VTRS - Viatris: Turning Point For Cheap Pharma Stock

2023-08-11 04:04:38 ET

Summary

- Viatris reported strong second-quarter earnings, beating estimates on both revenue and earnings per share.

- The company showed signs of sales growth on a divestiture adjusted basis and is on track for $500 million of new product revenue.

- Management is committed to 9% of shareholder returns through dividends and buybacks, which can create momentum going into 2024.

- Viatris remains the cheapest stock in its peer group, with positive aspects of the company on the rise.

Viatris (VTRS) reported earnings on the 7th of August and showed the first signs of a turnaround in their business with a beat on top- and bottom-line. Since the first time covering Viatris , there was a lot of criticism around debt, management and that stock was a value trap. Nevertheless, the stock returned 21% to shareholders with dividends included, easily outperforming the S&P 500. Year-to-date the stock has struggled to reach higher, but looking at the complete picture, pharma in general did not perform well. However, the positive aspects of the company are on the rise, while the company remains the cheapest in the pack of peers.

Strong Second Quarter

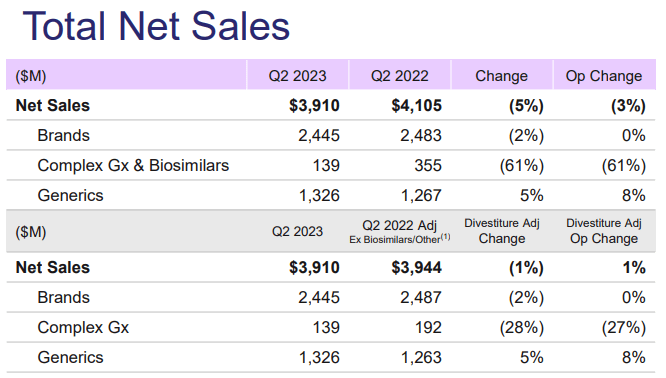

In the latest quarter, the spun off company from Pfizer (PFE): Viatris, was able to beat on both top-line and bottom-line and showed first signs of sales growth on a divestiture adjusted basis. Revenue of $3.92 billion beat estimates by $60 million and earnings per share of $0.22 beat estimates by $0.02. Total net sales grew 1.5% adjusting for the divestitures and with constant FX rate. This is the first quarter since the spin off, that there is sales growth on an operational basis, and gives hope for further stabilization of the business. In the developed markets, emerging markets and greater China, Viatris was able to grow sales. The JANZ (Japan, Australia, New Zealand) area saw sales decreases.

{kind=link}

Of course, the company can't just divestiture all assets and is in need of new products to grow sales again after the management is done with restructuring. Further, the company can't rely on the current assets to keep providing stable sales, because there will be business erosion nonetheless.

Viatris has 3 segments in their pipeline that are expected to reach $1 billion in peak annual sales by 2027-2028, which is 75% of new product sales compared to the current sales. The first segment is complex injectables and sterile products. There are 8 first to market opportunities already filed and one is expected to be filed in 2023. The second segment is select novel and complex products. One product has received FDA approval and 4 other products are still in phase 2-3. Lastly, there is the eye care portfolio, where two products already got the necessary approval and 4 more products are still in the pipeline. The company is on track for $500 million of new product revenue in 2023.

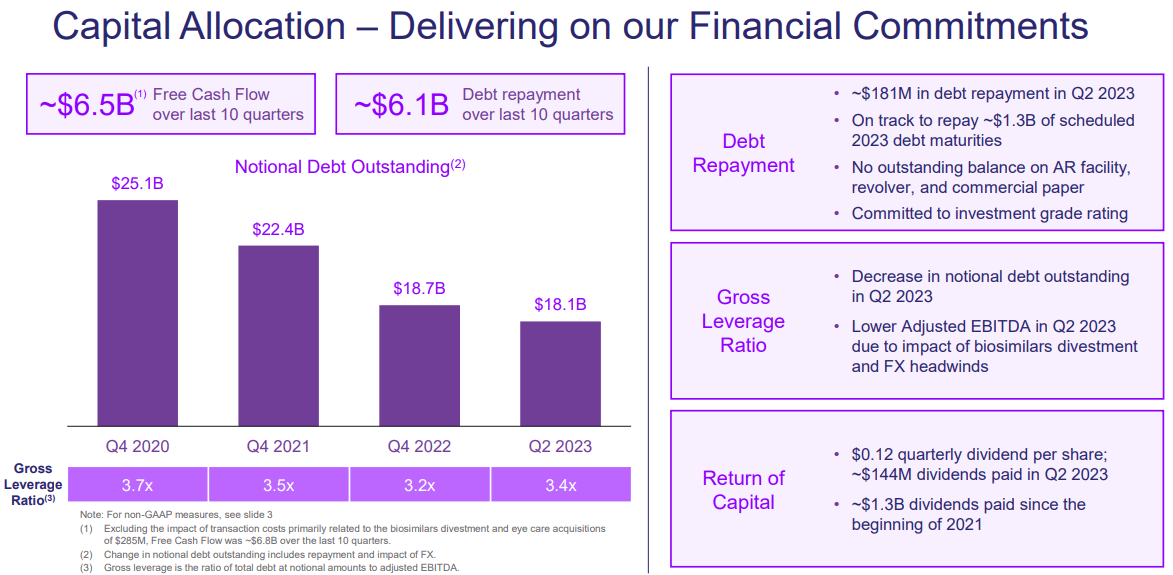

Over the last quarters, Viatris has been heavily focused on trimming the debt levels and decreasing the gross leverage ratio. Obviously, it is hard to get the gross leverage ratio lower when you divestiture parts of your business and lose EBITDA. So, it is a bit of a waiting game till the new products start earning profits to recover the EBITDA erosion.

{kind=link}

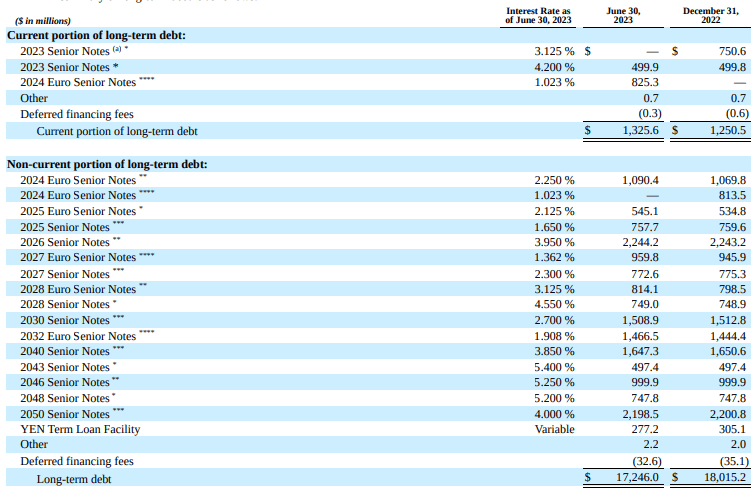

It is important to keep an eye on the maturities of the long term liabilities. These can not be higher than free cash flow, otherwise the business will be in problems.

In 2023, Viatris is on track to repay the $1.3 billion maturities on the senior notes. For the following years, the company will need to keep working on the debt repayments and it will impact the amount that the company can give back to shareholders. But it is of utmost importance that they prioritize the repayments to decrease interest payments. The 2026 debt repayment will be the heaviest, but should be the last real hurdle.

{kind=link}

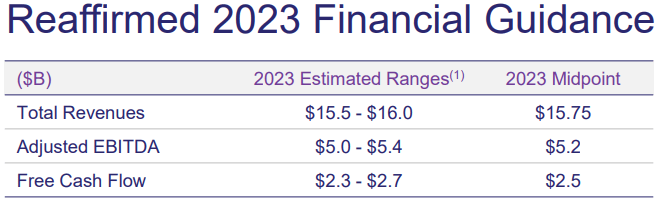

As long as free cash flow can stay stable around $2.5 billion, the company is in a safe place. In case, we see further deterioration in free cash flow, it could impact the share price. Nonetheless, must the management team be able to get a great divestiture deal done, then it could ease the pressure in the long term debt maturities and increase the allocation in free cash flow that can go the shareholders. The new CEO seems to be confident in free cash flow generation, and said this in the latest earnings call :

We intend to earmark approximately 50% of our free cash flow annually to be returned to shareholders in the form of dividends and especially share repurchases. With the remaining capital, we intend to invest in our businesses, both organically and inorganically.

This would mean that approx. $1250 million would go to shareholders and could signal a dividend increase in 2024 as the dividend payout is $570 million right now, or a share buyback of $700 million which would account for 5% of the market cap. I don't think 50% of free cash flow should go to shareholders and management better focus on the debt repayments like they did before, as they could risk to lose their credit rating.

{kind=link}

Valuation

The stock is trading at significant low prices, mainly due to the spin off, heavy debt burden and the notion of bad management. VTRS is trading at 7.2x price-to-earnings and at 3.7x forward PE. Price-to-free cash flow is sitting at 6.6x and price-to-book value at 0.64x, which all indicate the stock is rather inexpensive to say the least.

Further, I have decided to compare EBITDA free cash flow with other peers in the industry. I have done this while using EV-to-EBITDA and -free cash flow. EV stands for enterprise value and this takes into account the market cap combined with total debt minus cash and cash equivalents. Since the pharma industry tends to have heavy debt on the balance sheet, we want to include it when comparing businesses.

Based on the EV-to-EBITDA multiple, Viatris is by the cheapest company, followed by Pfizer and Sanofi ( SNY ).

Further, if we look at EV-to-FCF, we can see that Viatris is in the bottom side of the pack. Three other companies have a better multiple: Gilead Sciences ( GILD ), AbbVie ( ABBV ) and Sanofi.

Takeaway

Viatris has in my opinion come to a turning point. The business shows first signs of stabilization after the restructuring changes. New product revenue in slowly coming in and countering the business erosion. The new CEO Scott A. Smith, former COO of Celgene, should boost investor sentiment of those that were dissatisfied with management before. In addition, debt is decreasing at an incremental pace. The stock is trading at cheap multiples, whilst promising 9% returns in dividends and buybacks. Yet, I do hope lowering debt will remain the main focus of management.

There are definitely risks of further business erosion and the debt burden. Yet, the risks seems to be improving and most of it looks to be priced in. Therefore I rate Viatris a 'BUY' at $11 a share, with a solid margin of safety for both value appreciation and dividend income.

For further details see:

Viatris: Turning Point For Cheap Pharma Stock