VIRC - Virco Dirt Cheap And At An Inflection Point

2023-07-27 19:30:05 ET

Summary

- Virco Industries, the largest manufacturer of K-12 school furniture in the US, is set to benefit from increased school spending due to stimulus and pent up demand.

- The company's operating metrics are improving, including margins, sales, and order backlog, and it trades at a reasonable valuation of 6.4 EV/EBITDA.

- Virco's business is sticky with 80% of customers placing orders annually, and the company is well-positioned to benefit from reshoring trends and a less competitive industry landscape.

Virco Industries ( VIRC ) is the largest manufacturer of K-12 school furniture in the United States offering a variety of products from tables, chairs, and desks to storage carts. The company is vertically integrated, manufacturing furniture domestically from raw materials including wood, steel, aluminum, and plastic. They also handle site design and layout, delivery, and setup, making them a one-stop shop for school furniture needs.

Business is sticky with 80% of the customer base placing orders annually. This is in part driven by the desire for consistent design within a facility. In other words, customers don't want 4 different chair designs within a classroom. Those lasting relationships combined with a lull in school capex spending during Covid, ongoing stimulus, and new customer wins has put the company in possibly the best position they have seen in decades. The business is inflecting, sales and backlog are up, margins are improving, and trailing 12-month operating income is $13.5 million or $0.83 cents against a share price of $4.38 at this writing. The balance sheet is solid, and given a brutal 20-year stretch in the industry with competitors falling by the wayside and the ongoing reshoring trend there is enormous room for the share price to re-rate higher.

Virco:

- Stands to benefit from an uptick in school spending due to stimulus and pent up demand.

- Operating metrics are all trending up including margins, sales, and order backlog.

- Trades at a very reasonable valuation of 6.4 EV/EBITDA, a normalized trailing 12-month PE under 10 and at slightly above tangible book value.

Let's dive into a few details.

First and foremost, it is important to understand this is a seasonal business with the lion's share of deliveries happening in the warmer months when school is not in session. That means they typically make large profits in Q2 and Q3 and losses in Q1 and Q4. Given the disruption installation work represents to classrooms this makes sense. The company finances working capital needs during these peak times with a revolving credit facility from PNC bank. The facility is variable rate with rates between 7.65% and 9.75% in the most recent quarter. The only other debt is a mortgage of $4.6 million on their Conway Arkansas manufacturing facility at a rate of 4%. The balance sheet is solid with the only debt being the working capital and mortgage mentioned above. Book value is $4.11/share which does include real estate assets that may be understated on the books. They own 3 facilities in Conway Arkansas that include a total of approximately 1.8 million square feet in office, warehousing, and manufacturing space.

The real attraction here isn't bean counting of assets on the books as to me that acts as more of a floor in the case of calamity. The attraction is in the earnings and revenue inflection implying significant upside to that $0.83 cents in trailing 12 months operating income.

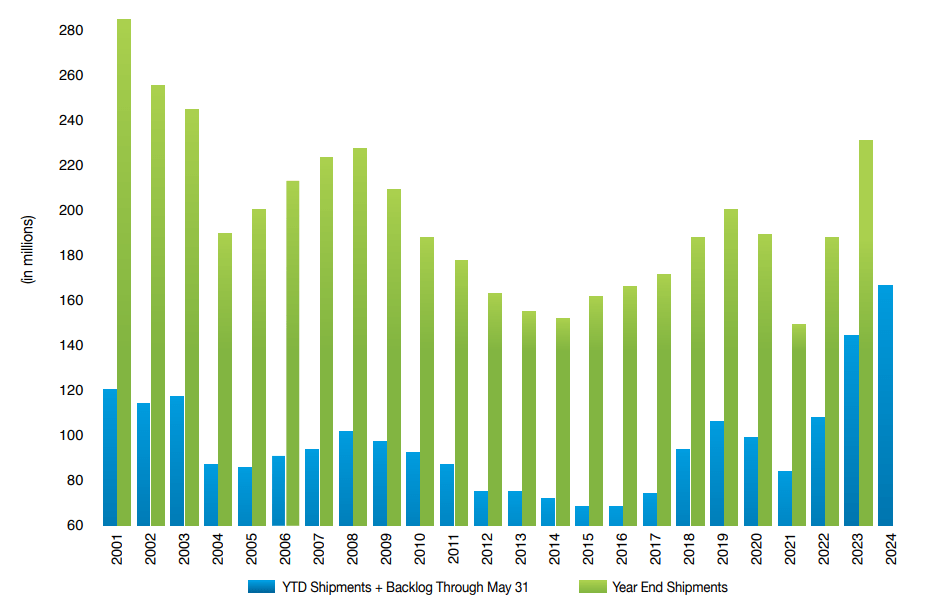

Let's start with the easy part. Order backlog is surging hitting an all-time high of $104.6 million at the end of Q1 versus $85.7 million last year a cool 22% increase. Due to the seasonal nature of their shipments the company tracks their progress in sales plus orders. As you can see from the chart below backlog is now at record levels.

{kind=link}

One note from the chart above. Historically the company had a meaningful level of sales of non-school furniture to big box stores. That is no longer the case. Those orders were generally shipped quickly and did not appear in backlog so the historical difference between backlog and full year sales has narrowed.

The latest 10-Q shows inventory has increased substantially over last year and as the company has described it.

Inventory increased by $19,343,000 at April 30, 2023 compared to April 30, 2022. The entire increase in inventory was attributable to increased quantity. The cost and valuation of inventory was stable. The quantity of inventory was increased in response to a material increase in unshipped sales orders

I think it is likely with surging backlogs that topline numbers will improve materially this year, but they look to squeeze more profit per dollar of sales compared to recent years as well.

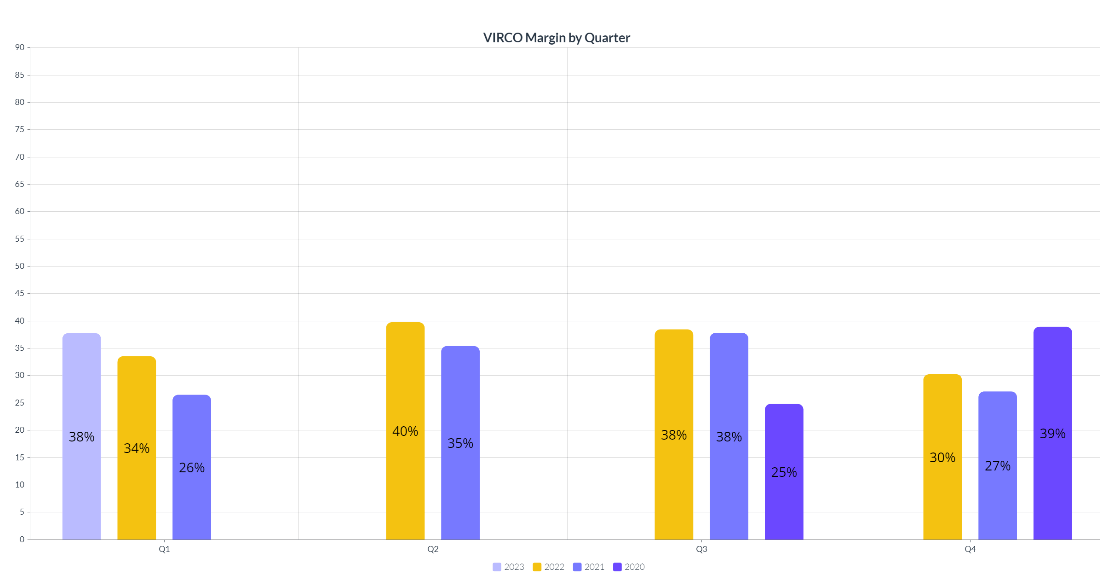

Like many companies Virco was caught a bit offside by input inflation, but price increases have now caught up lifting margins above recent levels. In addition, shipping costs have come down. I would not expect this to result in much margin upside beyond the current 39% from Q1, but it should help maintain a floor under what have been very healthy margins.

Quarterly margin comparison (Seeking Alpha Financials)

{kind=link}

Those improving margins have resulted in corresponding improvements in operating income rising from a $1.4 million dollar loss in 2021 to a $10 million dollar operating profit for the year ending January 2023 to $13.5 million for the trailing 12 months.

Going forward there are several reasons for optimism

- As manufacturing shifted to China after their entry into the WTO the industry experienced 2 tough decades. That resulted in industry consolidation, and competitors disappearing. Covid provided an additional whammy on the industry. That has left Virco as a large player in what is now a less competitive industry.

- Supply chain snags and other problems during the pandemic left many competitors struggling to deliver. Virco as a domestic manufacturer without complicated supply chains did not have similar problems. That resulted in new customer wins, and as stated earlier customers tend to stick around and reorder as there is a preference for continuity within facilities.

- As reshoring develops and becomes more prominent Virco is well positioned as an existing purely domestic manufacturer. The reliability associated with domestic manufacturing is a plus other manufacturers lack.

- The full end to end service from design to manufacture to delivery and setup is a value-added service many competitors lack.

It is difficult to estimate microcap earnings, but one could take a naive approach and assume a 22% backlog increase results in a conservative 15% topline increase over the next 12 months. That would place operating income at $15.5 million or about $0.96 cents a share all else equal. Subtract $3 million dollars in interest expense as a result of greater borrowing on the revolver to support working capital expansion, and a good base for earnings before taxes is $0.77 cents a share. Note the company is not currently paying taxes and has deferred tax assets of roughly $8 million dollars. Assuming a 25% tax rate going forward, fully taxed income in the above scenario would be $0.58 cents per share. My back of mind target here is about $7 dollars a share for a greater than 50% upside and a relatively reasonable fully taxed PE of 12 if the above assumptions are met. That number will move based on the results of operations, but given the strong financial position, and backlog providing some visibility to the revenue side I like the risk/reward.

Speaking of risks, here are a few.

Risks

- The company is highly dependent on school budgets. A drop in spending will directly impact their business. Their largest state is California who has in fact experienced budget shortfalls, although they have not fallen as heavily on education as they have other areas. While important to watch, I do think this is an area taxpayers want to spend money.

- The majority of their sales are made through a national purchasing organization. That contract runs through 2025, and while it is likely to be renewed there is a risk that if it wasn't, they would have to seek other avenues or purchasing groups for those sales.

- Changes in international trade rules could leave the company less competitive against foreign competition.

For further details see:

Virco Dirt Cheap And At An Inflection Point