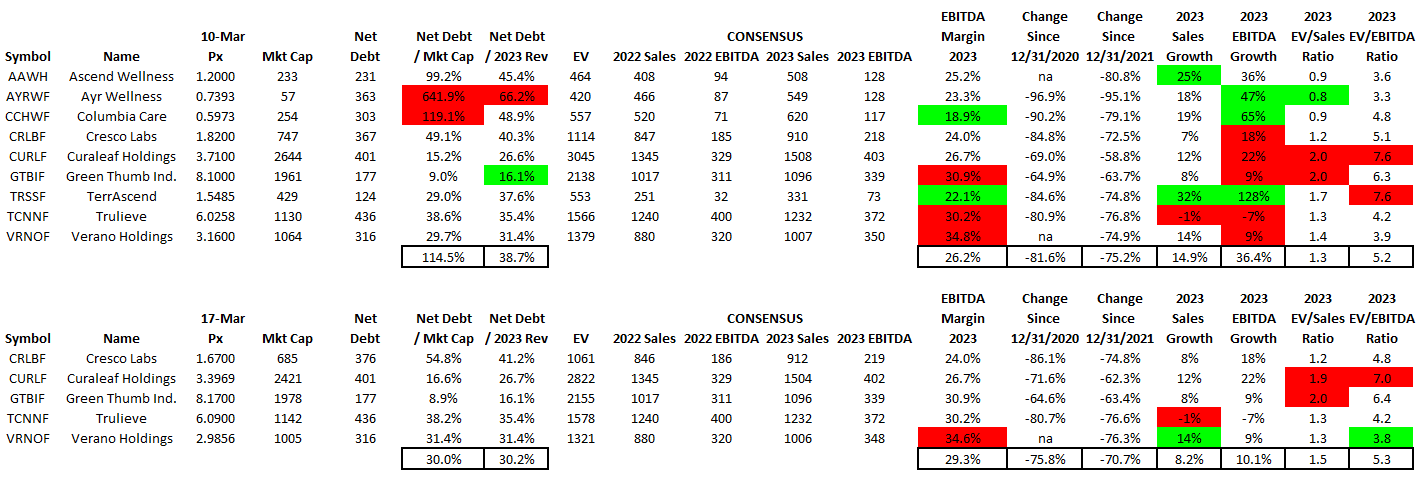

Verano is cheap based on current expectations! Looking at the 2023 estimates, the stock trades with an enterprise value just 3.8X projected adjusted EBITDA. This is the lowest of the 5 largest MSOs. The enterprise value to projected revenue is just 1.3X, which is tied with Trulieve for the 2nd-lowest among the 5 largest MSOs, but there are some Tier 2 MSOs that trade lower on this ratio.

Here is a valuation table for the 5 largest MSOs:

{kind=link}

Verano stands out for its projected EBITDA margin in 2023 of 34.6%, which is the highest and well above the average. It also has the highest projected revenue growth at 14%, which is above the 8% average.

I question what is the lowest valuation relative to adjusted EBITDA because I fear that revenue projections may decline as well as the adjusted EBITDA margins, just like they did already for GTI and Trulieve, which reported earlier this month. GTI saw its 2023 revenue estimate fall from $1.18 billion to $1.10 billion, a decline of 7%. Worse, projected adjusted EBITDA declined by 9%. Trulieve's revenue estimate fell 11%, and the expected adjusted EBITDA is now 13% lower.

Verano has 10 stores in Illinois, and GTI is big there and in Pennsylvania too, so the drop in expectations at GTI matters I think. Worse, Verano's footprint is very similar to Trulieve. The good news for Verano investors is that the stock is already trading pretty cheap to the adjusted EBITDA that is currently forecast. In fact, if it were to drop by 10%, Verano's enterprise value relative to it would still be the lowest (tied with Trulieve at 4.2X).

As I look out, I think that the 2024 estimates will drive the year-end valuation. I think that the current estimates for Verano are too high at $1.11 billion revenue and adjusted EBITDA at $367 million, a margin of 33.0%. I think that revenue could be lower, perhaps by 10%. This would be $998 million. I think that the adjusted EBITDA margin could drop to 31%, which would suggest adjusted EBITDA of $309 million. Using these lower numbers and applying a 7X ratio to the adjusted EBITDA yields an enterprise value of $2.16 billion. This works out to $5.48 for the stock, 83% higher. I shared a target for Trulieve of $12.30 in late February before it reported using the same 7X ratio for enterprise value to adjusted EBITDA at a discount that worked out to be pretty correct. This price is now currently $12.80 based on the current projected adjusted EBITDA of $405 million, which is 14% lower than the estimate ahead of its report. I currently project a 110% gain for Trulieve, which is better than my expected gain for Verano.

Conclusion

I really like Verano Holdings Corp., but I don't own any in my model portfolios for two reasons.

My first reason is that the valuation isn't great relative to peers, especially Trulieve and some of the smaller MSOs. I have written about Columbia Care ( CCHWF ), which is trading at a huge discount to the price implied by the pending Cresco Labs acquisition. The stock has underperformed Cresco Labs since I wrote about it, but I still expect the merger to go through, perhaps at a lower ratio. This past week, I wrote about Ascend Wellness ( AAWH ) and suggested it could rally to $2.24 at year-end, up now 88%. My target is based on a lower multiple than I am using for Verano despite what looks like greater growth prospects. Also, unlike Verano, which is already a big part of MSOS, the ETF doesn't own any AAWH.

Second, the chart doesn't yet look like the low is in. I shared a target, though, that conveys how well I expect the stock to perform over the next year. I expect a dip a head that I can buy in my model portfolios.

While I am a bit pessimistic about the stock price in the short-term, my target for year-end is much higher. For those that like the company for the long-term, I would wait until they report to add to any positions. For those who are actively trading cannabis stocks, I would suggest considering reducing Verano in favor of other names, either certain MSOs or stocks from other sub-sectors.

In my Beat the American Cannabis Operator Index model portfolio, I sold the rest of Verano at $3.04 on March 13th, adding later to two smaller MSOs. I had trimmed some a week earlier at $3.16 to buy Trulieve after it reported the two days later at $6.13, and also trimmed it at $3.01 on February 24th to add to buy Trulieve at $6.15. I first trimmed it on 2/16 at $3.17, reducing Trulieve at the same time at $6.92. I added CCHWF later that day at $0.625.

I reduced Verano Holdings Corp. in my Beat the Global Cannabis Stock index at $3.11 on 2/10, later adding to WM Technology ( MAPS ) at $1.08. I sold the balance at $3.17 on 2/16 and also trimmed Trulieve at the same time at $6.90. That money went into TILT Holdings ( TLLTF ) at $.074, replacing stock I had sold at $0.08 earlier in the month, and into two Tier 2 MSOs.

For further details see:

Verano Holdings Faces A Challenge