VIRC - Virco Hasn't Looked This Good In Decades

Summary

- In my view, recent global supply chain disruptions were a blessing in disguise for Virco as high shipping costs improved the competitiveness of U.S. school furniture producers.

- During the first nine months of FY23, revenues rose by 32.9% year on year while the net income soared by over 900% to $12.5 million.

- The balance sheet looks much better than a year ago and I think this paves the way for the reinstatement of quarterly dividends.

- Nearshoring due to global supply chain issues could give Virco an edge over Chinese competitors in the future.

Introduction

I like to write about companies that lack coverage on SA, and today I'm taking a look at Virco Mfg. Corporation ( VIRC ). It’s a manufacturer of movable furniture and equipment that is focused on the education sector. The company has been experiencing a significant improvement in its financial results following a couple of tough years and I think the reason behind this is improved competitiveness. During the first nine months of FY23, revenues rose by 32.9% year on year while the net income soared by over 900% to $12.5 million. In addition, Virco has a strong balance sheet and I think the company could reinstate its dividend in the near future. Let's review.

Overview of the business and financials

Virco was founded in 1950 by Julian Virtue and specializes in the manufacturing and sales of school and office furniture. Its products include student desks and activity tables, school and office seating, lightweight folding tables, and upholstered chairs among others, and the company claims to be the largest producer of movable furniture and equipment for the education market in the USA (see slide 3 here ). Virco is still being managed by members of the Virtue family, and they own over 30% of the company’s stock.

{kind=link}

You can find Virco chairs, desks, and tables across a large number of school classrooms, cafeterias, and science labs across the USA. The company has sold over 65 million of its 9000 Series School Chair alone since its inception. Virco currently has two facilities with a combined manufacturing and distribution footprint of 2.3 million square feet and employs more than 800 people. About 40% of them have over 20 years of experience at Virco which I think is a sign that the work environment at the company is good.

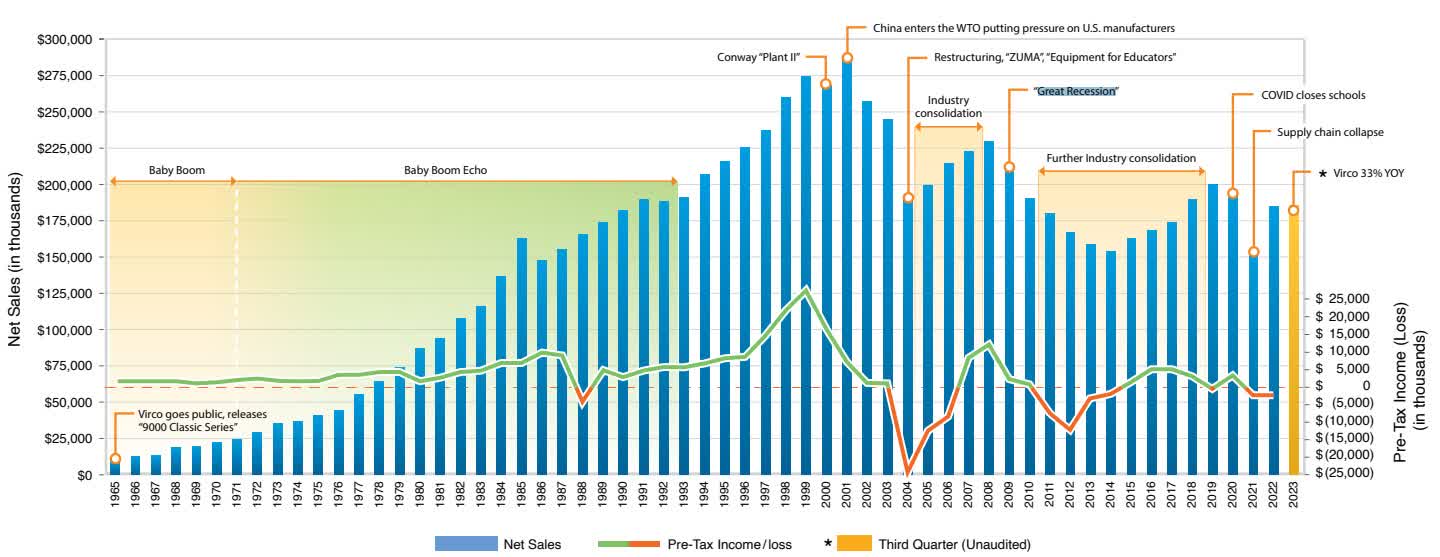

Looking at the historical financial data, we can see that Virco’s sales peaked in 2001 just as China joined the World Trade Organization. However, net income peaked in 1999 as Virco was already facing increased competition from local furniture suppliers for school and government contracts. Over the next two decades, Virco experienced sales and profitability improvements during periods of increased education spending as well as industry consolidation and paid out a total of five quarterly dividends in 2017 and 2018. However, the company's financial results over the past few years were negatively significantly affected by COVID-19 lockdowns.

{kind=link}

Yet, recent global supply chain disruptions were a blessing in disguise as high shipping costs improved the competitiveness of U.S. school furniture producers in 2022 just in time for the peak season in the summer. The vertical business model of Virco allowed it to take full advantage of the situation. Typically, about half of the company's annual sales are recognized between June and August, which means that Q2 and Q3 for its fiscal year are the strongest. The company usually books losses in Q1 and Q4.

Virco

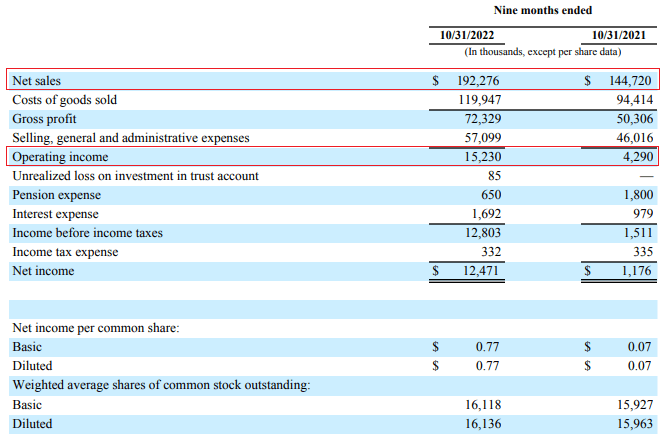

Looking at the latest available financial results, net sales rose by 32.9% to $192.3 million during the first nine months of FY23 while the operating income margin soared to 7.9% from 3% a year earlier thanks to both higher volumes and price increases. It seems the company has managed to pass cost increases to customers and it delivered and installed more than 21 million pounds of school furniture between June and August.

{kind=link}

Interest expenses increased significantly due to higher interest rates and the net debt increased to $14.7 million in October 2022 from $13.2 million in January 2022 as a result of higher receivables and inventories. Receivables rose due to the higher revenues and the company decided to boost its inventory due to supply chain issues affecting raw material supply and cash flow from operations was not enough to cover this increase. I expect the debt situation to improve over the coming months as inventories decline by about $15 million.

Virco Virco

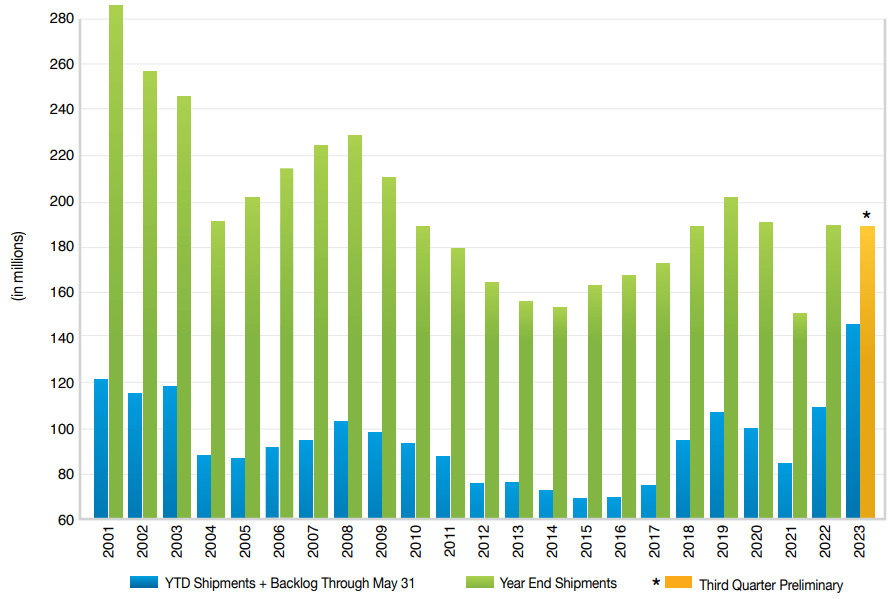

You see, Virco’s business doesn’t require a lot of CAPEX and the order backlog seems strong. Capital expenses for the first nine months of FY23 were just $2.6 million and the YTD shipments plus backlog were at the highest level the company has ever seen.

{kind=link}

While I expect sales volumes and margins to decrease eventually as shipping costs return back to historical levels, I think that an emerging trend of nearshoring of supply chains is likely to benefit Virco in the long run. In my view, the company is likely to remain profitable in FY24 and it could be debt free by the end of August or September of this year. I also expect the improved profitability to result in a reinstatement of the quarterly dividend over the coming months, which could boost the share price. Virco should report FY23 results around the end of April and I expect the company to be trading at a P/E ratio of below 7x if the share price remains unchanged until then.

Looking at the risks for the bull case, I think that there are two major ones. First, California is Virco’s largest market in terms of revenue, and potential cuts in education spending in the state could lead to a significant deterioration of FY24 sales. In January, Gov. Gavin Newsom signaled a slight decrease in funding for the state's K-12 schools and community colleges in his 2023-24 proposed budget. This would be the first cut in a decade. Second, the daily trading volume rarely surpasses 20,000 shares and this means share price volatility is usually high. In my view, it could be dangerous to start a large position as it would be challenging to exit without putting pressure on the share price.

Investor takeaway

Virco had been struggling to remain profitable for most of the past 20 years, but it seems that nearshoring due to global supply chain issues could give the company an edge over Chinese competitors. Virco had a great summer, and its balance sheet looks much better than a year ago. In my view, this paves the way for the reinstatement of quarterly dividends, and I plan to open a small position on a pullback below $4 per share. Yet, I think it could be dangerous to open a large position due to the low trading volume. I rate Virco as a speculative buy.

For further details see:

Virco Hasn't Looked This Good In Decades