VTRS - Viatris In 2024 May Be The Most Polarising Investment Opportunity In Pharma

2024-01-14 08:04:48 ET

Summary

- Viatris stock has been on the rise, up over 20% in the past month, reaching its highest price since February 2023.

- The company's revenues are derived from established brands, generics, and complex generics, with a significant portion coming from patent expired drugs.

- Viatris faces challenges in growing its generics business to offset declining revenues and is heavily indebted, which may impact its profitability and value proposition.

- Viatris is a tough business to value - shares are seemingly cheap, until you consider the shrinking top line revenues, and ~$17bn of debt.

- This could be one of the toughest investment decisions in Pharma - I am prepared to hold long term to see how things pan out, but the risks around such a strategy need to be highlighted. Management could send the business into a tailspin.

Investment Overview - Viatris A Pharma Of Global Significance

Shares in Viatris (VTRS), the company formed in 2020 via a merger between New York Pharma giant Pfizer's ( PFE ) Upjohn legacy asset division, and Netherlands headquartered generic drug giant Mylan, have been on the rise in recent weeks - up >20% across the past month. Current traded price is $12 per share, the highest price since February 2023.

Viatris stock was worth ~$16 per share post listing in November 2020, so investors who have been holding shares long-term are down ~25%, although Viatris' dividend of $0.12 per quarter, or $0.48 per annum, provides some comfort, yielding ~4% per annum presently.

~64% of Viatris's revenues, which are expected to reach $15.4 - $15.6bn in 2023, are derived from its established brands / Upjohn division, which includes patent expired drugs such as Viagra, Lyrica, Lipitor, Celebrex, and Epi Pen, with 32% coming from the generics business, and 4% from the "Complex Generics ("Gx") business.

In total, Viatris markets and sells >1,400 approved molecules, manufactured at 40 different sites globally. ~34% of the company's business is in Europe, 26% in the US, 17% in emerging markets, 14% in Greater China, and 9% in Japan, Australia and New Zealand (the "JANZ" region).

Is Viatris Stock Expensive Or Cheap? Smoke and Mirrors Valuation Disguises Some Unsettling Truths

At first glance, it is hard escape the conclusion that Viatris stock is exceptionally cheap. For example, Viatris' market cap - presently $14.3bn - is lower than its forecast revenue for 2023 of $15.5bn, giving the company a price to sales ("P/S") ratio of <1x. This is a rare phenomenon which is often interpreted as a sign of a company being undervalued, or, as a potential red flag - if the valuation is so low, there must be hidden problems at the company.

Viatris is also a profitable company - as the company's CEO Scott Smith, formerly President and Chief Operating Officer at Celgene Corporation, pointed out via a presentation given during a fireside chat at the JP Morgan Healthcare conference this week, the company has generated ~$7.2bn of free cash flow across the past 11 quarters, and expects to generate ~$2.3bn of annual free cash flow going forward.

If the company's top and bottom line performance is strong, as Viatris' appears to be, then, again, it would suggest the company is either substantially undervalued, representing a "screaming buy" opportunity (as I concluded back in June 2021, in a note for Seeking Alpha ), or that there may be some hidden underlying issues undermining a higher valuation.

The two most important issues to consider in this respect are firstly, that top line revenues are shrinking, and secondly, that the company is heavily indebted.

Ultimately, there was a good reason Pfizer was willing to offload its UpJohn business, and that reason is that the entire division consists of older drugs, with no patent protection, whose revenue contributions were in terminal decline owing to generic competition, new and better drugs, and less emphasis on marketing older drugs.

Viatris' biggest challenge is to grow its own generics and complex generics businesses fast enough to offset falling revenues within the established brands division, to make sure the business does not shrink, given shareholders generally see shrinking revenues as a red flag.

Unfortunately, Viatris' revenues were $17.8bn in 2021, $16.2bn in 2022, and are forecast to be $15.5bn in 2023 - this helps to explain why the share price has been falling - Viatris' valuation is tracking its declining sales, and will likely continue to do so, until the situation can be reversed.

At the same time, Viatris reported a long term debt position of $17.1bn as of Q3 2023, plus a current portion of long term debt of $1.3bn. Unfortunately, with paying down debt being an urgent priority for the company, which needs to maintain its investment grade rating and avoid a damaging (for the share price and business) downgrade, Viatris has substantially less cash to reinvest into its business than might be expected.

Viatris debt schedule (Q3 10Q submission)

Reviewing Viatris' debt schedule, it strikes me that the interest rate on most of the debt is not too onerous - the company chose the right time to take on debt, when interest rates were low, and may reap some benefit from that in the coming months and years, as interest rates are expected to rise, which will make Viatris debt look cheap. This may explain why Viatris' share price has been rising in recent weeks.

Nevertheless, >$17bn of debt is ultimately going to weigh heavily on a company Viatris' size, and restrict its profitability, and the value proposition for investors. As Fitch Ratings discusses it:

Viatris' 'BBB' rating reflects the company's global scale and diversification by product and geography, diverse pipeline of new products and commitment to debt reduction. However, revenue growth challenges, restructuring costs and pricing pressures offset these strengths. Following its sale of selected assets, Fitch anticipates Viatris will prioritize debt reduction to sustain its EBITDA leverage at or below 3.5x and FCF/debt at or above 10%.

In fact, in its JPM conference presentation Viatris states it expects to generate ~$2.3bn of annual cash flow going forward, and expects to invest 50% of this figure into the business, and return 50% to shareholders via quarterly dividends and share buybacks.

The fact that Viatris is effectively guaranteeing its profitability long-term can only be a good sign for investors, but on the more negative side, there is no guarantee the business will grow in size.

Viatris' Shrinking Pains - How The Company Plans To Rejuvenate Its Product Portfolio

Clearly, it is not going to be easy for Viatris to uncover a new Viagra, Lyrica, or Liptor - best-in-class drugs that still make annual sales in the triple-digit millions years after their patent protections have elapsed - and in fact, Viatris has done more trimming of its portfolio than adding to it since becoming a stand-alone company.

In 2022, Viatris agreed to sell its biosimilars business - regarded at the time as the crown jewel of its business in terms of future revenue potential - to Biocon Biologics. Admittedly, Viatris owns a ~13% share of Biocon, but when the deal was first announced, Viatris stock fell from ~$15, to ~$10 overnight, suggesting that investors wanted to see the business grow, not shrink.

Unfortunately, there will be further business divestitures in 2024 - as per Viatris' Q3 2023 quarterly report / 10Q submission :

On October 1, 2023, the Company announced it received an offer for the divestiture of substantially all of its OTC business, and entered into definitive agreements to divest its women’s healthcare business and, separately, in another transaction, its rights to two women’s healthcare products, its API business in India and commercialization rights in the Upjohn Distributor Markets. The transactions are expected to close by the end of the first half of 2024

Simply put, it is hard to get excited about a company that is $17bn in debt, and selling off its assets, even if that company is trading at a P/S ratio of <1x, and paying a dividend of 4%. Clearly, the company is not about to go on an M&A spree, or attempt to develop its own molecules in-house, which is the preferred strategy for Big Pharma. Developing new drugs with lengthy periods of patent protection is considered the most lucrative and profitable way to win in the Big Pharma field - and explains why, besides Pfizer, Merck & Co ( MRK ), GSK ( GSK ), Johnson & Johnson ( JNJ ), and Sanofi ( SNY ) have all spun out older business divisions into new business entities - shedding their dead wood, and their debt, while realising significant tax benefits - Merck, for example, paid itself an $8bn tax free dividend after spinning out its generics / women's health businesses into a new entity, Organon ( OGN ), in 2021.

Viatris' solution to its shrinking business has been to identify three markets where it feels it can make strategic, and ultimately financial, headway - eye care, dermatology, and gastroenterology. Eye care is the most established business to date, thanks to the approval of Tyrvaya - the dry eye disease therapy acquired via Viatris' $425m acquisition of Ophthalmology specialist Oyster Point last year - a rare case of Viatris using M&A to bolster its business.

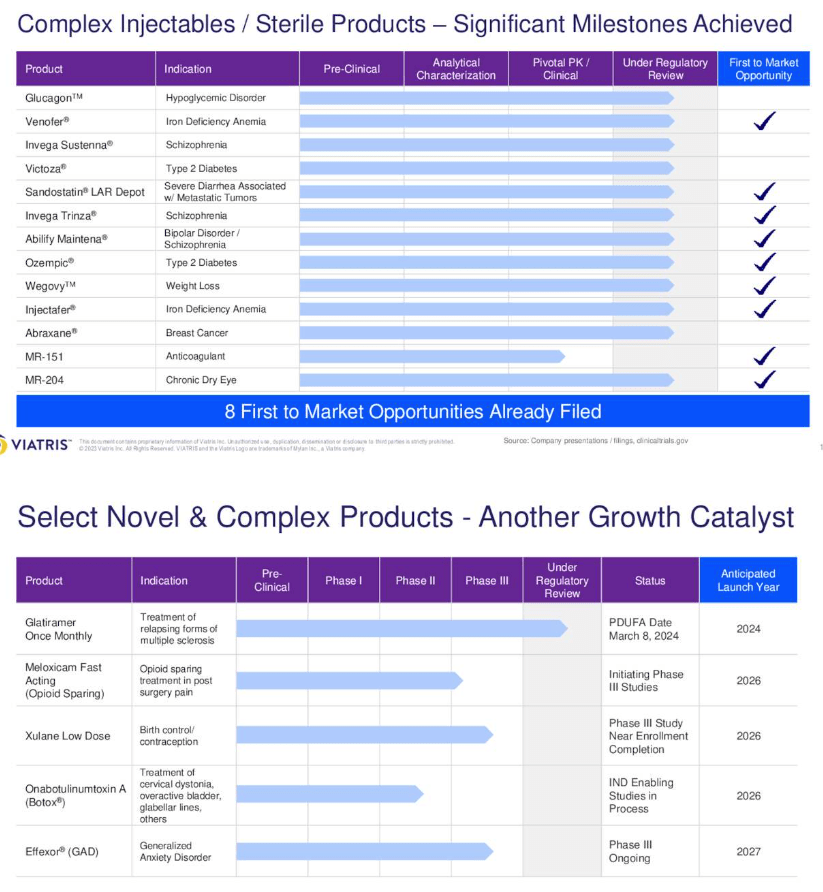

Management has suggested that Eye Care could be a $1bn revenue business by 2028, with three other assets at the Phase 3 clinical study stage, and that complex injectables can make a >$1bn contribution to the top line by 2027, and if we look at some of the products Viatris is aiming to bring to market, there are plenty of opportunities.

Viatris pipeline - complex generics (Viatris Q3 2023 earnings presentation )

{kind=link}

For example, Viatris is already attempting to bring a generic version of Novo Nordisk's GLP-1 agonist, marketed and sold as Wegovy for weight loss, and Ozempic for Type 2 diabetes, to market. Wegovy has been earmarked to become one of the biggest selling drugs of all-time, so it would be surprising if Viatris could successfully bring a generic version to market without fighting a fierce legal campaign.

These court battles are part and parcel of any successful generic drug company's modus operandi, however, so Viatris shareholders and prospective investors should probably get used to such protracted legal disputes.

On the dermatology and gastrointestinal front, there has apparently been little progress, and CEO Smith sounded somewhat evasive about the company's plans in these fields when questioned during his recent fireside chat - the CEO was asked "I think you've mentioned ophthalmology, dermatology, GI as kind of the big three, where of those three, do you see the most opportunity for Viatris?" His reply is shared below:

So that's hard for me to answer directly, right. There's different types of opportunities in those three buckets. I wouldn't say that one has way more opportunities than the other. I think part of the reason that we were initially focused on those three areas, is we saw a lot of opportunity in each of the three areas.

Again, there tends to be different types. It evolves over time, right, companies become more viable in terms of business development, or transaction over time and less. So it's a very dynamic situation. But we see all three of those therapeutic areas, I think, being very viable in terms of our ability to partner, to license, to acquire assets.

In short, although Viatris has made some moves on the business development front, most notably with its Oyster Point deal, management - both previous and current - has generally proven itself to be much more adept at selling off chunks of the business than making bolt-on acquisitions. The company will apparently net ~$3.6bn from the divestitures of its European consumer health business, and women's health business in 2024 - it would be miraculous if the company reinvests that money into M&A.

As such, although the outlook for the eye disease and generics businesses appears broadly positive, it may not be enough to offset the slow erosion of legacy brands revenues, although it may just be enough to keep shareholders happy in the short to medium term, with generous dividend payouts and share buyback programs distracting them from the longer term issues.

Concluding Thoughts - As Mysterious As Ever, Viatris Is A Polarising Stock That Is Complex To Value

Ultimately, Viatris defies valuation in many respects. It is difficult to value the company based on top line revenues, as the main revenue contributing assets are expected to make smaller and smaller contributions going forward - while management also appears ready and willing to keep selling off assets, making it unclear whether Viatris' top line will ever experience growth.

It is tempting to wonder whether, if approached by another company and offered, let's say, $17bn for all of its revenue generating assets, Viatris management would agree the deal, pay off its debt, and share whatever is left with shareholders - that may be the optimal strategy for valuing the business, in fact.

Essentially, the fact that the business is shrinking and heavily indebted is the key reason why the business looks so undervalued based on a P/S ratio, or a price to free cash flow ratio, or even when considering the generous dividend. A key question that needs answering is what size Viatris will be in 5 years' time? Will it be a $5 - $10bn revenue company, but with <$10bn debt, valued essentially the same as it is today?

That would be my conclusion at present - management inherited a complex, sprawling business with a mixture of old and new assets, some promising, others simply a drain on resources, a massive debt load, and a legacy brands business that provides an extremely solid, if slowly shrinking, source of >$15bn per annum in top line revenues.

The task has been to make the newer elements of the business work while maximising the revenue potential of the older assets all while paying down debt, and keeping investors happy. Management has not pleased shareholders by consistently making business divestitures, without showing that it has a clear plan to find new sources of revenues outside of complex generics and eye care so far.

Essentially, if we subtract the ~$10bn per annum revenue contribution from the established brands division in 2023 from the market cap valuation, we get $4bn, and then the question to answer is whether Viatris without its established brands is a business worth more or less than that $4bn figure. We can arguably discount the debt from this equation, as established brands revenues are profitable enough to support successfully paying down even such a large figure.

It is a tough question to answer, and my main concern is whether management will be able to find assets that generate the kind of revenue streams and profitability that the established brands division has, and still does. I think that could be an extremely challenging goal for a business busy paying down debt and keeping shareholders happy, but I also think that shareholders and the market may look more favourably upon Viatris at the end of 2024 than at the end of 2023, thanks to the cash earned from the divestiture, and the continuing strength of established brands.

The short term strength of the business - cash flow, revenue generation, dividend - takes the attention away from longer term fears around whether a globally successful generics business can be built on the ashes of Viagra, Lyrica, and Epi Pen, or whether more and more downsizing will be necessary going forward. For now at least, given the number of different of factors in play, I am happy to hold onto my shares and wait for the picture to become clearer.

For further details see:

Viatris In 2024 May Be The Most Polarising Investment Opportunity In Pharma