CA - Vista Gold: Attractive Valuation But No Clear Path To A Re-Rating

2023-06-04 03:59:01 ET

Summary

- Vista Gold has underperformed the GDXJ in recent years, impacted by inflationary pressures that have made projects more costly to build and impacted expected operating margins.

- Meanwhile, it's a competitive environment for juniors with only a few potential suitors left to transact given the number of deals we've seen.

- So, although VGZ is attractively valued, there's no clear path to a re-rating, and with the potential for further share dilution this year, I see better bets elsewhere.

Vista Gold ( VGZ ) is one of the better-performing precious metals stocks this year, up 20% year-to-date vs. a 5% gain for the Gold Juniors Index ( GDXJ ). However, this has followed two years of severe underperformance, with Vista Gold ("Vista") down 34% and 30%, respectively, in 2021 and 2022, declining at a pace that was nearly double of the smaller-cap gold mining benchmark. As detailed in past updates, I attribute the underperformance to inflationary pressures that have made projects more costly to build and dented expected operating margins. And this was in addition to producers trading down to their most attractive levels in years during Q3 2022, making it harder to justify owning higher-risk, non-revenue generating developers.

{kind=link}

Mt. Todd Project (Company Website)

As it stands today, the valuation gap between developers and producers has widened considerably, with several producers over 50% off their Q3 2022 lows and some developers continuing to scrape along the bottom of their bases with no real upside traction in their share prices. That said, developers continue to be inferior from a risk-adjusted basis, they're not paying shareholders to wait (dividends and or buybacks), and while inflation has cooled, it still hasn't been stamped out, with some gold producers like Gold Fields ( GFI ) expecting mid single-digit inflation this year. And while VGZ has offered a look at what a lower-capex/staged Mt. Todd Project could look like, it's a competitive environment with several developers to choose from, but many inching closer to the finish line while Vista treads water. Let's look at recent developments below:

All figures are in United States Dollars unless otherwise noted.

Inflationary Pressures

As discussed in a previous update on Vista, there was no disputing that the company had a solid project with scale (~480,000 ounces of gold per annum), a Tier-1 jurisdiction (Northern Territory, Australia), and reasonable upfront capex (~$1.07 billion inflation adjusted assuming 20% cost creep vs. Q4 2021 cost estimates), but the path to a re-rating was not clear, and I didn't see it as a top takeover target. The reason? From a re-rating standpoint, Vista did not have the capitalization to support a large-scale or staged development of Mt. Todd, with a market cap to initial capex ratio below 0.10 to 1.0, and despite an updated study, the initial capex estimates still looked stale at ~$900 million, suggesting an even lower market cap to initial capex ratio, which made pursuing the project near impossible without a sale or partner. Plus, from an operating cost and NPV (5%), these figures looked stale as well, with higher upfront capex, sustaining capital and per tonne costs likely to degrade the ~$1.0 billion NPV figure ($1,600/oz gold price).

Since these updates, we've seen a few major deals in the sector, with Gold Fields snapping up half of the high-grade Windfall Project in Quebec, and B2Gold ( BTG ) acquiring Sabina to control a major gold belt in Nunavut. Both companies were among my top-5 takeover targets given that they benefited from industry-leading grades and 55% estimated AISC margins ($2,000/oz gold price), making them highly attractive for suitors in an environment where cost profiles were increasing. And while Vista's Q4-21 study pointed to decent AISC figures ($930/oz), these costs were arguably stale when we've seen 12% plus cost inflation since Q4 2021 for producers, and many Feasibility Studies underestimate costs by 5% plus. Hence, a more conservative AISC figure for Mt. Todd might be $1,050/oz which doesn't do as much to improve margins for a major producer vs. projects like Windfall, Sabina, and Great Bear ( KGC ).

The good news is that inflationary pressures appear to be cooling off based on sector-wide commentary on Q4/Q1 Conference Calls, and the double-digit inflation experienced in 2022 appears to be in the rear-view mirror. However, inflation is still here to stay and it continues to look like we'll see a minimum of 20% plus cost inflation on 2021 projects that begin construction in 2024 or later, suggesting that while the massive Mt. Todd Project held by Vista in the Northern Territory of Australia is attractive, it's only getting more expensive to build it. And at the same time, the landscape is quite competitive, especially with De Grey Mining ( OTCPK:DGMLF ) unveiling a mammoth-sized project with lower capex estimates, a larger production profile, and a more attractive cost profile, also available in a Tier-1 jurisdiction, in the Pilbara Region of Western Australia.

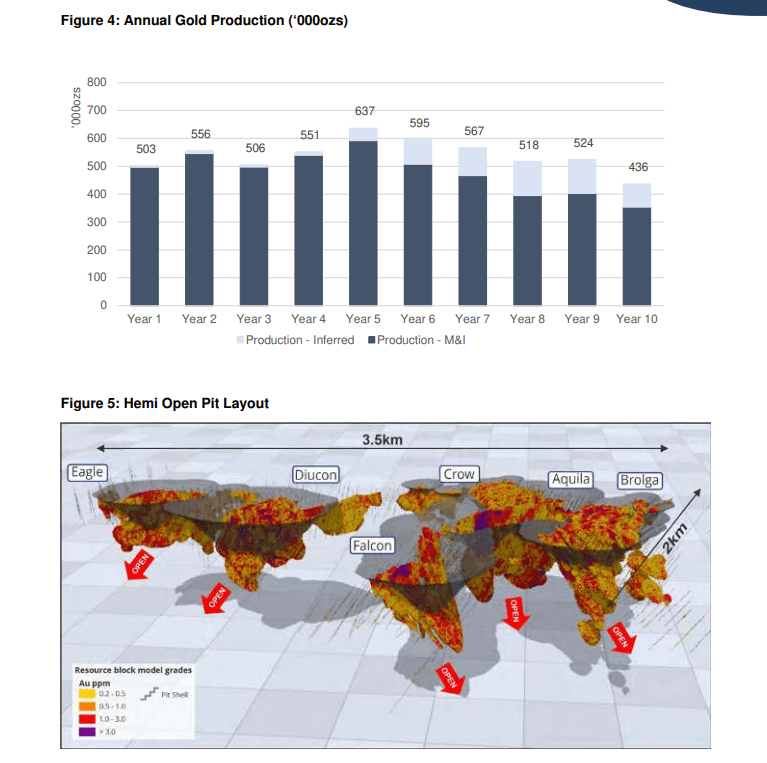

De Grey Mining's Mallina Project (Hemi plus regional) is expected to produce ~540,000 ounces over the first ten years at sub $900/oz costs and upfront capex of ~$900 million (assumes 20% inflation vs. estimates) with more updated costing estimates vs. Vista's Q4 2021 study, benefiting from a smaller plant (10 million tonnes per annum vs. 18.2 million tonnes per annum), higher grades (1.6 grams per tonne of gold vs. 0.90 grams per tonne of gold) and slightly higher recoveries (93.6% vs. 91.9%).

{kind=link}

De Grey Mallina Project Production Profile (De Grey Mining)

Obviously, the fact that a new mega project has shown up in Australia that's been advanced to PFS level doesn't mean that suitors will suddenly ignore Mt. Todd, but there is a proverbial new game in town when it comes to ~500,000 ounce undeveloped projects in Australia with sub $1.0 billion capex, and De Grey's Mallina offers a much higher After-Tax NPV (5%) of an estimated ~$1.50 billion (even incorporating some inflationary pressures) at a constant $1,600/oz gold price vs. Mt. Todd's estimated NPV of ~$850 million at $1,600/oz (adjusting for inflationary pressures). So, from a takeover standpoint and if suitors are looking to go shopping in Australia, I would argue that De Grey Mining offers the more attractive project and one that's more defensive against secular bear markets in gold given its significantly higher grades and better margins.

So, what's changed?

Given that many larger producers appear more gun-shy when it comes to mega projects ($800+ million in capex) in the current inflationary environment, Vista has provided insights into what a smaller-scale project could look like, and noted that at a 15,000 tonne per day throughput rate, the project could be built for less than $350 million with annual production of 150,000 to 200,000 ounces with higher all-in sustaining costs. I would argue that a "sub $350" million capex bill looks a little ambitious if we incorporated Q4 2022 cost estimates and a 2024 build start (even with the benefit of sunk costs/contract mining), and I think $360 - $370 million is probably more conservative, with Ikkari's upfront capex estimated at ~$400 million even with a 3.5 MTPA plant. That said, even if we give the benefit of the doubt at this sub $350 million figure for Mt. Todd 5k TPD, all-in sustaining costs would increase materially with Mt. Todd lacking economies of scale, meaning it would stack up unfavorably vs. other mid-sized undeveloped projects like Blackwater, Valentine, and Ikkari from a margin and payback standpoint.

The benefit of a smaller project is that it may appeal to more suitors, these suitors could look at a staged build, and it's still a solid operation with AISC likely to come in below the estimated industry average of ~$1,310/oz. That said, I don't see this smaller-scale scenario that's being offered up as a game-changer for Vista, and unlike Blackwater which is being built in an inflationary environment with the benefit of a scaled approach, Vista still can't finance the project on its own, whether it's a 50,000 tonne per day or 5,000 tonne per day operation. Therefore, although the company may get more interest from suitors at sniffing around the project, this is not a catalyst that would serve as a re-rating for the stock. However, in unrelated news, we have seen some encouraging developments, with the possibility of a lower royalty rate for Northern Territory projects, that would apply to Mt. Todd.

As noted in Vista's April update the Northern Territory Government's report offered a series of recommendations to make the Northern Territory more appealing from an investment attractiveness standpoint, with the possibility of a royalty rate of sub 5.0% that would be more competitive relative to other Tier-1 jurisdictions. If passed, this would be positive for Mt. Todd and would potentially increase interest in the project from suitors, with the current royalty structure being quite cumbersome under the NT Mineral Royalty Act 1982, especially when combined with additional royalties that will be paid to the Jawoyn Association Aboriginal Corporation [JAAC]. As shown below, the Northern Territory Royalty plus JAAC royalty would combine for $800+ million over the life of mine at a $1,600/oz gold price.

{kind=link}

Mt. Todd Financial Analysis (Mt. Todd TR)

Mt. Todd Financial Analysis (Mt. Todd TR)

Valuation & Competitive Environment

Based on ~120 million shares and a share price of US$0.60, Vista Gold trades at a market cap of $72 million, making it one of the cheapest developers in the market today, especially if we adjust for those holding upwards of 5.0 million ounces of gold resources. That said, this share count figure is a moving target that is hard to rely on, with barely $5.0 million in cash expected as of the end of Q2 2023 unless we see further sales under its At-The-Market equity program (~$453,000 raised in Q1 2023). Given that I would expect the company to want to maintain a cash balance of at least $4.0 million and a likelihood of raising a minimum of $4.0 million this year, I think a more conservative share count to use is 130 million shares, placing Vista's valuation at ~$78 million. This is still a very reasonable valuation, and there's no disputing that Vista remains cheap, but we could see pressure on the stock from ATM sales if the company doesn't go the route of a small capital raise.

{kind=link}

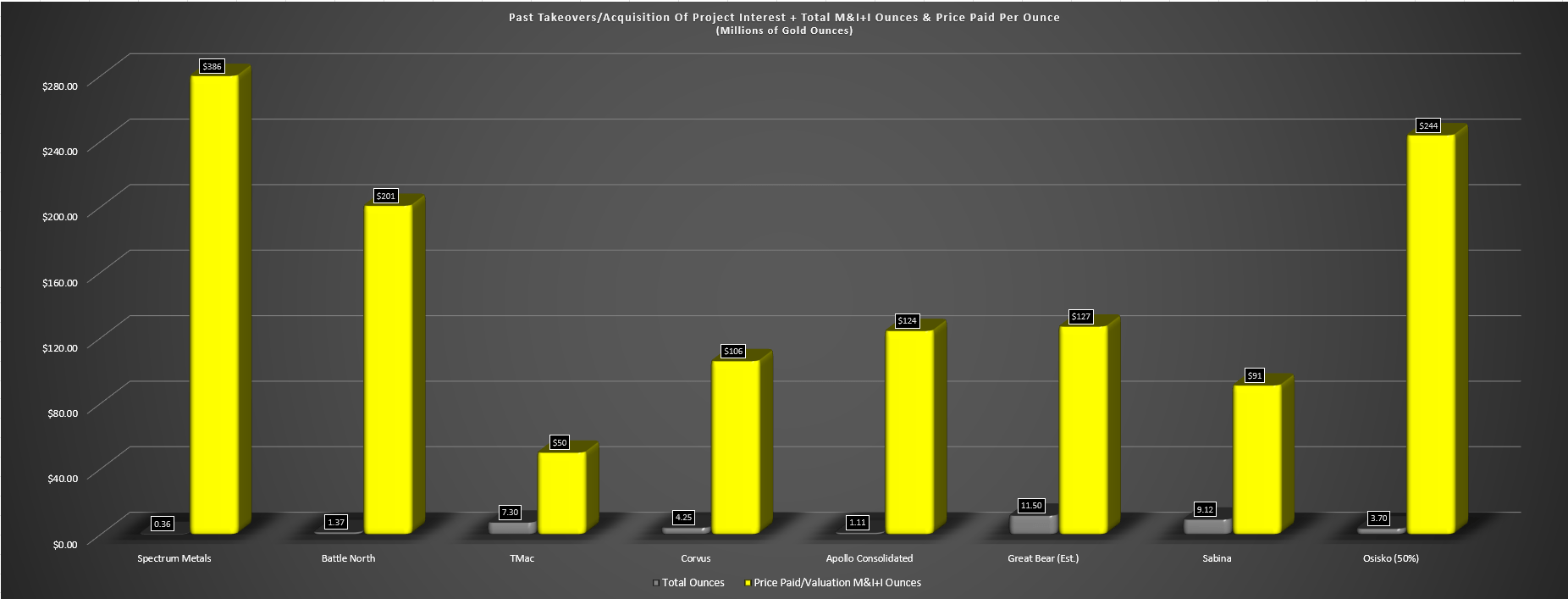

Past Takeovers/Acquisition of Project Interest - Total M&I+I Ounces & Price Paid Per Ounce (Company Filings, Author's Chart)

On valuation alone, Vista might seem like a no-brainer investment, trading at $11/oz on proven & probable reserves, a fraction of what suitors have paid for Tier-1 jurisdiction gold projects over the past few years (~$166/oz for resource ounces, not reserves). That said, there has been a theme to past takeovers, with suitors looking for two things, and sometimes both at once. This has been ounces that are higher grade than the industry average for their respective project types, and or the ability to leverage off existing infrastructure. The former attribute is clear in the acquisitions of the Penny West Project, the acquired interest in Windfall, the acquisition of Back River, the acquisition of Great Bear, and the acquisitions of TMac Resources and Battle North (both high-grade mines), which came with sunk costs given that they had mills and infrastructure in place.

In the latter case, several assets benefited from the ability to provide feed sources to existing mills, with Penny West material able to be trucked to Mt. Magnet, the ability for Evolution ( OTCPK:CAHPF ) to add a mill/resources in the Red Lake region with Bateman, the ability for AngloGold ( AU ) to add strategic resources west and south of Silicon with Corvus Gold. To summarize, even where grades were only slightly above grade (Corvus' grades were better than average heap-leach assets, but not Long Canyon caliber, Bateman's grades were good for underground assets, but not world-class at ~7.0 grams per tonne of gold), there was a strategic fit to the company to consolidate a land position and also get high-margin ounces.

I don't see Mt. Todd fitting this theme, with average grades for an open-pit asset and it being too low grade to justify trucking material and leveraging off another mill to reduce capex. And even with a staged operation that can be built in phases, this may open Vista up to more potential suitors, but there's no shortage of ~150,000 ounce per annum assets available, and there are arguably more attractive projects from a margin standpoint. So, I still don't see Vista being a top takeover target given that it's not high-margin enough to stand out (15k TPD), and it's a hefty capex bill (50k TPD) for most suitors to considering pursuing in an inflationary environment when there are other higher-margin assets already in the portfolio of producers capable of building a project of Mt. Todd's size that can be built/expanded (Red Chris Block Cave, Wafi-Golpu, Havieron, Canadian Malartic, Fourmile, Silicon/Beatty District, San Nicolas, Great Bear).

{kind=link}

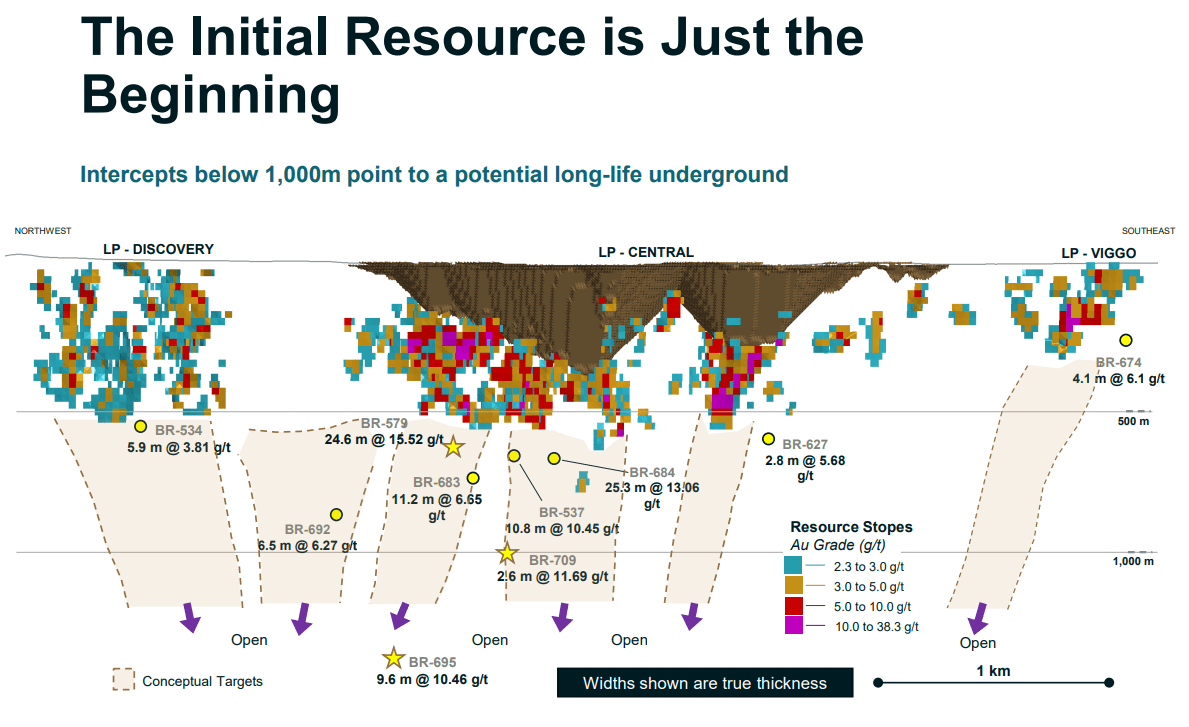

Great Bear Project - Kinross (Kinross Presentation)

This doesn't mean that Vista won't be acquired. I could certainly be wrong and I've been wrong before. However, if I'm going to invest in the developer space which carries higher risk, I prefer to bet on the most robust projects that have the highest likelihood of being taken over, such as past top ideas like Corvus Gold, Sabina Gold, Mariana, and others. And while Vista has done a solid job advancing this project while maintaining a tight share structure and is working hard to realize value for its shareholders, I continue to see better setups elsewhere in the sector on a risk-adjusted basis. Plus, while Vista is cheap on a P/NAV standpoint, several other developers are inching closer to their first gold pour and significant free cash flow generation, so on a blended forward 2-year cash flow and P/NAV basis, others remain more attractive, with Marathon offering a near ~30% FY2025 free cash flow yield.

Summary

Vista Gold has opened itself up to more potential suitors by looking at a 15k TPD scenario, and the strength in the gold price has certainly improved sentiment, even if is this partially offset by sticky labor inflation in prolific jurisdictions, and continued inflation in some consumables. Plus, it's positive to see the company working to reduce cash burn while it looks for a partner or suitor at Mt. Todd. That said, I see a high probability of further share dilution in the next 18 months with the dwindling cash position, and while VGZ is attractively valued, I don't see a clear path to a re-rating and it continues to be a waiting game for investors. So, while it's better positioned with it not needing a partner to commit to a multi-billion capex bill and more with potential partners vs. NovaGold ( NG ), I see it in a similar position with it not controlling its own destiny, hence I continue to favor other names in the developer space.

For further details see:

Vista Gold: Attractive Valuation, But No Clear Path To A Re-Rating