CA - Victoria Gold: A Better Year Ahead For This Struggling Producer

Summary

- Victoria Gold released its Q4 and FY2022 production results month, confirming its third significant guidance miss in a row with production coming into light in H2-20, FY21, and FY22.

- The culprit for the weaker performance last year was a splice failure on the conveyor belt for its overland conveyor which halted stacking activities for 3 weeks.

- However, even adjusting for this hiccup, Victoria was still nowhere near its initial guidance mid-point of ~177,500 ounces, and with a lower denominator plus inflationary pressures, unit costs soared year-over-year.

- Fortunately, after three consecutive guidance misses and with a new General Manager at Eagle, the company is up against easier comps with low expectations, setting Victoria up for a beat in FY2023 and a potential turnaround.

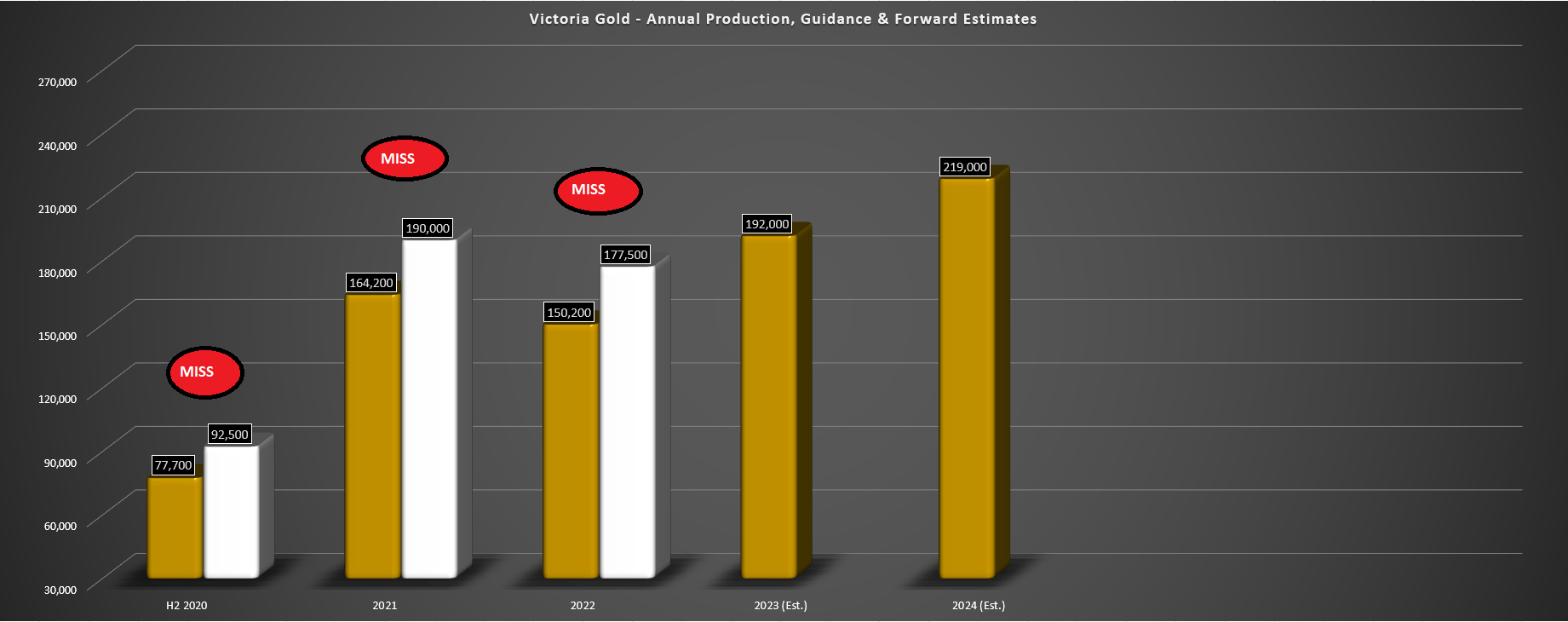

While most gold producers put together a solid 2022 performance operationally after a tough 2020 and 2021 due to COVID-19 absenteeism and supply chain headwinds, Victoria Gold ( OTCPK:VITFF ) was certainly an exception. Not only did the company miss its FY2022 guidance mid-point of ~177,500 ounces, but it didn't even come close, with production coming in at ~150,200 ounces. That represented a 15% miss vs. its annual guidance, and even more disappointing is the fact that the company provided soft guidance of 250,000 ounces in 2023 when teasing its Project 250 plans .

Given that Victoria barely eked out a 150,000-ounce year in FY2022, just trying to meet the elusive 200,000-ounce mark would be a better near-term target for the company. That said, while the past two and a half years have been disappointing (to say the least), expectations finally appear to be low enough to beat, and Victoria is up against easy year-over-year comps. Hence, we should see meaningful growth in financial/operating metrics year-over-year. Let's take a closer look at the Q4 results and why this name is worth monitoring as a potential turnaround story:

Eagle Mine Operations (Company Website)

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q4 & FY2022 Production

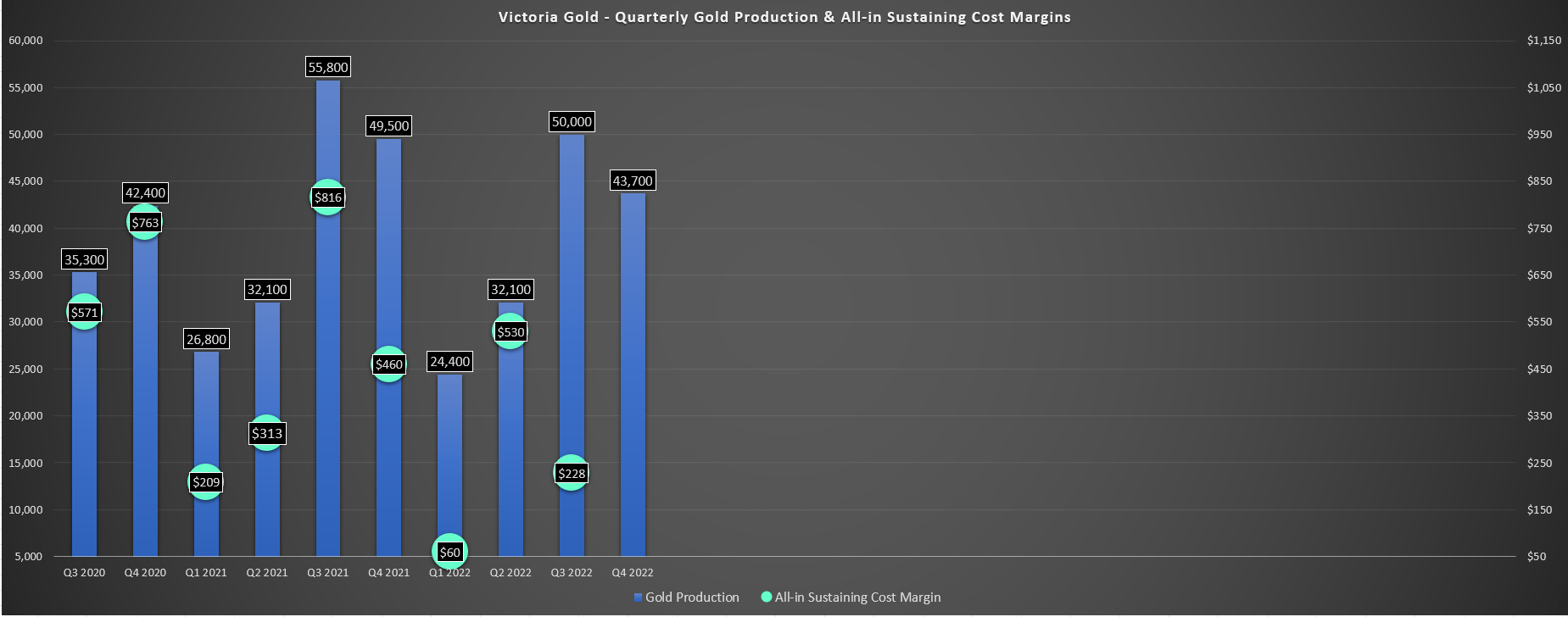

Victoria Gold released its preliminary Q4 results last month, reporting quarterly production of ~43,700 ounces, an 11% decline from the year-ago period. This was related to a decline in tonnes stacked in Q4 (~1.4 million tonnes) due to lower mechanical availability of the crushing and conveying circuit, with a splice failure of the conveyor belt reported in Q3 and not repaired until mid-October. The sharp decline in tonnes stacked was partially offset by higher grades year-over-year (0.90 grams per tonne of gold vs. 0.83 grams per tonne of gold), but it was not nearly enough to avert a double-digit decline in annual gold production.

Victoria - Quarterly Production & Costs (Company Filings, Author's Chart)

{kind=link}

Given the mediocre finish to the year, annual production didn't come in remotely near the initial guidance mid-point of 177,500 ounces for FY2022 and even missed the bottom end of guidance (165,000 ounces). The result was a nearly 9% decline in annual output for Victoria despite lapping an easy year given that guidance missed by a mile in FY2021 as well (~164,200 ounces vs. ~190,000-ounce guidance mid-point). Given this lackluster performance and the fact that the gold price spent most of Q4 below $1,900/oz, I would expect a weak margin performance in Q4 2022, with AISC margins likely to come in below $350/oz and full-year AISC likely to come in above $1,500/oz, translating to razor-thin margins.

Victoria Gold - Annual Guidance, Actual Production & Forward Estimates (Company Filings, Author's Chart)

{kind=link}

Fortunately, while FY2022 was a difficult year for the Eagle Mine with the failure in the overland conveyor, brutally cold weather in Q1, and inflationary pressures, 2023 is shaping up to be a better year. For starters, FY2022 was an expensive year from a sustaining capital standpoint (water treatment plant construction and mobile fleet rebuild). Secondly, diesel prices were elevated for much of the year, which can severely impact a high-volume low-grade operation like Eagle. Finally, the gold price didn't cooperate to help offset the higher unit costs due to lower sales volumes, elevated sustaining capital, and the impact of inflationary pressures (diesel, cyanide, labor).

Since Q3, we have seen diesel prices cool off, and they appear to be settling at a lower level which will provide some relief from a cost standpoint for Victoria. Secondly, the gold price should be much stronger in Q1 and Q2 unless it retraces a significant portion of its recent move, providing some help from a margin standpoint with a much higher average realized sales price. Finally, even if Victoria only produces 190,000 ounces this year compared to my estimates of 192,000 ounces, this would be a 27% increase in output year-over-year. That combination of lower sustaining capital (US$55 million guided for FY2022), slightly lower diesel prices, a higher gold price, and increased sales volumes should allow Victoria to report more respectable unit costs this year.

Assuming all-in-sustaining costs [AISC] were to dip below $1,325/oz in FY2023, this would be a more than 12% decline from estimated FY2022 costs of $1,510/oz, and we could see an $80/oz benefit on each ounce sold if the gold price continues to cooperate. The result would be meaningful margin expansion on a year-over-year basis, even if this is the minimum we would expect after significant margin compression last year and two very poor performances operationally. Whether this is related to easy comps or not, I would expect this to result in a meaningful improvement in sentiment, suggesting we may have seen a bottom for the stock in September.

Future Upside & Project 250

While it's quite clear that Project 250 (250,000 ounces per annum) won't be coming to fruition in 2023, I would not be surprised to see the company deliver close to this goal in 2024, with production improving to 220,000 to 225,000 ounces at sub $1,150/oz AISC. This could be achieved by improving stacking times to 11 months of the year with just one month of maintenance downtime for the crushing circuit, plus adding two 785 haul trucks and a loader, as discussed in the initial Project 250 plans. This would represent 45% plus production growth from FY2022 levels at much more attractive costs if successful.

Meanwhile, if the company can deliver on its Project 250 goal in 2025 (I am purposely using a more conservative timeline given the team's inability to meet targets to date), this would represent more than 60% production growth over the next three years. This would result in a significant increase in cash flow per share even if we were to see a flat gold price environment, making Victoria stand out among some of its peers. Plus, at a 240,000-ounce per annum production rate, Eagle should be able to operate at sub $1,125/oz AISC, which would transition it from a high-cost producer today (~$1,500/oz) to a producer with costs below the industry average.

Eagle Mine - Reconciliation & Bonus Ore (Company Presentation)

{kind=link}

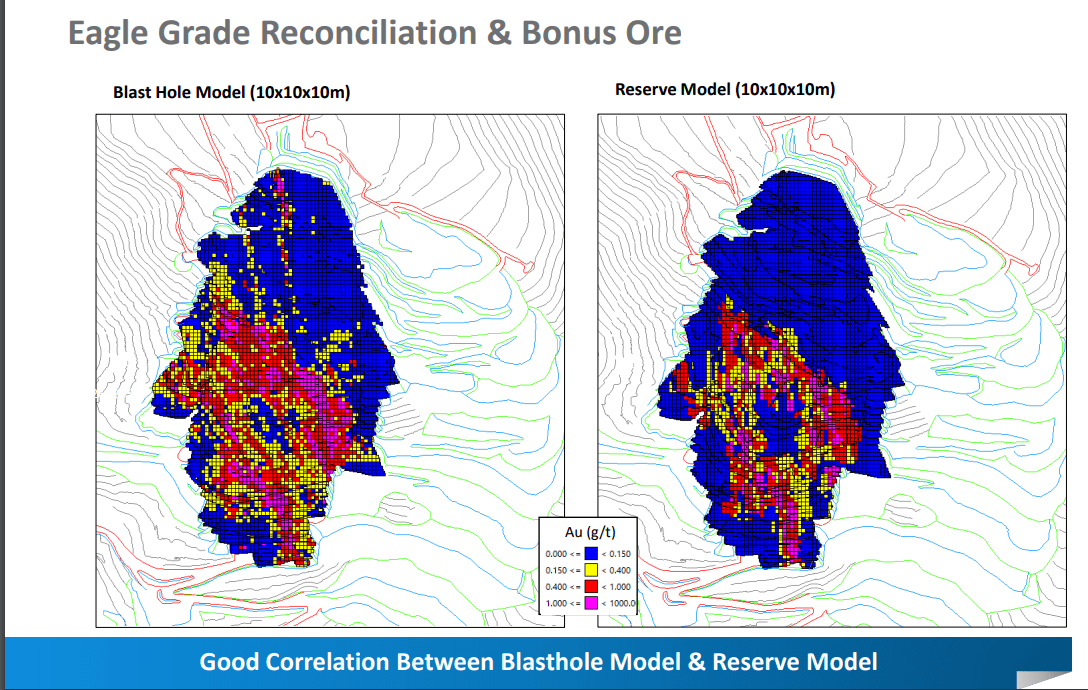

In this instance (and assuming continued exploration success), the stock might be able to reclaim its premium multiple it traded at when it first began commercial production. So, with sentiment for Victoria certainly much weaker than it was in 2020 when the stock traded above US$13.00 per share and the company benefiting from a new General Manager at Eagle, this isn't a bad turnaround story worth keeping an eye on, especially given that the Eagle Mine continues to perform well relative to projections (grade and recoveries performing to plan), which is the key to a successful turnaround (no major issues with the asset itself).

The reason is that Victoria Gold's underperformance vs. peers hasn't been so much related to disappointing results at Eagle but mostly due to extremely optimistic guidance provided by management that the company has failed to deliver to date. However, a better-capitalized operator with more experience may look at the considerable regional potential (Raven, Lynx), the likely 15+ year mine life, and the possibility for costs to consistently come in below $1,200/oz with optimization work as an opportunity to add a solid ~225,000 to 275,000-ounce per annum operation in a safe jurisdiction (Yukon).

To summarize, there are two paths to a potential re-rating, a turnaround with investors regaining confidence in this story or a takeover. Having said that, I don't see a takeover offer being as likely after the recent rally in the stock. The reason is that while Victoria isn't expensive at an enterprise value of ~$670 million, I don't see it as cheap either. Plus, most producers appear focused on returning capital to shareholders and growing off existing infrastructure, such as SSR Mining ( SSRM ) and Alamos ( AGI ) vs. acquiring. Let's take a closer look at Victoria's valuation below to see whether there's a large enough margin of safety to justify going long on the stock:

Valuation

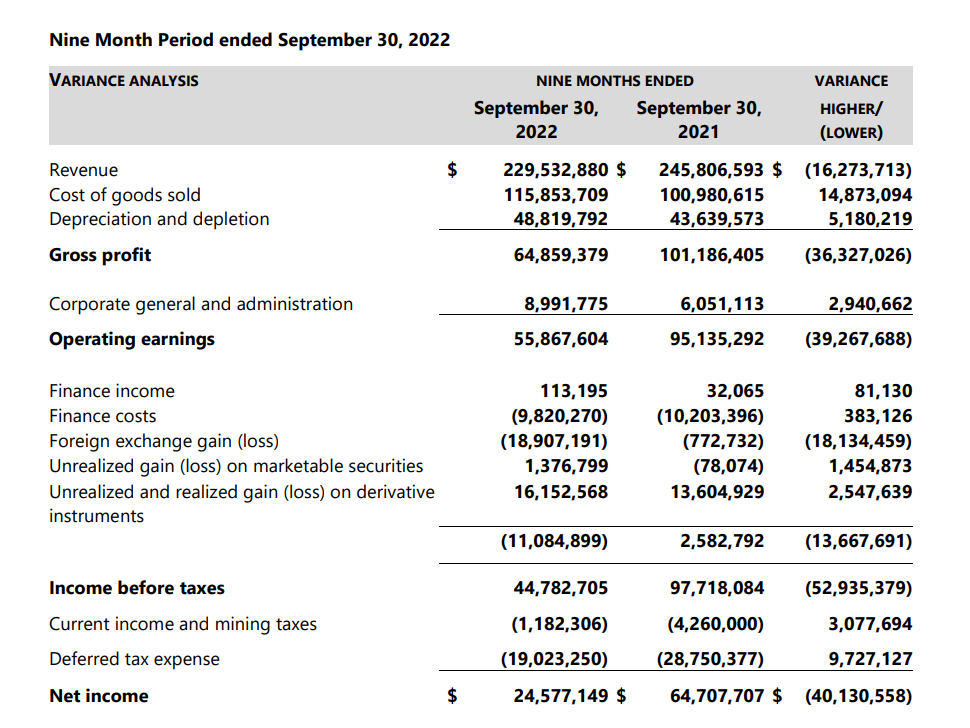

Based on ~69 million fully diluted shares (year-end 2023 estimates) and a share price of US$7.50, Victoria Gold trades at a market cap of ~$518 million and an enterprise value of ~$670 million. This is a reasonable valuation for a company with a project capable of producing 200,000+ ounces per annum in a Tier-1 jurisdiction and one with an estimated net asset value of ~US$900 million. That said, I don't think there's any way to justify a 1.0x P/NAV multiple for Victoria (given its miserable execution to date), and I think a multiple of 0.85x is more conservative. Using this more conservative multiple and after adjusting for net debt and corporate G&A, I see a fair value for Victoria of US$725 million [US$10.50 per share].

Financial Results & Year-to-Date Corporate G&A (Company Filings)

{kind=link}

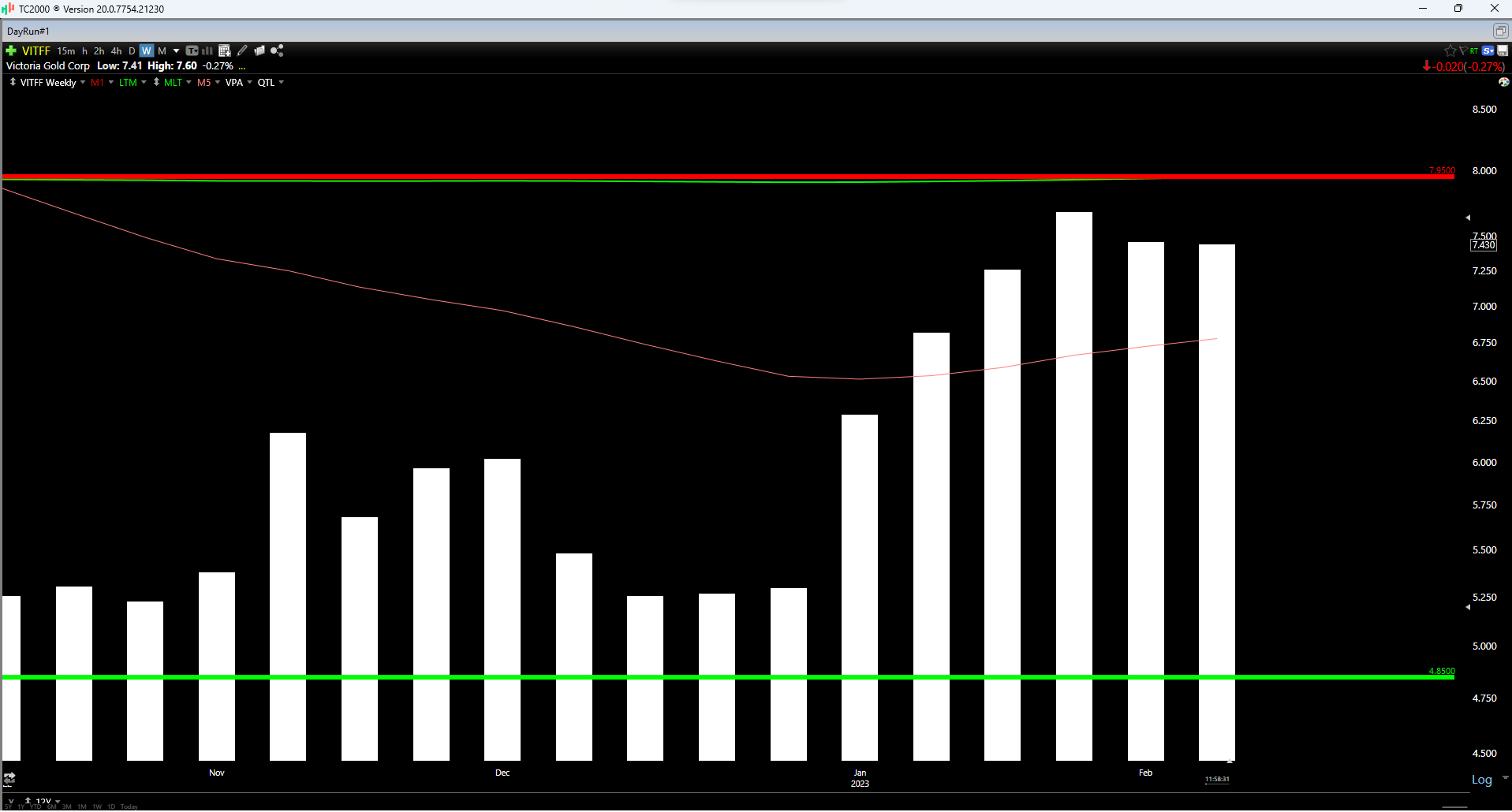

Moving to the technical picture below, Victoria Gold has strong support at US$4.85 and resistance at US$7.95, making starting new positions here much riskier (given that it's trading in the upper 10% of this range). If one was interested in betting on a turnaround in Victoria, the ideal time to buy the stock was below US$5.50, not above US$7.00, with it now more than 45% off its lows and in the upper portion of its trading range. In fact, I went long the stock on December 8th at US$5.50 and sold my position for a ~30% gain last month after the stock became extended short-term, and the easy money had been made following a sharp rally.

VITFF Weekly Chart (TC2000.com)

{kind=link}

Normally, I might consider holding my position for a larger gain. However, given that this team has struggled to execute since beginning production in 2020, I don't see any value in being greedy, and I see Victoria as a swing-trading candidate only. Hence, the mention of "three strikes, you're out" regarding the stock being investable. That said, if Victoria Gold were to slide back below US$5.50, where it would trade near support before May, I'd view this as an opportunity to start a position in the stock from a swing trading standpoint. At current levels, I don't see nearly enough margin of safety, and I think there are far safer ways to get exposure to this asset, such as Osisko Gold Royalties , which holds a 5.0% NSR royalty on Eagle.

Eagle Mine Operations (Victoria Gold Presentation)

{kind=link}

In fact, not only does Osisko Gold Royalties ( OR ) offer similar organic growth to Victoria Gold, but it has several hidden assets in its portfolio that it's receiving limited value for currently. One example is the recent ultra-high-grade lithium discovery made in northern Quebec by Patriot Battery Metals ( OTCQX:PMETF ) that could generate upwards of $1.7 billion in annual revenue by 2030, depending on spodumene prices. This could translate to annual attributable revenue of ~$24+ million per annum for Osisko Gold Royalties and upwards of $30 million at peak production, assuming 70% royalty coverage and its 2.0% NSR royalty, or ~12,000+ GEOs per annum (12% growth from current levels).

As noted above, Osisko Gold Royalties holds a massive NSR royalty on Victoria Gold's Eagle Project, with a 5.0% NSR, giving it desirable exposure to Eagle with the benefit of insulation from inflationary pressures. In the case of producers firing on all cylinders and trouncing estimates, like Lundin Gold ( OTCQX:LUGDF ), owning the producer outright and getting full exposure to the asset makes sense. However, when it comes to companies with a poor track record of execution and higher-cost mines (like Victoria Gold), I prefer to own the royalty/streaming companies as long as they provide similar growth at a reasonable price.

Osisko Gold Royalties - Organic Growth Profile (Company Presentation)

{kind=link}

In Osisko Gold Royalties' case, the stock remains attractively valued with exposure to the Eagle Mine, superior diversification, superior margins, and better shareholder returns with regular dividends and share buybacks. Hence, while I think a bet on Victoria Gold if it returns to the low end of its trading range (US$5.50 or lower) makes sense, I don't see the stock as investable at current levels, and it's tough to invest in the stock at all when it's tough to trust management guidance, and we continue to see negative surprises. Hence, my preferred way to get exposure to Eagle is through its royalty, especially with Victoria no longer offering a meaningful margin of safety after its recent rally.

Summary

Victoria Gold has had a tough two years with large guidance misses, and understandably, the market has lost some confidence in the company's ability to execute. The good news is that expectations are now low as we begin 2023, and the company is up against very easy year-over-year comps, suggesting a beat is likely this year. If I buy a turnaround story, I want a minimum 40% discount to fair value, which would require a dip below US$6.30 based on what I see as a conservative fair value of US$10.50. To summarize, I see more attractive bets elsewhere in the sector, and I don't see a favorable enough reward/risk setup to justify investing in Victoria here at US$7.50.

For further details see:

Victoria Gold: A Better Year Ahead For This Struggling Producer