VSAT - Viasat: Enabling Free Internet In The Skies

Summary

- Given the opportunities offered as a provider of free Wi-Fi for airline passengers in a rapidly growing market, the above -20% slump in Viasat's share price seems unjustified.

- Then, pessimists would point to the clouds of macroeconomic uncertainty, competition with Elon Musk's Starlink, and the negative free cash flow.

- However, there are other positives with the forthcoming launch of Viasat-3, together with the Microsoft contract for rural satellite internet and consolidation of the industry.

- Also, looking at the operating cash flow, backlog, and undervaluation with respect to the IT sector, the stock is an opportunistic buy.

- Using some moderation due to a highly volatile market, surging Covid infection numbers in China, and escalating recession risks in the U.S., I have a price target of $38.

Except if you are an outlier out of touch with technology, a surfer on the lookout for the next wave, or military personnel on active duty, it is highly probable that you have your smartphone at arm-length away in order to scroll its screen for the latest news, a video feed or a quick chat.

Now, think of boarding a four-hour flight with no internet, and having to painstakingly watch some preselected movies.

In these conditions, it is no wonder that Viasat ( VSAT ) has been bagging contracts related to WiFi terminals, that have helped to boost sales by 24% in its second quarter of FY2022 (Q2) which ended in September. However, as shown in the chart below, the stock has suffered by more than $10 or more than 20% since the company reported financial results in the second week of November.

This decline could represent an opportunity and this thesis aims to assess an investment in Viasat by considering macroeconomic headwinds and supply chain-related issues.

I start with the company's positioning in the airline industry where it competes with Elon Musk’s Starlink ( STRLK ) satellite network which is part of SpaceX ( SPACE ). There are also others like HughesNet, a wholly-owned subsidiary of EchoStar ( SATS ).

Obtaining Airline Contracts Amid The Competition

For Delta Air Lines ( DAL ), providing free wireless internet service for its passengers amounts to gaining a competitive advantage over some competitors such as Southwest Airlines ( LUV ) and American Airlines ( AAL ). Now, Delta already offers free internet to frequent flyers (Delta SkyMiles members) but has extended the service to everyone boarding its Airbus A321, 737-900ER, and 757-200 planes. For those not wishing to become members but still wanting to avail of the internet facility, an amount of $5 needs to be paid. Looking further, AAL, whose aircraft are also equipped with Viasat gear also plans to extend its offer of free WiFi to all passengers.

In these circumstances, there are opportunities for Viasat, by taking advantage of competition in the airline industry as stakeholders aim to make the internet freely available in the skies throughout the world.

{kind=link}

Shifting to a more cautious tone, there are also fears that the domestic market is getting saturated and more competitive too with Elon Musk’s SpaceX set to play a major role in the IFC (inflight communications) market. It has already signed an agreement with Hawaiian Airlines ( HA ) and JSX Airlines for this purpose.

Now, knowing Elon Musk’s ability to have disrupted fields like automobiles with Tesla ( TSLA ), rocket launching, and satellite-based communications with Starlink, it is logical for investors not to be over-enthusiastic about Viasat, but, over-pessimism is also not justified.

Viasat Amid Industry Consolidation

The reason is that we are still far from a scenario where SpaceX grabs market share from Viasat which already has a large installed base for IFC as an incumbent. Also, subject to regulatory approvals, its $7.3 billion merger with U.K based Inmarsat will reduce the mobile satellite communications services industry from three major players to two including Luxemburg-based Intelsat . Now, the latter bought Gogo's ( GOGO ) commercial aviation business back in August 2020 as part of the latter's Covid-driven restructuring. Gogo now focuses on 5G and business aviation in more of what can be termed a niche market style.

Therefore, this is an industry that is consolidating.

It is also one where most of the attention is on SpaceX's ability to provide global coverage with the FCC providing it the go-ahead to launch 7,500 satellites in Low Earth Orbit, despite Viasat's objection. But, there are questions as to the quality, namely the 350 Mbps per aircraft speed that Starlink intends to provide when considering that in an aircraft there are many users located at a concentrated location in contrast with satellite-based home internet where users are more dispersed. Thus, this should be more of a case where airlines will first observe SpaceX's ability to deliver on its promises, before committing.

{kind=link}

Furthermore, with the launch of the three ViaSat-3 communication satellites to cover the Americas, EMEA, and the Asia Pacific region, the company will increase bandwidth (internet speed), but at a reasonable price in terms of the “ best bandwidth economics in the industry ”.

Therefore, as airlines expand their free WiFi coverage throughout the world while also considering cost dynamics, expect Viasat to obtain more contracts like the one exemplified by China’s Sichuan Airlines for its A320 aircraft. This time, the Viasat terminal installed on the aircraft will connect to Chinese Satcom's Ka-band satellite network in order to provide the IFC service including video streaming, web browsing, messaging, etc.

These contracts should generate a sustained revenue stream, but, it is also important to assess how the company will perform with economic slowdown concerns escalating into recession risks in the first half of 2023.

Revenues And Backlog

The company missed both revenue and earnings expectations in Q2 while lowering its FY2023 expectations due to its aviation clients getting fewer aircraft deliveries from manufacturers, in turn being impacted by supply chain issues. This should adversely impact Viasat's revenues, and additional inflation-driven costs to be incurred in production and delivery will also weigh on earnings.

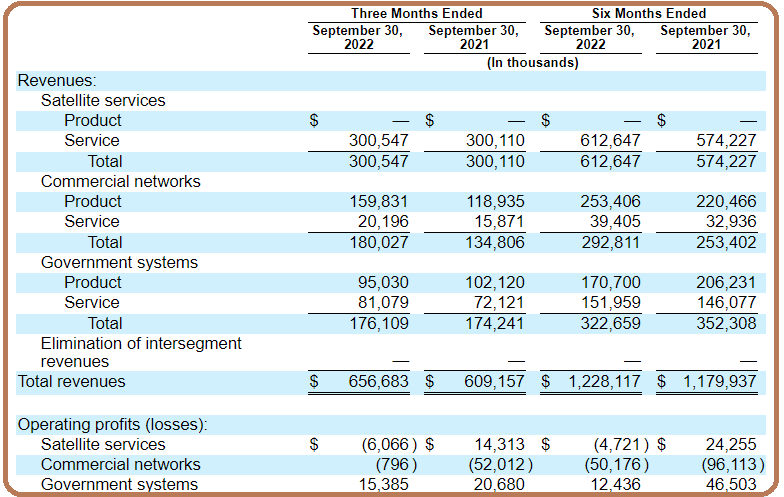

Switching to a positive tone, the company can rely on its Government Systems segment which, while not necessarily seeing the same level of growth as the Commercial Networks one, is profitable and raked in $15.4 million of operating profits in the last reported quarter, as shown below.

Segmental revenues and operating Profits for Q2 (Seekingalpha)

{kind=link}

Pursuing further, driven by IFC equipment deliveries and ground antenna systems, revenues for the Commercial Network segment which includes airlines are delivering better revenue growth than government systems and satellite services.

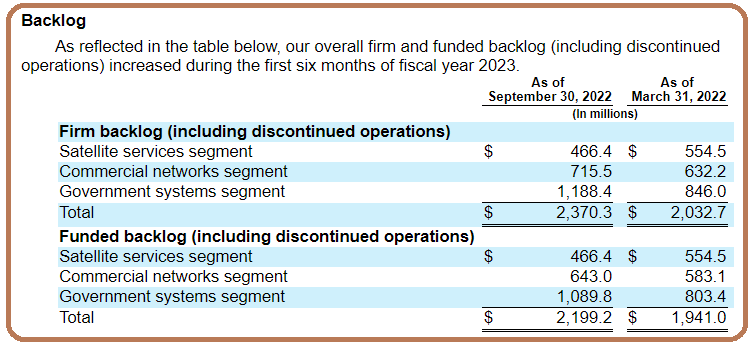

One important factor to watch out for during economic slowdowns for this communications equipment business is future revenue visibility, in the form of the $2.37 billion funded backlog as of the end of September, which included $1.1 billion in new orders. This backlog represents more than 80% of FY2022 revenues and can, to some extent, cushion Viasat's finances in case of acute turbulence as seen during the Covid lockdowns.

{kind=link}

Furthermore, looking into the balance sheet , the sale of Link16 to H3 Harris for $2 billion should reduce the debt which stood at $2.88 billion (net cash) in Q2 (end of September). This divestiture should prove timely in reducing debt related to the Inmarsat acquisition, which is currently being scrutinized by regulators in the U.K.

Cash Flow And Valuations

Now the company has improved its cash from operations on both on a year-on-year and quarterly basis. But its capital expenses remain high, namely due to the launch of the Viasat-3 which explains why its free cash flow is negative . In this respect, according to the management, this should change after the launch of the Viasat-3 for the EMEA region which is expected for the summer of 2023, soon after the Americas one in the first quarter . Therefore, there are chances that the FCF could turn positive in 2023.

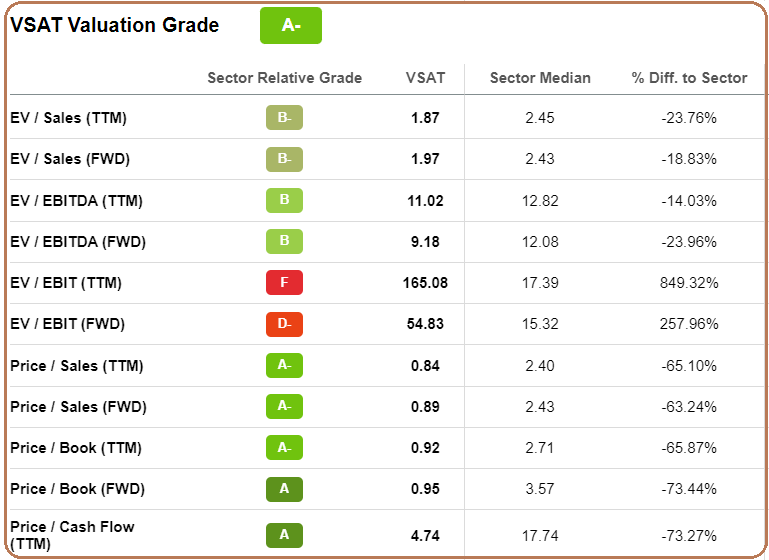

Therefore, for a value investor keen on the free cash flow metric, it may be preferable to adopt a wait-and-see posture. On the other hand, for someone looking for an undervalued stock based on several metrics including the Price-to-Operating Cash flow multiple of 4.74x which is 73% below the valuation for the IT sector (table below), it may just be the right time to buy.

{kind=link}

Adjusting for a 20% upside, I obtain a target of $38 (31.74x1.2) based on the current share price of $31.74.

To support my bullish stance, the stock could also benefit from momentum factors as the Falcon rocket which will launch its satellites into space has an impressive track record. Moreover, the expectation is for additional contracts, both new and for upgrades as Viasat increases its fleet of active aircraft by about 500 over the remainder of this fiscal year. To put things into perspective, airlines catering to passengers' internet needs should result in the in-flight Wi-Fi services market growing by 12.5% from 2022 to 2023 alone.

Concluding With The Microsoft Deal And Caution

The above bright picture which I have painted could be tainted by deteriorating macroeconomics, but, remember that Viasat disposes of a backlog plus a profitable government business too. On top, the company is active in satellite-based internet for rural areas where the cost of laying fiber and even installing antennas for mobile coverage is prohibitively expensive. In this case, the company has signed an agreement with Microsoft (NASDAQ: MSFT ) for covering a total of 10 million people across Africa and the world by 2025. This number is nearly 17 times the 590K subscribers Viasat had for its residential internet service in 2021, and the fact that it was chosen by the software giant instead of competitors gives credence to the company's technology.

Therefore, in case there are launch delays as there usually are for such types of endeavors, supply chain issues signifying fewer aircraft to be fitted with WiFi terminals, or some airlines limiting their enthusiasm for providing free internet in the skies as a result of surging Covid numbers in China, the company can rely on its rural satellite internet to power longer-term growth. However, in the short to medium term, expect the stock to suffer depending on how adverse news hit the market.

Finally, the $38 price target may seem on the low side given the opportunities, but, one must not forget that we are facing highly volatile market conditions, where it is better to be cautious. Along the same lines, in case there is no upside due to some launch delay for the Viasat-3 in the first quarter, it may be better to sell the stock with the aim of limiting losses.

For further details see:

Viasat: Enabling Free Internet In The Skies