VTRS - Viatris: Won't Take Much To Move The Needle

2023-06-15 12:37:07 ET

Summary

- Viatris remains a dirt cheap stock in a frothy market and pays a well-covered dividend yield.

- It continues to make progress towards deleveraging, and could return substantial capital to shareholders in 2024.

- With market sentiment working against the stock, it could deliver potentially strong total returns for investors should the tide change.

There are two sides to every coin, and that applies to the market, too. There are some names that are priced to perfection on hope and optimism, and because their forward valuations are extrapolated from near-term results, it won't take much for valuations to come crashing down should they disappoint.

On the other hand, there are other stocks that are so beaten down with plenty of negativity and risks already priced in, that it wouldn't take much for a strong upward revisions due to near-term results and the fickle market.

This brings me to Viatris ( VTRS ), which I last covered here back in March, noting its aggressive debt paydown and recent acquisitions. It appears the market hasn’t agreed with my bullish take, with the stock price falling by 14% since then. This could be due to market concerns over the upcoming ability for Medicare to negotiate drug prices and VTRS's leverage. In this article, I address these concerns and discuss why VTRS remains a deep value stock for risk tolerant investors, so let’s get started.

Why VTRS?

Viatris was formed after the merger between Pfizer's ( PFE ) Upjohn business and Mylan. Its medicines are used in 165 countries and its portfolio is comprised of over 1,400 approved molecules across a wide range of therapeutic areas that span both non-communicable and infectious diseases.

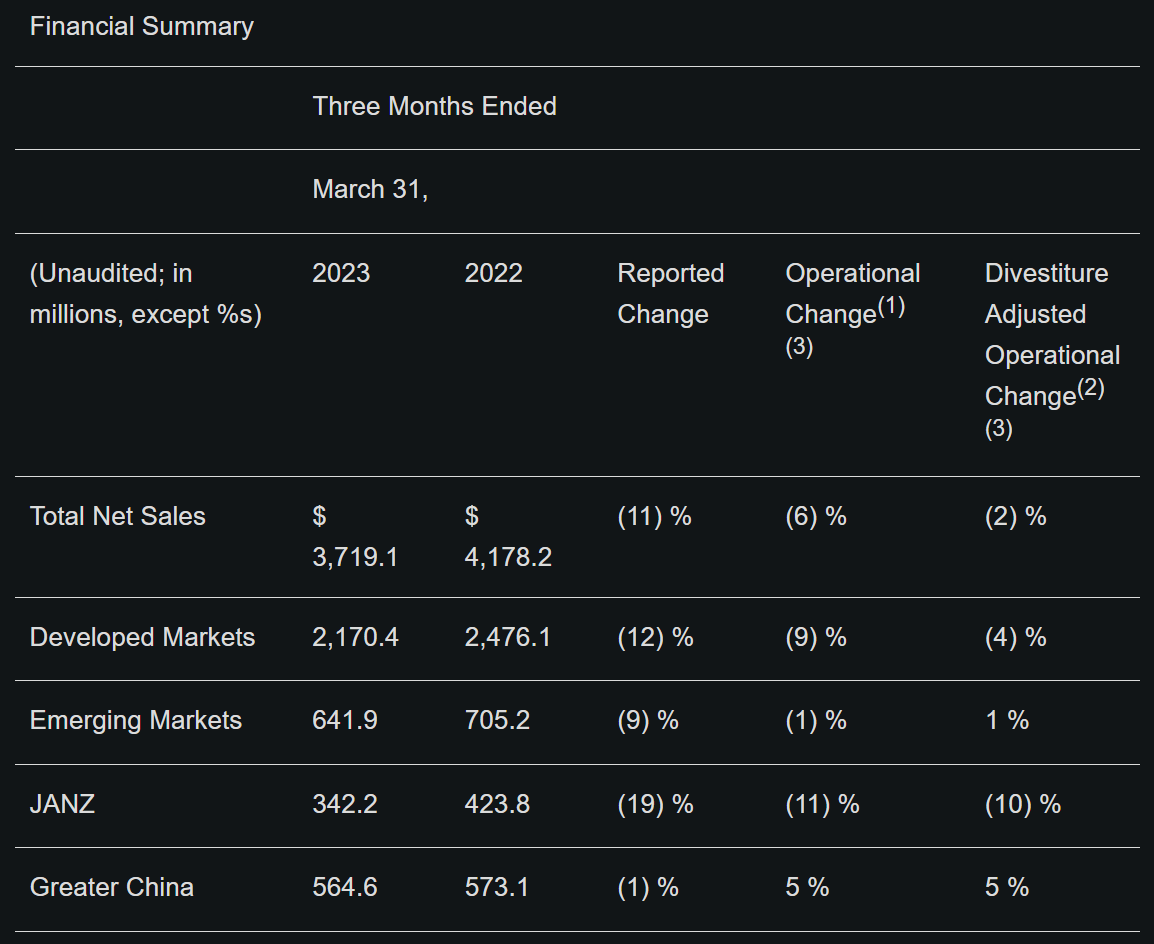

Viatris has demonstrated steady results against a shaky macroeconomic backdrop, with net sales (adjusted for divestures) declining by just 2% on a YoY basis, due primarily to foreign currency. Key branded drugs like Dymista, Celebrex, and Norvasc performed in line with expectations, and standard generics, including extended-release oral solids, injectables, transdermals and topicals performed ahead of expectations. This was offset by challenges in complex generics, which performed lower than expectations due to phasing of certain products.

From a geographic standpoint, VTRS saw growth in Emerging Markets and Greater China, offset by declines in Developed Markets and JANZ (Japan, Australia, and New Zealand).

{kind=link}

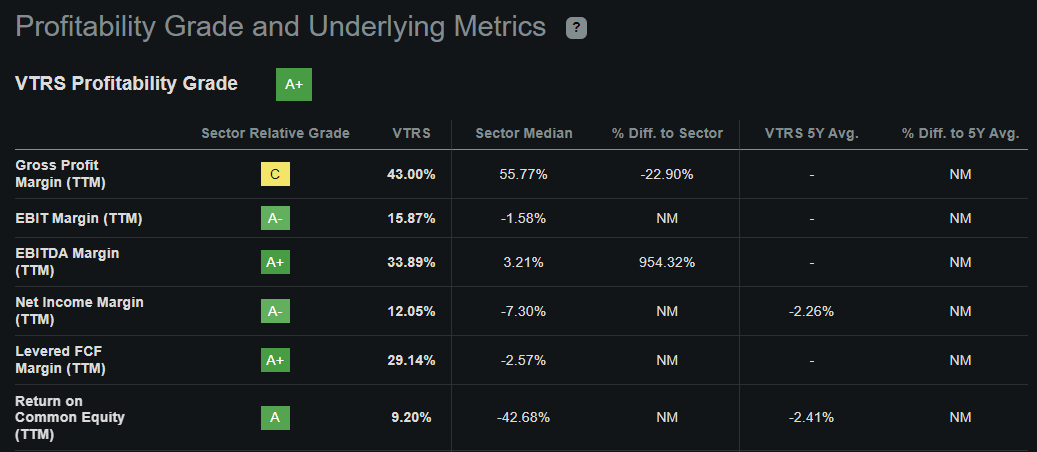

Nonetheless, the business remains well balanced with branded drugs representing 60% of Viatris's sales. This contributes to a strong profitability for the company in a sector that's riddled with smaller speculative names that are not yet in the black. As shown below, VTRS scores an A+ grade for profitability and generates a 34% EBITDA margin and a 12% Net Income margin, both of which sit well ahead of the sector median.

{kind=link}

Looking ahead, Viatris may be able to offset weakness in complex generics with its pipeline of drugs. This includes $85 million in revenue stemming from new products during the first quarter, with management expecting $500 million in new product revenue for the full year 2023, and its pipeline in Complex Injectables, Novel and Complex Products, and Eye Care is expected to generate $1 billion in peak sales by 2028. Moreover, management reiterated its full year guidance for $15.75 billion in total revenue and $2.3 billion in free cash flow excluding divestures.

Notably, Viatris recently got a new CEO in April who joined from outside the company. Based on his bio , it appears that he is a seasoned executive with over 35 years of experience in the pharmaceutical space. He also has big company experience from Celgene, which was acquired by Bristol-Myers Squibb ( BMY ), where he was President of Inflammation and Immunology. These are two growing areas in the pharmaceutical space from which VTRS could benefit from his experience.

The new CEO has guided for revenue growth in the second half of the year, leading to full-year revenue growth. He also discussed aggressive debt paydown, and the strong cash flow after it meets the leverage target during this month's healthcare industry conference :

Once we get and pay down our debt ratio to three (3x net debt to EBITDA), which we should be very close to, and we're going to look to be able to return to shareholders of the cash flow that we have left, which should be probably a minimum of $2.3 billion in 2024, pay half of that back to shareholders in terms of share buybacks and dividends and use the other half to enhance the portfolio through business development.

It appears that VTRS is well on its way to achieving its target leverage, as it was able to reduce long-term debt by $1.65 billion since the end of 2021 and currently carries a net debt to TTM EBITDA of 3.4x. Based on the CEO's comment above, VTRS could potentially return $1.15 billion in capital to shareholders in 2024 through buybacks and dividends.

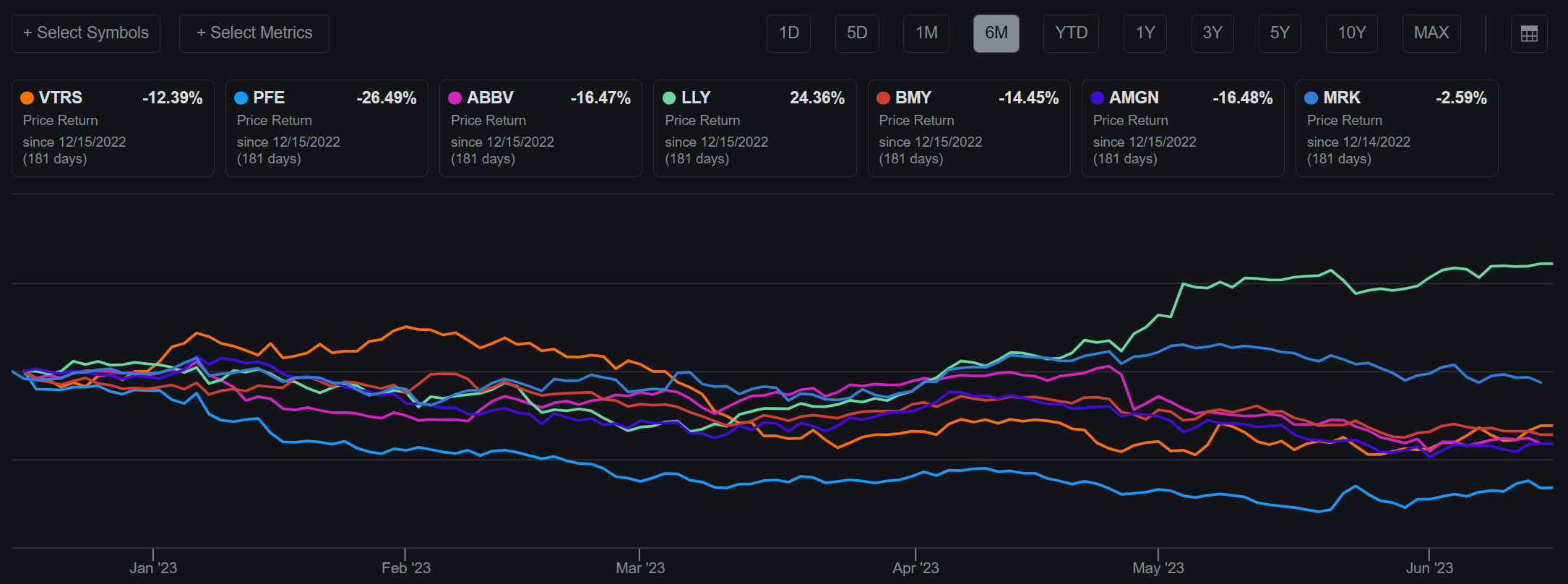

Risks to VTRS include the upcoming ability for Medicare to negotiate with drug companies and prices, with the agency set to list the first 10 drugs up for negotiation in 3 months' time. While it's difficult to quantify what the impact will be for VTRS, it appears that the market has already baked in plenty of for the entire sector, and VTRS isn't the only company to have seen material share price declines over the past 6 months.

{kind=link}

Meanwhile, VTRS currently yields 5% and the dividend is well-covered by a low 15% payout ratio. Plus buybacks at the current price of $9.76 and low forward PE of 3.3 are highly accretive to shareholders. While analysts expect just flat bottom line growth over the next couple of years, the current valuation more than bakes that in with a low PE. Analysts have an average price target of $12.51 , representing a 28% potential upside.

With such a low valuation, I believe the market has already priced in the aforementioned risks, even as VTRS continues to deleverage its balance sheet. Even with no capital appreciation, VTRS could still potentially deliver 10% annual returns through dividends and ~5% annual share count reduction based on the aforementioned capital return potential and the $11.6 billion equity market capitalization.

Investor Takeaway

Viatris is a dirt cheap stock that continues to produce steady results. Management has a clear plan to pay down debt and then begin aggressive returns of capital to shareholders, while also retaining capital to fund business growth and development. With many risks already priced in and a well-covered dividend, investors may be well-rewarded with potential capital appreciation while being paid a solid yield to boot.

For further details see:

Viatris: Won't Take Much To Move The Needle