VTRS - Viatris Stock Is Dirt Cheap And Worth Buying

2023-11-24 04:34:34 ET

Summary

- Viatris shares had a negative 25% total return in the past 2 years, underperforming the S&P 500.

- The decline is likely due to the company's debt burden and stagnant revenues.

- Despite this, now may be a good time to consider buying VTRS as its valuation is low and there are signs of future improvement in financial performance.

- I think Viatris may reach $14.52 next year, a 55% increase, trading at 5-6x earnings with ongoing debt reduction and potential new drug approvals.

Introduction

I wrote about Viatris ( VTRS ) shares about 2 years ago when they were trading at $13.63. My "Strong Buy" rating at the time didn't age well, as VTRS's total return showed a negative 25%, while the S&P 500 Index ( SPX ) ( SP500 ) returned to 'normalcy' after a severe 2022 drawdown.

Seeking Alpha, my coverage of VTRS

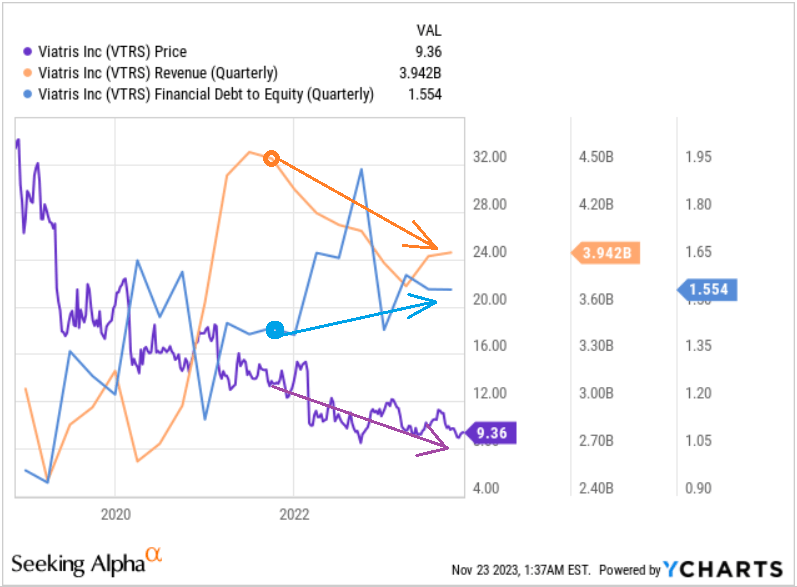

The most likely reason for the decline in VTRS during the period indicated is the company's debt burden and stagnating revenues:

{kind=link}

Nevertheless, now may be the right time to consider adding to your position or buying VTRS for the first time, as the valuation is low and there are signs of future improvement in financial performance. Let's test the strength of this thesis.

Viatris: Financials And Prospects

In case you don't know the company, Viatris Inc. is a Pennsylvania-based $11.4-billion market cap specialty and generic drug company formed in 2020 through the merger of Pfizer's ( PFE ) Upjohn business and Mylan N.V., is a prominent player in the healthcare industry. With 37,000 employees, it operates globally in 4 segments: Developed Markets, Greater China, JANZ, and Emerging Markets.

The company offers a wide range of pharmaceutical products, including prescription brand drugs, generic drugs, biosimilars, and active pharmaceutical ingredients (APIs), covering various therapeutic areas. In addition to providing medicines in different forms, such as oral solid doses and injectables, Viatris offers support services like diagnostic clinics and digital tools to aid patients in managing their health. The company distributes its products through various channels, including pharmaceutical wholesalers, retailers, e-commerce pharmacies, and specialty pharmacies. Notable products under its umbrella include Lyrica, Lipitor, and EpiPen auto-injector.

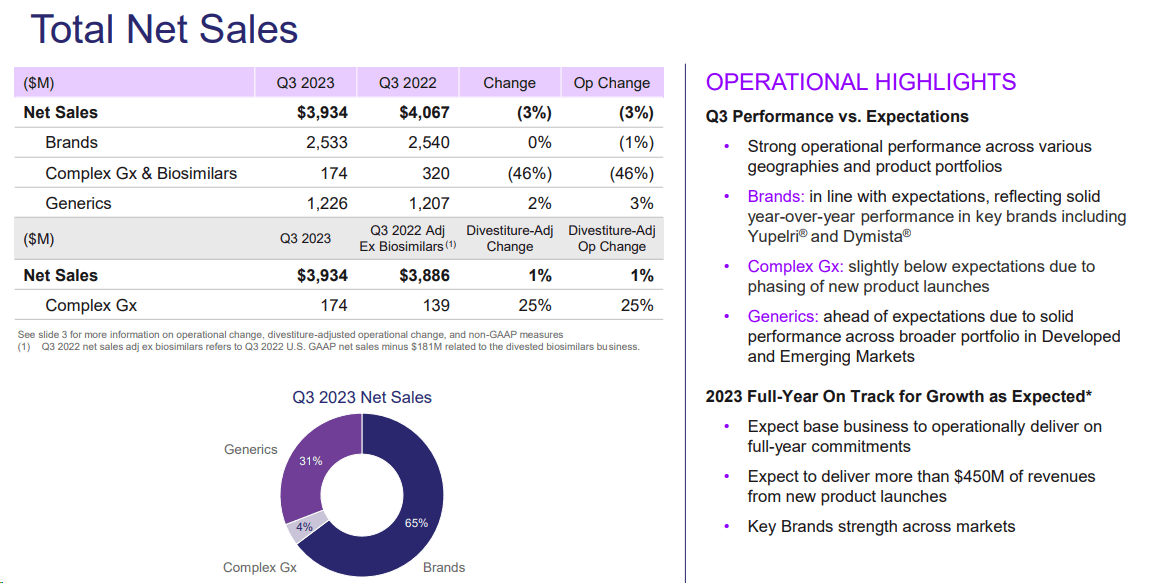

In Q3 FY2023 , Viatris reported total net sales of $3.93 billion, indicating a 1% increase on a divestiture-adjusted operational basis compared to the same period in FY2022. While brands, including key products like Yupelri and Dymista, met expectations with solid year-over-year performance, complex generics fell slightly below expectations due to the phasing of new product launches. On the other hand, generics, encompassing various product forms, surpassed expectations, driven by strong performance across a diverse portfolio in both Developed and Emerging Markets. The company achieved approximately $135 million in new product revenues during the quarter, primarily attributed to lenalidomide and Breyna in the U.S., with a projected target of exceeding $450 million in new product revenues for the entire year.

{kind=link}

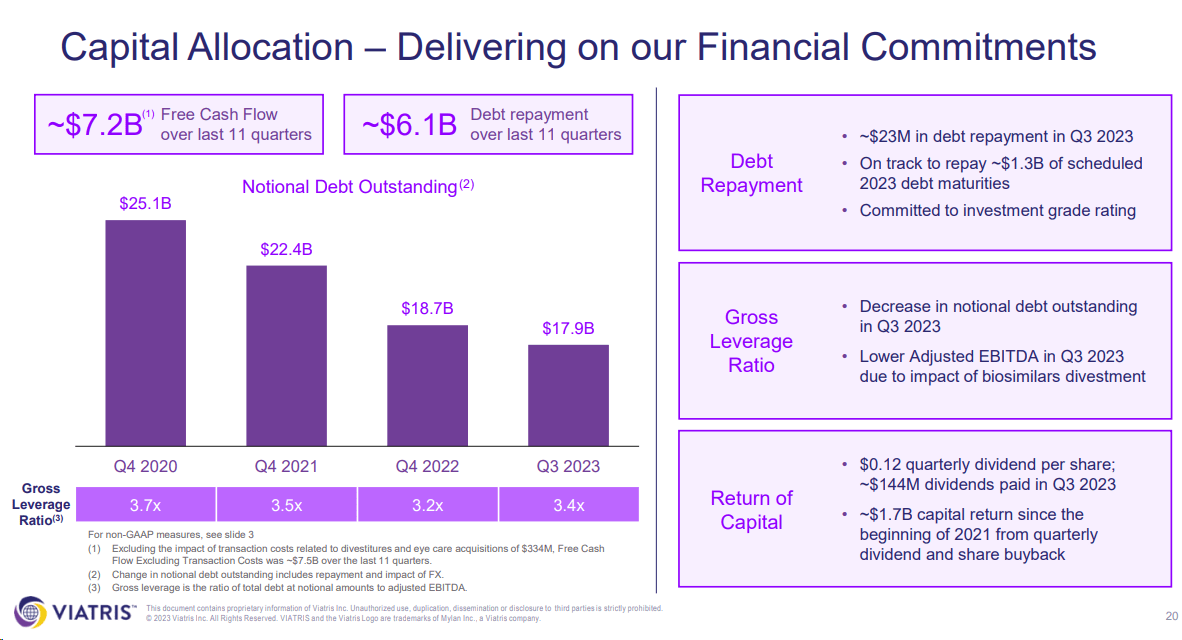

Financially, Viatris demonstrated robust performance, generating $834.1 million in U.S. GAAP net cash from operating activities and $732 million in FCF during the quarter. These positive results were mainly attributed to strong operating performance and well-timed capital expenditures, according to the management commentary .

Notably, the cash flow figures included transaction costs of ~$48 million related to eye care acquisitions and divestitures. Additionally, the company exhibited a commitment to debt reduction, paying down $23 million in Q3 and a total of $750 million YTD.

In recent developments, Viatris has undertaken significant corporate actions, including the planned divestiture of its OTC business, women's healthcare business, and certain product rights, with transactions expected to conclude by 1H FY2024. The gross proceeds from all the divestments under the terms of the deals are up to $6.94 billion, according to Seeking Alpha News . I expect that most of the proceeds will be used to repay debt. This should make VTRS's credit risk profile much more conservative, which should (in theory) have a positive impact on equity capital return requirements. Simply put, less debt means fewer potential problems and therefore higher valuation multiples for the stock.

Also recently, the company completed the acquisition of Oyster Point in 1H FY2023 for ~$427.4 million, focusing on pharmaceutical therapies for ophthalmic diseases. Additionally, the acquisition of Famy Life Sciences, a research company in ophthalmology, was finalized in the same quarter for $281 million. Through these strategic moves, Viatris tries to restructure its portfolio and expand its presence in the ophthalmology sector.

I like the policy that VTRS is pursuing with regard to shareholders' returns. According to the 10-Q, during the nine months ending September 30, 2023, Viatris repurchased ~21.2 million shares at a cost of around $250 million. At the same time, the FWD dividend yield at the time of writing is 5.18%, which is many times higher than the norm for the healthcare sector (median of 1.61%).

{kind=link}

The company has a fairly diversified pipeline of later-stage projects (already under regulatory review), which suggests accelerated revenue growth in several quarters. At the same time, the company will most likely continue to generate strong FCF. Speaking of FCF, the yield and margin are 17.85% and 13.1% respectively [YCharts data], which I think is very high for such a relatively large company.

Now that we've talked about FCF yield, it's time to turn our attention to the valuation and market multiples of VTRS.

Viatris Is Quite Cheap

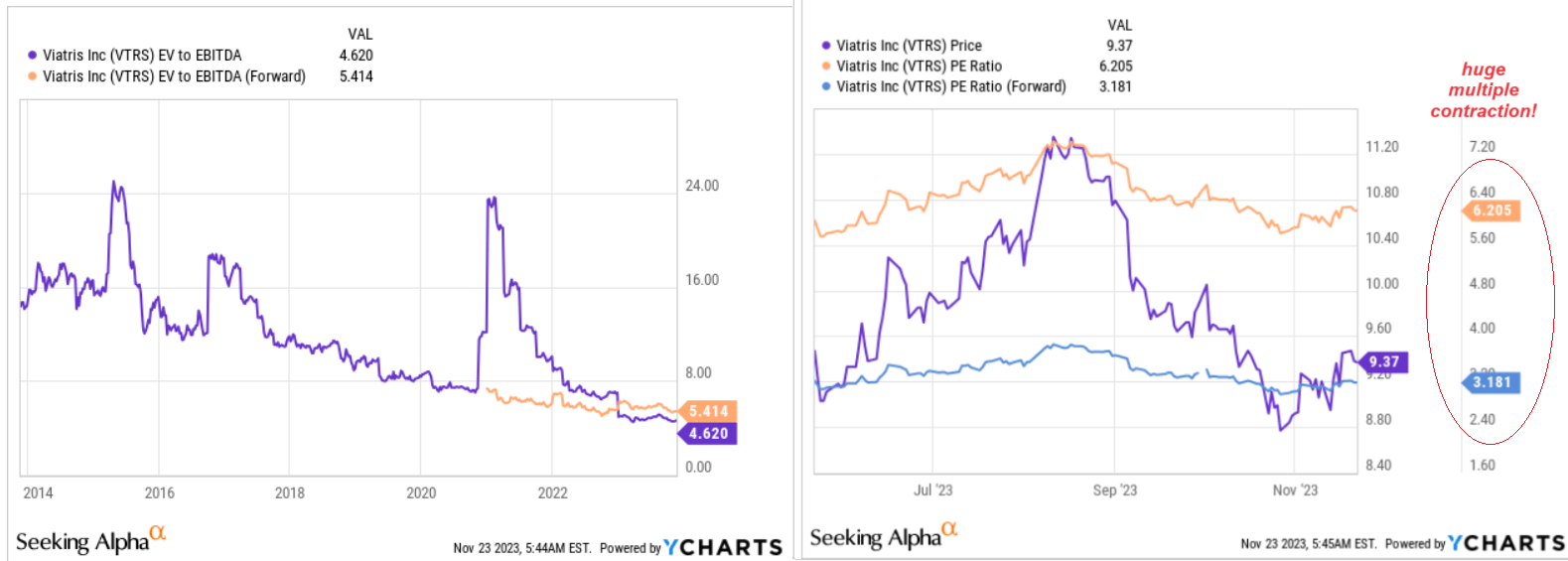

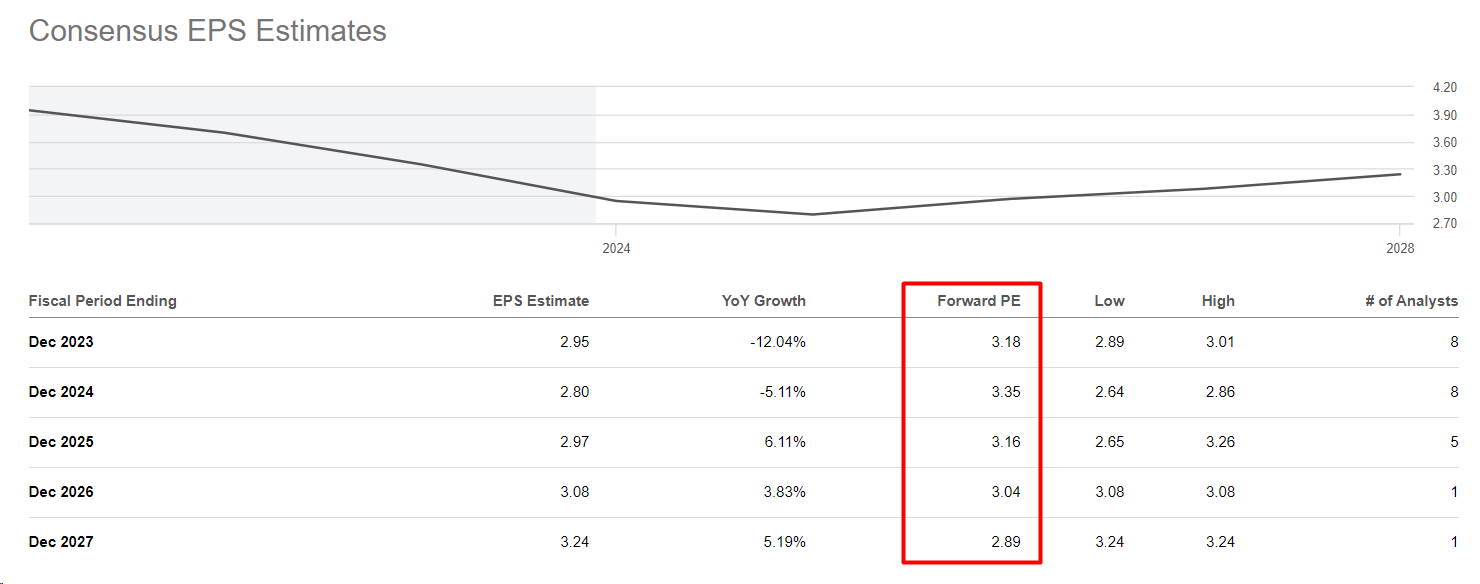

The stock trades at a P/E multiple of 3.2x for next year, which is pricing a ~49% discount to the TTM multiple of 6.2x; in both cases, VTRS looks very cheap. The company's forward EV/EBITDA is 5.4x, which in contrast gives a multiple expansion of ~17.2% to the TTM figure, which is not critical.

{kind=link}

Apparently, the market is assuming that Viatris will receive a one-off earnings per share boost next year, which should then be much lower in subsequent periods. In this case, a very low FWD multiple would be justified as it should return to its previous historical averages in the span of 3-4 years. However, this explanation for the cheap valuation falls apart when we look at Wall Street's projections , which do not assume that FY 2024 will be a one-off event for Viatris: The stock is expected to be extremely cheap through FY2027.

{kind=link}

Viatris has beaten analysts' EPS forecasts for the last three quarters, but even if we assume that FY2024 EPS will be 5-10% below the current consensus forecast, this results in an implied P/E ratio of ~3.61x, which is several dozen percent below the sector median (namely, by 80% according to Seeking Alpha). I think Viatris should trade at 5-6x earnings if the systematic debt paydown continues and some new drugs are approved next year. Even with a conservative estimate (low EPS estimate of $2.64 for FY2023, SA data), VTRS shares should cost $14.52 at the end of next year - that's 55% more than the price I see on my screen today.

The Verdict

Of course, investing in Viatris involves risks associated with the pharmaceutical industry's uncertainties, regulatory challenges, and intense competition, particularly in the generic drug market. Factors such as patent expirations, pipeline setbacks, legal disputes, supply chain disruptions, currency fluctuations, and the complexities of post-merger integration contribute to the risk profile. The company's financial health (first off, its large amount of debt), market sensitivity, and dependence on successful drug development further underscore the multifaceted risks for potential investors.

However, I think VTRS as a whole is moving in the right direction by continuing to generate a tremendous amount of FCF and spending it wisely on buybacks and generous dividends. The company's pipeline is diversified and management seems to have a clear plan to divest what should remain in the past to get rid of debt and move the company forward in a new way. The broader market doesn't believe it - that's why the stock is so cheap. But there is a possibility that investors will no longer be able to buy VTRS cheaply once Mr. Market changes his mind about it all. For these reasons, I am issuing a 'Buy' recommendation today.

Thanks for reading!

For further details see:

Viatris Stock Is Dirt Cheap And Worth Buying