VTRS - Viatris: Developing Into A Fantastic Investment Opportunity

2023-07-18 00:28:43 ET

Summary

- Viatris Inc. has a low valuation with a forward P/E of under 4 and a market cap of over $12 billion, predicted to reach $15.75 billion in revenues by 2023.

- The company recently acquired Oyster Point Pharma and Famy Life Sciences, expanding its exposure to the eye care market, and has a strong free cash flow (FCF) for further acquisitions.

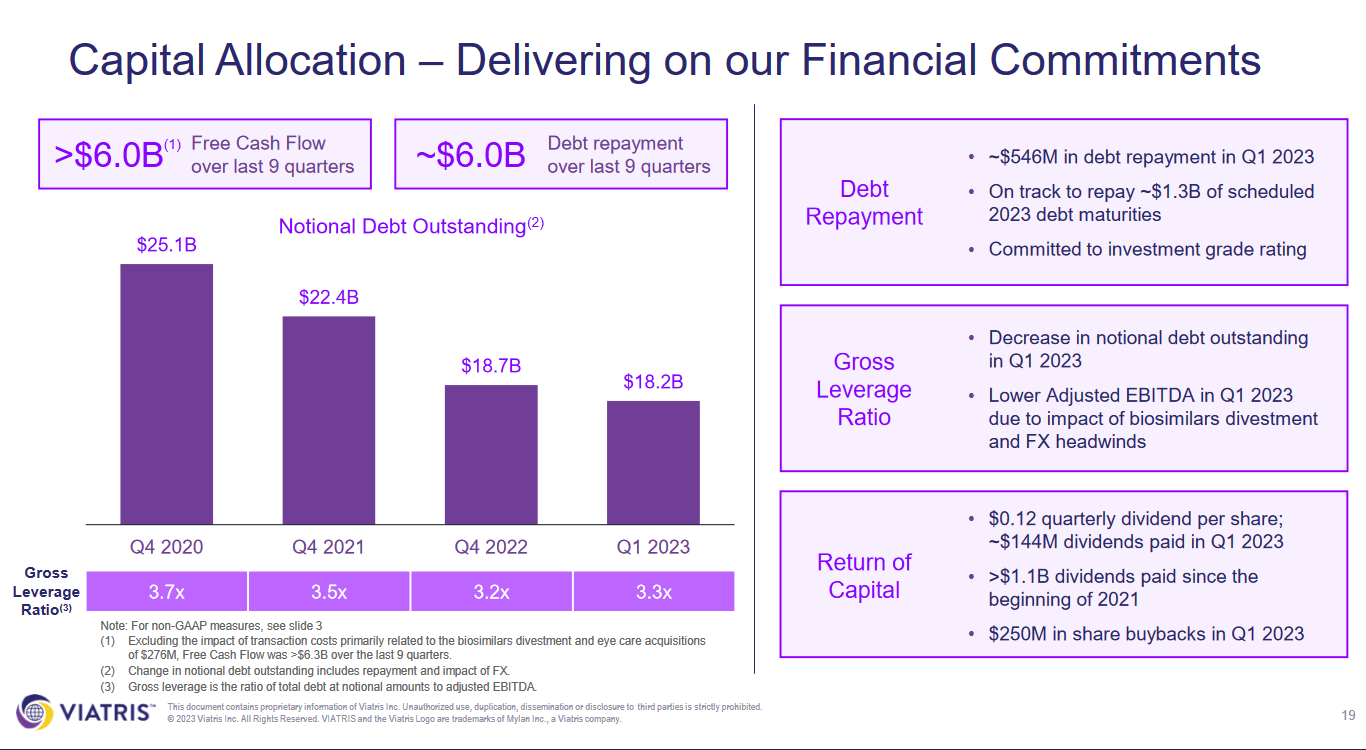

- Despite a significant debt burden, Viatris has managed to reduce its long-term debt by over 25% through strategic divestitures and strong FCF generation.

Investment Outline

Viatris Inc ( VTRS ) has received a low valuation with a p/e of just under 4 on a forward basis. The company operates as a healthcare company with an international presence. The market cap is sitting at just above $12 billion ad in 2023 they predict they will be reaching $15.75 billion in revenues. With solid margins and an FCF yield only increasing it's hard to view VTRS as a risky investment right now.

The fundamentals are fantastic and the management has a clear plan on which they are executing efficiently to further expand. If VTRS receives a higher valuation as a result of successfully performing their expansion plans then the upside here is huge. Even if they don’t get a higher multiple they offer a near 5% dividend yield and spent $250 million in buying back shares in Q1 2023 . Rating VTRS a buy here.

Recent Developments

Perhaps not that recently, but back in January of 2023 VTRS completed an acquisition of Oyster Point Pharma and also for Famy Life Sciences. This is presenting VTRS with additional exposure to the eye care market. The market here is expected to continue posting decent YoY and by 2032 will have achieved a 7.3% CAGR. According to some reports, there are more than 1 billion people currently living with vision impairments, and a large portion lack access to proper help with it. This acquisition presents VTRS with more market share here and should be beneficial to the earnings in the long run it seems.

A comment from the Viatris CEO Micheal Goettler highlighted some of the reasons for the acquisition, “Viatris has created a performance-driven, highly engaging and inclusive culture and we are pleased to welcome our talented, new colleagues to our team. We look forward to continuing to execute against our announced strategic objectives in 2023 that we expect will position Viatris for future growth”.

With the size of VTRS right now they are in a position where it makes more sense almost to expand through measures like this, rather than spending vast amounts of capital on R&D expenses. With FCF of nearly $1 billion in Q1 2023 as well, they seem fit to be very liberal with making further acquisitions if they’d like.

Margins

The margin profile of VTRS right now is a real highlight I think when viewing the company. Margins are solid and seem to have been growing at a solid rate over the last several years.

Margin Profile (Seeking Alpha)

The FCF is what I am looking at primarily. This is what gives me an idea about the future potential for a dividend increase. The payout ratio for VTRS is just 15% right now and I think there is more room for the upside. Comparing FCF to 2022 for the first quarter we see it dropped by 15%, but the capital expenditures also dropped, 26% that is. This helped offset some of the losses and ultimately still makes VTRS a cash flow machine that is capable of distributing a high dividend. With a strong portfolio of brands, I think VTRS is still in an excellent position to leverage this and maintain margins in the coming quarter similar to what is shown above here.

Value For Investors

For investors that are looking at VTRS, the biggest appeal I see for them is the dividend yield and the buyback program the management has established. That is the primary way for VTRS to return value to investors. The yield sits at nearly 5% and VTRS is starting to buy back shares as well, spending $250 million in the first quarter of 2023 on it.

{kind=link}

Going into Q2 2023 I think investors should be looking for VTRS to maintain this current trend of diverting a lot of capital to investors, but also paying down debt. A gross leverage ratio of just 3.3 is quite healthy I think and we are just going lower.

Valuation

DCF Model (Author)

As has been made clear already, I view VTRS as an undervalued company right now that deserves a higher multiple. The DCF model above shows that the share price is trading below what is considered the intrinsic value of $10.3 per share. I have put on a terminal 8% growth rate for the FCF but I think if margins continue to expand and they make more acquisitions we might see a growth rate of 10% instead. Historically the FCF growth has been 18% annually over the last 10 years. I think that is incredibly hard to continue to achieve and a lower amount seems more reasonable. Besides it's generating enough FCF to support the current dividend with ease and more FCF would be diverted to paying down debt I think. Trading below what I find to be the intrinsic value supports the buy case right now. If the share price corrects to my $10.3 target we have a 3% upside, paired with a yield of 4.7% creates a near market return here. I am also applying a 15% discount rate to the model which is my preferred MOS.

Risks

The company is currently facing a significant challenge in managing its debt burden. However, it's worth mentioning that the company has made commendable progress in reducing its long-term debt by over 25% through strategic divestitures and strong free cash flow generation. In 2022 alone, the company managed to pay off more than $3B of its debt, showcasing its commitment to deleveraging.

Interest Expense (Earnings Presentation)

The current business environment presents a unique opportunity for companies to explore the M&A market, and reducing the debt burden may enable the company to take advantage of potential growth opportunities through strategic acquisitions. However, careful financial planning and prudent management will be essential to strike the right balance between growth and debt management in this dynamic landscape.

Investor Takeaway

VTRS has been able to very impressively diversify its portfolio over the years and now boasts a strong set of revenue streams. The valuation of the business is however quite pessimistic with a p/e under 4 as the company is transforming itself. There seems to be a fear that margins and FCF could be hurt. But I think the downside right now seems so limited that investment, in the long run, will yield very substantial returns.

The management is also introducing a buyback program and spent $250 million in the last quarter on it. Having exposure to the healthcare sectors I think is very important for investors seeking a diversified portfolio. Viatris offers that and I am rating it a buy as such.

For further details see:

Viatris: Developing Into A Fantastic Investment Opportunity