CA - Vermilion Energy: Winter Is Here - So What?

Summary

- Vermilion Energy benefits from high energy prices in Europe.

- In Europe, the winter is mild so far, which has not resulted in a further spike in natural gas prices.

- Windfall profit taxes are a headwind, but VET should be highly profitable nevertheless.

Article Thesis

Vermilion Energy Inc. ( VET ) (VET:CA) is a Canadian energy company with some European energy assets which is beneficial in the current energy price environment.

Shares are inexpensive, but the surplus earnings tax in Europe hurts the company's profitability in the near term. Nevertheless, shareholder returns have recently been raised and should rise further going forward.

Company Overview

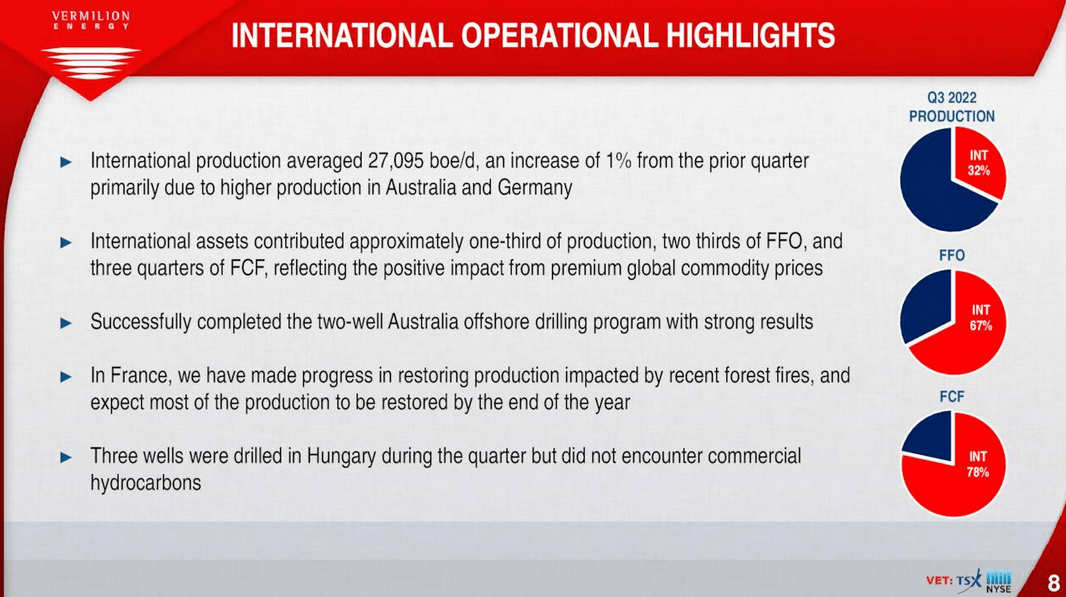

Vermilion Energy is Canada-based, but it operates internationally. The company produced 84,000 barrels of oil equivalent per day during the third quarter, relatively flat from the previous quarter -- 57,000 of that, or around 68%, was produced in North America, with the remainder being produced internationally. This international segment includes assets in Europe, such as in France, the Netherlands, Slovakia, and so on, but also outside of Europe, such as in Australia.

Oil prices are more or less the same around the world, as oil is easily shipped over the oceans at relatively low costs. That does not hold true for natural gas, where ocean shipping is expensive due to a lot of energy being needed to liquify natural gas. On top of that, LNG shipping capacity is constrained, which is why natural gas prices vary a lot from one geographic market to another. In North America, natural gas is pretty cheap, while natural gas prices are much higher in Europe and parts of Asia. That helps explain why Vermilion Energy's European assets are responsible for an outsized portion of the company's profits and cash flows:

{kind=link}

While only one-third of company-wide production is generated outside of North America, those assets contributed more than three-quarters of Vermilion's free cash flow -- natural gas prices being way higher in Europe versus North America makes these assets extremely lucrative in the current environment.

Unfortunately, that's also where Vermilion is running into some problems due to European countries demanding surplus profit taxes, which is why Vermilion had to reduce its guidance this year when these tax plans became more specific.

Strong Cash Flows Thanks To Advantageous Pricing Environment

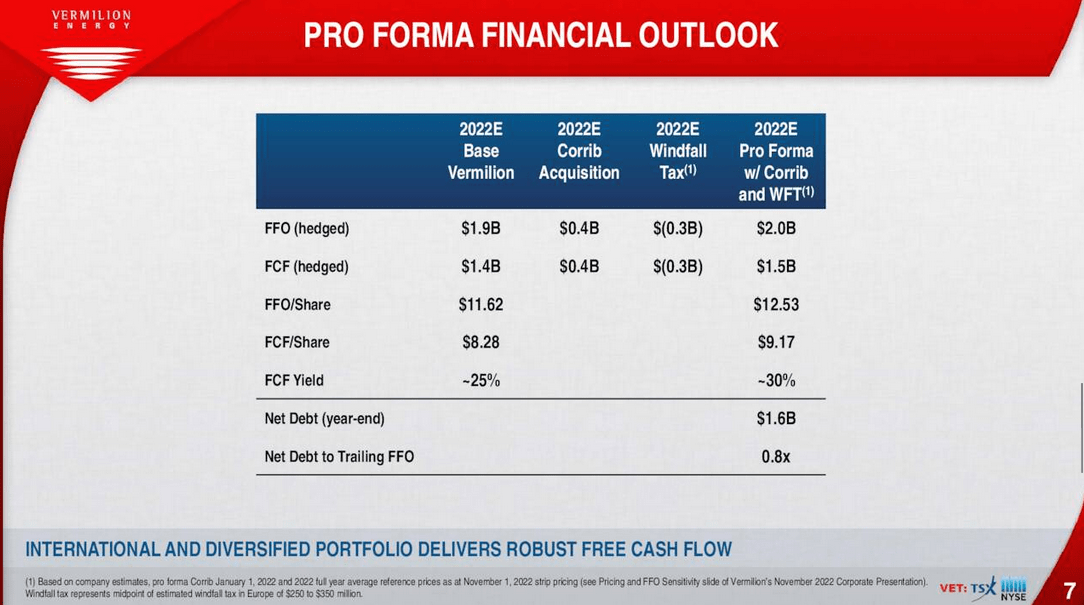

Vermilion Energy is a company that has grown considerably via acquisitions in the past. Recently, for example, the company agreed to acquire a stake in the Corrib Natural Gas Project from Equinor ( EQNR ). That deal was forecasted to be highly accretive immediately, as Vermilion's management planned that this takeover would add meaningfully to company-wide free cash flows and also to Vermilion's funds from operations:

{kind=link}

The deal adds $400 million to Vermilion's FFO and free cash flow, all else equal. Overall, that has made Vermilion assume that the company would generate about $1.5 billion in free cash flow, with windfall taxes already being accounted for. When we translate that to USD (Vermilion reports in Canadian Dollars), we get to free cash flows of US$1.12 billion at current exchange rates. Since Vermilion is valued at just US$2.49 billion, its assumed free cash flow yield for 2022 (final results have not yet been reported) is at a very high level of 45%.

When we also account for Vermilion's net debt by looking at its enterprise value instead of its market capitalization, we get to a free cash flow yield of 36%, which is still very high. The market's assumption here is pretty clear -- Vermilion is priced for a significant pullback in profits in the future. And that makes sense, I believe, at least to some degree. Energy prices in Europe will likely remain elevated versus the level of energy prices in the US or Canada, but with LNG infrastructure being built out on the continent over time, prices will likely not be as high as they were in 2022 forever. Eventually, energy prices in Europe should moderate towards a level that is still higher versus North America, but not as elevated as what we have seen last year. But even if that holds true, Vermilion could still be a very good investment. There are several reasons for that:

First, Vermilion Energy will benefit from the fact that it will be less hedged this year. A lot of hedging was a headwind last year, as Vermilion was not able to fully capitalize on high energy prices, as its sales potential was capped by its hedging activity. As energy prices are still elevated this year, fewer hedges should be a tailwind, all else equal.

On top of that, Vermilion Energy does not need to generate profits and free cash flows at the current level forever in order to be a good investment. In fact, even if its free cash flow were to be cut in half, its free cash flow yield would still be highly attractive, at around 22%. In a scenario where free cash flow falls by three-quarters, Vermilion Energy's free cash flow yield would still be in the 11% range -- far from unattractive.

Right now, analysts predict that 2023 will be more or less equal to the last year:

EBITDA is forecasted to come in at $1.69 billion this year, down 2% from the trailing twelve months figure. EBITDA does not necessarily move in line with free cash flow, of course. Some factors could make free cash flows decline versus EBITDA this year, such as higher costs for maintenance and growth capital expenditures due to inflation, higher wages, and so on. On the other hand, Vermilion's debt reduction efforts result in declining interest expenses, which could be a boost for the free cash flow conversion ratio relative to its EBITDA.

In order to be conservative, let's still assume that free cash flows will decline this year versus 2022, despite EBITDA dropping only marginally. Vermilion has forecasted that capital investments will rise this year, and that windfall profit taxes will be higher this year as well. According to a recent release , the company will generate free cash flows in the C$800 million space this year, which is equal to around US$640 million at current exchange rates. Relative to a market capitalization of US$2.5 billion, that makes for a free cash flow yield of 26% today.

Vermilion's Shareholder Returns

Cash flows this high give the company many options. Generally, cash flows can be used for shareholder returns via dividends and buybacks, organic growth, inorganic growth (M&A), or debt reduction. Vermilion currently plans to focus on debt reduction this year.

Management has recently stated that they plan to return around 25% of free cash flows to investors via dividends and buybacks. The remainder of the company's free cash flows are earmarked for debt reduction. If the US$640 million estimate is correct, that translates into shareholder returns of around US$160 million, or 6.5% of the current market capitalization. The remaining US$480 million, or C$600 million, would be used for debt reduction. Based on the year-end net debt estimate of C$1.4 billion, that would lower Vermilion's net debt to C$800 million, almost down by half in one year.

The 6.5% expected shareholder yield will primarily be driven by buybacks. The dividend is currently yielding around 2%, following a 25% dividend increase in early January. Investors can thus expect that Vermilion will buy back around 4%-5% of its shares this year -- not overly much, but far from bad.

If things go right, investors can expect substantially higher shareholder returns next year and beyond, however:

Analysts are currently predicting that EBITDA will decline only marginally in 2024 and 2025, by a couple of percentage points. At the same time, windfall profit taxes could end after 2023, which would offer a sizeable boost to free cash flows. But even if these taxes were maintained in 2024 and beyond, Vermilion could still generate around US$500 million to US$600 million in free cash flow in 2024 and 2025. The company would have substantially lower debt levels in those years, and could thus return a larger portion of its free cash flows to its owners. Since the free cash flow yield would still be 20% even with free cash flows dropping to $500 million, a 10%+ shareholder yield in 2024 seems quite possible, as there would not be any need for VET to be aggressive with debt reduction at that point.

Takeaway

Winter has come, but so far, it has not resulted in a spike in natural gas prices in Europe. While energy is still pricey on the continent relative to the US and Canada, prices have pulled back to some degree.

Vermilion will still be highly profitable this year, despite the pullback in energy prices versus the ultra-high levels seen last summer, and despite the adverse impact of windfall profit taxes.

Unfortunately, investors will probably not see very high shareholder returns this year, as management is focused on debt reduction. With VET likely offering a 20%+ free cash flow yield in 2024 as well, higher shareholder returns in the next couple of years seem possible, however.

Regulation and taxation in Europe and management's capital allocation policies remain factors to keep an eye on, but with VET paying down debt and trading at a very inexpensive valuation, it's hard to imagine how investors will lose money in the long run with this company.

For further details see:

Vermilion Energy: Winter Is Here - So What?