SPY - Virtus Investment Partners: More Downside Risk Ahead

Summary

- Continued strong headwinds will drive investors and savers away from financial markets, resulting in reduced demand for wealth management services and increased risk of asset impairment.

- Under such conditions, Virtus Investment Partners, Inc. is unlikely to post better financial results than the first three quarters of 2022, which were not positive at all.

- Virtus Investment Partners pays a decent dividend, so holding shares is fine, but poor growth prospects make adding shares to positions too risky at the moment.

Still Too Risky to Rate Virtus Investment Partners, Inc. Higher than Hold

2022 will certainly not be remembered as one of the easiest years for U.S. exchange operators. Market valuations of companies listed on U.S. stock exchanges faced severe headwinds due to macroeconomic and geopolitical issues.

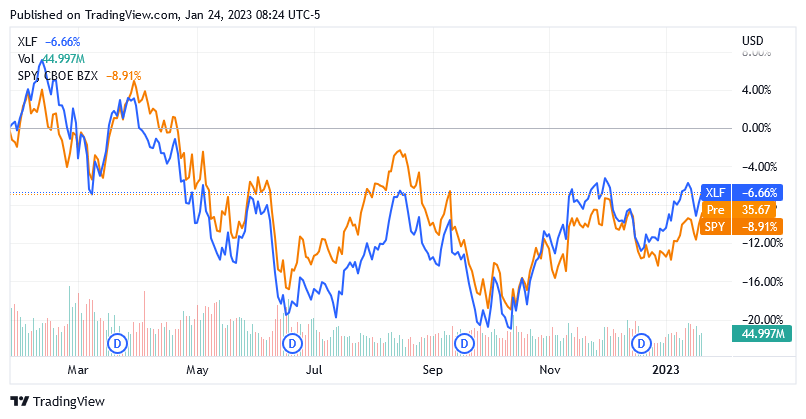

The SPDR S&P 500 Trust ETF ( SPY ), the index that aggregates large U.S.-listed stocks, is down 9% over the past 12 months, which has certainly not been well received by asset managers, as investing in U.S.-listed stocks is a relevant source of income for these companies.

{kind=link}

As a result, Virtus Investment Partners, Inc. ( VRTS ) can currently not be rated higher than a Hold rating.

Strong macroeconomic and geopolitical headwinds will alienate investors and savers from financial markets, leading to downward pressure on demand for wealth management services and an increased risk of asset impairment.

Under such conditions, Virtus Investment Partners, Inc. and other investment managers are unlikely to post better financial results (mainly in terms of Asset Under Management ("AUM"), sales, and earnings) than they did in the first three quarters of 2022.

With Asset Under Management, sales, and earnings being the primary drivers of Virtus Investment Partners stock prices, Virtus shares will struggle to get the right boost for the much-coveted recovery.

How Virtus Investment Partners Performed Through the First Three Quarters of 2022

Virtus Investment Partners has received lower investment management fees as assets under management have declined due to people's lower confidence in financial markets amid high levels of uncertainty and instability.

These two elements, which are still dominant, were introduced by high inflation, partly due to the energy crisis and partly due to increased government spending on arms, and central banks' monetary tightening, which has fueled recession fears to combat runaway inflation.

This was the common thread of the first 3 quarters of 2022, causing the following negative changes in adjusted diluted earnings per share.

After a 13% sequential decline in adjusted diluted earnings per share to $6.86 in the second quarter of 2022, Virtus Investment Partners reported another sequential decline in adjusted diluted earnings per share, but this time on a higher scale of 16% to $5.76 in the third quarter of 2022.

Driven largely by a lack of certainty about companies' future earnings and cash flows, bearish market sentiment in 2022 first spread among retail investors, who are much less risk-prone than institutional investors given the limited resources available, and then affected institutional investors as well. Bearish market sentiment then spread among institutional investors, who lost faith in analysts' forecasting models amid exceptional headwinds such as the war in Ukraine and record inflation not seen in over 40 years.

Virtus Investment Partners reflected the negative market sentiment, reporting a 16% sequential decline in total revenue to $7.9 billion in the second quarter of 2022 and a higher 28% sequential decline to $5.7 billion in the third quarter of 2022. The declines were observed in almost all investment strategies.

Net cash flows from Virtus Investment Partners funds improved slightly to -$3.3 billion in the third quarter of 2022 from -$4.8 billion in the second quarter of 2022, but were still worse than -$2 billion in the first quarter of 2022.

Redemptions weigh heavily on open-end funds whose outflows are not offset by institutional positive net inflows, which likely failed in global real estate, global equity and domestic equity mandates.

Not only have publicly traded equities faced headwinds that have plunged market valuations around the world, but 2022 has also proven to be a very challenging year for the housing market, one of the toughest in a generation.

Assets Under Management by Virtus Investment Partners Could Continue to Be Weighed Down by Many of the 2022 Negative Factors

Many of the adverse factors that have hampered market performance and net flows of assets under management by Virtus Investment Partners could continue to impact the overall market value of investments the firm manages on behalf of retail and institutional investors.

Inflation above 2% could stay with us for most of 2023, with the possibility of further rate hikes by the Federal Reserve in the first half of the current year. As long as the system continues to create jobs while the Fed's policy calls for a deterioration in employment levels as a signal to ease tight interest rate measures, the rate hike policy will likely remain in place.

Additional recession signals from the Fed will inevitably impact the unemployment rate, as more companies like Amazon, Twitter, Tesla, Google and Microsoft decide to cut jobs drastically. A higher unemployment rate will hamper consumption, which will ultimately translate into lower sales and margins and disrupt corporate growth programs. This inevitably impacts companies' future earnings or cash flows, and because of their heightened uncertainty, investors will be highly conservative in determining their present value as a measure of the stock's intrinsic value.

Cash is now very expensive, and investors have no incentive to use it to fund investments in publicly traded stocks, which may remain overvalued despite last year's loss.

Furthermore, higher interest rates undoubtedly favor investments in fixed-income securities, as these become more attractive than gold bullion, which, in contrast, does not yield any returns. However, if there is a consensus that bonds will be in high demand as interest rates rise, this should be reconsidered given the strong U.S. dollar currency appreciation. Gold's downtrend from early March 2022 to late October 2022 may not exactly indicate a burning passion for fixed income assets. Since gold currently has its main opponent in the U.S. currency, the decline follows the loss of the precious metal’s attractiveness in favor of the U.S. dollar, which, on the contrary, has managed to appreciate remarkably.

All these headwinds are likely to further fuel investors' risk aversion and keep them away from financial markets, which could potentially continue to weigh on the overall value of Virtus Investment Partners' assets under management.

Total assets under management decreased 6.7% sequentially to $145 billion in the third quarter of 2022 after a 15.2% sequential decline to $155.4 billion in the second quarter of 2022.

The Stock Valuation

Based on the observations in this analysis, Virtus Investment Partners, Inc. is unlikely to expect any good performance in the period ahead.

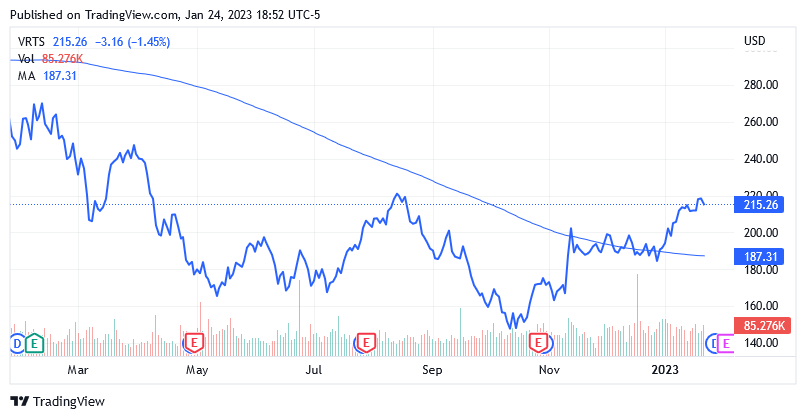

After rallying for the past 3 months, the stock has reached valuations that are inconsistent with the outlook, and there is a real risk of being caught in the nets of a significant loss, should market sentiment turn bearish.

The stock appears to be recovering like most of the market, but the storm may not be over yet, as the factors that caused 2022's severe headwinds still pose downside risks.

Shares traded at $215.26 apiece for a market cap of $1.58 billion as of this writing.

{kind=link}

Shares are trading significantly above the long-term trend of $187.31 and well above the middle point of the 52-week range of $141.80 to $273.03.

Virtus Investment Partners pays quarterly dividends, and the next of $1.65 per share will be issued on February 15, 2023. The payment results in a forward dividend yield of 3.02%, which is above the market's average S&P 500 dividend yield of 1.67% as of this writing.

Virtus Investment Partners, Inc. currently has a Hold rating because it pays dividends, while poor growth prospects make it too risky to add shares to positions.

If the market behaves rationally and takes business developments into account, it's easy to expect downward pressure on the stock. The irrational part of the market will respond to comments from central bank policymakers who from time to time allay recession fears.

But central banks have always said they expect payroll data to worsen before easing measures. Given what multinationals have done so far in terms of job cuts, there are signs the next recession could be a deep one. This could sound like a big surprise to the markets and potentially lead to significant share price declines.

In addition, there is the war in Ukraine with all its economic risks that the market cannot ignore or perhaps try to convince that the risks have already been anticipated and thus overcome. War is a very extraordinary event with unpredictable scenarios.

The war in Ukraine and its devastating effects on the economy are not likely to end anytime soon, as France and Germany will be sending tanks to Kyiv and the U.S. and UK have pledged military support to Ukraine, while Russia will certainly not stand by but will receive support by the geopolitical coalition of countries closest to President Vladimir Putin's regime.

Conclusion

Virtus Investment Partners, Inc. has not fared well in 2022, as high inflation, higher interest rates, and risks of recession weigh like boulders in financial markets and explain last year's share price drop.

Because some of these headwinds could continue to weigh on the company's business and possibly its stock price, it would be best not to go beyond a Hold rating with Virtus Investment Partners, Inc.

Currently, macroeconomic issues and geopolitical tensions determine the persistence of significant downside risks.

For further details see:

Virtus Investment Partners: More Downside Risk Ahead