WOLF - Vicor Continues To Underperform Relative To A Sky-High Valuation

Summary

- Despite being down nearly 50% over the past year, VICR still trades with a TTM P/E = 98x and a forward P/E = 78x.

- Meantime, the Q3 earnings report was less than supportive of such a high valuation level.

- Forward guidance for the upcoming Q4 earnings release (which came out February 10th last year) was also uninspiring.

- My advice is to SELL the stock and move the proceeds into a technology company with a significantly lower valuation and is growing faster.

The stock of Andover, Massachusetts-based power component manufacturer Vicor ( VICR ) was crushed in the 2022 bear-market: down ~50% (see below). It is also down 16% since my initial SELL rating back in May of last year (see Vicor: Whipsawed ). While the stock might appear to have bottomed-out a pre-pandemic levels, and is up 5% since the beginning of the year, has anything really changed? Note that Vicor still arguably trades at a considerably frothy valuation (PE=98x) and Q3 quarterly report in November was "ok", but still showed some recurring problems. Did that report, guidance for Q4, and the company's potential going forward support the current high valuation level? Today, I'll take a closer look at the company and answer that question.

Investment Thesis

Vicor designs, manufactures, and sells proprietary and efficient modular power delivery components - such as voltage converters, bridges, and current delivery devices. These include a full-range of brick-format DC-DC converters. There has generally been rising demand for these types of devices across a variety of fast-growing use cases including AI/ML compute engines, high-performance computing ("HPC"), and automotive - specifically, EVs. Meantime, VICR appeared to have a thriving business with Nvidia ( NVDA ), which gave the company some highly visible and supportive press.

In addition, Vicor believed EVs would be a major and positive catalyst for the company. Yet while EV vehicle sales growth was excellent in 2022, the same cannot be said for Vicor. What went wrong?

As they say, a picture is worth a thousand words:

Seeking Alpha

As can be seen in the graphic, full-year 2022 revenue is estimated to come in at $387 million. If so, that would be only a 10.6% increase as compared to the $359.4 million generated in 2021. Not bad, but not spectacular either. However, even as revenue has been growing, earnings estimates and actual earnings delivered have, generally, been on a downward trajectory.

Does this look like the profile of a company that deserves a near 100x multiple?

Earnings

To be fair, the Q3 earnings report delivered in late October showed some improvement, but it was still another top- and bottom-line miss . That said, revenue of $103.12 million was +21.5% yoy. However, GAAP EPS of $0.18 missed consensus by $0.03 and was down from $0.30 in the year earlier quarter. Among other things, operating expense jumped due to litigation expenses, which on the Q3 conference call were mentioned to be $4 million above Q1. Vicor CFO James Schmidt commented on the legal issue:

So that's ... a function of really a significant amount of ramp and legal expense associated with preparing for the trial, that is happening right now. So I think that will taper down obviously as that ramps up. But there will be other incremental legal costs coming in as we pick back up where we left off with the ITC activity around what Philip had mentioned, which is the -- basically Vicor as a plaintiff -- defending our IP. So I would say there is going to be a net reduction in legal costs over the coming quarters. But it won't revert back down to the low level had been maybe a year, year and a half ago.

As with many patent fights, it's hard to say how this will turn out for Vicor. That said, it's another in a long-line of disappointments for investor - first, it was the lack of adequate manufacturing capacity, then it was pandemic related supply-chain issues, now its on-going legal entanglements. It seems to me that better days for Vicor always seem to be in the (far off?) future. But let's get back the Q3 earnings report.

As I said earlier, revenue growth in Q3 was up nicely yoy (21.5%). However, on a sequential basis, revenue was up only 0.9% as compared to Q2. Meantime, the book-to-bill ratio was less than 1 - the second straight quarter that Vicor's the book-to-bill fell "below par". The backlog at the end of Q3 was down 9.4% from Q2, at which point it had stood at "above $400 million". I would guess the backlog now is significantly below $400 million and probably less than 4x annualized Q3 revenue.

Q3 gross margin - as a percentage of revenue - was 45.5%, down over 5 percentage points as compared to 50.4% in the year ago quarter and down 30 basis points from the previous quarter. Dr. Patrizio Vinciarelli, Vicor CEO, commented on the quarter:

A deteriorating macroeconomic environment caused a shortfall in demand for electronic products. Q3 profitability was significantly impacted by legal expenses ahead of a recent intellectual property litigation trial. Reflecting a reduction in demand caused by recent market conditions, the Q3 book-to-bill ratio came in below 1. We look forward to reducing production lead times and getting caught up with our backlog.

Going Forward

Vicor continues to invest in additional capacity - primary its first ChiP foundry that will enable the Andover fab to build Advanced Products with - the company says - capacity to support revenue of ~$1 billion per year.

In the Q3 earnings release, the company said: "Major advances in power density by our next generation ChiPs and recent design wins in our primary markets bode well for the future utilization of this capacity.” In addition, Vicor should be able to benefit the Biden administration's ability to get the CHIPS & Science Act passed, which could be the source of potential funding for new investments "in vertically integrated US-based manufacturing and also the possibility of leveraging its investment tax credit."

Indeed, in December Senator Ed Markey recently visited Vicor's new state-of-the-art ChiPs ("Converter housed in Package") fab - the world's first - and was there when Vicor received an award for Massachusetts' "Manufacturer of the Year" award. That being the case, I would assume that Vicor will be a strong contender for CHIPS funding.

However, over the near-term expectations continue to be murky. On the previously mentioned Q3 conference call, Philip Davies - Vicor VP of Sales & Marketing - said that the soft book-to-bill ratio was "reflective of the deteriorating macroeconomic environment." Yet he also said:

However, it's important to point out that we maintain substantial backlog as we enter Q4. From an end-market perspective, and on a more positive note, the outlook for the data center market in North America at the current time is still good, as hyperscalers continue to build out their machine learning technologies and capabilities, as well as upgrading their CPU racks with the latest Intel ( INTC ) and AMD ( AMD ) CPUs. Managing the transitions to newer processor platforms in our customer base will require some maneuvering of our NCNR backlog in Q4 from Gen3 to Gen4 factorized power modules.

That sounds promising - at least for Vicor's 380V-based products used for power distribution in data centers. However, the end-result is that Vicor - citing its "continued near-term dependence on outsourced production for certain package process steps" - guided for Q4 results "approximately flat" to Q3, with the potential for modest sequential improvement as the company will "increasingly leverage in-house process equipment to alleviate production constraints."

If Q4 revenue comes in flat with Q3 ($103.1 million), that would be up ~$14% from the $90.3 million in Q4 of last year. That's good, but not "great" - investors should expect much faster growth from a company sporting a P/E of nearly 100x. For full-year FY23, current consensus estimates don't appear to support that valuation either:

{kind=link}

Note that Q4 EPS estimates of $0.21/share would be only a penny above Q4 of last year.

On the other hand, and to be fair, FY23 earnings expectations of $1.13/share would be 57% higher than FY22. However - even if Vicor did manage to hit the $1.13/share estimate for full-year 2023, note that would be 50.6x the current stock price ($57.17). That said, I have my doubts that Vicor will achieve the estimates. After all, shareholders have seen future expectations dashed before, and - at this point - I see no reason to give management the benefit of the doubt (note the "Revisions" ranking of D- in the "Risks" section below).

The Competition

Meantime, global EV sales rocked in 2022, yet Vicor appears to be left behind. I say that because silicon carbide specialist Wolfspeed ( WOLF ) announced very strong Q1FY23 results with revenue of $241.3 million (+54.1% yoy) a $1.53 million beat while - as opposed to Vicor - margin expanded. Now that is an EV growth story that commands a premium valuation.

Meantime, more "old school" NXP Semiconductor ( NXPI ) was recently upgraded. EV-content sales was cited as being a strong and positive catalyst. NXPI currently trades with a forward P/E of only 11.3x yet is expected to have grown earnings in 2022 almost twice as fast as Vicor (19% versus 10%) while throwing of a $3.38/share annual dividend.

Risks

The risk of my negative slant on Vicor is that its sky-high valuation is proved to be correct: pending litigation is resolved in VICR's favor sooner rather than later, the new manufacturing capacity comes online and significantly improves margin and sales, the book-to-bill ratio turns higher and gets-up over 1, and the company starts to consistently grow revenue and earnings in the 15-25% range that its near 100x P/E implies it should.

Let's just say I have my doubts. For what it's worth, so does the current Seeking Alpha risk profile, which gives Vicor an overall rating of 2.0 (SELL):

Seeking Alpha

Summary & Conclusion

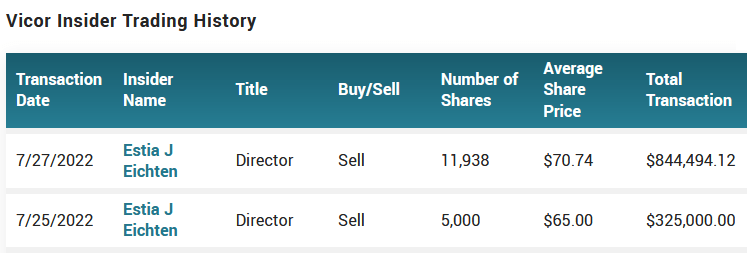

Vicor is going to muddle along with decent - but unspectacular - revenue growth and will generally stay positive on earnings (though on the low-end of what investors should arguably expect). Near-term guidance is blase, and there is at least one insider that isn't buying the hype. Back in July, Director Eichten sold VICR shares worth well over $1 million and at prices considerably higher than the current bid ($56.68):

{kind=link}

Regardless, I find WOLF a much more compelling risk/reward growth opportunity as compared to VICR, and would even prefer holding NXPI - which as I said earlier, is not only growing faster, but pays a decent dividend and sports a multiple 10x less than does VICR (which pays no dividend and likely won't for years to come). Another superior option is Broadcom ( AVGO ). Despite the recent news that Apple (AAPL) will (try to ...) design-out some Broadcom parts from its product-line, I find AVGO very attractive here with a forward P/E of only 14x and an $18.40/share annual dividend that is good enough for a 3.2% yield.

I'll end with a 3-year total returns comparison of the three companies:

Indeed, VICR has been the laggard and - in my opinion - will likely continue to lag going forward.

For further details see:

Vicor Continues To Underperform Relative To A Sky-High Valuation