CA - Vermilion: Ultimate Reality On Capital Returns

Summary

- Vermilion stock should have been a winner in 2022. But it ended the second half of 2022 a disappointment despite having all the reasons to have taken off.

- High taxes, and the selling off of natural gas towards the end of 2022 didn't help.

- But this is the ultimate reality, Europe's energy security isn't solved by 2 weeks of warm weather.

Investment Thesis

Vermilion ( VET ) has been a disappointing stock in the past several months.

There are several reasons why this was the case which is explored in this note.

What's different right now, is that Vermilion has sought to resume its capital return program. Vermilion estimates that it could return around CAD$200 million or 5.6% of its market cap to shareholders in 2023.

And that once its net debt gets closer to $1 billion, down from CAD$1.4 billion as of Q4 2022, it will look to further increase its capital return allocation.

What Happened?

In the second half of 2022, everything that could go wrong for Vermillion went gone wrong.

For example, at the start of 2022, Vermillion's acquisition of Corrib was thought to be completed at some point in H2 2022 . H2 2022 came around. And H2 2022 went. And what about the Corrib acquisition? Not completed.

Now, Vermillion believes that by the end of Q1 2023, Corrib's acquisition will be completed. What's to blame? Administrative delays.

Next, European governments were worried that fossil fuel companies were going to make too many profits. So, they taxed energy companies. A lot.

Lastly, the bitter irony was the weather. Thus, as 2022 progressed, this saw natural gas prices in Europe decline. Put simply, despite having all the reasons why natural gas prices should be high, the facts didn't play out.

On the other hand, I remain convinced that irrespective of where natural gas prices are right now, Europe's structural energy security issues are far from over. Indeed, all the dynamics that got us here in the first place haven't been dealt with.

Simply put, Europe's energy security isn't solved by 2 weeks of warm weather.

With that in mind, let's talk about capital returns.

Vermilion Resumes Share Repurchases

I think anyone that has closely followed Vermilion knows that this management team has been poor capital allocators. On top of that, Vermillion's management team has been less than transparent with its future capital allocation decisions.

Vermillion's management declared they'll buy back shares in 2022. Going so far as to provide a capital return framework.

Then, Q3 came around, and out of nowhere, they decidedly stopped repurchases. Being one of the few natural gas companies to have little in the way of a capital return program, aside from its razor thin 1.6% dividend yield.

For their part, Vermillion's management team contends that this was a necessary action given the windfall taxes. However, given that everyone knew that the windfall taxes were on the cards, this unexpected about-turn was unwelcomed by investors and we saw the stock sell-off.

Vermillion exited 2022 with approximately $1.4 billion of net debt. Vermilion states that for 2023, the vast majority of its free cash flow will be directed toward paying down its debt.

Vermillion seeks to get its debt to CAD$1 billion of net debt, at which point it will increase its capital allocation policy.

For 2023, Vermillion contends that it will increase its dividend by 40%. This translates to a 1.9% yield at current prices. So far, there's very little to entice investors into the stock, right?

Well, this is the crown jewel of the bull case.

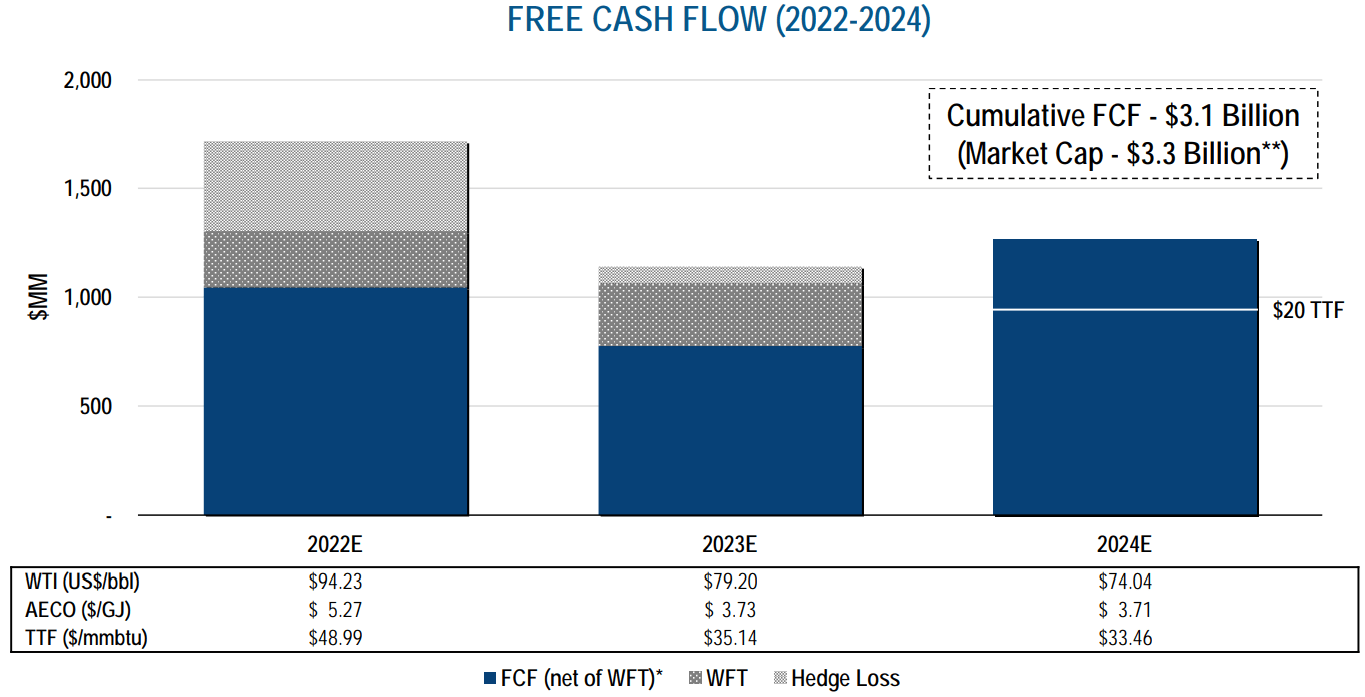

VET Stock Valuation -- 5x Free Cash Flow

{kind=link}

Vermilion maintains that in 2024, it won't have the temporary windfall tax, as that is expected to expire in the next year.

Further, Vermillion forecasts 2023 free cash flow of approximately CAD$800 million including the impact of temporary windfall taxes and hedging losses.

That puts the stock at somewhere around 4x to 5x this year's free cash flow.

The Bottom Line

Vermillion's stocks has fallen out of favor with investors, partially due to troubles of its own making. And partially due to aspects outside of its control. Namely, an unseasonal war winter.

However, keep in mind that the time to buy natural gas inventory isn't in the winter. Natural gas is mostly bought in the summer, when natural gas is cheaper, in preparation for the winter ahead.

That means that the natural gas storage for winter 2022, likely took place largely prior to Russia shutting off its Nord Stream pipelines.

However, for winter 2023, Russia is not likely to be available to replenish low European natural gas inventories.

Hence, Europe's 2023 energy security concerns are far from solved. Paying around 4x to 5x is an attractive risk-reward.

For further details see:

Vermilion: Ultimate Reality On Capital Returns