VIRC - Virco Manufacturing Enjoys Temporary Tailwinds But Is Expensive

Summary

- Virco Mfg. Corp. is one of the leading school furniture manufacturers in the U.S.

- However, the company's business was taken slowly by Chinese competition for the past twenty years.

- Recent COVID-related disruptions in China, coupled with extremely high transportation prices, have caused a surge in VIRC's revenues and profitability.

- I believe the company will return to cycle average profitability without these temporary tailwinds. There are no permanent changes to the long-term trend.

- Based on cycle average earnings, the company's current market cap is too high.

Virco Manufacturing Corporation ( VIRC ) is one of the leading school furniture manufacturers in the U.S.

The company faced two decades of decreasing business because of competition from China. In the last year, profits soared as supply shortages and high transportation prices made VIRC's products more competitive.

However, I believe the company's medium-term prospects are not great. Chinese competitors do not face tariffs on furniture. Supply bottlenecks and transportation prices are decreasing.

In the long term, VIRC faces a competitive industry and is not the lowest-cost producer. Competition could also come from suppliers like Mexico or Vietnam if Chinese manufacturers were banned in the U.S. In my opinion, the company would be more interesting if it had plans to relocate production to Mexico. Also, VIRC would be more interesting if it expanded its markets, to more fully utilize its assets.

In the past, short-term profit explosions were followed by substantial share price increases and subsequent disappointment, as demand receded. I believe this time is no different.

Note: Unless otherwise stated, all information has been obtained from VIRC's filings with the SEC .

Business description

Educational furniture : Between 60% and 70% of VIRC's revenues come from a single public bid for school furniture. Although each school purchases separately, VIRC presents a unified price list to all customers.

This industry is not particularly desirable for several reasons. First, in a bid system, the lowest-cost producer tends to gain the business. Competitors have the incentive to lower margins. Second, the business is concentrated in the summer months, with 50% of VIRC's revenues generated between June and August. Third, furniture is a tradable good, meaning that VIRC competes with global suppliers.

Not the lowest-cost producer : VIRC's manufacturing facilities are in California and Arkansas. These are not the cheapest locations for mass-production products like school furniture. Particularly, American workers' wages are much more expensive than their Chinese, Vietnamese, or Mexican counterparts.

Further, VIRC has not expanded its markets outside of educational furniture effectively. If that had been the case, production would not be concentrated on a few particular months, and capacity utilization would be higher, diluting fixed overhead in more volume. Today, VIRC has to amortize its operational fixed cost in a small volume generated by school purchases.

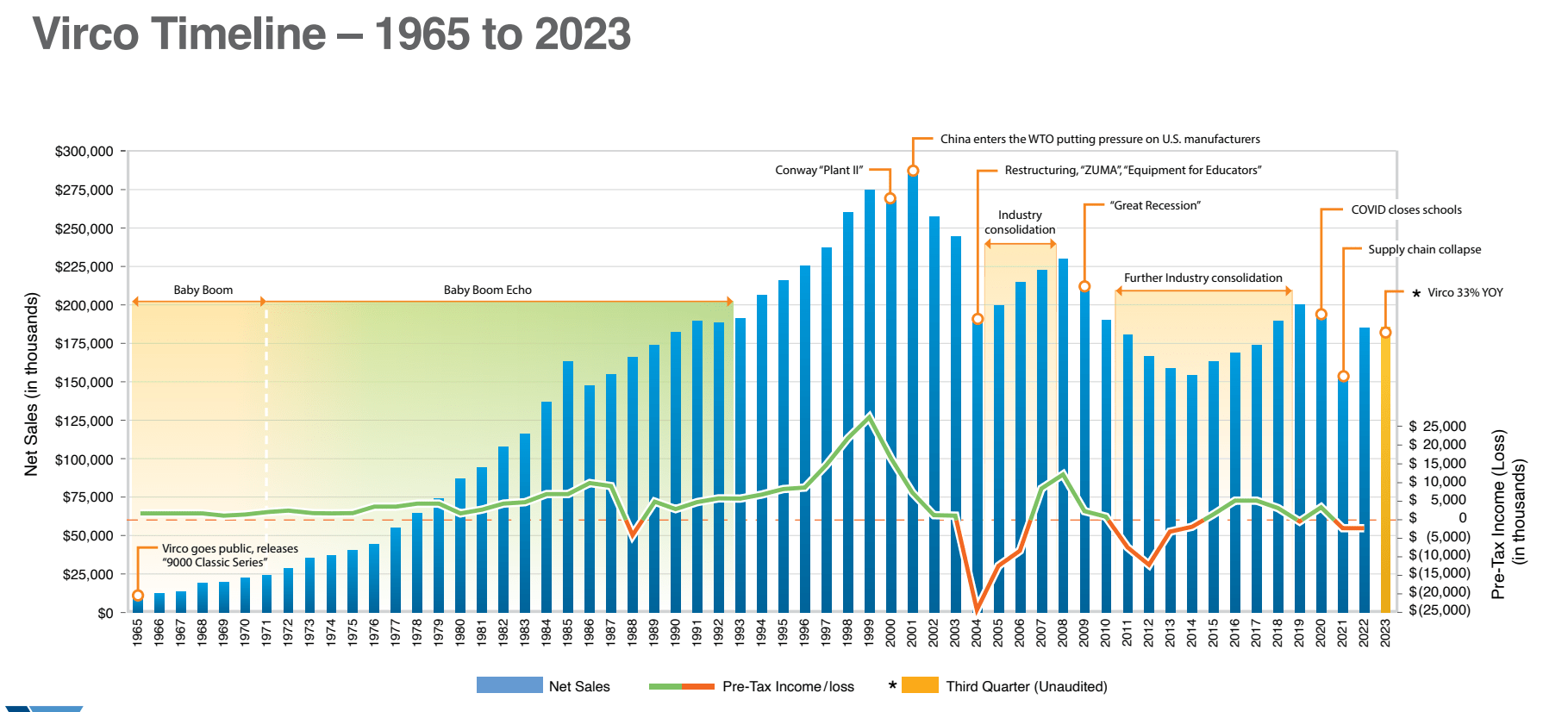

Globalization eats VIRC's lunch : Since China entered the WTO in 2001, VIRC has never reached the same level of revenues again (until 2022). As the magnificent timeline from the company's investor presentation below shows, VIRC revenues and profits also became cyclical after the introduction of Chinese competition.

VIRC's revenue and profitability historic timeline (VIRC's investor presentation)

{kind=link}

Operational leverage : Cyclicality is compounded by the operational leverage of three manufacturing facilities in the U.S. The chart below shows part of that leverage. Comparatively small changes in revenue generate enormous changes in operating profits. The same phenomenon can be appreciated from the second chart, showing volatile and low operating margins.

Recent developments

Revenue and profit explosion : VIRC's revenues exploded in 2022. As of October 2022 (3Q23) , the company's revenues are up 30% on a YoY basis, both at the quarter and 9M cumulative level. But the true magic occurs at the bottom line. Thanks to VIRC's operational leverage, the company's net income is up more than 1000% on a 9M basis and 600% on a quarterly YoY basis.

Short-term complications with Chinese competition have caused this increase in revenue and profitability. First, supply chains in China were delayed or completely halted by COVID-related lockdowns that started at the beginning of March 2022 . One of the most affected areas was the Guangzhou metropolitan area, which includes Foshan, China's furniture manufacturing center.

Second, seaborne transportation costs quadrupled between 2021 and 2022 and only started receding after the second half of 2022. Because furniture is bulky, transportation costs affect its competitiveness more. This came together just at the beginning of the 2022 school purchasing season, between June and August.

Sustainability

The four most dangerous words in investing: 'This time is different'. I believe that this time is no different.

VIRC's business is cyclical : The charts below show that VIRC has already passed through operating profit cycles, caused by unsustainable demand increases. Further, each previous cycle was accompanied by subsequent share price increases, leading to disappointment.

China is not disappearing : No tariff is imposed on Chinese furniture in the U.S., which could provide a long-term advantage to U.S. manufacturing. The recent lack of competitiveness was caused by COVID lockdowns (unlikely to repeat consistently) and high seaborne transportation prices.

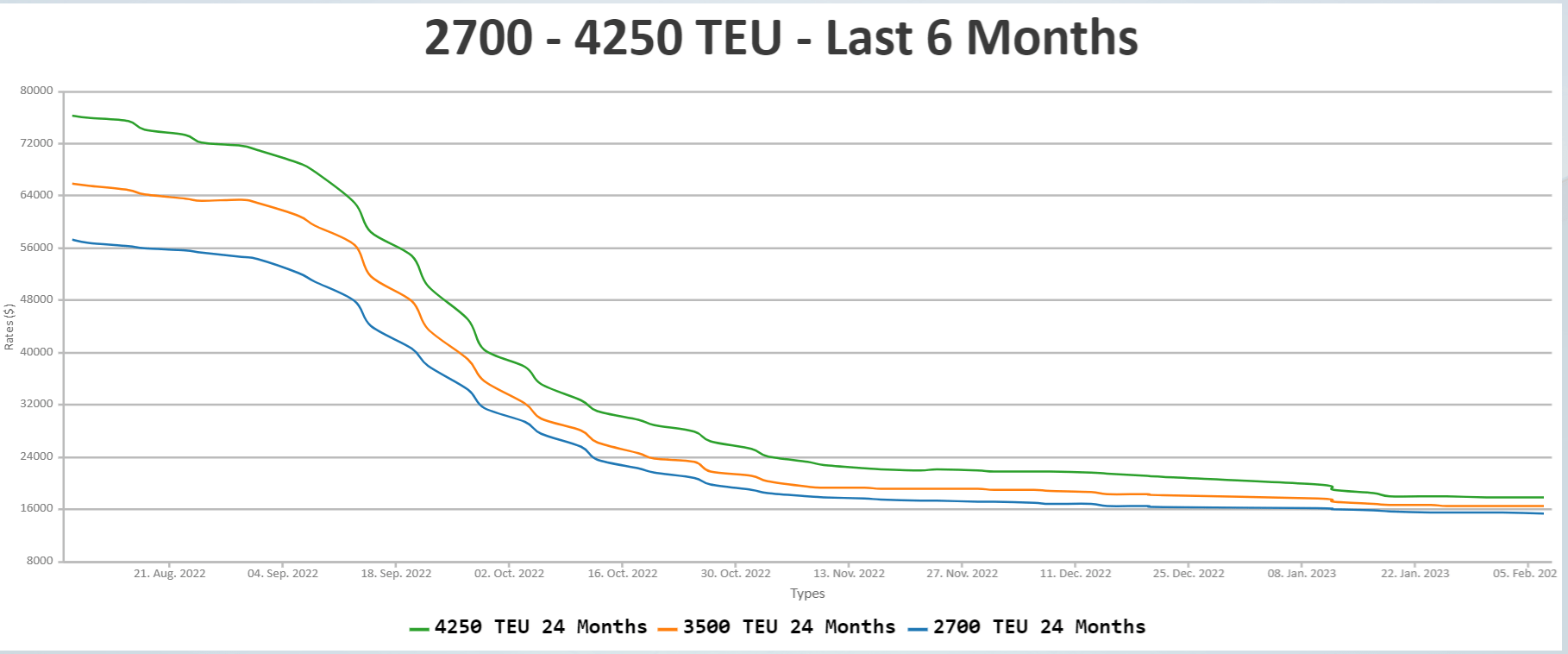

Transportation prices are down : Container ship rent prices are today less than 25% of what they were merely six months ago. The most important cost barrier to Chinese competition is gone.

Container ship rent costs per day (New ConTex indexes, VHBS)

{kind=link}

Other countries can compete : Even if Chinese manufacturing was banned in the U.S., other countries could compete with VIRC on a cost basis. Countries like India, Mexico, and Vietnam could have even higher cost advantages than China, whose low-cost working class is becoming more expensive.

Possible positive developments

These are not strategies commented on by management, but rather developments that would make me reconsider my long-term evaluation of VIRC.

Moving is difficult : VIRC's management has mentioned no plans to move manufacturing capacity to Mexico. The southern neighbor is an interesting manufacturing hub because it is very close, has free trade agreements in place with the U.S., and is labor cheap on a global basis.

However, even if the company decided to move part of its manufacturing to Mexico, the process would take years and be costly. VIRC has 800 full-time employees in the U.S.

Expanding the line : Given that VIRC mentions that 70% of its revenues come from school furniture from a single bid and that 50% of its revenues are generated in the summer months from school orders, there is an opportunity to increase production serving other markets. If the company utilized its assets and employees more, it could lower the portion of those fixed costs that are embedded in each product's price, therefore gaining competitiveness.

Valuation

Cycle average earnings : For the reasons exposed above, I believe that a gauge of VIRC's true long-term profitability is its cycle average earnings. The average operating income, starting from the cycle's peak in 2007, is $2 million. Starting from the peak in 2016, the average comes to $2.7 million.

Even without considering debts or taxes, those average seems low compared to the company's current $80 million market cap. If we subtract interest charges averaging $1.5 million, and taxes of 21%, the overvaluation is even more pronounced.

Conclusion

VIRC competes in a difficult market where the price is king, against some of the lowest-cost producers on earth. This dynamic has eaten the company's profits for almost two decades.

The recent divergence from that long-term trend has not been caused by permanent changes in conditions (new barriers to imports, new cost efficiencies in the company), but rather by temporal barriers to foreign supply, namely COVID in China and extremely high transportation costs.

I believe that once these two barriers are removed (and they have been for the most part), VIRC will lose part or all of the market share that it gained in the past year and a half. This has already happened in the past, with cyclical movements of profits and stock prices.

When valued using cycle averages of profitability, VIRC's current $80 million market cap seems very high.

For further details see:

Virco Manufacturing Enjoys Temporary Tailwinds But Is Expensive