VIRC - Virco: Strong Q3 2024 Results But Good Times Unlikely To Last (Rating Downgrade)

2023-12-12 20:59:19 ET

Summary

- The company’s net sales grew by 8.9%, and the operating income margin soared to 17.5%, which surpassed my expectations.

- In addition, Virco announced a $5 million share buyback and the reinstatement of quarterly dividends.

- However, I think it is as good as it gets, as the company is likely to come under pressure from Chinese competitors over the coming years once again.

- In my view, Virco is starting to look expensive, and the share price could be back to around the $4.00 mark by this time next year.

Introduction

I've been following US school furniture maker Virco Mfg. Corporation (VIRC) closely and so far, I've written 3 articles about it on SA. The latest of them was on October 10 when I said that it could be a good time for investors to trim or close positions as the company no longer looked cheap from a fundamentals standpoint. The market capitalization had declined by over 10% by December 7 but it has shot up by over a quarter since then on the back of strong Q3 FY24 financial results. In my view, Virco is starting to look overvalued and I’m cutting my rating on the stock to sell. Let’s review.

Overview of the Q3 FY24 results

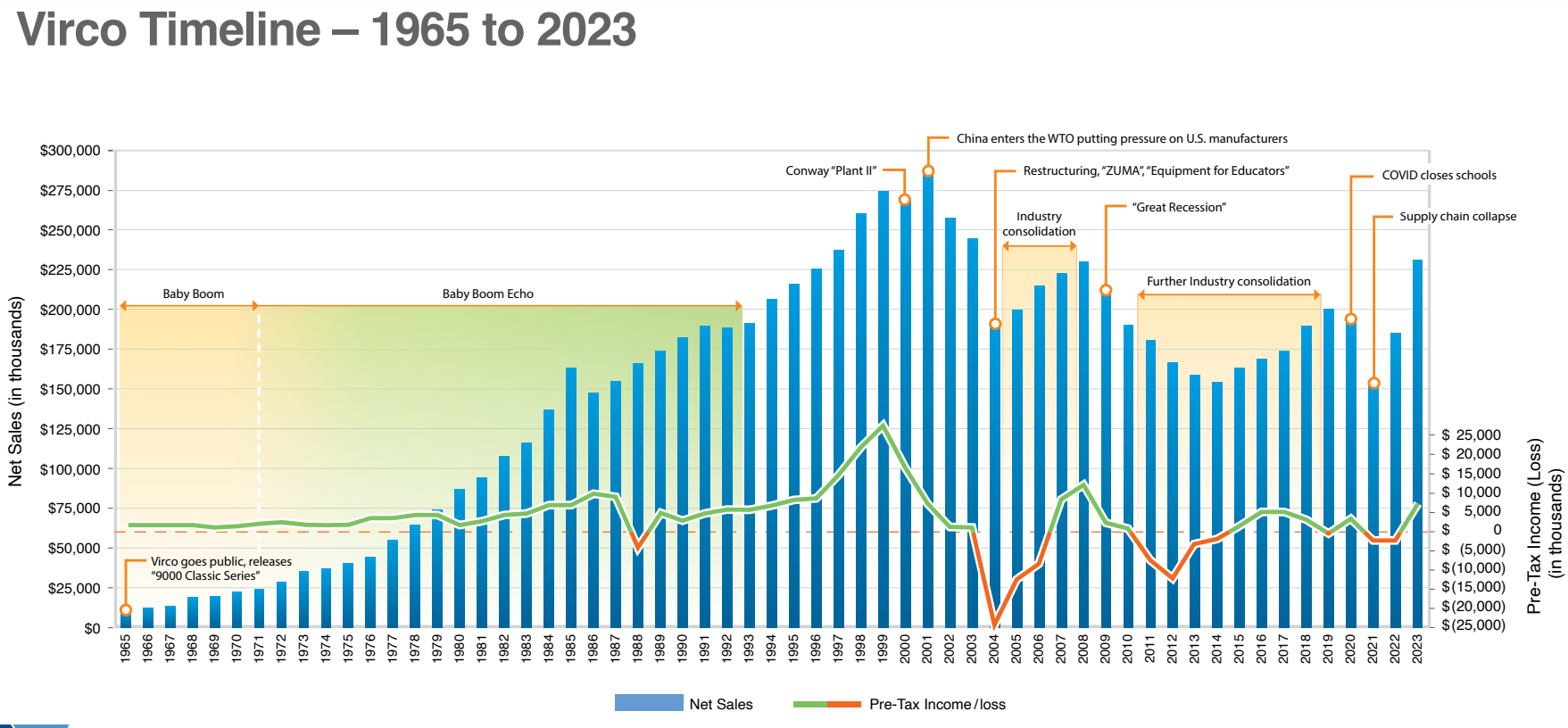

If you aren't familiar with the company or my earlier coverage, here's a brief description of the business. Virco was founded in 1950 and specializes in the manufacturing of school and office furniture. Its product offering features chairs, desks, and tables, with its most recognizable product being the 9000 Series School Chair – more than 65 million units of those have been sold in the USA since 1965. Virco has two manufacturing facilities and around 800 full-time employees. This is a seasonal business, with around half of annual sales being generated in June, July, and August as schools in the USA typically buy new chairs and desks during the summer break. The majority of orders usually come around 4-6 weeks before the selling season. Due to the seasonality, Q3 of the fiscal year is usually the strongest while losses are booked in Q1 and Q4.

Virco

In October, I said that net sales for Q3 FY24 could be slightly weaker compared to a year earlier as the backlog of unshipped sales orders was at $74 million as of July 31 (see page 20 here ), down by $7.2 million year on year. In light of this, I was surprised to see that net sales for Q3 FY24 rose by 8.9% to $84.3 million. The operating income margin, in turn, soared to 17.5% from 11.4% thanks to economies of scale as well as lower raw materials costs.

{kind=link}

Virco surpassed my expectations for the quarter and the share price also got a boost from two shareholder-friendly announcements with the release of the quarterly results - the reinstatement of a quarterly dividend and an open market share repurchase program. The company will start paying a quarterly dividend of $0.02 per share and plans to buy back shares for up to $5 million.

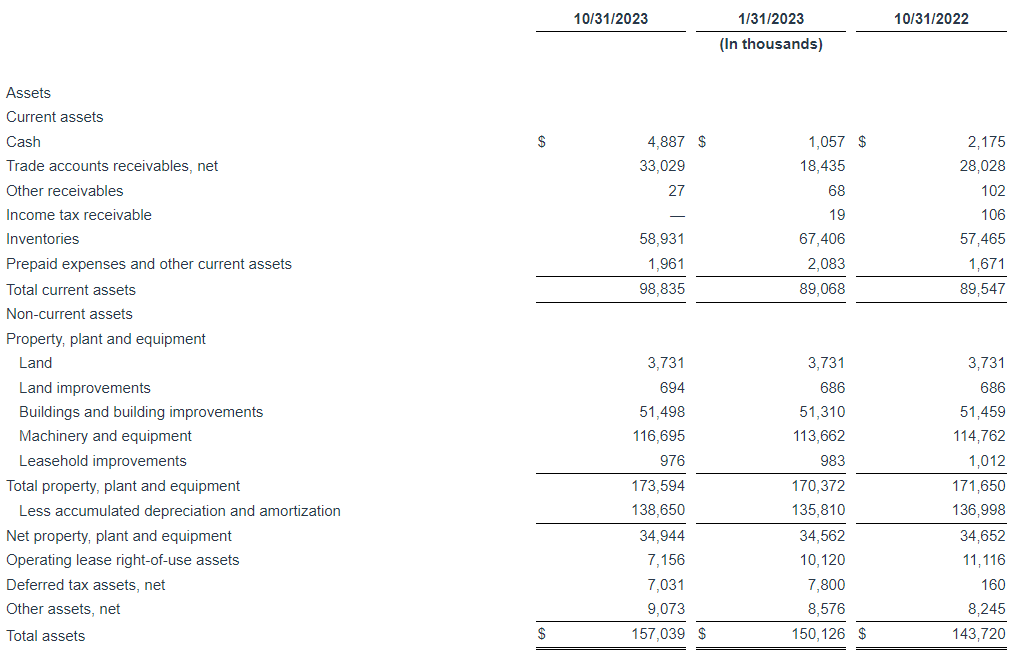

Looking at the balance sheet, net debt was down to $3.3 million from $44.9 million at the end of July as trade accounts receivable went down by $35.6 million quarter on quarter to $33 million. Back in October, I predicted receivables to be down to about $30 million at the end of Q3 FY24. Overall, the balance sheet of the company is in better shape compared to October 2022 when net debt was $9.8 million.

{kind=link}

{kind=link}

Overall, I think that Q3 FY24 was stronger for Virco than many investors expected and the dividend and share buyback provided a further boost for the share price. That being said, I think this is as good as it gets for shareholders as the next two quarters are usually loss-making and there are cracks forming below the surface. You see, the backlog of unshipped sales orders stood at $42.5 million as of October 2023, which is $2.3 million lower compared to a year earlier (see page 20 here ). In my view, Q4 FY24 net sales could be around the $35 million mark while the operating loss is likely to surpass $6 million. This would put the net income for the full fiscal year at around $17 million. While a forward P/E ratio of 8.7x doesn’t seem high, I doubt that this strong financial performance is sustainable. You see, Virco’s business got a strong boost for FY23 and FY24 from global supply chain disruptions as they put significant pressure on Chinese competitors. In the years before that, the company was struggling to keep up with low costs from imports and I expect this to gradually become the norm again over the coming years.

{kind=link}

So, how do you play this? Well, I think the best course of action for risk-averse investors is to avoid Virco stock. That being said, short selling seems like a viable idea as data from Fintel shows that the short borrow fee rate is just 2.54% as of the time of writing. There are about 1.2 million shares available for short selling and the short squeeze risk seems low as the short interest is just 0.39% of the float.

Looking at the upside risks, I think the most significant one is that aggressive share buybacks on the open market could further boost the share price over the coming months. While the daily trading volume over the past few months has typically been over 100,000 shares, it used to rarely surpass 20,000 shares before September 2023. If the trading volume dries up once again, share buybacks could account for a major part of it in the future. Other risks here are that the reinstatement of the dividend could attract more investors or that I’m being overly pessimistic about the financial performance of the company in Q4 FY24. Sure, the order backlog in October was weaker than a year ago but we saw the same for Q3 FY24.

Investor takeaway

Virco posted solid results for Q3 FY24 and announced a share buyback as well as the reinstatement of quarterly dividends. However, I’m concerned that the order backlog is lighter than a year ago and that the company is likely to come under pressure from Chinese competitors over the coming years once again. In my view, net sales and operating income are likely to decline in FY25 and the share price could be back to around the $4.00 mark by this time next year. I think risk-averse investors should avoid this stock.

For further details see:

Virco: Strong Q3 2024 Results But Good Times Unlikely To Last (Rating Downgrade)