VIRC - Virco: Time To Take Profits (Rating Downgrade)

2023-10-10 05:17:04 ET

Summary

- Virco had strong peak summer season with net sales rising by 29.6% and operating net income soaring by 90.2% to $21.3 million in Q2 FY24.

- I expect Q3 FY24 to be softer in terms of sales compared to Q3 FY23 due to the weaker order backlog.

- Virco is trading at an EV/EBITDA ratio of 5.6x on a TTM basis and I think this could be a good time for investors to trim or close positions.

- The good news seems fully priced into the share price, and I doubt the coming fiscal years will be as strong as Chinese competition intensifies once again.

Introduction

US school chair and desk producer Virco Mfg. Corporation (VIRC) is on my watchlist and I've written two articles about the company on SA so far. The latest of them was in June, when I said that I expected the strong backlog and high inventory levels to enable Virco to book operating income of over $25 million in Q2 and Q3 FY24.

Well, it seems that I might've been too conservative as the company announced on September 11 that it seems that I might've been too conservative as the company announced on September 11 that operating income for Q2 FY24 alone came in at $21.3 million , almost double the amount from a year earlier. Yet, I think that the company is no longer cheap from a fundamentals standpoint as the market capitalization has increased by almost 80% since my previous article and the share price is above the $5.99 target that I set. In my view, this could be a good time for investors to trim or close positions and I'm cutting my rating on the stock to neutral. Let's review.

Overview of the Q2 FY24 financial results

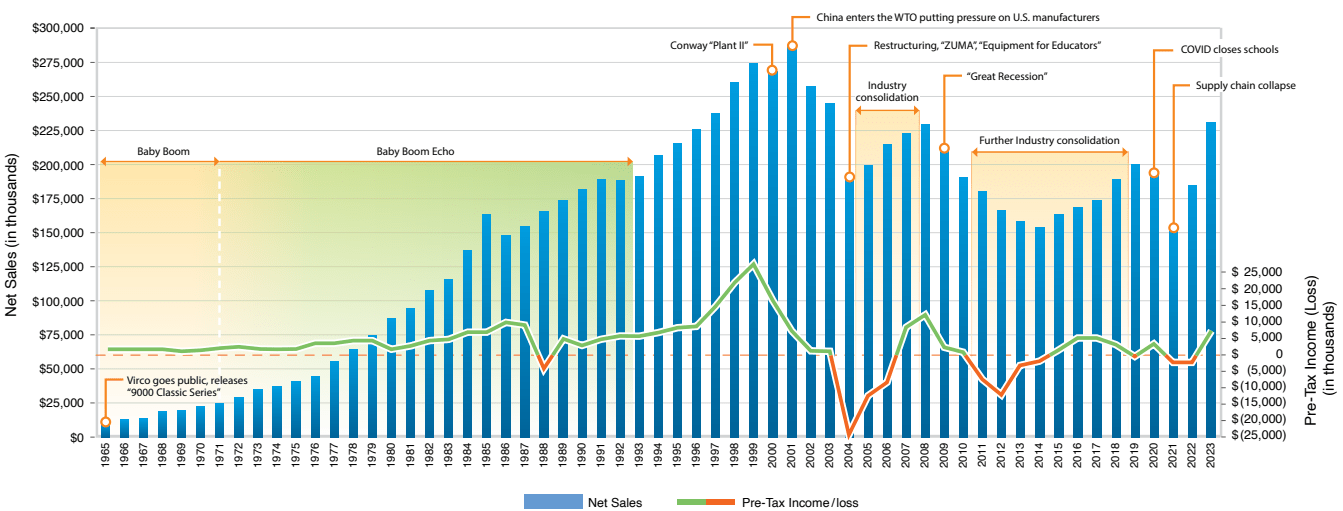

In case you're not familiar with Virco or my earlier coverage, here's a short description of the business. The company was established in 1950 by Julian Virtue and focuses on the production of school and office furniture. This includes chairs, desks, and tables and if you've gone to school in the USA, it's likely you've sat in a Virco chair at some point as the company has sold over 65 million units of its 9000 Series School Chair since 1965. Today, Virco is the largest producer of movable furniture and equipment for the education market in the US (see slide 3 here). It has two production facilities with a combined manufacturing and distribution footprint of 2.3 million square feet and some 800 full-time employees. The company is still run by the Virtue family, whose members own more than 30% of its shares.

Virco

As Virco focuses on the school market, its business is highly seasonal - about half of annual revenues are booked in the months of June, July, and August as this is when educational institutions typically replace chairs and desks before the start of the school year. The period between peak orders and peak deliveries is just four weeks and the company's facilities are specifically designed to support extreme throughput during the peak summer season. Virco's cash collections thus peak in late summer and fall and the company typically books losses in Q1 and Q4 of its fiscal year. In my view, the orderbook at the end of Q1 of the fiscal year is a good indicator for the strength of the peak summer season and my expectations for this year were high considering the backlog of unshipped sales orders stood at $104.6 million as of April 30 compared to $85.7 million a year earlier (see page 17 here ).

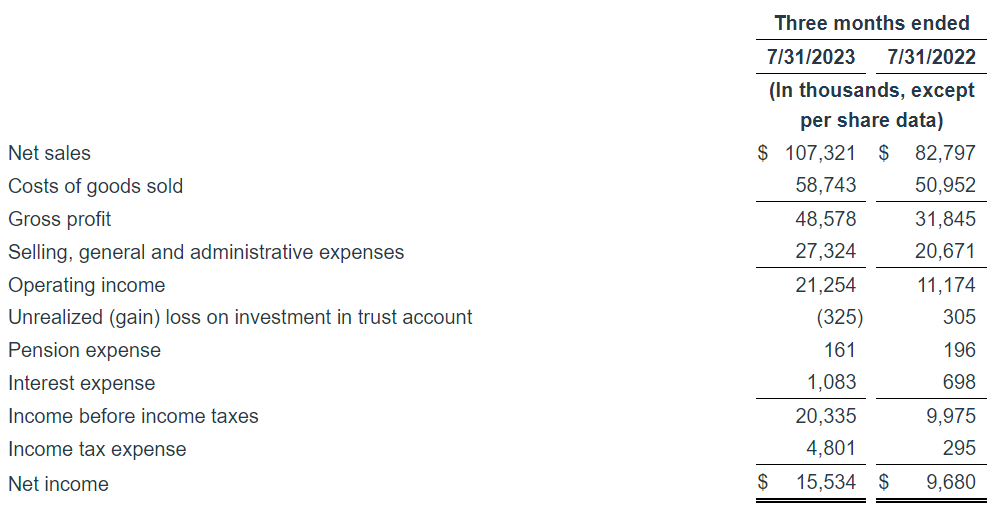

Well, Virco released its Q2 FY24 financial results on September 11 and I think they were very good as net sales rose by 29.6% year on year to $107.3 million while the gross margin for the quarter rose to 45.3% from a year earlier due to moderating raw material costs and improved operating efficiencies. The operating income, in turn, soared by 90.2% to $21.3 million thanks to economies of scale as well as price increases.

{kind=link}

Yet, I think that Q3 FY24 could be slightly weaker in terms of net sales compared to Q3 FY23 as the backlog of unshipped sales orders was at $74 million as of July 31 (see page 20 here ). This is $7.2 million lower than a year earlier, and I expect Q3 FY24 net sales to stand at around $70 million, with a net operating income of about $9-$10 million. This would bring the operating net income for Q2 and Q3 FY24 to just above $30 million, which is higher than my previous estimate of $25 million.

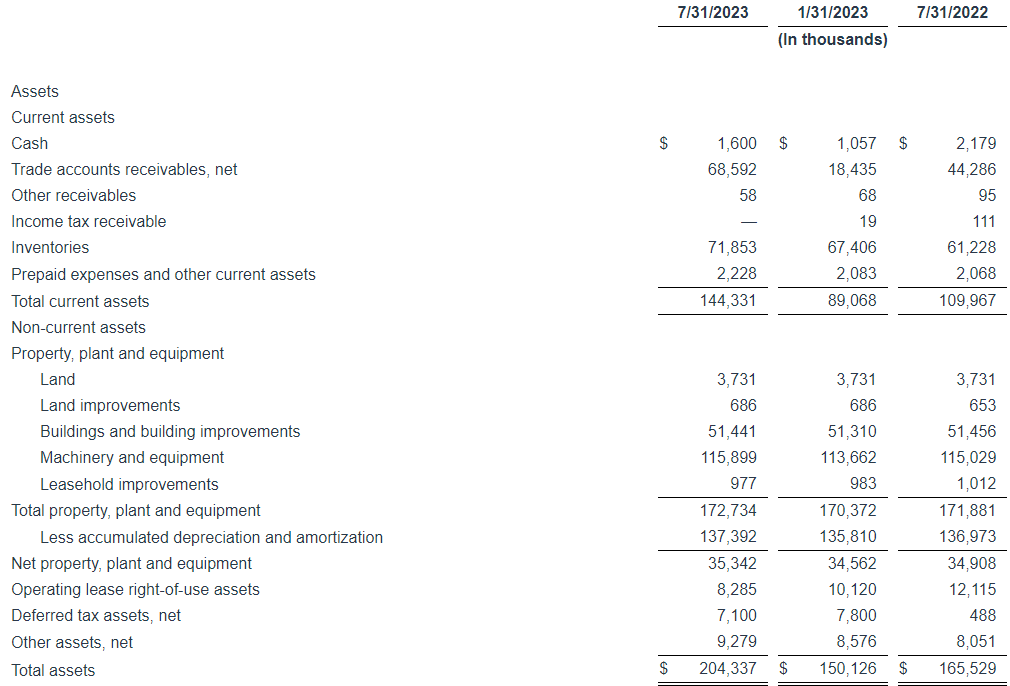

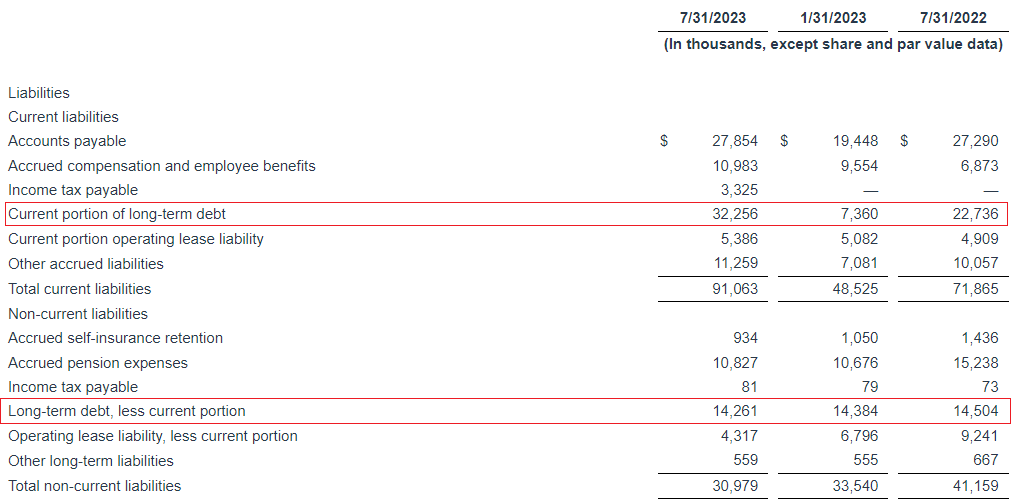

Turning our attention to the balance sheet, total assets were above $200 million as of July 2023, which is an unusually high level and the main reason behind this was the higher trade accounts receivables due to the strong sales in Q2 FY24. I expect receivables to be down to about $30 million at the end of Q3 FY24. Overall, I think the balance sheet is strong as net debt stood at $44.9 million at the end of July. I expect this level to decrease almost to zero in Q3 FY24 as receivables decline. The Q3 FY24 results should be released around the middle of December.

{kind=link}

{kind=link}

Turning our attention to the valuation, Virco has an enterprise value of $164.1 million as of the time of writing, and the TTM EBITDA stands at $29.1 million. This puts the EV/EBITDA ratio at 5.6x on a TTM basis. You could also argue that this is a seasonal business and therefore if the net debt is wiped out in Q3, the EV/EBITDA ratio could be down to around 4.1x (market capitalization divided by TTM EBITDA). While both levels might seem low at first glance, I think that Virco is starting to become expensive. You see, FY24 is shaping up as Virco's strongest fiscal year in a long time due to supply chain disruptions suffered by Chinese competitors early in the 2023 calendar year, and I doubt that the coming fiscal years will be as strong. Competition from China is likely to be back to previous levels in FY25, putting pressure on sales and margins once again, and I think that Virco shouldn't be trading at above 5x EV/EBITDA (with the current net debt).

{kind=link}

Investor takeaway

Virco experienced a strong peak summer season with an operating income of $21.3 million in Q2 FY24 alone. While I expect Q3 FY24 to be softer in terms of sales compared to Q3 FY23 due to the weaker order backlog, I think the company is on pace to surpass $30 million in operating income for the two quarters. That being said, the good news seems fully priced into the share price, and I doubt that the coming fiscal years will be as strong as Chinese competition heats up once again.

For further details see:

Virco: Time To Take Profits (Rating Downgrade)